Norrsken has entered the East African startup market. The foundation is now open for startups and ventures in East Africa to have access to investment as well as mentorship for their businesses.

Nature and The Size of Norrsken’s Fund

Originally from Sweden, Norrsken Foundation is a coworking space and investment fund based in Stockholm. The new tech fund and entrepreneurship hub opened today in Rwanda will support ventures across the region.

Norrsken’s location in Kigali, Rwanda is former École Belge campus. The startup will be making seed investments of between $25K to $100K for early-stage startups in all sectors starting this year, Norrsken CEO Erik Engellau-Nilsson said in a press release.

However, Norrsken’s size is still being determined and Norrsken Kigali will extend the fund to larger series-stage investments from $100K to $1 million in the future.

Norrsken’s foundation’s move into Rwanda is strongly connected to the organization’s focus on the power of tech entrepreneurs to solve problems and generate capacity.

“We believe the single most important thing we can do here is to help people get wealthy, because if that happens, more investors will start to look at this region and see there are business opportunities and bring more capital,” said Engellau-Nilsson.

“The aim is to build the biggest hub for entrepreneurship in East Africa. Startups that receive Norrsken funding from its Kigali center will receive mentorship and support of the overall Norrsken organization and network. That includes unicorn founders, leading tech founders, and developers. We also look to expand that network to local accelerators and incubators.” said Engellau-Nilsson.

Why This Launch Is Important For East African Startups

This launch of Norrsken’s Kigali center is so important and significant for startups in East Africa because this is Norrsken’s first launch outside of Sweden. The organization is hoping to open up 25 markets globally over the next decade.

Formed in 2016 by Niklas Adalberth, the founder of Swedish payments solutions unicorn Klarna, Norrsken aims to support impact-driven, early-stage ventures. Engellau-Nilsson was an executive with Adalberth at Klarna from 2013 to 2017.

“We wanted to use our experience and tech to solve real problems instead of finding another way to do things like deliver burrito’s faster,” said Engellau-Nilsson.

Norrsken has already invested in 17 ventures, including three Africa-focused startups- agtech company Wefarm, digital publisher Kognity, and weather forecasting firm Ignitia. Over 340 entrepreneurs and 120 companies currently work out of Norrsken’s Stockholm location.

Why Rwanda?

Norrsken said it chose Rwanda as the base for its East Africa because of the country’s progress over the last decade on infrastructure, increasing internet penetration and improvement in its business environment.

Rwanda’s ease of doing business has significantly improved in 2019. The country ranked higher than any African country on the World Bank’s Ease of Doing Business list — 29th, even before Spain.

Even with a relatively small population (12 million) and tech scene, the government of Rwanda has prioritized tech events and development in the country. This includes becoming a leader on drone delivery and regulatory systems, working most notably with San Francisco based UAV startup Zipline.

Of the East African countries from which Norrksen will source investments, Kenya stands out as one of the continent’s top hubs for tech startup formation, VC, and exits.

African startups are gradually being funded

How To Pitch For Norrsken’s New Fund

Startups or ventures in East Africa desiring to pitch for Norrsken’s new fund may do by clicking the informational and contact link Norrsken posted for its Rwanda hub today.

“If there are entrepreneurs who want to reach out to us, we’re ready to go,” said Engellau-Nilsson.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

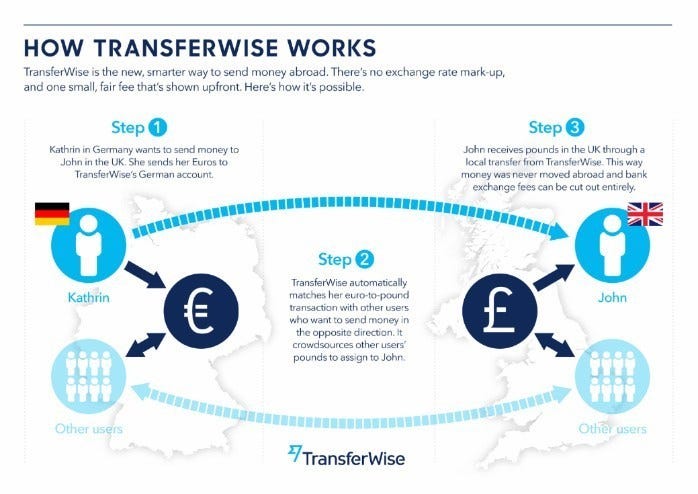

Barely 8 years since its life began in 2011, TransferWise, the UK-based money transfer startup launched by Kristo Käärmann and Taavet Hinrikus with headquarters in London and offices in a number of cities including Tallinn, New York, and Singapore, recently reached a $3.5bn valuation and made 33 new millionaires of its workers. Here are a few lessons to learn from Europe’s most valuable startup and its recent valuations.

TransferWise Is Partnering With Its Employees To Grow Its Value

Indeed, this is unlike other businesses where employees are expected to show up at workplaces, work, go and get paid. Over 1,600 employees at Transferwise collectively own around 2 million vested options, according to last year’s company filings. The latest valuation means that all these employees are now worth $250,000 per employee on average. Collectively, TransferWise’s employees and its alumni (so-called “Wisers”) are now armed with more than $70m to start up their own ventures. In total, 33 new millionaires from its employees’ figures were made millionaires. This brought the total number of employees or investors with six-figure holdings in the payments company to more than 150.

Now the startup is not insisting that the employees must stay back or reinvest their new wealth in the business. is encouraging those employees to go and start up their own ventures.

TransferWise’s Head of Recruitment, Ben Craig, said the startup actively encourages employees to channel their “entrepreneurial mindset” into other projects, through initiatives like a six-week paid sabbatical after four years with the company, even though this can lead to “Wisers” leaving TransferWise to focus on starting their own businesses.

“Our old employees are totally advocates of our brand and we’re advocates of their companies as well,” he says, referencing formal partnerships between TransferWise and Plum, and another potential partnership with Dataminer. “They’ve used our offices, we use their offices, we’re all in constant communication,” Craig adds. “We encourage employees who go out and start their own companies to lean on the skills of the two entrepreneurs who founded TransferWise, and to use the expertise of everyone who has worked with us over the last seven years to TransferWise to where it is today.”

The result of this is that the startup has now become the most valuable startup in the whole of Europe with its recent valuation at $3.5bn. Hundreds of its employees and early backers sold shares to new investors and existing stakeholders. Already more than a dozen former TransferWise employees have gone on to start their own businesses including Victor Troukoudes, chief executive of personal savings AI assistant Plum.

The wider diffusion of wealth to employees and investors is set to be a shot in the arm for the wider European ecosystem, as typically money from a successful startup is plowed back into other startups.

TransferWise Is Build On A Model So That It Not Only Allows Its Customers To Transfer Funds But Also To Buy Shares On Stock Exchanges

TransferWise allows its customers to open an online brokerage account and invest their savings in stocks of companies. Opening an online brokerage account is just as quick and easy as opening a digital bank account. The startup also allows its customers to find a cheap and reliable online broker via our broker recommendation tool.

For users of its online transfer services, there are 44 currencies they can use to exchange money between, within the app. They can also top up their Transferwise accounts in 18 currencies. The startup is also available in 144, almost all countries. At Transferwise, you can open an account for free and also maintain your account for free. There is no monthly cost to that.

Once your account has been opened, you can have your Transferwise ATM card delivered to your address for free. Unlike traditional banks, the startup does not charge any cost for the card. In fact, withdrawing money with Tranferwise from any ATM is free up to £200 / month and costs only 2% above this amount.

Also transferring money in the same currency as your Transferwise account has a flat fee. This will vary depending on your currency. The international transfer fee is €0.5–2.

Its only shortcomings are that it offers no interest on your savings; you cannot set up direct debits; overdrafts are not possible; joint accounts are also not available.

In short, TransferWise charges less than 1% on many currency transfers, compared to what the World Bank estimates is an industry average of more than 7%, thereby undercutting the fees charged by the big banks.

All these make TransferWise an uncommon success. Unlike many of its fintech peers, it has registered two straight years of profits, posting £6.2m in post-tax profits for its fiscal 2018 on £117m in revenue.

TransferWise Has Successfully Shown A New Way Startups Can Succeed Without The ‘Distraction’ of IPO

The founders of Transferwise, Taavet Hinrikus, and Kristo Kaarmann, said this week that they sold “much less than 20%” their own holdings, which are worth $1.3bn at the new valuation. Other big shareholders include Andreessen Horowitz with $65m worth and IA Ventures with $267m worth. Hinrikus said the $292m sale would allow some of the company’s earliest backers to realize the substantial gains on their investments, without forcing it through the “distraction” of an initial public offering.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

The amount of fund raised by the startup was not disclosed, but the funding came from South Africa’s Cape Town-based VC firm HAVAÍC.

“We are excited that Havaic is investing in MPOST. As a seasoned investment and advisory firm, HAVAÍC will undoubtedly bolster MPost’s growth and impact in the region. This is a vote of confidence in our product and indeed our vision as a company,” said chief executive officer of MPostAbdulaziz Omar was quoted as saying.

The startup which has developed a patented technology allows users to transform their phone into a unique mobile postal address and mobile postal box.

“This partnership with Startupbootcamp, HAVAÍC and MPost will enable us to enhance the efficiency and user experience of the product, and improve the long term benefits to our clients and stakeholders,” said chief technology officer (CTO) Twahir Mohamed.

MPost At A Glance

The startup was founded in 2015 by Abdulaziz Omar and Twahir Mohamed. The startup allows mobile phone numbers of its users to be converted into official virtual addresses which will allow the users to be notified whenever they get mail through their postal addresses.

The startup has already gained 40,000 users, mostly as a result of its partnership with the Postal Corporation of Kenya. It has been primarily self-funded but obtained some angel investment last year. The latest round of funding comes from established investment and advisory firm HAVAÍC, which also plans to participate in MPost’s forthcoming Series A round.

HAVAÍC’s Rob Heath, the partner responsible for pan-African and international business at the firm said HAVAIC invested in the startup because:

“After spending time with Aziz and Twahir in Nairobi and seeing the solution in action, it’s clear that this is not just a technology and commercial product. MPost makes a real impact on people’s daily lives and as an investor, it’s rewarding when we can tie these two elements together. That being said, this is a great example of African problems producing global solutions — one of the cornerstones of our investment thesis at HAVAÍC.”

MPost is further moving to Uganda ahead of further launches in Rwanda, Botswana, Tanzania, and South Africa.

Last year, the startup participated in the Startupbootcamp AfriTech accelerator program in Cape Town, where it was introduced to HAVAÍC. MPost will also welcome Startupbootcamp AfriTech co-founder Zachariah George onto the board to represent both his business and HAVAÍC.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Even though e-commerce is seriously gnawing at physical shops. Physical shops with a messy environment would most definitely get a little crumb of what is left. Of the 70% of consumers surveyed in a study commissioned by ServiceChannel, a facilities management platform, and who said they had once experienced messy stores, over two-thirds have walked out of stores because of the way they looked.

The study suggests that struggling retailers who neglect stores to cut costs hasten their demise by turning off shoppers. The survey was carried out on 1,521 consumers and 70% of them said they recently have had a negative experience with a messy store.

Over two-thirds admitted they have walked out of stores because they were messy or disorganized.

Four out of five shoppers said they would rather have a clean store than ones with the newest tech, and two-thirds said retailers are forgetting the basics—like clean floors and well-stocked shelves—in the rush to add tech.

“The vast majority of purchases are still being done by people walking into a location. And their experience of that location has never been more important,” Buiocchi, the CEO ServiceChannel said in an interview.

“If you look at folks like Allbirds or Warby Parker, Bonobos or Soul Cycle or Shake Shack, their locations are so comfortable and well laid out and so well maintained. You would never walk into a Warby Parker or a Shake Shack and say ‘Man this place is messy.’ Or the lights are dim or it’s too cold in here. They just don’t let that happen.’’

ServiceChannel is in the business of selling software and services that allow retailers to manage store maintenance, connect with and pay contractors, and track invoices, so it is no surprise that it is touting a survey that concludes store cleanliness is crucial. But he has a point that is often overlooked by retailers.

With ServiceChannel, retailers can book contractors and manage maintenance jobs on mobile phones.

“Much like when you get an Uber or Lyft ride and the entire ride is digitally recorded, the transaction is digitally recorded so someone 3,000 miles away can go fix a toilet for you at a Banana Republic and you will know based on the GPS coordinates when that person got there, how long they stayed, whether they showed up on time, and they can send you a picture,” Buiocchi said.

ServiceChannel is seeing that many of the new online brands that are opening stores are quick to recognize the value of rigorous maintenance and are signing up as customers.

“There are the people that get it, and there are the people that don’t get it,” Buiocchi said. “Five years from now what are the chances that the people who don’t get it are going to be in business?”

Buiocchi says reports of a retail death end are overrated. As stores close, new retail disruptors are opening locations and expanding.

“Good progressive retail is investing in their brick-and-mortar experiences and enjoying the benefits of that,” he said. “Bad retail is not and they’re unfortunately being penalized for that.”

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

As you would expect, the first implication of the Kenyan new currency policy (which is that the country’s currency would be replaced with a new generation of banknotes and that Kenyans must return their 1,000 shillings ($10; £8) notes to banks by 1 October, in a bid to fight money laundering, counterfeits, and corruption) is that many businesses would go in for it.

The new currency notes will be in Sh50, Sh100, Sh200, Sh500 and Sh1000 denominations. Although Kenya’s Central Bank Governor Prof Patrick Njoroge said the Sh50, Sh100, Sh200 and Sh500 notes will be phased out slowly, he has however insisted that:

“The emergence of counterfeits has become a great concern. All the Sh1000 notes were withdrawn by a gazette notice on Friday. Those in possession [of the bank notes] have until October 31, 2019 to release them,” said Prof Njoroge who urged Kenyans to have the notes changed.

Below are the implications of the change in this currency policy on Kenyan businesses.

By November This Year, All Those In Possession of The Old Ksh1000 Notes Will Not Be Able To Use Them

This is directive of the Central Bank of Kenya. Mr. Njoroge said the Central Bank of Kenya is giving all Kenyans in possession of the old Ksh1000 a four-month transition period in order to allow them enough time to change the old currency within their possession.

For Kenyan exchanging less than 5m shillings, they would be able to do so at their local bank but any amounts higher than that will need approval from Kenya’s central bank. Those are to seek approval from Kenya’s Central Bank include those without bank accounts and with over Ksh.1million of the old currency.

Another strategy would be to block all ways of exploiting the new policy. The bank is already in talks with managers of foreign-exchange bureaux and money-remittance providers to put in place controls to prevent illicit financial flows.

There is an alleged feeling of desperation among those suspected to be hoarding money acquired illegally and who are hence unable to bank it as they cannot openly declare its source. Such individuals are faced with the challenge of losing the money when it is devalued on 1st October as Kenya officially moves on to the new currency as is dictated by the 2010 Constitution, reports Kenya’s Investment Company Soko Directory

Commercial banks are expected to obtain confirmations from customers on the nature of their businesses that generate the respective large cash transactions.

Kenyan Shillings Can Be Used Once In A While In Uganda and Tanzania, But This Is No Longer Going To Be The Case

With this new policy, Kenyan businesses using Kenyan shillings to transact or do foreign exchange businesses in Uganda and Tanzania will not be able to do so again. Mr. Ngoroge has communicated to banks across the East African region where Kenyan shillings is often used as a legal tender to ensure that Kenya’s illegal money did not get exchanged in their countries. To this effect, the Bank of Uganda, Uganda’s highest bank has mandated all banks in Uganda to stop accepting Kenyan currency at the counter. A statement from Uganda’s Central Bank said the move is aimed at boosting Kenya’s fight against counterfeits and illicit flows.

“The Central Bank of Kenya has informed Bank of Uganda that they have issued a new series of Kenya banknotes effective May 31, 2019…..in light of new developments, BOU will not accept Kenya shillings at its counters with immediate effect,” the notice reads.

The memo also said the new currency is only available in Kenyan banks. The bank further directed all commercial banks in Uganda to subject all cash flows from and into Kenya to due diligence. The Tanzanian central bank has also stated the same.

With the new move, expect previously hoarded cash to be collected back for redistribution. There are a total of 217.6 million pieces of 1,000 shillings in circulation in Kenya according to a statement by the Central Bank of Kenya (CBK).

The Kenya Association of Manufacturers is leading the pack of those Kenyans who see opportunity from this. KAM chairman, Sachen Gudka has been quoted as saying:

“This change is likely to redirect monies that are presently hoarded and funneled into funding illicit economic activities into the formal banking and lending structures to finance the production of real goods and services.”

He also believed that the move will give citizens a better purchasing power and push for higher demand and supply for local products, and as such boost positive legit businesses in the country.

There Is A Big Question On Whether The Design Of The New Currency Is Constitutional

Article 231 (4) of the Constitution of Kenya states that “Notes and coins issued by the Central Bank of Kenya may bear images that depict or symbolize Kenya or an aspect of Kenya but shall not bear a portrait of any individual.”

Activist Okiya Omtatah has since gone to court to block the new currency over the inclusion of the portrait of Mzee Jomo Kenyatta, contrary to the requirement of the constitution.

The Chief Justice David Maraga has been asked by the High Court to constitute a 3-judge bench to deliberate on the matter.

Nigeria introduced a similar ban on old notes in 1984 in an attempt to crack down on corruption, as did Ghana in 1982 to help with tax evasion.

This may be a big-time signal for businesses in Kenya to consider storing their cash in foreign domiciliary accounts.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Lagos residents will now have one more online ride-sharing option to choose from by July this year. Egypt’s ride-sharing startup SWVL has announced plans to launch in Lagos, Nigeria in July. 5O buses would be on the road from the date of the launch, according to Swvl’s Country General Manager in Nigeria. This is expected to be a huge challenge to existing ride-sharing options, such as Uber, Bolt, and ride-hailing motor-bike alternatives.

SWVL expects the surging population of Nigeria’s most populous city to be on its side. The startup is already in Kenya and Egypt and has plans to expand to Uganda soon. Other target countries include Thailand and Vietnam, and possibly operations in seven world mega-cities by the end of this year.

Barely 2 years in existence, it is the most funded startup in Egypt.

Swvl’s Business Model

SWVL’s goal is to make it easier for Egypt’s residents to book bus rides at a fixed rate on existing routes.

Users schedule trips, pay online or in cash and are given virtual boarding passes.

Even with fierce competition from the likes of Buseet and Uber vying into premium public transport service, SWVL’s application has been downloaded for well over 360,000 times on Google play store and Apple iStore.

The platform completes 100,000 rides monthly.

It was the first company to introduce the service in Egypt in 2017 before Careem and Uber joined the sector late last year.

Swvl is however different from its competitors because of its series of partnership deals. The startup’s credit facility agreements with Nasser Social Bank and EFG Hermes Bank, and after-sales support and maintenance services with Ford-trained technicians are some of these moves.

What Egyptian SWVL users think about the startup is its priority on affordability, comfort, and safety.

Not Afraid Of Competition

Although Swvl is the first riding app to offer bus services in Egypt, giant transportation startups Careem and Uber have recently offered their own bus services.

Mostafa Kandil, Egyptian CEO and founder of Swvl, has however noted that the joining of Uber and Careem to the industry has not influenced Swvl’s growth asserting that they have witnessed remarkable development since the two competitive players have launched. In 2018, the startup was valued at nearly US$100 million, becoming the second Egyptian company after Fawry to reach these figures.

The startup has recently signed an agreement with Ford motor company to deploy more cars on the road. Ford Transit, which the startup intends to use is already the third best selling van of all times. SWVL is already in possession of about 100 Ford Transits. Hazem Taher, SWVL’s Head Marketing Manager, said the vans were ready to go and they’re excited to push them on SWVL’s route.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

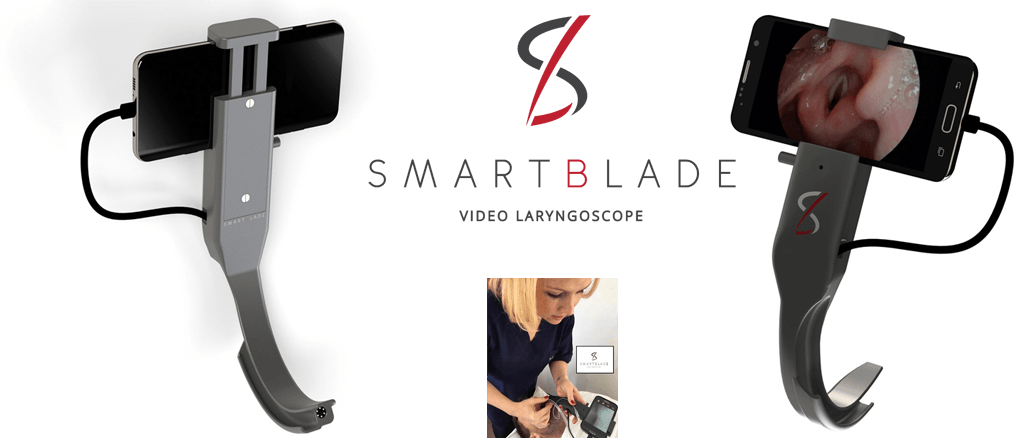

Once SmartBlade app is loaded onto the smartphone, it will allow the user to access the camera in the laryngoscope, which in turn allows for video viewing, storage, and transmission. In other words, the app will help users to see videos of their larynxes.

A laryngoscope is an instrument for examining the larynx, or for inserting a tube through it.

The company has been incubated at the Cape Town-based hardware incubator Savant over the past few years and has now become the first recipient of investment from the Savant Venture Fund, launched after the incubator itself raised funds, from the South African SME Fund.

SmartBlade will use the investment, which comes in the form of a convertible note, to take its innovation to market and deliver on the global interest and demand it says it has seen for the device.

“Following the successful launch of the video laryngoscope, the company will look to utilise its smartphone endoscopy expertise to bring associated medical devices to market,” Savant venture fund manager Nick Allen said.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Looking to raise capital for your startup through equity crowdfunding? No loans? Just some hard currency from some money messiahs? That is what South African businesses are turning to now. Intergreatme has recently succeeded in raising over R32.7 million ($2.2 million) by simply putting up an online request for equity funding on Uprise.Africa and getting overwhelmed by public contributions. This was a big moment for the startup looking to help ordinary people get rid of the daily pain associated with submitting forms and documents through an innovative technology platform.

The startup was founded by a team of young South Africans three years ago and is now valued at about R120m. The team envisions a world where personal data can easily and securely be shared among a host of applications. As long as an activity requires a person’s information, Intergreatme sees a market.

How The Startup Scaled The Hurdles and Raised The Funds

Narrating how the startup raised the funds through equity crowdfunding, Intertreatme CEO said in a recent interview:

We had no idea how successful it was going to be. We thought it was going to be like a 60 day campaign of climbing Mount Kilimanjaro. We needed to get 250,000 that day and we hoped to just do some cold calls. I printed out my full contact list on my phone and my whatsapp list, my email list, and we thought it’s going to be a campaign. But we had no idea that the demand was more than that. We thought that we could raise the 24 million and we thought that we were going to procure a common amount ever.

For startups looking to use crowdfunding to raise capital, he says they are not just going to put a pretty video online and hope people come and invest. They need to do the hard job behind the scenes.

‘‘There are billions and trillions of dollars of money waiting to be deployed,’’ he says. ‘‘People get paid money to invest money. But your business fundamentally needs to be right. Your team needs to be right. What you plan to do needs to be right. So do those things right. And then you can just sample your user base. Just run a poll on Facebook or Instagram or Twitter, just saying, ‘‘Hey, if we rank car, would you invest? And if so, how much will you? You’ll get, you will get an answer. I don’t think you need to do a lot of work to get those answers.

On the pattern of investing, he said about 402 people turned up and contributed to the startup through equity crowdfunding.

We had minimum commitment of 1000 rand and a maximum commitment of 5 million. We had about five, five millions. Wow. We had a couple of millions. It was so cool. We didn’t expect it. And it was just people. We started by saying, if you’ve used our technology before and you sure that you had the wow moment, would you like to invest in this? Tick this box, if you want. But ultimately they, they invested in us as people.

Before that, we had a very successful launch party, which I think was key to the fundraising, where we had a private donation from our whatsapp list. This was two weeks before that. And we’ve got about 120 investors there. And then we had about 250 people at our launch party when the startup was first started. We used that time not to sell the technicalities of the business, but to sell out emotional stories as founders to show that it’s normal for us to overcome unrealistic odds.

He said the crowd bought into the human stories and not the technicalities.

‘‘We said it’s normal for us to overcome adversity and challenges, that it doesn’t matter what comes our way. It’s normal for us. We will find a way to succeed. And so people bought into the emotional story. They always say, you shouldn’t invest in a business. You should invest in people. And yeah, basically people bought the founder’s shares, in the founder’s energy, in the founder’s vision. And so literally everyone in that room at the launch party made us the first 27 million. And so we sold apps 27 millions in the first 72 hours and there were just a frenzy of people trying to jump on and grab the last time.

I think if you look inside now, it is 32 million, 409,000 rands. So they’ll have to be some refunds for some people who just came in and about a hundred people came in on the last day, like before three o’clock.

On Why They Choose Uprise.Africa to Raise The Funds

He says Uprise.Africa has direct exposure to all the upsides and downsides of the business

‘‘I didn’t know who they were,’’ he says. ‘‘We made it a conference. I related with its CEO as a founder. She said cool. They have a framework and are licensed to do it. So effectively it’s as good as a payment gateway. So if you’re running an ecommerce business and pay fast or need paypal or visa, mastercard go to them for a widget. They can accept payments, but they’re relying on how good your business is .

One of my favorite little proverbs is if a bird is sitting on a tree on the branch, it’s not worried about the branch snapping. It has faith and confidence is in its wings. Crowd funding is an easy way to take money from the crowd, but there’s a context to it. If we show the analytics of the money we raised, everyone is within one or two steps of our network. And so accountability is really your socially accountable tool to your community and your network. If they believe in you, you’re not going to have a much bigger responsibility to them.’’

He says Uprise.Africa will own a 25% stake in the startup.

‘‘They will also have an independent board member. Uprise.Africa will be representing the crowd and yeah, fix me. But there are voting rights and things. So Uprise.Africa has the stake on behalf of the people who invested in the initiative. I think they manage it for about 12 months or so and then they give it to us. They have also put automated technology in place for the share registers and the certificates and the reporting.’’

On Why More Black Women Invested In The Startup Through The Crowdfunding

‘‘I think maybe it’s because we spent a lot of time with Uber drivers and optimistic ladies and all security guards and receptionists. They used our technology and they’re like, sweet, I can get my license renewed. Daily visits to the management system are amazing. So it is just crazy for us because we actually thought that we were so proud that we managed to get 30% black female ownership. They were like, this company’s plan is going to dilute that potentially down to 22%. We had signed agreements to become level two. And so it was a concern. It was just, again, a miracle from the universe that it actually ended up swinging way better than we could give. I’ve imagined it. So I think that’s the beauty of opening it up to the crowd. If you’re focusing on one or two high net worth individuals, you’re kind of going for a specific target.’’

Other Startups In South Africa Are Also Resorting To Crowdfunding

Crowdfunding is having a moment in SA. BackaBuddy, the funding project used to raise money for service station attendant Nkosikho Mbele, for example, has so far generated over R107 million for various causes.

Uprise.Africa CEO and co-founder Tabassum Qadir say the company is in negotiations with one of the new share trading exchanges to have equity crowdfunding investors trade their holdings on its platform.

‘‘Although crowdfunding has long been used to support start-up ventures, equity crowdfunding is different as it enables people to become direct shareholders in a venture, ’’ Qadir says,

This is in contrast to traditional crowdfunding services that generally only allow contributors to get new products from the ventures they support for free.

To ensure that the interests of investors are protected, Qadir says prospective companies need to be vetted by its investment committee. Once approved by this committee, a designated Uprise.Africa board member will act as an overseer of investors’ interests in the company.

In exchange for about R24 000, Uprise.Africa will conduct due diligence and organize a 90-day ‘campaign’ to build interest in the company.

Qadir says using crowdsourcing to support start-up businesses is widely seen as a way to drive economic development. The World Bank, for instance, estimates that the global equity crowdfunding sector will be worth more than $93 billion by 2020.

Without crowdfunding, prospective investors either have to wait for a company to be listed on the JSE or invest at least R100 000 into a venture equity firm’s portfolio to get a stake in emerging businesses. With equity crowdfunding, however, for as little as R1 000, they could get a stake in a company as it is about to enter a fast-growing stage.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Good news for users of cryptos. There are plans by thirteen of the world’s largest banks, including UBS, Barclays, and Santander, to launch crypto versions of major global currencies in 2020, according to the Financial Times. The banks would be led by UBS and they have been working on crypto, nicknamed Utility Settlement Coin (USC) since 2015 to determine if blockchain can help optimize processes in wholesale banking.

Here Is What This Means

To make this a reality, the 13 banks, in addition to Nasdaq, have also invested £50 million ($63 million) in a new venture, Fnality, to run the USC project.

The USC will make it possible for users to get digital cash instruments to settle their transactions.

The system will be denominated in major global currencies including the US dollar, yen, euro, and sterling.

Each unit of the crypto denominated in a specific currency will be backed by the corresponding unit of traditional currency, so as to keep the price of the coin stable.

At the outset, the project will focus on creating niche applications. That is, Fnality will initially focus on creating the necessary market infrastructure that will make the crypto to work.

These initial applications will include meeting margin requirements in derivatives trades. A derivative is referred to as the security or financial instrument that depends or derives its value from an underlying asset or group of assets.

They are simply contracts between two or more parties. The value of such a contract is determined by changes or fluctuations in the asset where it derives its value from.

Currently, that process takes at least a day to be satisfied, but it would become almost instantaneous with the USC, according to Fnality CEO Rhomaios Ram cited by the Financial Times.

Beyond that, the USC could soon make it possible to clear and settle trades immediately. This could prove to be transformational, according to Hyder Jaffrey, head of strategic investments at UBS’ investment bank.

This May Suggest That More Banks Are Finding Blockchain and Cryptos Acceptable

Although this is not assured, USC suggests that banks are gradually finding confidence in blockchain and cryptos. However, these 13 banks will most likely still have to scale some legal and regulatory challenges in their efforts to adopt the technology and will need to prove that the scalability issues that hamstrung early experiments in crypto have been resolved.

The journey may be a tougher one though. This is because to develop an ecosystem that will be enough to convince the majority of banks and financial institutions (FIs) across the world to throw away existing processes for transaction settling will take time.

Indeed, the USC is a major step towards sealing a major approval for the technology but the end of the road is still far. The weight of the banks backing the USC should help the project secure traction — but this won’t guarantee success.

It appears blockchain technology is gradually gaining momentum. Facebook is seriously ready to launch its own crypto solution. The social media network has been busy pushing out efforts to enter financial services via a crypto solution. The solution will aim to provide payment options for its 2 billion users. A 2020 launch date is expected any moment from now.

A group of banks in Japan is also considering a 2020 calendar date for the launch of the group’s own cryptos. For sure, 2020 is going to be a year of blockchain technology. When these happen, blockchain tech may be signaling that it has become accepted into the mainstream system as a legitimate way of transacting, a hope that has since been hanging unfulfilled.

Combine all of these with USC, you get to find that cryptos are beginning to gain traction both within retail and institutional settings.

However, blockchain’s potential would still need to convince more of its believers. The head of Germany’s central bank said, for instance, that its trial of using blockchain to transfer and settle securities didn’t prove to be faster or cheaper than existing processes. Bank of America’s (BofA’s) tech and operations chief, Cathy Bessant, also echoed that she has yet to see a genuine use case that can scale to meet enterprise needs — despite the bank holding or having applied for the most blockchain-related patents among US FIs.

Should the USC finally work as desired, it would be an end to all these speculations and fear. Repeated over and over again without much concern, blockchain would finally come to stay.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

When Mr. Tola Fadugbagbe relocated back to Lagos, Nigeria’s largest city for the second time in his young life, there was nothing yet like cryptocurrency or bitcoins or tokens or Blockchain technology. He could only be fused into one of the over 17.5 million people living in the city. And it appeared he was merely making up the population because it seemed the city looked too overwhelming to fit in. It didn’t take long before several months of homelessness hit him hard in the face.

‘‘For several months, I stayed in an uncompleted building. Life was nothing but hell. I was running around struggling to get funds to complete my education to university level,’’ he tells Afrikan Heroes.

Then a job stint at a highly successful real estate development company. A break-away to start up a local block making factory, and a sudden bankruptcy and closure of the facility because clients who promised to pay took delivery of his blocks but never cared to pay back, Mr. Fadugbagbe says he is still banking on his integrity, determination, cryptocurrency and blockchain technology to take him farther than he has ever thought.

‘‘ One thing I always prove to people about myself wherever I go is integrity. Anywhere I am, people always get to know me as someone with integrity. That was why I stayed longer than expected at the real estate company,’’ he said.

Mr. Tola said he learned his lessons about running his first startup the hard way:

While I was working in the real estate company, I discovered that there was a problem that needed to be solved: the quality of concrete blocks being delivered to this site. You know, the blocks they usually supplied the real estate company were not strong enough. So I thought that if I ventured into this business, I could make some future from it. So after I left the real estate company, I set up a block making factory.

When the factory was up and running, I was so happy that I was progressing. I was generous and selling on credit. But before I knew what was happening, people were withholding my money and they were telling me stories. As I’m talking to you now, these people are still owing me. I was back to square one after that nightmare: I could not even produce even though my equipment was on ground.

‘‘Till Date, It Has Been Marvelous Getting Involved in Cryptocurrency.’’

While reading about cryptocurrency and blockchain technology sometime in 2016 from two of his Facebook friends ‘who were not usually detailed about the terms and the philosophy behind the concept’, Mr. Tola got interested and began extensive studies and inquiries into what cryptocurrencies are, only to discover that cryptocurrencies suited his philosophy. Since then, he says it has been ‘‘marvelous getting involved in cryptocurrency.’’

Today, he is part of a local network in Lagos and Nigeria that hosts conferences, seminars, boot-camps, and workshops training people on what cryptocurrency is and how they can trade in it.

I believe that cryptocurrency is a big deal. Big corporations can’t stop talking about cryptocurrency. They can’t stop implementing cryptocurrency in one way or the other. Look at the CEO of JP. Morgan, Jamie Dimon, who once told his workers that if they ever got involved in bitcoin they would be fired. He called Bitcoin a fraud, a scam and an evil. Few weeks later he bought bitcoins on Poloniex. Right now, J.P Morgan is using fragments of JPM Coin, the native coin of JP Morgan Bank. I mean JP Morgan is a US banking giant that move trillions of dollars across the globe daily. Right now they want to use their own token to scale payment protocols and remittances,’’ he says.

Mr. Fadugbagbe is not far from the truth. Earlier in February 2019, J.P. Morgan became the first major U.S. bank to create its own cryptocurrency with the launch of “JPM Coin.” The digital token was designed to settle transactions between clients of its wholesale payments business, specifically for international payments and securities transactions that migrate to the blockchain.

Mr. Fadugbagbe remembers one incident about how cryptocurrency has been more than a helpful innovation in the payment system.

‘‘Someone in the US sent bitcoins to me today. I sent Naira equivalent to the person’s beneficiary in Nigeria. If they are to rely on Western Union, the fees, the delay and all that would be too much,’’ he said.

‘‘I believe that cryptocurrency has come to stay. You know, there are some people in Diaspora that find it difficult to send money back home. Now, crytopcurrency has made it a lot more easier for them because they could just create crypto accounts over there and using those accounts, they can now send bitcoins to me, and I, in turn pay off their beneficiaries in Nigeria the Naira equivalent of the bitcoins sent to me. These things happen within a space of few minutes.

He says that unlike fiat currency that government can only print more, borrow more and yet remain heavily in debt, cryptocurrency always has an edge.

‘‘You can’t inflate it. Instead you can only reduce it. This means that, with time, crypto can always gain value. The only downside of it that it that it is highly volatile. That is why people should be cautious about the type of crytocurrrency they get involved in. In fact, the crypto market is highly competitive right now. So if you lay your hands on a token doing similar things to other similar tokens in the similar same crypto market, and if the token is not highly innovative, then it would not scale,’’ he says.

‘‘Whether You Like It or Not, Everybody Will Get Involved In Cryptocurrency’’

Mr. Fadugbagbe said the only thing remaining for cryptocurrency to become widely accepted is for governments to give their nod to it. For that, he sees a huge opportunity for early investors.

”So if you look at the future of cryptocurrency, you can’t but be part of it at this early stage. Many people see Bitcoins, ethereum and cryptocurrency as the dark part of the internet because some governments are yet to approve it. Whether we like it or not government plays a major part in controlling the mindset of the citizens. Just take a look at the stories of MTN and DSTV before they became big players in their industries. We all know are they were first rejected by governments,” he says.

Why Africa is Lagging Behind In Cryptocurrency and Blockchain Technology?

Mr. Fadugbagbe says Africa is lagging behind because of the continent’s low rate of adoption of the innovation. He says anything revolutionary will be adopted quickly in any continent or any country when the government welcomes it wholeheartedly. Although he says African governments are usually ‘‘just slow in adopting something as disruptive as cryptocurrencies,’’ he has hope that Africa would get there someday.

”This is one of the reasons why we’ve been hosting seminars, workshop, bootcamps. We still need to engage the government.We just have to keep talking about this. We hope that one day, we would get the attention of the government to approve the necessary framework for cryptocurrency and blockchain technology. Just take, for instance: if you can now travel to all West African countries using Bitcoins. It would really mean that more people would get interested in bitcoins. If the government also says you can now pay your tax with bitcoins, many people would be eager to pay tax,” he says.

Mr. Fadugbagbe also finds a big problem with the way international communities see cryptocurrencies coming out of Africa.

”International communities believe that an average Nigerian or African is a scammer,’’ he says. ‘‘ Once cryptocurrencies are coming out from Africa or Nigeria, the international community doesn’t usually trust them, even when the intention is good,’’he says.

How Startups Can Leverage Crypto To Boost Their Businesses

Mr. Tola says smart startups can leverage cryptocurrencies to boost their business even without any formal partnerships with any blockchain organizations or blockchain platforms. To do this, he says African startups may consider accepting cryptocurrencies such as bitcoins, bitcoin ethereum or any other viable coins. Doing this not only boosts startups’ businesses but also gives their businesses free advert.

”Free advert because cryptocurrencies guys everywhere in the world will begin to refer your business. Take for instance, the impact of having a barbershop somewhere in Nigeria where you can now have hair cut and pay with bitcoins. In trying to convince your folks about the existence of such barbershop, you may begin to refer to such words as ‘‘look at the barbershop here. Look at its office phone number.’ The same way, you may refer to a hotel in Cameroon where you can now check into, pay with bitcoin and get discount. Or somewhere in Zambia where you can vacation to and pay with cryptocurrency. This will give startup owners free adverts. Just imagine a consumer in Nigeria, Cameroon, Senegal, South Africa, Uganda talking about your business.”

”This is why celebrities keep progressing because we keep talking about them. Who knows? But Reginal Daniels has so much been in the news and may be landing brand ambassador deals even. So this will give startups free adverts, thereby generating more leads for their businesses.”

‘’Governments Can Use Blockchain Technology To Keep Records Of The Number Of Books Received By Each Student’’

Mr. Fadugbagbe tells prospective blockchain technology investors in Africa to start submitting proposals to the government because there is a huge opportunity in that regard.

‘‘Africa needs blockchain tech the most. We can use blockchain to curtail the inefficiencies in the system. In most education ministries in Africa, for instance, books are distributed from time to time. Government can use blockchain tech to keep records of the number of these books received by each student. For every book the students receive, they can thrown in a token from their backends, using a smartphone. This is the smartest way to get feedback from Africa’s cluttered data management system. So let’s begin by sending in proposals,’’ he said.

Mr. Fadugbagbe says blockchain technology makes for more accountability and efficiency in the system, and unlike humans, data stored in blockchains cannot be tampered with.

‘‘You look at blockchain as a record that cannot be edited,” he said. ‘‘For instance, a list of items or names, or a football team. When humans are involved, they can add or remove the names at will, but with blockchain technology, the list cannot be padded. So once added, the information cannot be altered.”

For a business model that was worth over $700 billion as of January 2018, the global cryptocurrency market is booming and is not relenting. Mr. Tola Fadugbagbe does not see this ending too. No longer homeless and frustrated by bad debt, at least not in the category he once fitted in at his former startup, he has since moved on.

‘‘Right now,’’ he says, ‘‘I am living in a good and comfortable apartment. I have been reinvesting into large scale agriculture — a cocoa farm and and poultry — from the proceeds of my blockchain business. My aim is to grow them into the biggest phase they could ever be in. I like my life so simple because of what I have experienced in the past. I’m not going back to that nightmare.’’

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.