The Fitch rating, of the African Development Bank, published 24th July in London, is affirmed as AAA, with a stable outlook, on improved assessments, qualifications, and estimates. The rating provides a significant boost for the Bank at a time when it is discussing a substantial general capital increase to finance its strategy and activities over the next few years.

Fitch Ratings is one of the leading global providers of credit ratings, commentary and research. The agency upgraded the intrinsic assessment to ‘aa’ from the previous ‘aa’-driven by an improvement in Fitch’s assessment of the Bank’s business environment.

The Bank’s ‘aaa’ support from its shareholders was based on Fitch’s forecasts that the Bank’s net debt will be fully covered by callable capital from ‘AAA’ rated member countries by 2021.

The projection assumes shareholder approval of an increase in subscribed capital from 2020, and lending growth averaging 7% year on year in 2019-2021.

Other key points from the Fitch rating include the following:

The Bank’s solvency assessment of ‘aa’ primarily reflects its ‘strong’ capitalization.

The equity to asset and guarantees ratio remains within the ‘strong’ range.

Fitch’s usable capital to risk-weighted assets (FRA) ratio, newly introduced, was just below the threshold for an ‘excellent’ assessment (35%) at end-2018 and is likely to be ‘excellent’ in 2019.

The overall risk is rated as ‘low’, with risk management policies seen as conservative and assessed as ‘excellent’.

Concentration risk is considered ‘low’ and has benefited from the Exchange Exposure Agreement with other development finance organizations.

Equity participation is expected to remain below 5% of the banking portfolio by 2021, in line with the internal limit of 15% of risk capital.

FX and interest rate risks are very limited and conservatively managed.

The liquidity assessment is ‘aaa’ and the quality of liquid assets is ‘excellent’.

The Bank’s business environment now translates into no negative adjustment (from a one-notch negative adjustment previously) to the improved intrinsic rating, which reflects a stronger assessment of the bank’s strategy to ‘medium’ risk from ‘high’ risk.

The Bank’s outlook is rated as Stable.

As the Fitch rating states, the process for a General Capital Increase (GCI-VII) is expected to be completed by end-2019, including a final agreement on its amount.

The President of the African Development Bank, Akinwumi Adesina welcomed the assessment and said, “I am delighted by the affirmation of the AAA rating as well as the accompanying explanations, which clearly explain the solid and comprehensive reasons for the overall improvements in the intrinsic rating, as well as the ‘extraordinary support’ we receive from our shareholders. It is a massive boost for the Bank to be encouraged so strongly in the year of the General Capital Increase and with so much hard evidence provided.”

He added that “It is also a tribute to all our stakeholders, partners, and those who have been working at and with the Bank during this past year. Fitch’s rating is not just about our credit; it speaks volumes for the Bank’s solid achievements, consistent strategy, development impact, leadership, and overall direction.”

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

A veteran exporter of Kenyan fresh fruits and vegetables and a young South African farmer specializing in the design, provision, and management of indoor and outdoor hydroponic systems, were the winners of this year’s youth AgriPitch competition, organized by African Development Bank in partnership with the Western Cape Government in South Africa.

The event which is the 2019 youth AgriPitch Competition themed “Climate Smart Agriculture: Business and Employment Opportunities for Africa’s Youth” took place in Cape Town, South Africa from 24th to 28th July.

Kenyan Alex Muli, CEO, and Co-Founder of Goshen Farm won $25,000 for best agribusiness in the mature start-up category, while Paul Sheppard, from South Africa, Co-Founder of Future Farms, took the $10,000 prize for the early start-up category.

“It was a great event. I met many pioneers in the various agri-tech spaces with many potential and exciting projects, with the renewed hope of access to finance models coming to the fore. The prize money will help our company to upscale to the size we want to grow to, as well as meeting potential investors and learning more about the industry,” said Sheppard.

Muli, who co-founded Goshen farms with his mother in 2011, said it was exciting to be shortlisted as agripreneur in the Mature Startups category. “The boot camp was a great learning experience for me and helped me to know how to better tell the story about my business. I was humbled to meet fellow agripeneurs from other African countries who are doing great stuff out there hence rewriting our continent’s story, a story of hope, transformation, and sustainability by young Africans for Africa,“ he said.

Over 400 agribusiness proposals from across the continent participated in the AYAF competition, which culminated in an award gala dinner, where six winners from the two categories received a total of U$ 74,000.

This AgriPitch Competition was part of a larger forum, the African Youth Agripreneurs Forum (AYAF) an annual forum of the African Development Bank’s flagship, Enable Youth Program, which focuses on youth employment and food insecurity.

“At the African Development Bank, we believe that the future of the continent’s youth lies in more rapid and inclusive economic growth which creates quality jobs. This is why the Bank has developed a number of key programs, such as Enable Youth and the Jobs for Youth in Africa Strategy. To date, the Bank has committed over $350 million to Enable Youth investments in 12 countries on the continent, “said Dr. Edward Mabaya, Manager, Agribusiness Development Division at the African Development Bank.

The forum provided a platform for youth agripreneurs and key stakeholders to brainstorm with experts, business leaders, investors and policymakers on issues that affect youth employment and key solutions to addressing these.

It also served as a call to action to support innovative agriculture growth through intense engagement and mentorship for small and medium enterprises and emphasized that with greater support and opportunities to set up their agribusiness enterprise, youth can become the driving force of Africa’s agriculture transformation.

Sponsors of the 2019 AgriPitch Competition and African Youth Agripreneurs Forum include the Bank’s Youth Entrepreneurship and Innovation Multi-Donor Trust Fund (funded by The Netherlands, Demark, Italy, Sweden, and Norway); the Western Cape Government’s Department of Agriculture; The Korea-Africa Economic Cooperation Trust Fund; and The Africa Climate Change Fund.

“We strive to disrupt the African Agricultural ecosystem the way we do best by creating resilient markets for our agricultural produce. We will be there soon,” Muli said.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

Ethiopia is on course to liberalize its economy. Apart from opening bids for its first-ever privately owned telecom license, foreigners who are not citizens of Ethiopia may soon get a law that would allow them to set up and run insurance services as well as set up microfinance banks.

Here Is The Deal

Two draft bills that aim to restructure the country’s existing business law governing insurance companies and microfinance institutions have been passed by Ethiopian Council of Ministers.

The bills would definitely scale through and be passed into law since they were developed by the National Bank of Ethiopia and endorsed by the Ethiopian Council of Ministers.

What is just remaining is for the Ethiopian House of People’s Representatives, the Ethiopian parliament’s lower house, to which it had been forwarded to, to put its final ratification on it.

Under the new law, all that is needed, among other things, for a foreigner to set an insurance or microfinance business is for the foreigner to be a foreign national of Ethiopia.

This is part of restructuring Ethiopia’s current laws on insurance and microfinance sectors, according to the Ethiopian PM’s office.

The decisions to amend the East African country’s existing business laws governing insurance companies and microfinance institutions were made in line with recent and ongoing “large-scale” reform measures in the sectors, the Ethiopian Prime Minister’s Office revealed in a statement.

Here Is The Change These New Laws Are Bringing To The Table

Article 656 of the Ethiopian Commercial Code provides that the law shall determine the conditions under which physical persons or business organizations may carry on insurance business.

Recourse is however made to other parts of the commercial code and other laws to find out as to who may undertake insurance business and the conditions under which it may be undertaken in Ethiopia.

Accordingly, Article 513 of the commercial code provides that banks and insurance companies cannot be established as private limited companies, i.e., a private limited company cannot engage in banking, insurance or any other business of similar nature.

Similarly, Article 6(1) of the Licensing and Supervision of Insurance Business Pro No 86/1994 provides that no person may engage in the insurance business of any type unless it applies to and acquires a license from the National Bank of Ethiopia for the particular class or classes of insurance.

Furthermore, Article 4(1) and Art 2(3) of the same proclamation provide that such person has to be a share company as defined under Article 304 of the commercial code.

These requirements/conditions in effect prevent foreigners from engaging in the insurance business and foreign banks from opening branches and operating in Ethiopia.

The most probable reason for this position is the need to protect infant domestic insurance companies which do not have the desired financial strength, know-how, and human resources to be able to compete with foreign banks which have the superior capacity in these areas.

The new laws, therefore, are preparing to change all these.

Under the new law, all that is needed, among other things, for a foreigner to set an insurance or microfinance business is for the foreigner to be a foreign national of Ethiopia.

Freeing Up The Economy

Ethiopia has also recently announced that government would no longer be monopolizing its telecom sector. At the moment, there is no MTN, Airtel, Safaricom, Vodafone or any other mobile telecom operator in the East African country of Ethiopia, but that will no longer be the case before this year ends. The country is set to award its first set of telco licenses to multinational mobile companies by the end of 2019.

Before this happens, Ethiopia’s government has continually monopolized the country’s telecom industry. Hence, this is expected to end a state-wide monopoly and open up one of the world’s last major closed telecoms markets.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

The World Economic Forum on Africa 2019 Start-ups Programme in Cape Town, South Africa, aims to tackle these issues by focusing on how to scale up the transformation of regional architecture related to innovation, cooperation, growth, and stability.

Under the theme, Shaping Inclusive Growth and Shared Futures in the Fourth Industrial Revolution, the 28th World Economic Forum on Africa will convene more than 1,000 regional and global leaders from politics, business, civil society, and academia to shape regional and industry agendas in the year ahead.

The 28th World Economic Forum on Africa aims to tackle these issues by focusing on how to scale up the transformation of regional architecture related to smart institutions, investment, integration, industry, and innovation.

Under the theme, Shaping Inclusive Growth and Shared Futures in the Fourth Industrial Revolution, the meeting will address the African Union’s Agenda 2063 regional strategic priorities under four programme tracks:

Innovation: Readiness for the Fourth Industrial Revolution

Cooperation: Sustainable Development & Environmental Stewardship

Growth: Digitalization & Competitive Industries

Stability: Leadership & Institutional Governance

Criteria – Be less than 10 years old – Have received more than $1 million in funding – Be headquartered in Africa and/or with a primary market focus on Africa – Be developing a product or service that makes a substantial long-term positive impact on business and society – Be considered a high-potential company in their field with a disruptive business model or significant product or service innovation – Not be a subsidiary or a joint venture – The chief executive officer/founder must represent the start‑up at the World Economic Forum on Africa 2019

The 28th World Economic Forum on Africa will be held on 4–6 September 2019 in Cape Town, South Africa.

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Access Bank and GE Healthcare are to provide sustainable healthcare equipment financing to private healthcare providers; The partnership will help the private healthcare providers to deliver access to affordable healthcare services.

Access Bank will provide access to loans for eligible healthcare providers, while GE Healthcare will support the program through the provision of GE healthcare equipment and technical support. The equipment under the partnership scope includes Imaging Solutions including Magnetic Resonance Imaging (MRI) and Computed Tomography (CT), Ultrasound Machines and Life Care Solutions.

Borrowers which qualify for loans include private healthcare providers such as hospitals, clinics, diagnostic centers and other private practices offering a broad array of services.

Speaking at the signing ceremony, Mr. Eyong Ebai, General Manager for GE Healthcare West, Central & French Sub-Saharan Africa said, “We are committed to investing in Public and Private Partnerships that innovate new delivery models that will improve access to affordable and quality patient outcomes, as we progress towards Universal Healthcare Coverage (UHC) in Nigeria. Our partnership with Access Bank will help lift the financial burden off the healthcare providers.”

Earlier this year, GE Healthcare rolled out a similar initiative in partnership with Medical Credit Fund to provide Small and Medium Enterprises (SMEs) with financing for healthcare equipment.

“There is a need to provide innovative financing models for healthcare providers especially in the private sector, who currently face challenges accessing financing for the purchase of healthcare equipment due to the risk associated with the business.

As a financing institution, we are committed to providing financing at both the health-service-provider level and at health-service-consumer levels to ensure that the people of Nigeria have all they need to live healthy lives.” Said Mr. Herbert Wigwe, CEO Access Bank.

Access Bank was earlier this year recognized for the second time as the ‘Outstanding Healthcare SME-Friendly Bank of the Year’ at the Nigerian Healthcare Excellence Award (NHEA) 2019.

The need to provide affordable healthcare in Nigeria is key to the development of the Nigerian Healthcare sector. Even as the World Health Organisation has identified UHC as a unifying concept and goal for the Government as they strengthen their health systems and discharge their obligations under the right to health.

GE Healthcare and Access bank scheme were therefore born out of the necessity to provide the needed support to the Nigerian Healthcare environs, by providing healthcare finance at affordable rates and longer tenor.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

Take it or leave it, laws and regulations say who does or does not do business in a country. Ghana is one of those countries whose local laws are not only bad for wholly foreign-owned startups but almost murderous of all foreign-owned startups desiring to exist and do business in the country.

Now, here is the interesting part: Ghanaians seem to have discovered one of these laws and are now relying on it to chase away wholly-owned foreign businesses. They are fixing attention on Section 27 (1) of the Ghana Investment Promotion Centre (GIPC) Act.

Ghanaian traders want this law which has been left a white elephant since its passage to be enforced by the authorities. In the next three months, if threats are anything to go by, expect a massive war against foreign-owned retail businesses in Ghana.

Here Is Why

According to Section 27 (1) of the GIPC Act, a person who is not a citizen or an enterprise which is not wholly-owned by a citizen shall not invest or participate in the sale of goods or provision of services in a market, petty trading or hawking or selling of goods in a stall at any place. The list of prohibited trading activities are:

The sale of goods or provision of services in a market, petty trading or hawking or selling of goods in a stall at any place;

The operation of taxi or car hire service in an enterprise that has a fleet of less than twenty-five vehicles;

The operation of a beauty salon or a barbershop;

The printing of recharge scratch cards for the use of subscribers of telecommunication services;

The production of exercise books and other basic stationery; f. the retail of finished pharmaceutical products;

The production, supply, and retail of sachet water;

All aspects of pool betting business and lotteries, except football pool

Consequently, enterprises eligible for foreign participation and minimum foreign capital requirement are as follows:

A person who is not a citizen may participate in an enterprise other than an enterprise specified in section 27 if that person

In the case of a joint enterprise with a partner who is a citizen, invests a foreign capital of not less than two hundred thousand United States dollars in cash or capital goods relevant to the investment or a combination of both by way of equity participation and

The partner who is a citizen does not have less than ten percent equity participation in the joint enterprise; or

Where the enterprise is wholly owned by that person, invests a foreign capital of not less than five hundred thousand United States dollars in cash or capital goods relevant to the investment or a combination of both by way of equity capital in the enterprise.

A person who is not a citizen may engage in a trading enterprise if that person invests in the enterprise, not less than one million United States dollars in cash or goods and services relevant to the investments.

For the purpose of this section, “trading” includes the purchasing and selling of imported goods and services.

An enterprise referred to shall employ at least twenty skilled Ghanaians

Chase Away Foreigners?

Ghana Union of Traders Association (GUTA) is planning a mammoth demonstration against the government in three months if it fails to enforce laws governing retail trade, said Dr. Joseph Obeng, President of the Association, at a press conference held at the Central Business District (Opera Square)

GUTA is insisting that if the government does not do as expected and the time comes for the demonstration, its members will not be stopped.

Source: Manuel Orozco, Rachel Fedewa, Micah Bump, and Katya Sienkiewicz, 2005. “Diasporas, Development and Transnational integration: Ghanaians in the U.S., UK, and Germany.” Washington, DC: Institute for the Study of International Migration and Inter-American Dialogue.

GUTA President said these confrontations are just actions by local retailers to preserve Ghana’s retail space and should not be seen as xenophobic attacks.

“We are going to declare the destiny day demonstration in three months, where all other laws will not be regarded if our pleas are not being noticed,” he said to the delight of the traders.

Meanwhile, the Accra Region Police Command has described the shutting down of shops belonging to foreigners by some Ghanaian traders as an act of vigilantism that is criminal and could lead to arrests.

Source: Commission of the European Communities: Eurostat, Netherlands Interdisciplinary Demographic Institute (NIDI). 2001. Push and Pull Factors Determining International Migration Flows, “Why and Where: Motives and Destinations.”

Nigerian traders in Ghana, for instance, have also been calling for a review of Ghana’s trade laws, to complement already existing ECOWAS treaties that permit free trade among African economies.

According to the President of the association of Nigerian traders in Ghana, (NUTA), Chief Chukwuemeka Nnaji, a review of existing trade laws in Ghana could help tone down “unnecessary tensions between foreign and retail traders.”

“I’m still surprised that the Ghanaian Parliament has still not amended the laws. Let that law be amended to suit the ECOWAS Trade Treaty. I think we have to change our minds. I believe there is an issue with misinformation which must be dealt with,” he argued.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Founders have to be resilient and thick-skinned. Prepare yourself to exhaust your network of investors, and accept the fact that fundraising is going to take time, even if that’s a hard pill to swallow.

Securing a fresh injection of investment capital can drastically accelerate your startup’s growth, so it’s good to know that there’s no shortage of money up for grabs these days. According to a recent venture capital report from Magnitt, nearly US$800 million in investments were made in the MENA region last year.

But just because the money is out there doesn’t mean the fundraising process will be a breeze. The reality is that investors are picky and often guided by strict criteria to fit their investment thesis. When you seek them out, most will reject you, that’s just part of playing the game. Luckily, there are some rules that can make the process a bit more predictable. Odds are you get a “no”.

Taking into consideration the media’s infatuation with writing articles on multimillion-dollar investments into startups on a daily basis, it can look like these deals happen overnight. They don’t.

In fact, most entrepreneurs will openly tell you about what a struggle the fundraising process can be. Author and business guru Steve Schmitz puts this in perspective in the context of his own fundraising journey.

He wrote: “We raised $40 million of equity from 63 investors. We contacted more than 1,000 prospects. That’s about 6%. That means 94% of the people said no.”

Blackstone CEO Steve Schwarzman had the same 6% hit rate when starting out, too, and his company now manages more than $500 billion of capital.

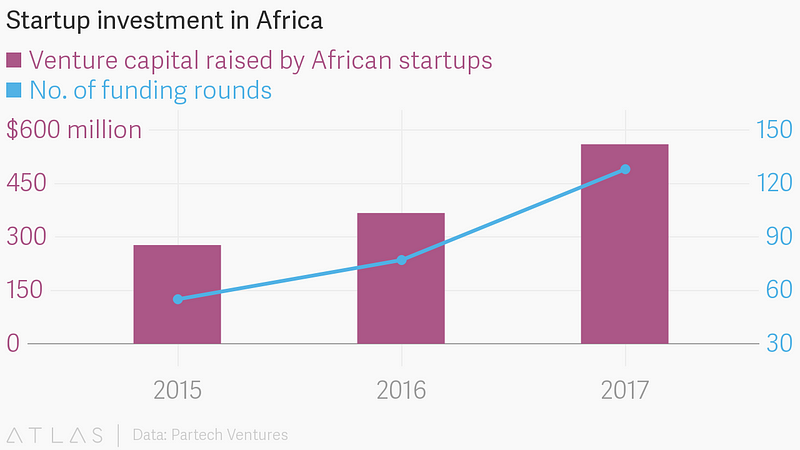

Startup investment in Africa (2015–2017). Credit: Quartz/Partech Ventures

Think of it this way: let’s assume you’re raising a $600,000 seed round, and the average check size for your investors participating in the round is $100,000. This would mean you’d need six investors in on your round. If you operate under the 6% rule, you would have to meet with 100 investors to close your round.

Keep in mind that the 6% rule holds up for qualified investors who cut checks of the size you’re seeking at companies that are at the same stage you are. If you hit up the SoftBank $100 Billion Vision Fund for a $50,000 unit size, that wouldn’t count as an investor. Being told “no” is normal.

Famed speaker and author Tim Ferriss has an excellent podcast episode about just how critical it is to learn from every “no” we get. One of his guests mentions that she heard “no” at breakfast, at mid-morning coffee, at lunch and twice during the afternoon, before ever getting to dinner (where she heard it again).

Founders have to be resilient and thick-skinned. Prepare yourself to exhaust your network of investors, and accept the fact that fundraising is going to take time, even if that’s a hard pill to swallow.

How To Secure The Magic 6%

The 6% rule can apply in any part of the world, but some places will have to stretch outside their borders to make it work. In the MENA region, fundraising often forces founders to go outside their hometowns and home countries to complete fundraising. Online crowdfunding platforms have been instrumental in removing geopolitical borders stateside, and this will surely benefit the 344 million households in the developing world, too. Regardless of where your investment comes from, you can set workable goals to achieve success under the 6% rule.

Here’s How:

1. Use your unit size to set your investor target list size.

It’s easiest to break the total investment you’re seeking into smaller units for starters. Think back to the example above of the $600,000 investment. If you were aiming for $50,000 units, the 6% rule would require you to talk with 200 qualified investors (assuming each investor bought one unit in the worst-case scenario), or 100 investors at $100,000 unit sizes. You can use the rule and your unit sizes to determine the size of your investor target list.

Egyptian startup Swvl did this when it secured five investors for its $8 million Series A round in April 2018, and the Series B that followed at the end of the year.

Once you determine your list size, create a pitching schedule. Assuming it’s not Ramadan -which tends to bring the investment world to a screeching halt- start pitching five times each week for 20 weeks. Factor in eight weeks of researching targets and eight weeks for term sheets to close the deal, and you’re looking at 36 weeks minimum from start to finish.

2. Be ready with prepped materials.

I always have the staples ready to go during fundraising time. Read Venture Deals by Brad Feld to get your lingo down, and understand the basics, it’s VC 101. Then, put together a pitch deck, a term sheet, a clean cap table, a data room, accurate and up-to-date financial statements, and a financial forecast. Preparation is key to secure and close deals, and doing this homework in advance shows that you know what you’re doing.

Verifiable forecasts coupled with a concrete plan to reach them is what secured Wuzzuf its $8 million investment.

This Egyptian startup bootstrapped its job site and recruiting platform in the aftermath of the 2011 Egyptian revolution.

Having survived the toughest economic conditions, the company is now one of the fastest-growing internet companies in Egypt, with more than 250 employees expecting to help 1 million people get hired by the end of this year.

3. Lose the materials when it’s more about relationships.

Pitch decks are great for angel group presentations and pitch competitions, but I’m not a big fan of bringing all of that to one-on-one pitches. If you’re meeting an investor at your nearest Costa Coffee, pitch without materials.

Building a personal connection is what got Jamalon its $10 million Series B investment, not a stack of papers.

Founder Ala Alsallal credits the mentorship he received from Fadi Ghandour, Aramex founder and Wamda Capital chair, with his success, saying relationships made the difference in getting him where he is today. So put away your computer, break the ice, share your story, and dive into your big vision. If the person shows interest, you can talk about materials.

4. Maintain a pipeline, and take your time.

Organize your resources and manage the investors you talk to in a customer relationship management system or a spreadsheet, just as you would a sales pipeline.

Take a note from the Sandler Training book, and use the “submarine trick,” which is inspired by World War II movies in which crews handle attacks on their submarines by closing the door to each compartment behind them.

Salespeople should close each step completely as they go, that way there’s no risk of needing to turn around, and go back on something that’s already been decided. Never forget that a signed term sheet is engagement, not a marriage.

Definitive documents take time to prepare. Wires take time to transfer. Plan ahead so you don’t run out of cash before you complete your raise.

Ultimately, you won’t fundraise for your startup overnight. And rejections will come. Period. Just remember that even if 94% of investors say “no,” 6% will give you the “yes” you need to make the grind pay off.

Zach Ferres is the CEO, Coplex, a Venture Builder that partners with industry experts and innovative enterprises to start high-growth tech companies.

The startup recently announced a $2.5M equity financing round. The Series Seed Round was led by DFE, the family office of Bennett Dorrance of Campbell Soup fame; and AZ Crown, the family office of Insight Enterprises Co-Founders Tim and Eric Crown.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

What are the prospects of African Continental Free Trade Area agreement hold for Africa’s development?

You know that Africa is a continent that trades the least with itself. There are benefits trading with your neighbors, like reduced costs and so on. The first thing that African countries will benefit from this agreement is the opportunity to trade with their neighbors by just opening borders.

The second is that it will push countries to transform their usual commodities into manufactured goods. You need to have complementary products to trade effectively with your neighbors. So, it will be a good incentive for African economies to enter a process like AfCFTA that will help to transform their economies.

What is your view on the future of Africa-Russia relationship?

Africa needs to diversify its relationships for its own benefit. A diversified relationship protects one if one of many partners falls on bad times. So, it is important for Africa, from that perspective, to diversify its relationship. So the Russia-Africa relationship is welcomed in that context.

How best can Africa leverage on its relationship with Russia to bridge its infrastructural gap?

Russia, as you know, has advanced technology. In infrastructure, Russia is well known for power. It has capabilities in solar and hydropower energy that can be implemented in our continent. So, I think that it will be good for African and Russian private sectors to jointly develop those activities.

Some are canvassing that Africa countries should bring home some of their foreign reserves held abroad for investment in Africa. What is your view? There is an initiative that we launched in Afreximbank when I was there, which is ongoing. Yes, it is correct for Africa to try and use, as much as possible, its own resources, including external reserves. There is no reason the continent should be borrowing money when it has money in deposits in other places.

Won’t it have an adverse impact on foreign exchange markets on the continent? No. It won’t. These reserves are backed by strong ratings of an institution like Afreximbank. You have currency in America or in Europe. If you have it in Africa it is still your own, so it should not affect your exchange rate.

On the event that this becomes a reality, which institution will warehouse the foreign reserves?

Foreign exchange reserves have to be held in a strongly rated institution because they are important assets of a country. So, AfDB can hold those reserves likewise the Afreximbank. In my view, these are the two institutions that can hold such a reserve.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

Vice President, Business Development and Corporate Banking of the African Export-Import Bank (Afreximbank), Mr. Amr Kamel would be a credible chronicler of the advent and sustained the trajectory of the progress of Africa’s premier trade finance institution, having been at the Bank for all but two of its 26 years of existence.

Little wonder then, that Mr. Kamel currently oversees the Bank’s origination and business development, including Client Relations, Project Finance, Export Development, Syndication and Agency, Trade Finance, Guarantees, and Specialized Finance as well as Advisory and Capital Market departments. His experience spans many banking functions, including structured trade finance, documentary credits, operations, loan administration and agency, treasury, marketing, and business development.

For one who believes that more African entrepreneurs must be enabled to handle and benefit from businesses run within the continent, Mr. Kamel is leading the Bank’s team of business development experts to get as many as 700 commercial banks to provide financial services to Small and Medium-Sized Enterprises (SMEs).

Everyone agrees that SMEs are the true drivers of growth and employment in developing economies and Kamel believes that if Afreximbank’s services reach more of this category of businesses by this year’s end, the Bank’s mandate of promoting, financing, promoting and expanding intra-and-extra-African trade would be met as its founding fathers expect.

The goal for the teeming small businesses in Africa is to have access to finance, which traditional commercial banks and their international partners have denied them and continued to make inaccessible as global uncertainties rock the international financial landscape. The Bank hopes to pump $25 billion into the market to support intra-African trade in the five-year period ending 2021.

Already, according to Mr. Kamel, Afreximbank is helping the continent to survive the ongoing global trade war through the implementation of the African Continental Free Trade Area (AfCFTA) agreement, especially now that it is set for the launch of its operational phase. The inaugural Intra-African Trade Fair held last year in Cairo, Egypt attempted to connect buyers and sellers on the continent as never before.

Mr. Kamel hopes that the biennial event will grow to become a living bazaar for building long-term relationship among Africa’s businesses and entrepreneurs. Mr. Kamel already looks forward to the expansion of the fair and the buy-in of more businesses in the coming years. Mr. Kamel’s managerial acumen has been largely influenced by his academic and professional background. He is an Economics graduate of the American University of Cairo and holder of an MBA in Financial Management from City University, New York.

He started his banking career in 1985, working variously for Bank of Credit and Commerce, Bank of America, and Chemical Bank, before joining Afreximbank in 1995 as a Senior Operations Associate. Mr. Kamel then progressed through the ranks to the position of Director, Banking Operations in January 2011 before he was promoted to his current position in 2016. Indeed, based on Mr. Kamel’s vast experience in the financial sector, some refer to him as the Doyen of corporate banking.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

The center has the latest types of equipment and focuses on the promotion of esports in Africa.

Paradise Game Center officially opened its doors on Wednesday, July 24th, 2019. Located in the neighborhood with the largest population of the Ivorian capital, the first floor of the new shopping center Cosmos Yopougon, is now home of the largest video game venue of West Africa.

With 1200 sq. meters of space, the center has the latest pieces of equipment and focuses on the promotion of esports in Africa through tournaments and esports players training for international competitions. Video game fans can now enjoy the latest games while preparing for the upcoming FEJA, the largest esports event in Africa.

Starting in September 2019, a dedicated room of 80 m² will host middle school and high school students for training sessions on computers, robotics, and the development of video games.

In 2020, the game center will host the first « edtech & e-learning program » of Yopougon where startups, teachers, students, and entrepreneurs will work together on creating future educational tools for Africa.

These two initiatives are aimed at getting the youth to join the new technology wave and be abreast of robotics, artificial intelligence, and virtual reality.

Paradise Game provides entertainment for children and parents as well. Through various games and activities, they will learn how to build a stronger parent-children relationship.

For the opening of the game center, the entire month of August will be dedicated to celebration activities both inside and outside the Cosmos Yopougon shopping center. From video game crash courses to learning poems and playing board games, the community will be able to discover everything Paradise Game Center has to offer.

« We ambition to transform the entertainment industry in Africa by using games as a way to learn and by allowing young Africans to discover the video game field, robotics, and virtual reality », declared Sidick Bakayoko, founder of Paradise Game.

With more than 500 000 visitors expected per year, Paradise Game Center is positioning itself as a platform to entertain, educate and empower young Africans.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.