Angel investors are continuing with their undeterred investments in the Egyptian startup ecosystem. Kashat, a Cairo-based fintech startup which just launched out in 2020, has secured an undisclosed amount of funding from Cairo Angels, a global network of angel investors targeting startup opportunities in Egypt, the Middle East and Africa. Kashat’s expansion will be aided by the investment.

Sumair Farooqui, Founder of Kashat.

“We are grateful to Cairo Angels for putting their trust and faith in our mission and becoming part of our journey. We are excited to enter the next phase of our growth where we will continue to innovate to deliver solutions that help enhance opportunities for our users to be included in the wider financial system of Egypt,” stated Sumair Farooqui, Founder of Kashat.

Why The Investors Invested

“We are pleased to have closed this investment round, which is the largest investment in Cairo Angels’ history. Kashat has been recognized as one of the top Fintech players, having launched a unique product that caters to the Egyptian market’s needs. We are confident in the Kashat team’s ability to succeed in the Egyptian market and beyond,” said Aly El Shalakany, Chairman of the Cairo Angels.

Cairo Angels, which is a group of angel investors recently launched a new $3 million micro fund to invest in early stage startups’ seed and pre-Series A in the Middle East and Africa region, with a major focus on Egypt and Saudi Arabia. One of the leading and oldest angel networks of the region, Cairo Angels has been actively investing in Egyptian startups.

Kashat, the first Nano lending mobile application in Egypt, was created by Sumair Farooqui and Karim Nour and offers short-term loans ranging from 200 EGP to 1500 EGP with a repayment plan of up to 61 days.

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

The heads of medium to large organisations have a very specific and all-embracing role to play. Peter Drucker, modern business futurist, said it best in 2004: “The CEO is the link between the Inside that is ‘the organisation,’ and the Outside of society, economy, technology, markets, and customers.”

Francois Kriel, Director at Kriel & Company

It’s a wide-angle lens role that is bestowed on CEOs while everyone else in the organisation applies a much narrower focus in one direction, for the most part, according to the Harvard Business Review.

In a medium to large organisation, the CEO does not get involved with the day-to-day operations of the organisation. This is a responsibility shared (among others) by the Chief Operating Officer (COO), the Chief Financial Officer (CFO) the Chief Information Officer (CIO) and the Chief Technology Officer (CTO).

The CIO as a focused enabler of business growth

CIOs are facing unprecedented challenges to improve business outcomes, transform business models, modernise technology and enhance customer experience. In the era where privacy matters, the focus applied by today’s CIO is ideally placed to now zoom in on the protection of personal data.

In terms of the POPIA, the CIO’s job description in terms of legal responsibilities should include the following day-to-day responsibilities: ensuring the organisation puts practical frameworks in place to lawfully store and process personal information under the provisions of POPIA; seeking legal counsel or liaising with the organisation’s compliance officers regarding implementation of the framework; facilitating communication with the Information Regulator relating to POPIA matters, e.g., in the case of a data breach investigation or when the organisation needs to act on public data requests; and having a good working understanding of data privacy legislation, such as the POPIA and GDPR.

Practically, the following job descriptions are fundamental for an organisation to thrive in an age where privacy matters:

Align digital strategy development with organisational or enterprise goals. The CIO should act as the translator of the organisational and business strategy into a digital roadmap to give full effect to organisational goals and privacy legislation requirements. The CIO’s focus should ideally be more organisational, and less ‘tech’ as is commonly assumed.

Translate leadership to implementation by way of change management. Create awareness among employees, IT and security teams by educating them on the place protection of information holds in the organisation.

Project the ability to lead a project management team or effectively project manage various ongoing change, digital transformation, security or data privacy initiatives across the organisation.

In a world where change – such as legislation affecting organisations on a systemic level – happens quickly, we need the vision of the CEO to remain uncluttered and allow them the opportunity to make tough decisions. The CEO’s focus on the wider purpose will help organisations thrive.

The role of the CIO should be to strategically, operationally and practically transporting the organisation there via a digital highway – the only road that will lead thriving organisations to where they need to be, ahead. A visionary boardroom understands this difference.

Francois Kriel is Director at Kriel & Company

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

YouTube has announced that it’ll now be easier for creators to change their name and profile picture on channels.

“Until now, creators had to change their name and icon for their entire Google account — so their name on YouTube would be the same name they send emails from in Gmail.”

YouTube

“That didn’t necessarily make sense from a branding or professional perspective, and the new system should offer a bit more flexibility for creators who might prefer to send emails under their actual name instead of their channel name.”

There is one catch, however, creators with a verification badge will have to reapply if they decide to change their name.

YouTube is rolling out “Checks” – a new tool to help make uploading videos and receiving ad revenue easier for creators.

“Hey Creators! Today we’re rolling out a new step in the upload process on Studio desktop called “Checks” – which will automatically screen your uploads for potential copyright claims and ad suitability restrictions,” says YouTube in a blog post.

This new tool is expected to help creators minimize the number of videos uploaded with copyright claims and/or yellow icons to avoid surprises or worries.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Data and data analytics? Big business. We generate a massive amount of information every day, sourced via the Internet of (Every)Thing(s), GPS trackers, fitness wearables, software-as-a-service, web content and social media. This information can be analysed computationally to reveal patterns, trends and associations; yielding outputs with a multitude of uses. For example, we can use it to predict trends and patterns, find the most lucrative opportunities, and manage our time and resources more effectively.

Dina Biagio, Partner at Spoor & Fisher South Africa

But how does intellectual property (IP) law protect data, enabling it to be monetised? And what should businesses be aware of, as they grow increasingly dependent on data?

Copyright and common law

In South Africa, data is protected under copyright and the common law prevents unlawful competition. There is a distinction between an individual data item and a compilation of data (the latter, resulting from sourcing data items and organising them so as to make them useful).

An individual data item is eligible for copyright protection only if it is “original”; that is, not copied from an existing source, and if its production required a non-trivial degree of skilled judgement or labour. So copyright subsists in data items emerging from complex analysis, but not in raw data.

In contrast, where information has been (lawfully) gathered from publicly available sources and arranged into a compilation that can be searched and analysed, the compilation (but not the individual data items) is eligible for copyright protection.

As a general rule, copyright entitles the owner to prevent others from copying the original work but does not prevent independent re-development. However, proving that a compilation has been copied can be difficult, especially where the compilation is of raw, technical or public information.

Consider a database containing vehicle specifications and spare parts details that are publicly available. If a competitor were to compile the same information, independently and from scratch, the re-developed database is likely to be identical to the pre-existing ones.

How much must be copied?

An objective similarity between works will lead to the conclusion that work has been copied. But how much must be copied? ‘Data scraping’, where data items are (usually automatically) collected from public sources like websites, is commonplace. And this is sometimes permitted under the ‘fair dealings’ exception to copyright infringement, available in many jurisdictions.

Under SA law, copyright infringement occurs if a ‘substantial part’ of the original work is copied. So much must be copied that the value of the original compilation is sensibly diminished, particularly where the defendant takes ‘for the purpose of saving himself labour’.

Similarly, the owner of a database right existing under the European Directive on Copyright and Rights in Databases would have recourse where a ‘substantial part’ of the contents of their database is extracted or re-utilised. This applies even when the copying results from the repeated and systematic extraction or re-utilisation of insubstantial parts of the contents.

Unlawful competition

So we can own a copyright in data and data compilations, and we can prevent others from copying a substantial part of it. In Europe, we can own database rights. We can possess materials that contain data, and we can know data, but is it possible to own the data itself?

Our Courts have held that information or knowledge of whatever value and however confidential is not property and there is no real right of ownership comparable to ownership of corporeal property.

But a person having a quasi-proprietary or legal interest in data, or in a compilation of data, can seek relief for misappropriation, on the grounds of unlawful competition.

This interest could stem from having created the data/compilation; mandating another person to do this; or being granted an exclusive right to the data by the person who created, or mandated the creation of, the data/compilation.

Unlawful competition is based on the principle that no business should benefit at the expense of its rivals through the use of improper methods. But there is a fine (and sometimes blurred) line between competition that is deemed to be lawful and that which is not.

Unlawful competition is sometimes characterised by ‘springboarding’: starting not at the beginning with one’s own development but “using, as the starting point, the fruits of someone else’s labour”.

Ultimately though, the unlawfulness of business practice will be determined in each case, with regard to several subjective factors like the honesty and fairness of the conduct involved, the morals of the trade sector, and the importance of competition in a particular market.

As a trend, all businesses are likely to become increasingly dependent on data. You will need to navigate the legal minefield of data rights and interests, use data lawfully and optimise the value to be gained by exploiting it.

Dina Biagio is a Partner at Spoor & Fisher South Africa

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

One of Africa’s leading telecoms conglomerates, Airtel Africa, has denied reports that it plans to halt operations in Kenya. The news was first reported in a tech news platform Techweez after Prasanta Das Sarmato, CEO of Airtel Kenya, assessed the viability of the company after The National ICT Policy 2019 was signed.

Prasanta Das Sarmato, CEO of Airtel Kenya

“Equity Participation, a clause in the policy states that only companies with at least 30% substantive Kenyan ownership, either corporate or individual will be licensed to provide ICT services.”

Airtel however, has said that it would not be leaving the Kenyan market – “we remain committed to delivering quality and value for money products and services to all our customers whilst ensuring effective, uninterrupted communication is achieved across the entire country.”

Airtel goes on to say that it would continue to significantly invest in the enhancement of its network and distribution across Kenya.

“We are now rolling out approx 600 new sites to expand our network using the ultra fast 4G technology across the country. In addition, across key cities, we have upgraded our network to be 5G ready. This significant expansion and upgrade will improve coverage as well as customer experience in both urban and rural areas.”

Airtel Kenya has made a number of improvements to its network in order to meet the regulatory minimum threshold on quality of calls across the country. Airtel Managing Director, Prasanta Das Sarma said that 270 sites were upgraded from 2G and 3G sites to 4G while more than 400 sites were added in upcountry towns and highways.

“In total, the upgrade covered 20 counties. Some more sites will be added by the end of April when the work will be done,” says Sarma. “We are vindicated when we see more customers using us. With this kind of expansion, we will be able to satisfy CA criteria (on voice quality).”

Airtel Africa – and Telkom – came under fire earlier this year when the Communications Authority of Kenya (CA) placed the telco’s under scrutiny after allegedly violating the quality of services across their networks.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

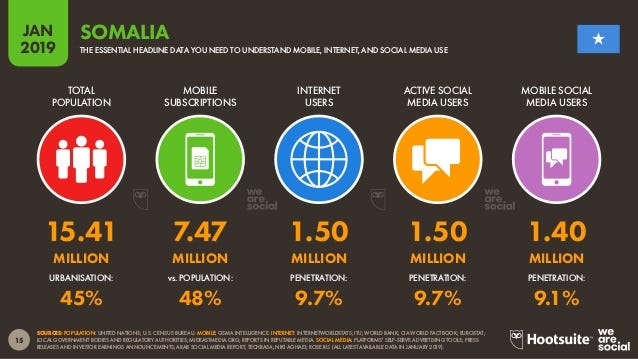

Hormuud Telecom, the largest telecommunications network in Somalia, has got a lot of things going for it, including having one of its towers reportedly bombed into pieces by Kenya Defence Forces (KDF) in 2019. But perhaps its biggest achievement so far is not only picking the country’s first mobile money license, but also being the first to proceed to launch the country’s first indigenous mobile money app, a benign way of mocking neighbouring Kenya’s Safaricom for accusing it of a heinous crime that necessitated the KDF’s retaliatory bombing.

Hormuud CEO and Chairman Ahmed Mohammed Yuusuf

Dubbed WAAFI, the fintech app will offer Somalis access to a variety of digital services on a single platform for the first time in an official manner. Consumers can use the WAAFI app to access their bank accounts, conduct online transactions, submit foreign remittances, and make international and domestic phone calls.

“Somalia is a unique example of a country where digital adoption is widespread among all age ranges and demographics. We are continuing to see a move towards a position where Somalia can claim to be the world’s first truly cashless economy, and the roll out of WAAFI is an important step on that journey. Providing businesses and customers with more efficient technology is going to be a driving force behind the development of the Somali economy and its integration with the wider international community,” Hormuud CEO and Chairman Ahmed Mohammed Yuusuf said.

Somalia was one of the last African countries to connect to the internet. Source: World Economic Forum

What Difference Does WAAFI Make Since Somalia Is Already A Large Mobile Money Market?

WAAFI is a fully integrated mobile money service that replaces the existing USSD technology used by many Somalis. In Somalia, USSD-enabled mobile money technology is widely used, with penetration rates of up to 80% in urban areas and up to 55% in rural areas.

WAAFI also allows people to make in-country bank transfers using their phones, which is a first in Somalia. This helps Somalia achieve its goal of becoming a cashless economy and combats fraud, as over 95 percent of the Somali shilling in circulation is estimated to be counterfeit.

WAAFI helps users to deposit and withdraw money from their bank accounts using their EVC Plus wallet. Businesses can use this to produce QR codes that enable customers to deposit funds directly into their bank accounts.

“The WAAFI app has transformed how I do business. Having important digital services all housed under one app makes it easier to pay my employees and trace transactions quickly. Even when I’m abroad or cannot be physically present, with this app I can check on my business and address any problems. Operating throughout the pandemic, this app has allowed me to keep my customers and my employees safe. With contactless payments, we can reduce physical contact and the spread of the virus in our communities,” Abdulaziz Mohamed Nurani, the founder of premier fashion retailer Tik, was quoted as saying.

Hormuud continues to expand its high-speed digital infrastructure across Somalia with the launch of the app. According to Hormuud, roughly half of Somalia’s urban population has access to 4G internet, with slightly more than 60% having access to 3G, both of which are considered broadband-level services in frontier economies.

The telco received the first mobile money license from the Central Bank of Somalia in February 2021, indicating that its mobile money network EVC Plus is now officially controlled and authorised by the Central Bank. In Somalia, Hormuud Telecom has 3.6 million customers, with 3 million of them using EVC Plus.

However, granting the mobile money license does not mean that mobile money operations have not been going on in the country. For every month in the year 2018, the country recorded approximately 155 million mobile money transactions, worth $2.7 billion. Similar transactions have also been going on in the country for the past 10 years.

What the Central Bank of Somalia merely did was to issue the country’s first ever money license to an entity, thereby ending the era of unregulated mobile money services in the country.

CBS’ license to Hormuud Telecom is a major achievement for the telecom company as it helps it to partially heave some sighs of relief from the country’s crowded telecoms market, currently made up of 11 licensed local operators.

Although Hormuud’s new license may not make much difference as there are already numerous unregulated services in operations, it may however help the telco to position itself early for post-regulation market share.

According to the World Bank 2017 report, mobile money service in Somalia has reached a penetration rate of 73% (83% in urban areas), compared to a penetration rate of 15% for formal bank accounts. Somalia’s Dahabshiil is one of the largest money transfer companies in Africa, operating in 155 countries.

Majority of Somalian households (58%) make one to four transactions each month and tend to use mobile money over cash for purchases between US$2 and $300. A mobile money account must be linked to a bank account for transactions over $300. As a result, digital money is an excellent cash replacement, and it can be used for everyday transactions such as bill payments, paycheck receipts, and merchant transactions. Nevertheless, a study by Hormuud Telecom revealed that cash-out rates on mobile money platforms in Somalia are less than 5%, indicating a greater number desires to keep money in mobile wallets rather than cash it out.

In contrast to Kenya’s well-known Mpesa mobile money transfer service, Somalia’s transactions are mostly in US dollars. Though mobile money providers are mobile network operators, they are increasingly becoming part of large conglomerates that also provide banking and money transfer services, as in Kenya.

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

As Egypt’s startup ecosystem continues to gain momentum, the Netherlands has touched down in Cairo to join in the frenzy. This is represented in the recently signed partnership between Egypt’s Ministry of International Cooperation and the Netherlands embassy in Cairo as well as Alexbank for the launch of an entrepreneurial programme called “Orange Corners Egypt”.

Dante Campioni, CEO of Alexbank

Orange Corners Egypt is a Dutch program that offers training, networks, and facilities to young entrepreneurs looking to start and develop creative businesses.

“Egypt’s youth are the driving force of our nation. Only by involving, empowering and enabling them, we will be able to achieve real strides towards sustainable development. 2021 is the year of private sector engagement: we are pushing towards the national development agenda through public-private partnerships that foster the sustainability ethos and spread it across several sectors; especially the entrepreneurial scene,” Rania Al-Mashat, Egypt’s Minister of International Cooperation, said.

The project is divided into two incubation programs, one in Cairo and the other in Upper Egypt (Assiut), each of which provides recurring 6-month training cycles for 15–25 entrepreneurs at a time. The entrepreneurial training gives particular attention to startups in agriculture and the creative field, and ensures that at least half of the participants are women.

Orange Corners Egypt will be able to associate enrolled entrepreneurs with follow-up opportunities within the Egyptian entrepreneurial ecosystem more easily thanks to the Ministry of International Cooperation’s support. The Ministry will assist the program’s implementation partners in finding untapped opportunities for creative ideas to contribute to Egypt’s growth through various sectors while achieving the SDGs.

Alexbank, one of Egypt’s largest banks, will be a key private sector investor in the program. It will contribute an annual financial contribution to the program as well as in-kind assistance, such as master classes and mentorship for participating entrepreneurs.

Egyptian service providers Cultiv in Cairo and Outreach Egypt in Upper Egypt provide entrepreneurship training in Egypt. In the first quarter of 2021, the first training cycles began.

“Our participation in the Orange Corners initiative by the Embassy of the Kingdom of the Netherlands in association with the Ministry of International Cooperation is driven by our strong belief in Egypt’s startup scene. Egypt is a country of talented youth seeking the opportunity of becoming entrepreneurs, and the Orange Corners model can certainly contribute to fulfil this wish by bringing also to Egypt a well-experienced startup framework. What’s more, we are excited to see the program hosting chapters in two distinct and vibrant regions of Cairo and Upper Egypt, thus offering a truly inclusive approach. We’re also particularly happy that the programme can provide opportunities in the field of agribusiness and agritech, giving the chance to a new generation of entrepreneurs to venture into the evolution and integration of the agricultural sector that is so important to Egypt,” Dante Campioni, CEO of Alexbank, said.

Han-Maurits Schaapveld, Ambassador of the Netherlands, said:

“Young Egyptian entrepreneurs are the oxygen of Egypt’s economy. Therefore, we are very excited to collaborate with the Ministry of International Cooperation and Alexbank to provide essential support for entrepreneurs to further develop their skills and ideas through Orange Corners Egypt.”

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

The Africa focused software company that is best known for connecting African developers to global clients has expanded their talent pool beyond the continent to welcome Latin and South American developers. Andela according to company sources took this step to expand its talent pool which it says is open to Africans and non-Africans in those regions. According to Andela’s CEO, Jeremy Johnson, the company “has always been part of our long term roadmap, and we’re excited that the world is ready for it.”

Andela’s CEO, Jeremy Johnson

He describes the move as a reflection of the “future of work,” one that is remote and not restricted by geographical boundaries or a need to share physical spaces.

In July 2020, Andela closed its physical offices in Nigeria, Uganda and Rwanda to become a fully remote company. The particular rationale at the time was to increase the number of Africans who could apply to work for the company as software developers.

While the pandemic’s restriction on physical movement influenced that change in policy, there was some logic to it. Andela’s physical offices were sited only in major cities in each country they operated (Lagos, Nairobi, Kampala; their Cairo operation was remote-first from day one). Anyone who wanted to be an Andela developer had to move to these cities.

It is the expectations of the company that by going remote, a qualified developer anywhere in Africa could apply to Andela. At the time, Johnson said it opened Andela up to 500,000 potential engineers from the previous 250,000 available under a physical-office model. However, the remote logic was destined to extend naturally; if going remote opens Andela up to more African developers, it also opens them up to developers everywhere in the world.

In the past six months, Andela says it has witnessed a 750% increase in applications from qualified engineers outside of Africa. More than 30% of inbound applications in March 2021 alone were from outside of Africa; half of that 30% were from Latin America, according to the company. Latin and South American countries are Spanish and Portuguese-speaking countries from Mexico on the southern border of the United States, through Colombia and Brazil to Chile and Argentina.

Andela frames this diverse base as an advantage for their clients. Companies who have people from different geographies on their engineering teams stand to get the benefit of diverse backgrounds, lived experiences and approaches to work that improve the quality of their products.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Leaving the Bank in a position many described as envious, Segun Agbaje has proved his mettle as he prepares to bow out as chief executive officer (CEO) of Guaranty Trust Bank and its ancillary holding companies. Looking back at some of the outstanding impacts of his leadership, one couldn’t help but point to the major role he played in putting together Guaranty Trust Bank’s landmark US$350million Eurobond offering in 2006 and later in the same year, the listing of its US$750 million Global Depository Receipts (GDR) in an unprecedented concurrent global offering in the domestic and international capital markets – which made Guaranty Trust Bank the first Nigerian company and first African bank to be listed on the Main Market of the London Stock Exchange.

Group Managing Director of GTBank, Segun Agbaje

But it has not always been like this. When fate trust the leadership of the Bank on his after the death of co-founder Tayo Adenirokun, Mr. Agbaje came under severe criticisms and the Bank also lost a lot of positive perception mileage as many worried whether he could step into the big shoe left by Tayo as he was fondly called by members of staff. Shortly after becoming CEO, he led the bank to launch the first Sub-Saharan Africa financial sector benchmark Eurobond when the Bank launched its US$500million Eurobond without a sovereign guarantee or credit enhancement from any international financial institution.

Agbaje no doubt possesses a deep sense of loyalty and is driven by values of hard work, integrity, and discipline. He is probably one of few banking executives who stayed with one bank for thirty years, attaining the peak of his career there. This is not because of a lack of better options, but because of Agbaje’s commitment to the bank he had seen and groomed from its infancy days. He also helped in developing the Interbank Derivatives market amongst dealers in the Nigerian banking industry and introduced the Balance Sheet Management Efficiency System.

His deep understanding of the Nigerian business environment has seen him initiate and execute large, innovative and complex transactions in financial advisory, structured and project finance, balance sheet restructuring and debt and equity capital raising in different sectors like Oil and Gas, Energy, Telecommunications, Financial Services and Manufacturing industries.

According to Agbaje’s recount, the several responsibilities he handled in the bank over the years exposed him to the international financial markets and the people who worked in them – merchant banks, investment bankers, lawyers, and investors. It also gave him a deeper understanding of what people wanted from a first-class bank.

Under his leadership, GT Bank Plc won several awards including Best Bank in Nigeria by Euromoney; African Bank of the Year by African Banker Award; Best Bank in Nigeria by World Finance UK; Most Innovative Bank by EMEA Finance; Best Banking Group by World Business Leader Magazine and Best Bank in Nigeria award by the Banker Awards; Best Mobile Banking and Mobile Money awards, Best Digital Bank awards and, Digital Wallet of the Year award.

Ahead of the disruption in the banking sector, Agbaje gave GT Bank a headstart when he launched the Habari mobile platform in November 2018 for customers to carry out a wide range of services including “pay for tickets, book holidays, stream music, buy online, watch videos, and then, because we are a bank, we can provide the payment engine.” He predicted even then that any bank that does not transform itself into a trusted single, integrated platform will get smaller and smaller as the fintechs and telcos grow larger and take over.

Agbaje won the African Banker of the Year award in 2012. He serves on the boards of other business concerns including Guaranty Trust Bank in Kenya, Rwanda, Uganda, Ghana and the United Kingdom. Agbaje has other commitments as well, but none of them run parallel to that of GT Bank. He is a member of the board of directors and audit committee of PepsiCo, a position he resumed on 15 July 2020. He is also a member of the Mastercard Advisory Board, Middle East and Africa.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

The Central Bank of West African States, which serves the eight west African countries that share the common West African CFA franc currency, has published the terms under which member countries’ national treasuries will link their solutions to a central platform run by the West African Economic and Monetary Union Interbank Grouping (GIM-UEMOA) in order to issue digital currency and prepaid cards for electronic payments of public allowances (salaries, scholarships, pensions, etc.).

West African Central Bank

“Digital currency is a monetary value reflecting a claim on the issuing institution that is held in electronic form, including magnetic; distributed without delay in exchange for remittance of funds in a sum equal to or greater than the monetary value issued; and recognized as a means of payment by natural or legal persons other than the issuing institution,” reads instruction №008–05–2015 governing the terms and conditions for carrying out the activities of electronic money issuers in the Member States of the West African Monetary Union (WAMU).

Located in Dakar, Senegal The Central Bank of West African States is a central bank serving the eight west African countries which share the common West African CFA franc currency

Here Is What You Need To Know

The rules provide that the institutions that can issue electronic money are banks; payment financial institutions; decentralized financial systems and electronic money institutions.

The rules therefore encourage public treasuries to promote the use of payment and withdrawal cards, electronic wallets, and telepayments, as well as any other modern payment method and instrument yet to be developed, in particular by forming groups with the goal of developing national or regional electronic transfer processes.

However, payment through electronic or digital money has been limited, for now, to those who receive public state benefits, such as civil servants, grant recipients, or retirees.

Any national public treasury can act by submitting an application to the Central Bank for authorization to issue electronic money, which will conduct a compliance review of the file.

Similar To Central Bank of Tunisia’s Digital Currency Project

The country’s Dinar Digital network under “Central Bank of Tunisia Digital Currency” project brings together member financial institutions, with the aim of using blockchain technology to fully digitalise the country’s fiat money (cash). The BCT Digital Currency project hopes to also improve efficiency and reduce the costs of financial transactions for Tunisians.

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer