AGCO Group has revealed plans for further development of the Future Farm project in Zambia. This was announced on 31 July 2019, at the 150ha farm outside Lusaka by Gary Collar, AGCO Senior Vice President and General Manager, Asia Pacific and Africa (APA) and the Future Farm Senior Manager, Kalongo Chitengi, during a groundbreaking ceremony attended by Her Royal Highness Senior Chieftainess Nkomeshya Mukamambo II; Chongwe District Commissioner, Mr. Robster Mwanza and Doreen Bailey, Political and Economic Section Chief at the US Embassy in Zambia.

Upgrades for Phase II will include the construction of student and staff accommodation with 24 rooms, communal amenities such as a canteen that sits over 80 people and an Insaka homestead – a traditional complex of grass gazebos with a central courtyard to encourage interactive learning. The second phase of the Future farm will also include upgrades to the existing road and farm infrastructure and digitizing the mechanization and agronomy training material to ensure that this knowledge is accessible even to farmers in remote parts of the continent.

Guests were welcomed by Nuradin Osman AGCO Vice President and General Manager, Africa who emphasized the significance of AGCO’s Africa strategy to empower the continent’s farmers as global Agri-preneurship shifts focus to see Africa as the answer to global agricultural expansion and food security. This is in line with AGCO’s vision for its business operations in Africa to develop and support a sustainable food production system, increase farm productivity by implementing modern farming techniques and develop a range of training courses for farmers, machine operators, and dealers.

“When we conceptualized the Future Farm, our aim was to be a catalyst in the development of a sustainable and prosperous agricultural industry across the continent, with innovative solutions built around the needs of African farmers,” explained Gary Collar. “To achieve this we are designing our solutions with Africa in mind and ensuring that we can support our products and customers, locally.”

While a project such as the Future Farm is committed to advancing African farmers to be owners of profitable agribusinesses, AGCO understands that the private sector cannot achieve a sustainable agricultural sector in Africa alone. There are other constraints slowing the speed of progress in Africa that need to be tackled in parallel with Governments.

“African Governments must look at agriculture beyond the development agenda, but rather as a profitable industry that can boost the region’s economy,” explained Nuradin Osman.

The Government of the Republic of Zambia has identified Agriculture as central to its job creation and poverty alleviation strategy as the sector employs over 70% of the population and contributes 19% of the country’s GDP. The government is engaged in projects aimed at increasing the volume and value of Agricultural outputs produced and sold – particularly by small-hold farmers.

“I am so pleased that this development is happening in my chiefdom, for which agriculture is the main occupation. The AGCO tractor hire service and training piloted in my chiefdom have shown how better crop yields can be achieved and have already been positive for some of the farmers,” noted her Royal Highness Senior Chieftainess Nkomeshya Mukamambo II.

The cutting edge training facility was first launched in 2015 with an initial investment of 9 million US dollars and is designed to demonstrate the value of mechanization and best agronomy practices for both small and large scale commercial farming operations.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

The Basketball Africa League (BAL) today announced Cairo (Egypt), Dakar (Senegal), Lagos (Nigeria), Luanda (Angola), Rabat (Morocco) and either Monastir or Tunis (Tunisia) as the host cities where the inaugural BAL regular season will take place and Kigali (Rwanda) as the host city for the first-ever BAL Final Four and BAL Final.

Additionally, the BAL announced NIKE and Jordan Brand will be the exclusive outfitter of the new professional league featuring 12 club teams from across Africa and scheduled to begin to play in March 2020.

The announcements were made by BAL President Amadou Gallo Fall during a reception at the Musée des Civilisations Noires in Dakar in the presence of FIBA Secretary General Andreas Zagklis, FIBA Africa Executive Director Alphonse Bilé, NBA Commissioner Adam Silver and NBA Deputy Commissioner Mark Tatum, along with current and former NBA and WNBA players.

“Today’s announcements mark another important milestone as we head into what will be a historic first season for the Basketball Africa League,” said Fall. “We now have seven great host cities where we will play and our first partnership with a world-class outfitter. We thank our first partners NIKE and Jordan Brand for supporting us on this journey and ensuring our teams have the best uniforms and on-court products.”

Beginning in March 2020, the six cities will host a regular-season that will feature 12 teams divided into two conferences, with each conference playing in three cities. The regular season will see the 12 teams play five games each for a total of 30 games, with the top three teams in each conference qualifying for the playoffs. The six playoff teams – the “Super 6” – will play in a round-robin format to determine the four teams that will advance to the BAL Final Four and BAL Final in Kigali, Rwanda in late spring 2020. The BAL Final Four and BAL Final will be single-elimination games.

NIKE and Jordan Brand will outfit the league’s 12 teams with official game uniforms, warmup apparel, socks and practice gear, with six teams featured in NIKE and the other six teams in Jordan Brand. The collaboration with NIKE and Jordan Brand marks the BAL’s first partnership.

The announcement about the NBA and FIBA’s launch of the BAL, which would mark the NBA’s first collaboration to operate a league outside of North America, was made at the NBA All-Star 2019 Africa Luncheon in Charlotte, North Carolina on Saturday, Feb. 16.

The NBA and FIBA also plan to dedicate financial support and resources toward the continued development of Africa’s basketball ecosystem, including training for players, coaches and referees, and infrastructure investment.

Additional details about the BAL will be announced at a later date.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

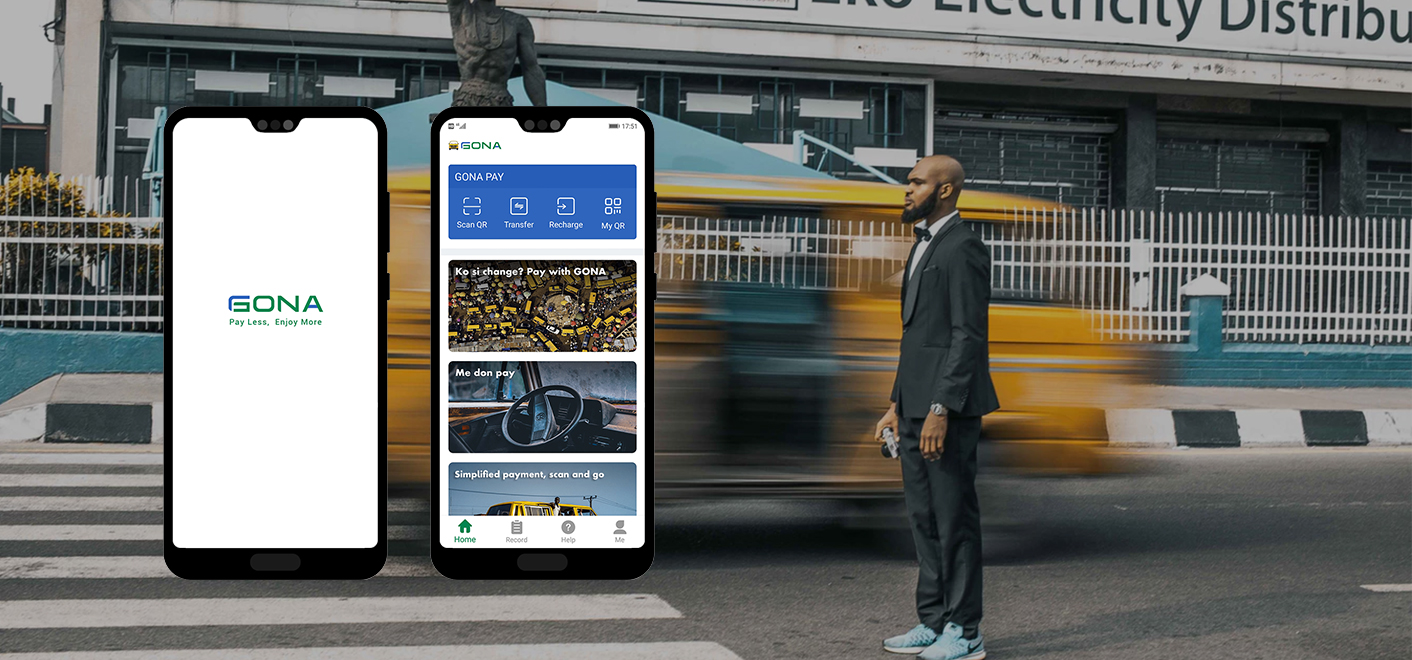

More Africa-focused startups are raising funds to either expand or grow their businesses this year. Apart from Opay’s recent funding round, GONA, the Chinese startup that offers cashless bus services and payment solutions with a focus on the Nigerian market is the latest to join the bandwagon.

This is remarkable because it shows that the African startup ecosystem is gradually fusing into the global startup ecosystem.

Here Is The Deal

News website, c.m.163.com says the Chinese-led investment came from Crystal Stream Capital, UnityVC and Shaka VC.

According to Liu Xiaojun, the founder and CEO of GONA the round of financing will be used for team building and product technology upgrades.

This new investment will further allow GONA to employ more locals to help develop the product and expand its popularity.

“We will try to employ the best people to help the most Lagosians have a better daily commuting experience,” says co-founder, Noah Gu.

Larry, a partner at ShakaVC, notes that the minibus scene provides more efficient and convenient travel services for hundreds of millions of Africans, and the market potential is huge.

As the first Chinese fund to focus on early African investment in Africa, ShakaVC will support the development of GONA in local resources, experience, and capital.

GONA boasts of thousands of active users and nearly 10,000 transactions every day.

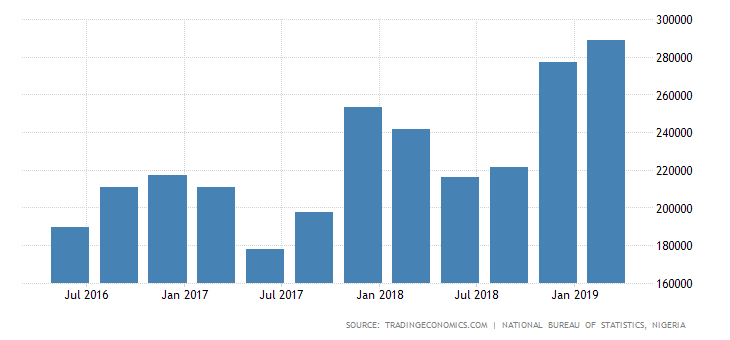

GDP From Transport in Nigeria increased to 288637 NGN Millions in the first quarter of 2019 from 277338.67 NGN Millions in the fourth quarter of 2018. GDP From Transport in Nigeria averaged 198649.70 NGN Millions from 2010 until 2019, reaching an all-time high of 288637 NGN Millions in the first quarter of 2019 and a record low of 144848.60 NGN Millions in the first quarter of 2010.

What GONA Does

GONA is a mobile payments platform with primary operations in Lagos.

GONA is enabling cashless payments on ‘informal transit’ public buses in Lagos and is also working to solve the pains of inconvenience in the local travel market. This it is doing by using technical means to improve operational efficiency.

‘‘The Rains Are Here, You deserve a less stressful bus ride to work. Pick up your smartphone and purchase a ticket on GONA, monitor the closest buses to you and hop onto one. Pay for your ride in style, avoid the chaos of “No Change”, Gona tweeted.

The startup recently announced the completion of a multi-million dollar Pre-A round of financing.

Even though GONA is headquartered in China, Lagos remains its primary focus. In Lagos, GONA has fully completed localization, with roll-out in certain routes within Lagos, one of which is Yaba to the University of Lagos (UNILAG) campus.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Less than a year after its first round of venture funding, the Canadian Clearbanc, a startup which provides funding for other startups to spend on marketing and customer acquisition, has secured $300 million Series B financing round on Wednesday. This is record-breaking for a startup that just raised $70 million in December 2018.

The round was led by Highland Capital and existing investors Inovia and Emergence Capital.

Canada-based Clearbanc, which was pitched as an alternative to traditional venture capital funding, last raised $70 million in December.

See the pitch deck the Clearbanc team used to get traditional venture investors on board with its unconventional sales pitch.

Clearbanc is betting that venture capital is the next in line for disruption, and they just raised $300 million in venture funding to prove it.

The Canadian startup, which provides funding for other startups to spend on marketing and customer acquisition, announced Wednesday a $300 million Series B financing round led by Highland Capital, Inovia, and Emergence Capital. The financing portion of the round was led by Arcadia Funds with participation from Upper90 Ventures.

Clearbanc pitches itself as an alternative to venture capital for startups spending heavily on things like Facebook and Google ads, and this is its second venture funding round in less than a year. According to Pitchbook data, the company closed a $70 million Series A in December.

Clearbanc claims to automate the pitching process using a machine learning model that can supply companies with anywhere from $10,000 to $10 million in funding instead of giving up a portion of the company to an investor just to turn around and spend the funds on ads. This model works particularly well for e-commerce startups that need to get in front of new customers to grow, according to Gary Vaynerchuk, CEO of VaynerMedia and Clearbanc investor.

So how was the Clearbanc team able to sell traditional venture investors on a model that is in direct competition with their own? Here’s the pitch deck that convinced investors that disruption could be worth $300 million.

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Following an open tender and a highly competitive international bidding process, the African Development Bank through its African Legal Support Facility (“ALSF”) and the National Petroleum and Gas Commission, representing the government of the Republic of South Sudan, selected the Centurion Law Group to build capacity in the Republic of South Sudan’s oil and gas sector.

The project is a result of the ALSF’s commitment to foster legal and technical best practices and transparency across South Sudan’s oil & gas value chain. It will focus on providing specialized capacity building training to officials from the National Petroleum and Gas Commission, including the development of best practice procedures for the negotiation, evaluation, and monitoring of contracts in the oil and gas sector.

As South Sudan continues to increase oil production – its most important export commodity – and attract foreign investment into its oil & gas sector, this project will enhance the National Petroleum and Gas Commission’s ability to fully exercise its functions as a regulator and a facilitator in the oil sector.

As per the South Sudan Petroleum Act of 2012, the National Petroleum and Gas Commission notably provides general policy direction with respect to petroleum resources, acts as a supervisory body in matters relating to petroleum resource management, approves all petroleum agreements on behalf of the Government and ensures that they are consistent with the Act.

“The National Petroleum and Gas Commission is a key institutional pillar of South Sudan’s oil & gas sector,” declared Hon. Caesar Oliha Marko, Chairperson of the Commission. “We are delighted to be working with a reputable firm like Centurion to enable our country’s oil industry to meet its obligation to our citizens and investors. Building capacity is key to us ensuring that we deliver on the promise of making oil work for everyone in South Sudan”.

The project will notably focus on reviewing South Sudan’s existing legal and fiscal framework and ensure the transfer of skills and know-how to the government’s representatives and experts.

“It is a real honor to have been selected for this project with the Petroleum Commission,” declared Nj Ayuk, CEO of the Centurion Law Group. “Local content development and domestic capacity building are at the core of everything we do as a firm. We take this project as a unique opportunity to contribute to the development of South Sudan and Africa’s oil industry in general. We are grateful to the African Development Bank and the Republic of South Sudan for entrusting us with this responsibility.”

“As a team, we truly believe in the role the National Petroleum and Gas Commission has in shaping the future of South Sudan’s oil & gas sector,” said Glenda Irvine-Smith Centurion’s Director of Business Development & International Relations, who will coordinate the project on behalf of Centurion.

“South Sudan in East Africa’s most mature petroleum province with the potential to double its current output of over 150,000 b/d in the next five years. Through CenturionPlus, our lawyers and experts on-demand platform, we will mobilize the best African and international experts for the benefit of South Sudan. We are honored to have been entrusted by the Commission and the African Development Bank to accompany South Sudan in this journey.”

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

Five months ago, Cyclone Idai ripped through the Southern African region, causing a massive humanitarian disaster that affected three million people. More than a thousand perished, while 200,000 lost their homes, many of whom are still to this day living in refugee camps.

Economic losses were estimated at more than $1 billion across the affected countries – Mozambique, Malawi, Zimbabwe, and Madagascar. However, the devastating impacts of such disasters – especially for Least Developed Countries (LDCs) and small states in Africa – tend to be deeper and more far-reaching than initial reports would indicate.

The consensus among scientists is that extreme weather events such as droughts, floods, cyclones, and landslides, are now occurring with increased frequency and greater intensity. There are long term consequences such as desertification, erosion of arable land, and changes in ecological balance, which can prove difficult to reverse. As a result of climate change, there is a heightened risk that while vulnerable Commonwealth states are recovering from one natural disaster, another will strike.

For instance, Mozambique was still reeling from the impact of Cyclone Idai in March when Cyclone Kenneth – the strongest in the country’s history – bore down barely six weeks later. In fact, there have been no fewer than 13 emergency events in Mozambique since 2015 (mirrored by 12 in neighboring Malawi). Indeed, 109 disasters recorded in the country over the past 50 years have incurred more than $1.15 billion in economic damage.

Statistics such as these demonstrate the vital importance for all our member countries of planning long term strategies to manage disaster risks and of building resilience through disaster preparedness, as was acknowledged by Commonwealth Heads of Government when they met in 2018.

They affirmed their commitment to the Sendai Framework for Disaster Risk Reduction – the international agreement for mobilizing governments, private sector, and other stakeholders to reduce risks and build resilience. By doing so, our leaders acknowledged that rather than merely responding after disaster strikes, it is more cost-effective and prudent to invest beforehand in prevention, protection, and preparation.

Yet disaster risk reduction remains a relatively low priority for international development finance. Apart from the costs of post-disaster reconstruction and response, of every $100 spent on international aid in the past two decades, only 40 cents have been spent on pre-disaster risk management.

Moreover, the field of disaster risk finance is complex and evolving, making it even harder for small states and LDCs to tap into the limited funding available. Information is fragmented, and donors and lenders often have widely varying procedures and requirements that need to be navigated in order to unlock finance.

Bringing clarity to disaster risk finance

To tackle these impediments, and to help create a more streamlined and integrated approach to accessing funds, the Commonwealth will soon be launching a new disaster risk finance portal. This web-based platform, designed to make it easier for capacity-constrained governments to gain access to the funding they so urgently need, will be ready for preview when our annual Commonwealth Finance Ministers Meeting, convenes in Washington DC this October with Cyprus in the chair.

As well as helping governments to find what disaster finance instruments are available, the portal will assist them in identifying those that are most suited to their particular needs and circumstances. A one-stop-shop, with information collated from a range of sources and clearly presented, will save governments time and effort, and help them to make more informed decisions on disaster preparedness and response.

The theme for our Commonwealth Finance Ministers Meeting – Avoiding Debt Crises – also strikes a chord, as disasters push many countries into taking on emergency loans to rebuild and recover. For most low and middle-income countries, such public debt easily becomes unsustainable and makes them vulnerable to the additional high risk of debt distress.

The Commonwealth has an impressive record of successful advocacy to bring to international attention the difficulties associated with managing debt issues – and of offering practical solutions. Last month, we launched Commonwealth Meridian, our state-of-the-art sovereign debt management software. It builds on the successes of the Commonwealth Debt Recording and Management System (CS-DRMS) which over recent years has been used by more than 100 agencies – including the finance ministries, treasuries and central banks of 60 countries – to manage more than $2.5 trillion of public debt.

This complements the work of the Commonwealth Finance Access Hub set up in 2016 to help small and vulnerable states make successful funding applications for projects that will help them adapt to climate change and mitigate its impact. To date, the hub has helped countries gain access to $25.3 million, with a further $367.4 million in the pipeline. It does so by embedding long term specialists within ministries to provide expert advice and to build local capacity for the longer term.

Tools such as these, together with many other projects and programmes and advocacy strategies, are components in a suite of support offered by the Commonwealth collectively so that all our members are better equipped and ready to cope with disasters, including those related to climate change.

Our combined Commonwealth purpose is to reduce the number of people being pushed into poverty and food insecurity by recurring natural disasters, and whose opportunities to share the benefits of inclusive and sustainable progress are impaired when economic growth falters.

Where the planning and wherewithal to assist people with recovery from trauma and to rebuild their lives is lacking, community cohesion and nation-building can also be severely compromised and set back. Without sustained action to mitigate risks and build resilience, hopes of achieving the Sustainable Development Goals by 2030 are slender.

By mobilizing multilateral action, particularly in support of those who are marginalized or more vulnerable, with the stronger working alongside the less secure, we are able to build defenses against disaster which may be needed by any of us at any time. So the Commonwealth shines as a beacon of hope for a more harmonious world, and for cooperation to sustain the health and well-being of our planet.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

Andrew Rinaldi, the co-founder of the all-in-one, SaaS-delivered cybersecurity platform Defendify, knows all too well what it takes to obtain startup funding. Rinaldi and Defendify recently secured $1.6 million in pre-seed funding to help get their business up and running. Defendify secured the money from private investors with participation from the Maine Technology Institute and early-stage cybersecurity industry investor 3dot6 Ventures. In this interview with Chad Brooks, he shares his deep wealth of experience.

Q: How do you know when it is time to raise funds?

A: Really, it’s just math. Through business planning — which, yes, we all have to do — you figure out what you’ll need to get started and grow. And with that comes identifying the funding required to make that a reality.

If you don’t have the requisite funding readily available, it’s time to look to other people. As things progress, your position will absolutely change over and over, but creating some early projections and forecasting — even if rough — paints the picture.

Q: How do you know you are ready for an investor, versus just asking family and friends for money?

A: You’ll need to extend the conversation to new resources just as soon as you’ve exhausted friends’ and family dollars, or if they’re simply aren’t any friends and family options for you.

The other primary driver for going beyond friends and family is for access to new opportunities and resources. Some call it “smart money,” where whoever is helping fund your cause also brings their expertise, networks and often vast resources to the table. That, together with the short- and long-term financial impact, can be a major catalyst for your business and is the perfect time to think beyond friends and family. [Are you actively seeking financing options for your business? Check out our reviews and best picks of business loans.]

How to find the right investor for your startup

Q: How do you find potential investors?

A: It’s all about networking. Start with family and friends, then move to your professional network. Who do they know that might be interested? … Through the course of that outreach and sharing your story over and over, you are then introduced to more and more people beyond your network, who I call your extended network, and eventually, find prospective investors that might align. Yes, you can conduct cold outreach as well, and we all do, but it’s the power of your network — and extended network — that nets you the most effective relationships.Q: How do you find potential investors?

Q: How do you know if an investor is right for you and your business?

A: There has to be alignment, and I would suggest that starts with your core values. It’s not all that different than how you might seek employees or partners that believe in you and your vision. They can’t just have a basic business or financial goals — they have to have a mindset and operate in a way that works for you and with you.

I’ll also say it’s really important to pay attention to your gut. Sometimes you just know innately if an investor is a good fit or not, and that absolutely should be taken into consideration.

Q: What should your proposal to an investor include?

A: I would say to look at a proposal to an investor more like you would a marriage than a business. Yes, you have to go through the practical motions and economics that make for a good fit, but in the end, it’s mostly about having a healthy, mutually beneficial relationship that can stand the test of time. If you can’t overcome adversity and subjectivity and ride through the trials and tribulations together, you won’t be successful — no matter how good an idea or product you might have.

Q: Once you secure an investment, what role does the investor play in your business?

A: It all depends on who the investor is. Some will be totally hands-off and just check in casually, perhaps no more than chatting at the backyard barbecue or over a coffee or beer. That’s commonly where family and friends fall. Others will want to dig in more regularly or even participate as operators, not only to understand how the business is progressing but to see where they can help.

The good news is, everyone with a vested interest genuinely wants to help. Building a business from the ground up requires all the help you can get. It may come in many different forms — financial, networking opportunities, new customers and partnerships, constructive criticism, or candid advice. Whatever the case, it’s always worth listening (and remember, you don’t have to do everything everyone asks of you). These are people who want you to succeed, believe in you, and care about you. One thing is for sure — you’re in it together.

Q: What are the benefits of getting funds from an investor versus taking out a traditional business loan?

A: Traditional business loans aren’t usually an option for early-stage startups. While some lenders promote working with startups, it’s rare they actually do. I recommend exploring nontraditional loan opportunities.

For example, we have an amazing relationship with the Maine Technology Institute, which fuels innovation by providing technology development loans with preferable terms to early-stage companies. Their goal isn’t to run up the bill with interest or lock you in for the day you go public, [but] rather see you through to success and generate local jobs and economic impact. Those kinds of opportunities are well worth pursuing and often more fruitful.

The primary benefit of funds from investors is availability. Investors are willing to bet on you, especially early on, in ways the banks or lenders will not and may not for many years to come. And once convinced to invest, they can move quickly to infuse capital into the business, which can be a huge benefit.

That includes the potential for follow-on funding when you need additional dollars. Now, that doesn’t mean investor funds are simply readily available out there in the world. Actually, it’s just the opposite. Raising funds from investors is a full-time job on top of your full-time job of building and running the business.

Rapid-fire questions

Q: What piece of technology could you not live without?

A: The most important thing about running and scaling a healthy business is effective communication. Slack is a great tool for everything from regular check-ins to timely company updates and even sharing a funny story or joke. Slack doesn’t replace in-person communication or meetings — nothing can — but it can help promote ongoing chatter, transparency, and visibility while minimizing interruptions and interference.

Q: What is the best piece of career advice you have ever been given?

A: Many years ago, when I was building my first business, one of my longtime mentors introduced me to the notion that I should stop working “in the business” and start working “on the business.” I hadn’t ever thought of things that way, but once I did, it changed my whole perspective.

Now it seems so obvious; however, the truth is we all get caught up “in the business” to varying degrees. This advice not only resonated when I first heard it but is something I come back to each and every day.

Q: What’s the best book or blog you’ve read this year?

A: I really enjoyed One Bullet Away by Nathaniel Fick (who happens to also now be a leading cybersecurity executive). On one hand, [it’s] an intense and detailed journey taking you through the harsh realities of war and military life, [and] at the same time a tremendous and thoughtful story about leadership and accountability.

Q: What’s the biggest risk you’ve taken professionally? Did it pay off?

A: Moving to Portland, Maine. Building my past business in Boston for many years, my wife and I would occasionally escape the city for weekend trips north. I’ve had the good fortune of traveling extensively in my life and couldn’t believe all that Portland and Maine had to offer, and just a couple of hours away. So, when I looked beyond the amazing restaurants, fascinating culture, great schools and outdoor life, I was pleasantly surprised to discover a sprouting startup, tech and creative community.

It’s no secret Maine hasn’t historically been considered a center for business impact. So, betting on Portland was a huge risk. But it’s paid off big. You’d be absolutely amazed at the people and resources that are around. Turns out it’s not all lobsters and potatoes.

There are a ton of very smart and uber-successful people in Maine, including a rapid influx of talent migrating away from the ever-increasing cost of living in big cities like Boston and New York. If anyone out there is considering taking the same risk and seeing how Maine can pay off, I’m more than happy to share the secret.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Time for early investors and startups in Kenya to leech onto the country’s blossoming petroleum industry! It is now safe to say that Kenya is now an oil-producing nation in the world, the only nation in the whole of East Africa, after South Sudan to actually export oil.

The country has just sealed its first oil export deal worth Sh1.2 Billion ($11.6m). With 60,000 to 100,000 barrels per day, Kenya is set to displace either Ghana, Brunei or Chad in the ranking of oil-producing and exporting countries by production capacity.

“We are now an oil exporter. Our first deal was concluded this afternoon with 200,000 barrels at a price of 12 million US dollars. So, I think we have started the journey and it is up to us to ensure that those resources are put to the best use to make our country both prosperous and to ensure we eliminate poverty,” Kenyan President Uhuru Kenyatta said

Here Is The Deal

This deal which is the first-ever in the whole of Kenya’s history saw Kenya selling off 200,000 barrels of oil at a price of Sh1.2 billion ($12m).

Kenya discovered commercial oil reserves in its Lokichar basin in 2012 and Tullow Oil estimates the basin to contain an estimated 560 million barrels in so-called 2C proven and probable oil reserves.

Tullow has said this would translate to 60,000 to 100,000 barrels per day of gross production.

Tullow Oil is a multinational oil and gas exploration company founded in Tullow, Ireland with its headquarters in London, United Kingdom. It has interests in over 150 licenses across 25 countries with 67 producing fields and in 2012 produced on average 79,200 barrels of oil equivalent per day.

Source: Statista 2019; Oil Production in Africa from 2001 to 2018 (in 1,000 barrels per day)

The government and Tullow Oil had expected to start exporting crude under the Early Oil Pilot Scheme (EOPS) by June this year but that appeared unlikely with the company only having trucked about half of the amount that will be needed for the first shipment.

In May, Kenya’s Ministry of Petroleum said about 88,000 barrels of oil had so far been trucked to Mombasa and was targeting to accumulate 200,000 barrels that would form the first export cargo.

The oil that has been ferried to Mombasa was produced in 2015 during an extended well testing exercise. By end of March, Tullow had shipped all the oil stored in Lokichar and has been setting up an Early Production Facility, which will produce 2,000 barrels a day.

Currently, major oil producers in Africa include Nigeria (0.0449), Libya (0.0101), Egypt (0.0418) and Algeria (0.0913), producing a total of 0.1881 trillion cubic feet of gas cumulatively which is 5.4 percent of the world’s total production.

In 2018, Africa’s total oil production amounted to around 8.19 million barrels of oil per day.

Africa’s production rate is, however, decreasing at a rate of 1.1 percent per annum. Africa’s consumption rate is at 138.2 billion cubic meters at a growth rate of 1.4 percent. It would take Africa 68 years to completely deplete its reserves.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

PRESIDENT BUHARI RECEIVES ILO TEAM 0A&B; President Muhammadu Buhari addresses the Director-General of International Labour Organisation, (ILO), Mr. Guy Ryder and his team during an audience with the President at the State House Abuja. PHOTO; SUNDAY AGHAEZE. AUGUST 1 2019.

PRESIDENT BUHARI RECEIVES ILO TEAM 0A&B; President Muhammadu Buhari addresses the Director-General of International Labour Organisation, (ILO), Mr. Guy Ryder and his team during an audience with the President at the State House Abuja. PHOTO; SUNDAY AGHAEZE. AUGUST 1 2019.

PRESIDENT BUHARI RECEIVES ILO TEAM 4; R-L; Chief of Staff, Mallam Abba Kyari, President Muhammadu Buhari in a handshake with the Director-General of International Labour Organisation, (ILO), Mr Guy Ryder, Director ILO Country office of Nigeria, Mr Dennis Zulu, Ms Cynthia Samuel-Olonjuwon during an audience with the President at the State House Abuja. PHOTO; SUNDAY AGHAEZE. AUGUST 1 2019.

PRESIDENT BUHARI RECEIVES ILO TEAM 6; President Muhammadu Buhari in a handshake with Mr. Yasser Hassan. Others are Director ILO Country office of Nigeria, Mr. Dennis Zulu, Ms. Cynthia Samuel-Olonjuwon, UN Resident Coordinator, Edward Kallon and Director-General of International Labour Organisation, (ILO), Mr. Guy Ryder (R) during an audience with the President at the State House Abuja. PHOTO; SUNDAY AGHAEZE. AUGUST 1 2019.

PRESIDENT BUHARI RECEIVES ILO TEAM ; R-L; Permanent Secretaries, SGF Mr. Boss Mustapha, Chief of Staff, Mallam Abba Kyari, President Muhammadu Buhari in a handshake with the Director-General of International Labour Organisation, (ILO), Mr Guy Ryder, Director ILO Country office of Nigeria, Mr Dennis Zulu, Ms Cynthia Samuel-Olonjuwon Mr Yasser Hassan. UN Resident Coordinator, Edward Kallon during an audience with the President at the State House Abuja. PHOTO; SUNDAY AGHAEZE. AUGUST 1 2019.

PRESIDENT BUHARI RECEIVES ILO TEAM 7; President Muhammadu Buhari in a handshake with NLC President Comrade Ayuba Wabba. Others are Director ILO Country office of Nigeria, Mr. Dennis Zulu, Ms. Cynthia Samuel-Olonjuwon and Mr. Yasser Hassan during an audience with the President at the State House Abuja. PHOTO; SUNDAY AGHAEZE. AUGUST 1 2019.

SUNDAY AGHAEZE( HND Mass Comm, PGDBA) PERSONAL ASSISTANT TO THE PRESIDENT International Photojournalist +234-803-3031520, 0805-2039160 email; suaghaeze@gmail.com aghaezesun@gmail.com

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

Zimbabwe is set to repeal the Indigenisation and Economic Empowerment Act as the country moves to enhance the attractiveness of the minerals sector to foreign direct investment (FDI). This is remarkable because it is the first time in 11 years since foreign investors stopped owning 100% stakes in companies they set up in Zimbabwe. For the economy, this is by far a direct way of telling investors to come to do business in Zimbabwe.

Here Is The Deal

Under the new arrangement, the Indigenisation and Economic Empowerment Act will be replaced by a more “business-friendly” Economic Empowerment Act, but in the interim, the Indigenisation Act has been amended to remove the critical diamond and platinum sub-sectors from the reserve list.

“Government, through the 2018 Finance Amendment Bill amended the Indigenisation and Empowerment Act and platinum and diamonds are now removed from the reserve list and shareholding will depend on negotiations with investors.

“Subsequently, the Indigenisation and Economic Empowerment Act will be repealed and replaced by the Economic Empowerment Act, which will be consistent with the current thrust “Zimbabwe is Open for Business,’’ Zimbabwe’s Finance and Economic Development Minister Mthuli Ncube, was quoted as saying while presenting the Mid-term Fiscal Policy Review statement and Supplementary Budget in Parliament yesterday.

The Indigenisation Act which is due for repeal requires foreign companies to give shareholdings of up to 51% in joint ventures to local partners.

The Implication Of The Intended Repeal

This repeal is expected to be revolutionary. First, it now means that local shareholding will depend on agreed terms by investors, while foreign shareholding can reach up to 100 percent.

Then again, it means that foreign investors can now work under an environment with less threat of breach of contract.

Such threats had a negative effect on the global investor community on Zimbabwe as a breach of contracts is anathema to investors.

The mining sector remains a key driver of Zimbabwe’s economic development, typically contributing circa 10 percent to the country’s gross domestic product (GDP) and around 60 percent to exports.

And true to form, during the first half of the year, the sector contributed US$1.3 billion, about 68 percent of the total exports of US$1,9 billion during the period.

The scrapping of the Indigenisation and Economic Empowerment Act is one of the measures that is expected to provide impetus to the economic contribution of the sector.

Expect More Foreign Direct Investment In The Zimbabwe Mineral Sector

The Indigenisation Act has already been amended to remove the critical diamond and platinum sub-sectors from the reserve list. The rest of the minerals have also been removed from the list.

The Indigenisation and Economic Empowerment Act worked to discourage and alienate much-needed FDI and investment as the way it was implemented threatened business.

Around 2013, the indigenization programme shook a lawfully and morally binding agreement between Zimbabwe’s largest platinum producer, Zimbabwe Platinum Holdings (Zimplats) and Government.

Comprehensive Strategy Already In Place for All Foreign Companies

The Zimbabwean government has over the past several months secured a number of mining investment deals, with the latest being a joint venture agreement between State-owned diamond miner, the Zimbabwe Consolidated Diamond Company and Russian firm, Alrosa.

The new diamonds agreement will see about US$12 million being invested in the exploration of diamond deposits over the next three years.

Minister Ncube yesterday said that Government will put in place a “comprehensive strategy” to see the coming into fruition of these deals.

“These investments will, however, take some time (up to 10 years of production) to give visible net benefits in view of long gestation periods for mining projects.

“Government will, therefore, in the second half of the year unveil a comprehensive strategy and roadmap towards a US$12 billion mining industry by 2023,” he said.

“The attainment of this milestone is not an event, but a process, which is well underway with concrete start-ups and expansion of projects in a number of minerals, which include platinum, gold, ferrochrome, coal and hydrocarbons, lithium, diamonds, iron ore, among others.”

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.