Africa’s Private Sector Gets $3.5 billion Support from Japan and the AfDB.

The fruits of the ongoing 7th Tokyo International Conference on African Development (TICAD 7) have started yielding with the joint target of $3.5 billion under the Enhanced Private Sector Assistance for Africa initiative (EPSA4) by the Government of Japan and the African Development Bank (AfDB). Both Japan and the Bank have pledged to set a target of $1.75 billion each, from 2020-2022, to enhance the fourth phase of EPSA to spur private-sector-led sustainable and inclusive growth in Africa. They agreed to focus on the social sectors to help in human resource development across the continent.

Speaking on the agreement, the Japanese Minister of Finance, Mr. Keisuke Suzuki said that building on the successful achievements so far, Japan and the African Development Bank decided to upgrade EPSA in both quality and quantity to meet financial needs for infrastructure development as well as for the private sector development in Africa. He added that it is his wish that the new EPSA initiative will lead to business, investment promotion, and job creation in Africa.

According to the agreement, the three core areas that will be the focus for this EPSA4 would be electricity, transportation, and health. Projects and programs for these three key priorities will be formulated and implemented in line with the G20 Principles for Quality Infrastructure Investment and G20 Shared Understanding on the Importance of UHC Financing in Developing Countries. African countries will also be provided with support to improve and create conducive business environments to attract private investments.

Dr. Akinwumi Adesina described the development as worthy of celebration, noting that it is a sign of the strong and impactful partnership between Japan and the African Development Bank. He highlighted that the African Development Bank and the Japan International Cooperation Agency (JICA) are long-term partners for promoting the development of Africa. EPSA helps to deliver much needed to support the private sector.

It could be recalled that during EPSA1 (2005-2011), Japan set the target of providing $ 1 billion in loans and $ 2 billion under the second phase (2012-2016). The ongoing EPSA3 (2017-2019), Japan and the African Development Bank are cooperating closely to provide the targeted joint amount of $ 3 billion.

As of today, the Bank and JICA under ACFA have co-financed 25 projects to improve key transportation and electricity transmission networks. These include the Construction of Three Intersections in Abidjan in Côte d’Ivoire and Power Sector Reform Program in Angola.

“Under EPSA 4, JICA and the African Development Bank will provide co-financing of $3.5 billion. This is a significant increase over EPSA-3. Increase is what we need to meet the needs of Africa. Increase is what we need to raise the level of our ambitions for Africa. Increase is what we need to build upon the solid foundations of co-financing over the last 13 years, and deliver even greater and more impactful development results in the years ahead. Now, let us arise with renewed vigor. Let us deliver even greater impacts for African countries through EPSA 4,” Dr. Adesina concluded.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

On 12 April, Africa witnessed a historic moment, one that could potentially prove seismic in shaping its future. Jumia, the e-commerce startup that has been catering to African consumers through the online sale of products since 2012, officially launched its Initial Public Offering (IPO). The “Jumia Phenomenon”, it being the first African tech start-up listed on the NYSE, has now firmly cast the spotlight on the continent’s start-up scene. A range of stakeholders including governments, investors and prospective entrepreneurs are keen to learn and participate in what is happening.

Whilst Jumia brought on a revolution in a fragmented and outdated African retail environment by bringing mainstream e-commerce to Africa, an undertaking that will lead to positive spillover effects for Africa’s tech ecosystem (such as Jumia Alumni Founders), I want to highlight other innovations happening on the continent that are supported by venture capital, through my experience at Savannah Fund, which has invested in over 30 start-ups in seven countries over the last six years. Given that I’m writing from Arusha, Tanzania — an agricultural hub in the heart of the Rift Valley on the slopes of Kilimanjaro and Meru — I will focus on agriculture’s potential tech transformation and highlight some of the challenges African start-ups face.

Despite this acknowledgment, Africa remains the most food-insecure region in the world and a net importer of food. This calls for a fresh approach; agritech may just be the answer.

Aerobotics is one tech start-up rising to this challenge by employing drone imagery and artificial intelligence to enable early pest and disease detection to help forecast yield. Another start-up, Tulaa in Kenya, which provides smallholder farmers with quality agricultural inputs on credit and also employs artificial intelligence to connect farmers, input suppliers and buyers in a digital marketplace.

Innovative business models employing sophisticated technology very often require partners and investors not only with an understanding of Africa, but with expertise in sub-sectors like artificial intelligence and robotics, and how they can be developed and applied within an African context. Venture capital firms, contrary to the common misconception, are not simply providers of capital, but by way of their team composition often add value to their portfolio companies precisely through this wide range of knowledge and expertise on the operational and business side.

In staying with agriculture, we cannot ignore climate change. The existential threat of this crisis looms large over our planet, and Africa is the continent that will be most severely impacted. Apart from the fact that climate change is set to create uninhabitable living conditions and an explosionin migrants around the world, it is also very likely to affect those in the agricultural sector in Africa and in particular small-scale farmers who rely on consistent yields to earn a living.

WorldCover, an emerging market climate insurance start-up, is one such company that is helping to address this problem by offering crop insurance to smallholder African farmers, providing a much-needed safety net against unpredictable weather patterns.

This is an area where African venture capital firms can thrive. Start-ups with profiles similar to WorldCover’s are often seeking not only capital, but also the right partners who can provide the necessary assistance to navigate specific African markets and a diverse set of countries in areas such as those dealing with regulatory compliance and local recruitment.

The reverse direction is also an area of value, helping African start-ups access global markets and capital and assistance, as the likes of Savannah Fund have done, by providing a bridge to Silicon Valley and increasingly to Europe and Asia. Aerobotics have taken this path, from the farms and orchards of South Africa to one of the biggest agricultural markets in the world: California.

With the backdrop of some early successes in agriculture, what challenges lie in venture-backed start-ups in Africa?

• Evolution in early-stage funding: It’s often said one of the last areas of the private equity/venture capital ecosystem left to develop is the early stage (this follows over two decades of $100 million+ funds struggling to find a good pipeline of deals in Africa). Tech start-ups on the continent are starting to emerge as well as funds to crack this chicken and egg problem. This phase will naturally incur a lot of risk-taking, pivoting of start-ups and yes, failures — VC is in the risk business, unlike later-stage funds that are in the scaling-up business. Challenges remain, but there are some important recommendations as outlined in the recent Frontier Economics report.

Image: Maxime Bayen

Image: Maxime Bayen

• Strong governance is key A challenge with African start-ups (often first -time entrepreneurs) that we tend to encounter comes in the area of governance and accurate reporting of key metrics and financials. Often they fail to recognize that instituting strong mechanisms early establishes good habits for the future, creates transparency and order, avoids skirmishes with local tax authorities and severely improves their chances of executing successful follow-on fundraising. Savannah Fund has evolved to be a lot more hands-on in this area, as it is critical to leveling the playing field and being globally competitive.

Transition to scaling up In addition to the work done by the likes of Andela and Moringa to provide a pipeline of local talent, start-ups sometimes seek access to capital, markets and talent globally as they scale. We have noticed companies that are able to leverage global connections (Silicon Valley to Japan or Cape Town to London) are at a distinct advantage vs. those that do not. This is where early-stage VC firms can act as an important bridge for start-ups coming from a less developed environment — this includes helping start–ups join global accelerators such as 500 Startups,Techstars or YC to the west, Efounders program by Alibaba to the east, or access development finance debt within African or European multilateral institutions.

The latter is often cheaper capital if it’s shown to have a development impact, such as helping smallholder farmers or creating jobs of the future. Founding teams need to be creative, but stay focused and not get distracted. Examples of start-ups successfully leveraging global firm expertise and capital sources include Aerobotics joining the Google Launchpad for Africa and WorldCover graduating from YC.

Mohammed Al-Beity is an Associate at Savannah Fund, a seed capital fund specializing in US$25,000-US$500,000 investments in early stage high growth technology startups in sub-Saharan Africa.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Airtel established its presence in Africa in 2010 when it bought Kuwait-based Zain’s Africa operations for $10.7 billion

Bharti Airtel’s Africa arm posted a revenue of $795.9 million in the June quarter, up 6.9% y-o-y, from $744.5 million

Bharti Airtel’s Africa arm has crossed the 100-million customer mark across its operations in the continent, the company said in a statement on Wednesday.

This is significant for the company, which entered the continent in 2010. Airtel Africa is currently the second-largest mobile operator in Africa by the number of active subscribers; South Africa’s MTN is the largest.

“The positive momentum we have seen in customer acquisition further underpins our medium-term aspirations for revenue and profit growth,” Raghunath Mandava, Airtel Africa’s chief executive officer, said in the statement.

Airtel Africa is the holding firm for Bharti Airtel’s operations in 14 countries in the continent across three regions — Nigeria; East Africa, comprising Kenya, Uganda, Rwanda, Tanzania, Malawi and Zambia; and the rest of Africa, including Niger, Gabon, Chad, Congo Brazzaville, the Democratic Republic of the Congo, Madagascar and Seychelles. Nigeria alone accounts for almost half of its earnings before interest, taxes, depreciation and amortisation (Ebitda).

Airtel established its presence in Africa in 2010 when it bought Kuwait-based Zain’s Africa operations for $10.7 billion. Over the past few years, it has been trying to expand in Africa through local acquisitions.

Africa has also proved to be a beacon of hope for the company, currently faced with a struggling India business, which is battling a tariff war waged by Reliance Jio’s entry in September 2016.

Bharti Airtel’s Africa arm posted a revenue of $795.9 million in the June quarter, up 6.9% year-on-year, from $744.5 million, largely driven by double-digit growth in Nigeria and East Africa, and partially offset by a decline in revenue in the rest of Africa.

Airtel Africa posted a net profit of $132.2 million in the June quarter, a decrease of 12.2% against the previous year, as higher finance costs and lower gains on exceptional items offset its growth in operating profit. The June-quarter results were the company’s first financial results after it raised $750 million in June through its initial public offering (IPO). The shares were then priced at 80 pence per share, giving it a market capitalization of around $3.9 billion.

Its average revenue per user was $2.7 in the June quarter. Airtel Africa’s Ebitda rose 9.7% year-on-year to $347.6 million in the June quarter, from $316.9 million in the previous year.

The company’s revenue from data services grew to $207.1 million in the quarter, from $156.6 million a year ago, while voice revenue was flat at $469.9 million.

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

MUFG and Afreximbank Sign Memorandum of Understanding

African organizations and their Japanese counterparts are using the opportunities of the ongoing Tokyo International Conference on African Development (TICAD) at Yokohama City Japan to ink deals and enter into series of agreements. The most recent of such deals is between the MUFG Bank and African Export and Import Bank (Afreximbank) signed a Memorandum of Understanding (MOU) to provide a broad framework for collaboration between the two organisations.The MOU will further strengthen the relationship between MUFG and Afreximbank, allowing for increased cooperation across Africa through the joint financing of transactions in Corporate, Project, and Sovereign financing, as well as enhancing the Trade Finance offering both organisations.

Speaking on the MoU, Mr. Takanori Sazaki, Regional Executive for MUFG in EMEA, said: “As we at MUFG seek to strengthen our presence across Africa through innovative opportunities, this MOU with Afreximbank is perfectly timed. The continent is undergoing remarkable growth and shows no sign of relenting due to market expansion and growth in investment from overseas. He noted that Japanese businesses are increasingly viewing Africa as a new frontier, as the seventh TICAD gathering clearly demonstrates, “and we look forward to facilitating discussions with international organisations, private companies and government bodies to enable long-term investment and trade expansion as part of this.” MUFG’s involvement in Africa goes back more than 90 years to 1926, when Yokohama Specie Bank, a forerunner of MUFG, opened an office in Egypt. Today MUFG has offices in Cairo, Egypt, and Johannesburg, South Africa.

Reacting to the development, the President of Afreximbank, Prof. Benedict Oramah, said that the Bank is proud to be signing this MOU with MUFG, noting that it strengthens the already good relations built over the past several years. The MOU sets a solid foundation for reinforcing the economic bond between Africa and Japan at a time of increasing global trade tensions. He added that “it creates a unique opportunity for African businesses to benefit from MUFG’s increasing African presence while also enabling MUFG to enhance its offerings to Japanese entities seeking business opportunities across Africa.”

Afreximbank is the foremost pan-African multilateral financial institution devoted to financing and promoting intra-African trade and trade between Africa and the rest of the world. It works with international partners to leverage trade financing into Africa. The Bank was established in October 1993 by African governments, African private and institutional investors, and non-African investors. Since 1994, it has approved more than $67 billion in credit facilities for African businesses, including $7.2 billion in 2018. Afreximbank had total assets of $13.4 billion as at 31 December 2018. It is rated BBB+ (GCR), Baa1 (Moody’s), and BBB- (Fitch).

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

Japan has Promised to Help Africa Double its Rice Production by 2030

The Japanese Prime Minister Shinzo Abe has promised that Japan will help Africa double its Rice production by 2013. Mr. Abe made this known during a symposium hosted yesterday by the Sasakawa Africa Association (SAA) at the ongoing Tokyo International Conference on African Development (TICAD) at Yokohama City, Japan. The SAA according to the Japanese Prime Minister will work with the Japan International Corporation Agency (JICA), to help African countries double their rice production to 50 million tonnes by 2030. The Prime Minister maintains that “Japanese technology can play a key role in innovation which is key to agriculture” .

The Symposium which focused on Africa’s youth bulge, unemployment rates, agricultural innovations and technologies, solutions and job creation opportunities in the agricultural sector had many African political leaders and institutions in attendance.

Speaking, the Chairman of Nippon Foundation, Yohei Sasakawa said that his team always believed in the agriculture potential of Africa, and that they are paying more attention to income-generating activities than before. To this end, he is of the view that Nippon Foundation will help shift the mindset of small-holder farmers from producing-to-eat to producing-to-sell. “We are hopeful that Africa’s youth can take agriculture to a new era, and that they can see a career path in agriculture,” he added.

The need to end global hunger was top priority at the event and this was reiterated by the President of African Development Bank Group President, Dr. Akinwumi Adesina who called for urgent and concerted efforts to “end hunger”. Dr Adesina noted that in spite of all the gains made in agriculture, the world is yet not winning the global war against hunger. “We must all arise collectively and end global hunger. To do that, we must end hunger in Africa. Hunger diminishes our humanity,” Adesina urged.

It could be recalled that the United Nation’s Fodd and Agriculture Organisation (FAO) in its 2019 State of Food and Security warned that the number of hungry people globally stands at a disconcerting 821 million. Africa alone accounts for 31% of the global number of hungry people – 251 million people.

Dr. Adesina commended the late founder of the Sasakawa Association, Ryochi Sasakawa, for his tireless efforts in tackling hunger, noting that it is passion, dedication and commitment to the development of agriculture and the pursuit of food security in our world has been the hallmark of Sasakawa’s work. Since coming to Africa, the Sasakawa Association had between 1986 and 2003 operated in a total of 15 countries including – Ghana, Sudan, Nigeria, Burkina Faso, Benin, Togo, Mali, Guinea, Zambia, Ethiopia, Eritrea, Tanzania, Uganda, Malawi and Mozambique.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

Egypt’s startups have been consistent in VC fund raising so far. And it appears more investors are headed for that North Eastern country than to any Sub-Saharan African country, apart from Nigeria and South Africa this year. Egypt’s Fintech startup, NowPay, has just joined that wagon. The startup said it is closing a new undisclosed round after raising USD 600,000 in Seed funding from Silicon Valley’s Endure Capital and 500 Startups.

Here Is The Deal

Although this round of investment was not disclosed, the startup has however raised USD 600,000 in Seed funding from Silicon Valley’s Endure Capital and 500 Startups

About NowPay

The Cairo-based startup, launched in early 2019, came out of stealth promising to improve financial wellness of corporate employees in emerging markets through its fintech solution that helps people get their salaries in advance at any point during the month.

“Saving, spending, budgeting and borrowing. Those are the four pillars of financial-wellness. We want to improve every aspect of those for employees,” said Mostafa Ashour, Cofounder and CEO of NowPay who previously led Innovation teams at Microsoft Research.

Ashour started NowPay with co-founders Ahmed Sabry of Amazon Lending, and Cherif Radi who led special projects at Orange.

“In order to reduce money worries, lower financial stress and cut down attrition rates, employees need to feel that they can get their salaries whenever they are cash-strapped,” said Ashour, explaining that his solution helps employees better manage their budgets, overcome cash flow problems and avoid unexpected events.

Fintech startups in Egypt have also seen a wave of investment. Egypt’s MoneyFellows recently joined the list of startup fundraisers in Africa. The Cairo-based fintech has raised over $1 million in a bridge round (Pre-Series A). The investment came from 500 Startups and Dubai Angel Investors, both of which had previously invested in company’s seed round as well, last year, Beirut-based Phoenician Fund, and some individual investors including some of its previous angels.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Barely 3 years old, Nigerian startup Esusu, a financial technology platform which helps individuals save money and build credit, has closed a $1.6 million seed round of funding

‘‘Against All Odds: Today we are delighted to officially announce Esusu’s $1.6M round of financing,’’ Esusu co-founder Wemimo Abbey noted.

‘‘While this is an exciting moment for our company, our work to unlock financial opportunity for millions around the world is only beginning. Grateful for our friends, family, investors, and partners that have stuck with us against all odds.’’

Here Is The Deal

The round of investment was led by Acumen Fund with participation from Sinai Ventures, Kleiner Perkins, Katapult Accelerator, Plug and Play Tech Center, Global Good Fund, Temerity Capital Partners, and prominent angel investors.

The $1.6 million in venture capital would help Esusu to scale, expand market share, and focus on product development.

The new funds will also enhance the rent reporting platform, onboard new partnerships, and extend overall reach.

The startup also plans to grow its team — hiring in key leadership roles across sales, technology, and operations.

“With the support of our strategic investors and partners, Esusu is poised for unprecedented growth and ready to scale to serve the millions of Americans struggling to save and create a financial identity,” said Abbey Wemimo, Co-Founder and Co-CEO of Esusu. “There are 45 million people in the United States without a credit score; our platform helps to score them, build their credit profiles and will ultimately unlock over $3.1 trillion in untapped capital.”

Why The Investors Invested In The Startup

Eliza Golden, Portfolio Manager of Acumen said Esusu must have been chosen because:

“As impact investors focused on improving the financial health of all Americans, we look for entrepreneurs who are tackling frictions in the financial services industry that are adversely affecting both sides of the market. We’re excited by Esusu and the vision of co-founders Samir and Abbey to build better tools for traditional financial services industry players. Esusu serves lower-income and historically credit-challenged consumers, while simultaneously empowering these consumers with credit-building tools that can transform their access to wealth-building — rather than predatory products and services.’’

What Esusu Does

Founded in 2016, Esusu is at the forefront of paving a permanent bridge to financial access by providing financial solutions for low-to-middle income consumers.

Esusu’s groundbreaking rent reporting platform captures rental payment data and reports it to credit bureaus to boost credit scores. This allows tenants to build and establish their credit scores while helping property owners attract tenants, reduce turnover, and improve collections to increase their operating income. Esusu creates the community and systems needed to build credit and thrive.

Co-founded by Abbey Wemimo and Samir Goel alongside founding team members Albert Owusu-Asare (CTO) and Robert Henning (CFO), the Esusu app helps people establish and build credit.

In 2018, Esusu debuted its peer-to-peer savings app on iOS and Android.

This year, Esusu launched its signature rent reporting platform to give renters credit for making monthly payments, a benefit historically reserved for homeowners.

Esusu has been at the forefront of the technology integration of rent reporting and partners with leading public and private sector housing developers to report rent payment data to credit bureaus.

Rent reporting has proved to not only lift credit scores but it helps landlords improve underwriting, reduce missed payments, and retain tenants longer.

“Esusu is growing swiftly to meet the demand for our rent reporting platform, and our nonprofit and corporate partnerships are essential to scaling while continuing to ensure safe and friction-free customer experience,” said Samir Goel, Co-Founder and Co-CEO of Esusu. “Our technology is capturing financial information that has never been recorded to equalize the playing field and increase access to capital and credit for millions that have been underserved by the financial system.”

Esusu has also entered into a number of partnerships with national organizations including the Local Initiatives Support Corporation (LISC) and Credit Builders Alliance (CBA).

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

The World Bank Sells Off Stake in Eco Bank Transnational

The World Bank Group through its private sector arms, the International Finance Corporation (IFC) and the funds managed by the IFC Asset Management Company have spurned off its 14 per cent stockholding at Ecobank Transnational to Arise B.V. which has made Arise a shareholder of reference in Ecobank Transnational with a 14 per cent stake. The transaction had J. P. Morgan Securities as Sole Placement Agent and Sole Financial Advisor to IFC and the funds managed by AMC in the transaction.

Describing the transaction as a success, the Senior Advisor at the International Finance Corporation (IFC) Mr. Paolo Martelli, said that the decision to divest from Eco bank Transnational was part of IFC’S ordinary asset portfolio rotation, and that Arise B.V. is a highly reputable investment house with a strong developmental mandate for Africa. It could be recalled that the IFC invested in Eco bank for more than ten years and that investment has helped to increase access to credit for entrepreneurs and SMEs in Sub Saharan African Countries including IDA countries in which the Bank operate. That investment according to the IFC helped achieve the kind of development impact it was looking out for when it made the investment. In spite of this divestment, the IFC maintains strong commitment to the development of the Sub Saharan African Region and is continuing to invest in other projects in these countries, sources at the global investment group say.

Responding, the Chief Executive Officer of Arise B.V., Deepak Malik, described the investment as being in line with his organizations core business mandate of investing in Africa’s local prosperity and that Arise is excited to have acquired 14 per cent shareholding in Eco bank Transnational Incorporated (ETI).

He noted that Arise aims to collaborate with local Financial Service Providers (FSPs) in Sub – Saharan Africa to boost economic growth through strengthening the local banking sector. This transaction with ETI will see Arise collaborate with Eco bank to advance financial inclusion on the continent, he added.

Ade Ayeyemi, Chief Executive Officer of Eco bank Transnational described the transaction as a welcome development, saying that the Bank welcomes Arise as a shareholder of ETI and believe that there would be a strong synergy in the Bank’s core objectives especially in ensuring and enshrining financial inclusion and the potential for the development of our continent. He added that Ecobank must also take the opportunity to extend her deep appreciation to IFC for its commitment to and support for Ecobank in the last 10 years. “We made meaningful progress with the strong collaboration and look forward to continuing to work with IFC in other areas in the future” he added..

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

PRESIDENT BUHARI RECEIVED PRESIDENT OF SOUTH AFRICA AND BENIN

President Muhammadu Buhari got the President of South Africa, H.E Cyril Ramaphosa during a side gathering at the seventh Tokyo International Conference on Africa Development (TICAD in Yokohama Japan. Photograph; SUNDAY AGHAEZE. AUG 28 2019

PRESIDENT BUHARI PRESIDENT OF SOUTH AFRICA 0A. President Muhammadu Buhari RECEIVED the President of Benin, H.E Patrice Talon during a side meeting at the 7th Tokyo International Conference on Africa Development (TICAD in Yokohama Japan. PHOTO; SUNDAY AGHAEZE. AUG 28 2019

PRESIDENT BUHARI PRESIDENT OF SOUTH AFRICA. President Muhammadu Buhari with the President of South Africa, H.E Cyril Ramaphosa during a side gathering at the seventh Tokyo International Conference on Africa Development (TICAD in Yokohama Japan. Photograph; SUNDAY AGHAEZE. AUG 28 2019

PRESIDENT BUHARI PRESIDENT OF SOUTH AFRICA 3. President Muhammadu Buhari received the President of Benin, H.E Patrice Talon during a side meeting at the 7th Tokyo International Conference on Africa Development (TICAD in Yokohama Japan. PHOTO; SUNDAY AGHAEZE. AUG 28 2019

PRESIDENT BUHARI PRESIDENT OF SOUTH AFRICA. President Muhammadu Buhari (M) Chats with the President of South Africa and Minister of Foreign Affairs, Mr Geoffery Onyeama during a side gathering at the seventh Tokyo International Conference on Africa Development (TICAD in Yokohama Japan. Photograph; SUNDAY AGHAEZE. AUG 28 2019

PRESIDENT BUHARI PRESIDENT OF SOUTH AFRICA 4. President Muhammadu Buhari (M) Chats with the President of South Africa and Minister of Foreign Affairs, Mr Geoffery Onyeama during a side meeting at the 7th Tokyo International Conference on Africa Development (TICAD in Yokohama Japan. PHOTO; SUNDAY AGHAEZE. AUG 28 2019

BENIN PRESIDENT

PRESIDENT BUHARI PRESIDENT OF SOUTH AFRICA. President Muhammadu Buhari RECEIVED the President of Benin, H.E Patrice Talon during a side gathering at the seventh Tokyo International Conference on Africa Development (TICAD in Yokohama Japan. Photograph; SUNDAY AGHAEZE. AUG 28 2019

PRESIDENT BUHARI PRESIDENT OF SOUTH AFRICA 0A. President Muhammadu Buhari RECEIVED the President of Benin, H.E Patrice Talon during a side meeting at the 7th Tokyo International Conference on Africa Development (TICAD in Yokohama Japan. PHOTO; SUNDAY AGHAEZE. AUG 28 2019

PRESIDENT BUHARI PRESIDENT OF SOUTH AFRICA. President Muhammadu Buhari Chats with the President of Benin, H.E Patrice Talon during a side gathering at the seventh Tokyo International Conference on Africa Development (TICAD in Yokohama Japan. Photograph; SUNDAY AGHAEZE. AUG 28 2019

PRESIDENT BUHARI PRESIDENT OF SOUTH AFRICA 1B. President Muhammadu Buhari Chats with the President of Benin, H.E Patrice Talon during a side meeting at the 7th Tokyo International Conference on Africa Development (TICAD in Yokohama Japan. PHOTO; SUNDAY AGHAEZE. AUG 28 2019

PRESIDENT BUHARI PRESIDENT OF SOUTH AFRICA. President Muhammadu Buhari got the President of Benin, H.E Patrice Talon and his appointment during a side gathering at the seventh Tokyo International Conference on Africa Development (TICAD in Yokohama Japan. Photograph; SUNDAY AGHAEZE. AUG 28 2019

PRESIDENT BUHARI PRESIDENT OF SOUTH AFRICA 2. President Muhammadu Buhari received the President of Benin, H.E Patrice Talon and his delegation during a side meeting at the 7th Tokyo International Conference on Africa Development (TICAD in Yokohama Japan. PHOTO; SUNDAY AGHAEZE. AUG 28 2019

PRESIDENT BUHARI PRESIDENT OF SOUTH AFRICA 3. President Muhammadu Buhari got the President of Benin, H.E Patrice Talon during a side meeting at the seventh Tokyo International Conference on Africa Development (TICAD in Yokohama Japan. Photograph; SUNDAY AGHAEZE. AUG 28 2019

PRESIDENT BUHARI PRESIDENT OF SOUTH AFRICA 3. President Muhammadu Buhari with the President of South Africa, H.E Cyril Ramaphosa during a side meeting at the 7th Tokyo International Conference on Africa Development (TICAD in Yokohama Japan. PHOTO; SUNDAY AGHAEZE. AUG 28 2019

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

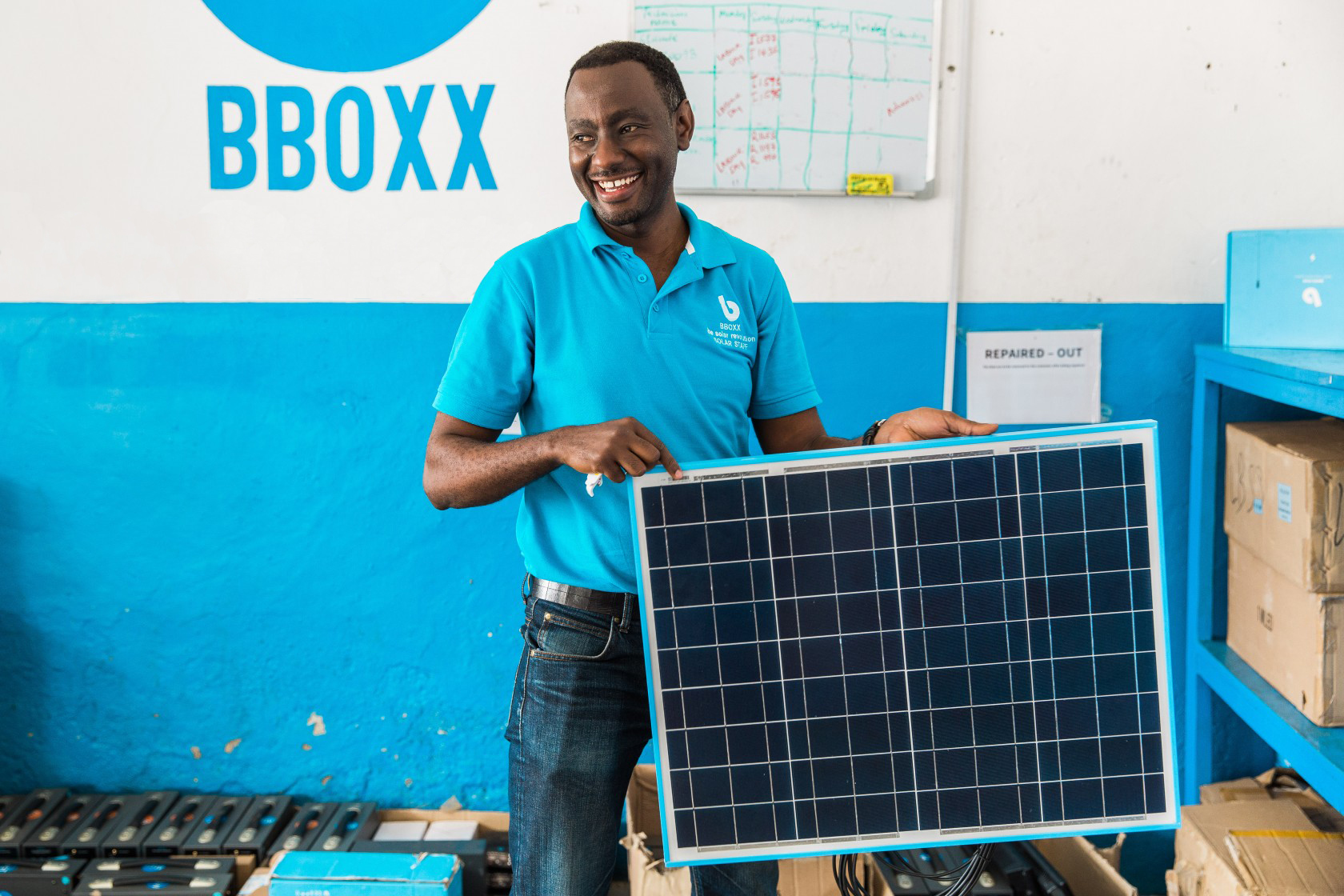

London-based startup BBOXX has been in Africa since 2010 and has installed about 200,000 home solar systems across Africa so far. Still determined to make more impact, the startup has now raised $50 million investment led by Japanese industrial giant Mitsubishi, marking another major funding milestone in the off-grid solar market.

Here Is The Deal

The funding was led by Japanese industrial giant Mitsubishi.

Mitsubishi’s investment into the UK-based pay-as-you-go solar provider is another funding milestone for the off-grid market.

Other investors include Engie, the French energy giant that’s made other off-grid solar investments, including its 2017 acquisition of East African home solar installer Fenix International; Luxembourg-based investment fund Bamboo Capital Partners; Dutch investment fund DOEN Participaties; and Canadian growth equity fund MacKinnon, Bennett & Company (MKB).

The funds will help BBOXX, which operates in Rwanda, Kenya, Togo and the Democratic Republic of the Congo, to break into new African markets, where an estimated one in three people live without reliable access to electricity.

The startup also plans to use the new funding to target new markets in Asia, where it has already opened an office in Karachi, Pakistan.

Roughly 600 million of Africa’s 1.2 billion residents lack grid electricity, making it a key market for off-grid solutions featuring the increasingly cost-effective tools of solar panels and wireless payment plans.

BBOXX’s largest rival, Fenix International, supplies 500,000 homes and was acquired by Engie in late 2017.

What BBOX Stands To Gain From The Investment

Mansoor Hamayun, BBOXX’s chief executive and co-founder, said Mitsubishi’s “extensive reach” and “technological expertise” would help the company to supply more people living without access to modern utilities and services.

“The funding is further evidence of Japanese interest in Africa and in PAYG [pay as you go] solar energy globally,” he said.

“We look forward to this next phase of growth that will help us to transform more lives, unlock potential and grow our already global footprint by opening up new markets, and develop our product range,”Hamayun said.

Mitsubushi’s power solution group operated about 6 gigawatts of net generation capacity globally as of mid-2019, including some wind and solar generation and energy storage.

About BBOXX

BBOXX, an Imperial London College spinout launched in 2010, has installed about 200,000 home solar systems across Africa, many of them coffee and vanilla bean farmers living off-grid. It networks its solar systems and inverters via its Pulse monitoring technology which allows BBOXX and its rivals to use mobile money to charge customers a monthly fee for the use of mini solar panels and ultra-efficient lighting strips. The fixed-period contracts usually run for about two years, until the equipment is paid off.

Customers can then choose to keep their existing kit and use the electricity for free, or upgrade their system to include more panels and extra appliances under a new contract.

2014 shares of renewables of regional total primary energy supply — Source: IEA

Earlier this year, BBOXX sold a 50% stake in its Togo-based business to EDF Energy in return for funding to help grow the company.

BBOXX hasn’t made batteries a central part of its offering, although it does offer a small, 650 watt-hour system linked with a 300-watt solar array for “households and microbusinesses with unreliable grid connections.”

It does offer liquified petroleum gas (LPG) stoves and canisters filled with biogas under a similar pay-as-you-go program, to allow them to replace more expensive and polluting cooking and heating fuels.

A Look At Global Investment In Off-Grid Startups

According to a March report from Wood Mackenzie Power & Renewables and Energy4Impact, investment in off-grid energy access — primarily residential solar to power lights, cellphones and other household devices, but including microgrids that power entire communities — has risen from nearly nothing in 2010 to a total of nearly $1.7 billion at the end of 2018.

Startups distributing solar-based energy products to those not adequately served by the conventional electric grid in Sub-Saharan Africa and South Asia have raised $1.3 billion since 2013, largely from family offices and development finance institutions seeking to combine profits with impact.

More than $1.2 billion of this investment has occurred over the past two years. A growing share of this money is coming from corporate strategic investors, ranging from oil and gas majors like Shell and Total, European utilities like Engie and EDF, and energy technology providers like Schneider Electric.

Overall, the solar home system market has raised more than $1.1 billion through 2018. Some of the biggest investments include Zola Electric (formerly Off Grid Electric) with $261 million, M-Kopa Solar with $194 million, D.Light with $188.5 million, Lumos with $108 million, Greenlight Planet with $82 million, and Mobisol with $79 million.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

.png?w=680&ssl=1)