For startups venturing out into the unknown territories of a tech startup business, here a few tips shared by Wiza Jalakasi, head of international expansion at Africa’s Talking on how to build a successful tech company at the just-concluded third Google Launchpad Accelerator Africa program held in Lagos Nigeria. Wiza runs Africa’s Talking which raised $8.6m from the IFC, Orange Digital Ventures and other partners. Africa’s Talking is on its international expansion efforts as it scales APIs for infrastructure (SMS, USSD, voice, airtime, banking, and mobile money) across Africa

Patience And Passion

Building a business takes time, for most, it takes four to five years. There is a process that is involved and it’s not always colorful. It’s day-to-day grinds, doing seemingly mundane things and you need to get it in your head that that’s the only way for you to get where you’re going. Fall in love with the process.

Focus

You need to focus on your business. It’s very easy for you to get distracted by ecosystem events. Don’t be your start-ups. Spend your time and energy on things that are directly related to the outcomes of your business. Mind your own business, drink water. Remain teachable. Check your psychology as grow, especially when people start talking about you. Don’t let that get into your head, tomorrow is another day and you still need to pay your bills.

Customer Care

Spend time with your customers. If as an entrepreneur you’re not willing to get your hands dirty, it’s not going to work out for you. Do not fall in love with this notion that you can sit on your high table with a laptop on your lap and think this is how you’ll build your business. Sometimes you need to sit down and talk to someone to get things done. That’s how you build a technology company.

Be Stable In Competition

When you see similar business pop up, that’s a good thing. It validates that there’s value in the space that you’re creating and it’s important for you to be aware of what’s happening in the industry. Don’t be scared when you see the competition and don’t double down on trying to beat the competition directly. Focus on your customers.

Be Accountable

If you’re trying to run a business and you’re trying to avoid accounting, it’s not going to work. You need to get comfortable with basic administration. You need to be running a profit and loss from day one.

Loss Will Come Anyway

Don’t have a goal of making a profit immediately. You’ll make a loss for many years. What’s important is keeping those records so when the time comes for fundraising, you have your ducks in order.

You may think investors don’t want to see losses on your books but what investors are looking for is a consistent attitude towards record-keeping and responsibility, you must build that from day one.

Get Some Culture For Your Startup

The company culture is what you as the founder do on a day-to-day basis. You can’t build culture through writing nice bullet points. It’s what you do on a day-to-day basis and you can only lead by example. Be deliberate about the culture from day one.

Fundraising Is About Story-telling

Fundraising is about telling a good story. The market doesn’t always reward great ideas, if you fail to tell a good story you might not have access to capital. Be good at storytelling. If as a founder you are not good at storytelling, find someone who can do it for you.

If you’re not good at storytelling, start building relationships early. Some investors will back you simply because you’re consistent with the information and they’ve seen you grow.

Think Twice Before Expanding

Expansion is extremely difficult. You’ll spend twice your budget. I don’t recommend that tech startup jumps into expansion from day one. Stop and validate your idea in your home market and respect that base.

See Yourself As A Different Person From Your Startup And Respect Partners And Staff

Kindness is an important tool that you can leverage to build your tech startup. Be kind to yourself as a founder. Separate yourself as a founder from your tech startup. The success or failure of your start-ups will never be tied to the success or failure of you as a person.

Your business partner will more likely become one of the most important people in your life. Have empathy for who they are — their strengths and weaknesses. Take time to cultivate an authentic relationship in which you as co-founders can have extremely difficult conversations on a day to day basis without breaking the company.

Take care of yourself. You can be a start-up founder and live a normal life. This idea that you need to be breaking your back to make your start-up work is not true. Let it go.

Be kind to your staff. The people working for you are going to make a pass on opportunities that they could take advantage of elsewhere. If you treat your staff members as your first customers and your job as the CEO is to make sure your customer is happy, they will actually build the business for you.

Reputation Opens Doors

Be guarded about your reputation and integrity, people will use it to decide on whether to work with you.

You don’t get what you don’t ask for. Speak to people and share your progress and struggles.

Launchpad Accelerator Africa Class 3 comprised of 12 startups from six African countries — Egypt, Kenya, Nigeria, Senegal, South Africa, and Uganda. 58% of co-founders were female.

Teams who graduated were trained in machine-learning technologies and implemented AI in their product as a result. The startups in this class raised about R129 million in funding, created more than 120 jobs and accumulated over 270,000 users on their services.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

When your startup is ready to go looking for funds, term sheet usually serves as the first set of document you send to investors or investors send to you. It is a negotiation document that details the intended equity participation from the investors in your startups. Most times, term sheet is a bullet-point document outlining the material terms and conditions of a business agreement. Term says in details what your start-up is giving, and what it is getting in return. It then lays out the guidelines of how both parties will act to protect the investment.

More or less, a term sheet is generally not binding, unless the parties say so. Once a term sheet has been “executed”, it guides legal counsel in the preparation of a proposed “final agreement”. The length or the volume of a timesheet depends on the stage of funding your startup is in.

Generally, term sheets for seed rounds are usually much lighter and shorter than for series A or beyond. That is, once you have less at stake, you should expect a term sheet that is less complex, as no one wants to unnecessarily spend on extra legal fees, or burn hardly found the time. In all, term sheet could be a pager, or 10 pages of documents, in simple, clear terms.

What To Look Out For In Every Term Sheet

For every founder or investor reviewing a term sheet proposed by potential investors, or drafting one, they should specifically look out for:

Unfavorable terms. Such terms include a harsh term on debt financing and convertible note terms that could bankrupt you

Demand for too much controlling stake that may replace you

Terms that can restrict your ability to raise further funding

Investors that are impatient and or want a short and quick exit, and that are not willing to respect your timeline of breaking even.

What And What Should Be Found In A Term Sheet?

Who is issuing the note or stock

Type of collateral being offered

The valuation

Amount being offered

Shares and price

What happens on liquidation or IPO

Voting rights

Board seats

Conversion options

Anti-dilution provisions

Investors rights to information

Founders obligations

Who will pay legal expenses

Non-disclosure requirements

Rights to future investment

Signatures

General Points About Reviewing These Common Terms In A Term Sheet

Investors may want to generally prolong the negotiation after term sheet stage may have been completed. When you see this coming, just exercise some patience. Every single provision in that document may not matter today as they would in the long run.

Make the term sheet a win-win for everybody. Founders do not want difficult or greedily overbearing investors, much as investors would not want dishonest or crooked founders.

As a general rule, aim for dilution of around 20% per round of financing. Don’t be in a hurry to go beyond that amount. Your startup may still have a long way to go.

Dilution occurs when holders of stock options, such as company employees, or holders of other optionable securities exercise their options. As the number of shares outstanding increases, each existing stockholder owns a smaller, or diluted, percentage of the company, making each share less valuable.

When you are still at the seed stage of your fundraising and you desire to give up a good amount of your stocks or company’s shares to outsiders, just know that those shares will not come back to you, until you, of course, restructure your startup.

A term sheet is not permission to go on a spending spree. Founders should not make the mistake of thinking the money will be transferred once they receive a term sheet, and therefore go on a spending spree. Wait until the deal is closed. This is because a term sheet itself is not an executed deal or even a promise.

Negotiating A Term Sheet

The best way to win the whole term sheet episode is to carry a lawyer with you who understands the intricacies of every clause inserted into the term sheet. Hone your negotiation skills.

‘‘Having information that the other side doesn’t have gives [you] an advantage… [VCs] take advantage of entrepreneurs who haven’t been through this before… they were totally willing to take advantage of us.” — Mitch Kapor, Founders at Work

Make Sure You Do Not Leave Due Diligence Out Of The Question

Due diligence is very important both for the investor and the founders. Due diligence can cover a wide range of many subjects ranging from legal to technological to human resources. Your in-house team can do this, or you hire an external solicitor or organization. So take time and conduct due to diligence on your potential investors, and particularly answer the following questions:

Do you trust the investor? Trusting is the make-or-mar of your startup.

Are you going to get along with the investor even if funding is immense? This is better imagined than never.

Are there companies that have benefited from their contributions?

What do the investors do when a portfolio company doesn’t do well?

Then Seal The Deal

A little space is usually allowed for investors to conduct their due diligence on your company. Make sure your technology is well patented and that trademarks and designs are registered, and that the documentation of your company is well preserved at the company and trademark registries. This is because investors usually check to see if those things are in order and if the sole owner of the products or business rightly belongs to you.

Sign A Binding Contract

Having noted that the term sheet is not a binding agreement, have it at the back of your mind to negotiate any term you feel deeply uncomfortable with. The best advice is usually to let your lawyer do the job and help you reach a win-win deal.

Time-Lines

Negotiation from the stage of the term sheet to the final agreement usually takes some weeks, depending on whether the deal is simple and the parties are easily agreeable. For complex deals, however, expect a long time for due diligence, legal restructuring, and aligning with many investors.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

In this essay, Paul Graham, an English-born computer scientist, entrepreneur, venture capitalist, author, and essayist shares his thoughts on the commonest reasons why startups die off sooner than they think. Below are his thoughts:

In the Q & A period after a recent talk, someone asked what made startups fail. After standing there gaping for a few seconds I realized this was kind of a trick question. It’s equivalent to asking how to make a startup succeed — if you avoid every cause of failure, you succeed — and that’s too big a question to answer on the fly.

Afterwards I realized it could be helpful to look at the problem from this direction. If you have a list of all the things you shouldn’t do, you can turn that into a recipe for succeeding just by negating. And this form of list may be more useful in practice. It’s easier to catch yourself doing something you shouldn’t than always to remember to do something you should. [1]

In a sense there’s just one mistake that kills startups: not making something users want. If you make something users want, you’ll probably be fine, whatever else you do or don’t do. And if you don’t make something users want, then you’re dead, whatever else you do or don’t do. So really this is a list of 18 things that cause startups not to make something users want. Nearly all failure funnels through that.

1. Single Founder

Have you ever noticed how few successful startups were founded by just one person? Even companies you think of as having one founder, like Oracle, usually turn out to have more. It seems unlikely this is a coincidence.

What’s wrong with having one founder? To start with, it’s a vote of no confidence. It probably means the founder couldn’t talk any of his friends into starting the company with him. That’s pretty alarming, because his friends are the ones who know him best.

But even if the founder’s friends were all wrong and the company is a good bet, he’s still at a disadvantage. Starting a startup is too hard for one person. Even if you could do all the work yourself, you need colleagues to brainstorm with, to talk you out of stupid decisions, and to cheer you up when things go wrong.

The last one might be the most important. The low points in a startup are so low that few could bear them alone. When you have multiple founders, esprit de corps binds them together in a way that seems to violate conservation laws. Each thinks “I can’t let my friends down.” This is one of the most powerful forces in human nature, and it’s missing when there’s just one founder.

2. Bad Location

Startups prosper in some places and not others. Silicon Valley dominates, then Boston, then Seattle, Austin, Denver, and New York. After that there’s not much. Even in New York the number of startups per capita is probably a 20th of what it is in Silicon Valley. In towns like Houston and Chicago and Detroit it’s too small to measure.

Why is the falloff so sharp? Probably for the same reason it is in other industries. What’s the sixth largest fashion center in the US? The sixth largest center for oil, or finance, or publishing? Whatever they are they’re probably so far from the top that it would be misleading even to call them centers.

It’s an interesting question why cities become startup hubs, but the reason startups prosper in them is probably the same as it is for any industry: that’s where the experts are. Standards are higher; people are more sympathetic to what you’re doing; the kind of people you want to hire want to live there; supporting industries are there; the people you run into in chance meetings are in the same business. Who knows exactly how these factors combine to boost startups in Silicon Valley and squish them in Detroit, but it’s clear they do from the number of startups per capita in each.

3. Marginal Niche

Most of the groups that apply to Y Combinator suffer from a common problem: choosing a small, obscure niche in the hope of avoiding competition.

If you watch little kids playing sports, you notice that below a certain age they’re afraid of the ball. When the ball comes near them their instinct is to avoid it. I didn’t make a lot of catches as an eight year old outfielder, because whenever a fly ball came my way, I used to close my eyes and hold my glove up more for protection than in the hope of catching it.

Choosing a marginal project is the startup equivalent of my eight year old strategy for dealing with fly balls. If you make anything good, you’re going to have competitors, so you may as well face that. You can only avoid competition by avoiding good ideas.

I think this shrinking from big problems is mostly unconscious. It’s not that people think of grand ideas but decide to pursue smaller ones because they seem safer. Your unconscious won’t even let you think of grand ideas. So the solution may be to think about ideas without involving yourself. What would be a great idea for someone else to do as a startup?

4. Derivative Idea

Many of the applications we get are imitations of some existing company. That’s one source of ideas, but not the best. If you look at the origins of successful startups, few were started in imitation of some other startup. Where did they get their ideas? Usually from some specific, unsolved problem the founders identified.

Our startup made software for making online stores. When we started it, there wasn’t any; the few sites you could order from were hand-made at great expense by web consultants. We knew that if online shopping ever took off, these sites would have to be generated by software, so we wrote some. Pretty straightforward.

It seems like the best problems to solve are ones that affect you personally. Apple happened because Steve Wozniak wanted a computer, Google because Larry and Sergey couldn’t find stuff online, Hotmail because Sabeer Bhatia and Jack Smith couldn’t exchange email at work.

So instead of copying the Facebook, with some variation that the Facebook rightly ignored, look for ideas from the other direction. Instead of starting from companies and working back to the problems they solved, look for problems and imagine the company that might solve them. [2] What do people complain about? What do you wish there was?

5. Obstinacy

In some fields the way to succeed is to have a vision of what you want to achieve, and to hold true to it no matter what setbacks you encounter. Starting startups is not one of them. The stick-to-your-vision approach works for something like winning an Olympic gold medal, where the problem is well-defined. Startups are more like science, where you need to follow the trail wherever it leads.

So don’t get too attached to your original plan, because it’s probably wrong. Most successful startups end up doing something different than they originally intended — often so different that it doesn’t even seem like the same company. You have to be prepared to see the better idea when it arrives. And the hardest part of that is often discarding your old idea.

But openness to new ideas has to be tuned just right. Switching to a new idea every week will be equally fatal. Is there some kind of external test you can use? One is to ask whether the ideas represent some kind of progression. If in each new idea you’re able to re-use most of what you built for the previous ones, then you’re probably in a process that converges. Whereas if you keep restarting from scratch, that’s a bad sign.

Fortunately there’s someone you can ask for advice: your users. If you’re thinking about turning in some new direction and your users seem excited about it, it’s probably a good bet.

6. Hiring Bad Programmers

I forgot to include this in the early versions of the list, because nearly all the founders I know are programmers. This is not a serious problem for them. They might accidentally hire someone bad, but it’s not going to kill the company. In a pinch they can do whatever’s required themselves.

But when I think about what killed most of the startups in the e-commerce business back in the 90s, it was bad programmers. A lot of those companies were started by business guys who thought the way startups worked was that you had some clever idea and then hired programmers to implement it. That’s actually much harder than it sounds — almost impossibly hard in fact — because business guys can’t tell which are the good programmers. They don’t even get a shot at the best ones, because no one really good wants a job implementing the vision of a business guy.

In practice what happens is that the business guys choose people they think are good programmers (it says here on his resume that he’s a Microsoft Certified Developer) but who aren’t. Then they’re mystified to find that their startup lumbers along like a World War II bomber while their competitors scream past like jet fighters. This kind of startup is in the same position as a big company, but without the advantages.

So how do you pick good programmers if you’re not a programmer? I don’t think there’s an answer. I was about to say you’d have to find a good programmer to help you hire people. But if you can’t recognize good programmers, how would you even do that?

7. Choosing the Wrong Platform

A related problem (since it tends to be done by bad programmers) is choosing the wrong platform. For example, I think a lot of startups during the Bubble killed themselves by deciding to build server-based applications on Windows. Hotmail was still running on FreeBSD for years after Microsoft bought it, presumably because Windows couldn’t handle the load. If Hotmail’s founders had chosen to use Windows, they would have been swamped.

PayPal only just dodged this bullet. After they merged with X.com, the new CEO wanted to switch to Windows — even after PayPal cofounder Max Levchin showed that their software scaled only 1% as well on Windows as Unix. Fortunately for PayPal they switched CEOs instead.

Platform is a vague word. It could mean an operating system, or a programming language, or a “framework” built on top of a programming language. It implies something that both supports and limits, like the foundation of a house.

The scary thing about platforms is that there are always some that seem to outsiders to be fine, responsible choices and yet, like Windows in the 90s, will destroy you if you choose them. Java applets were probably the most spectacular example. This was supposed to be the new way of delivering applications. Presumably it killed just about 100% of the startups who believed that.

How do you pick the right platforms? The usual way is to hire good programmers and let them choose. But there is a trick you could use if you’re not a programmer: visit a top computer science department and see what they use in research projects.

8. Slowness in Launching

Companies of all sizes have a hard time getting software done. It’s intrinsic to the medium; software is always 85% done. It takes an effort of will to push through this and get something released to users. [3]

Startups make all kinds of excuses for delaying their launch. Most are equivalent to the ones people use for procrastinating in everyday life. There’s something that needs to happen first. Maybe. But if the software were 100% finished and ready to launch at the push of a button, would they still be waiting?

One reason to launch quickly is that it forces you to actually finish some quantum of work. Nothing is truly finished till it’s released; you can see that from the rush of work that’s always involved in releasing anything, no matter how finished you thought it was. The other reason you need to launch is that it’s only by bouncing your idea off users that you fully understand it.

Several distinct problems manifest themselves as delays in launching: working too slowly; not truly understanding the problem; fear of having to deal with users; fear of being judged; working on too many different things; excessive perfectionism. Fortunately you can combat all of them by the simple expedient of forcing yourself to launch something fairly quickly.

9. Launching Too Early

Launching too slowly has probably killed a hundred times more startups than launching too fast, but it is possible to launch too fast. The danger here is that you ruin your reputation. You launch something, the early adopters try it out, and if it’s no good they may never come back.

So what’s the minimum you need to launch? We suggest startups think about what they plan to do, identify a core that’s both (a) useful on its own and (b) something that can be incrementally expanded into the whole project, and then get that done as soon as possible.

This is the same approach I (and many other programmers) use for writing software. Think about the overall goal, then start by writing the smallest subset of it that does anything useful. If it’s a subset, you’ll have to write it anyway, so in the worst case you won’t be wasting your time. But more likely you’ll find that implementing a working subset is both good for morale and helps you see more clearly what the rest should do.

The early adopters you need to impress are fairly tolerant. They don’t expect a newly launched product to do everything; it just has to do something.

10. Having No Specific User in Mind

You can’t build things users like without understanding them. I mentioned earlier that the most successful startups seem to have begun by trying to solve a problem their founders had. Perhaps there’s a rule here: perhaps you create wealth in proportion to how well you understand the problem you’re solving, and the problems you understand best are your own. [4]

That’s just a theory. What’s not a theory is the converse: if you’re trying to solve problems you don’t understand, you’re hosed.

And yet a surprising number of founders seem willing to assume that someone, they’re not sure exactly who, will want what they’re building. Do the founders want it? No, they’re not the target market. Who is? Teenagers. People interested in local events (that one is a perennial tarpit). Or “business” users. What business users? Gas stations? Movie studios? Defense contractors?

You can of course build something for users other than yourself. We did. But you should realize you’re stepping into dangerous territory. You’re flying on instruments, in effect, so you should (a) consciously shift gears, instead of assuming you can rely on your intuitions as you ordinarily would, and (b) look at the instruments.

In this case the instruments are the users. When designing for other people you have to be empirical. You can no longer guess what will work; you have to find users and measure their responses. So if you’re going to make something for teenagers or “business” users or some other group that doesn’t include you, you have to be able to talk some specific ones into using what you’re making. If you can’t, you’re on the wrong track.

11. Raising Too Little Money

Most successful startups take funding at some point. Like having more than one founder, it seems a good bet statistically. How much should you take, though?

Startup funding is measured in time. Every startup that isn’t profitable (meaning nearly all of them, initially) has a certain amount of time left before the money runs out and they have to stop. This is sometimes referred to as runway, as in “How much runway do you have left?” It’s a good metaphor because it reminds you that when the money runs out you’re going to be airborne or dead.

Too little money means not enough to get airborne. What airborne means depends on the situation. Usually you have to advance to a visibly higher level: if all you have is an idea, a working prototype; if you have a prototype, launching; if you’re launched, significant growth. It depends on investors, because until you’re profitable that’s who you have to convince.

So if you take money from investors, you have to take enough to get to the next step, whatever that is. [5] Fortunately you have some control over both how much you spend and what the next step is. We advise startups to set both low, initially: spend practically nothing, and make your initial goal simply to build a solid prototype. This gives you maximum flexibility.

12. Spending Too Much

It’s hard to distinguish spending too much from raising too little. If you run out of money, you could say either was the cause. The only way to decide which to call it is by comparison with other startups. If you raised five million and ran out of money, you probably spent too much.

Burning through too much money is not as common as it used to be. Founders seem to have learned that lesson. Plus it keeps getting cheaper to start a startup. So as of this writing few startups spend too much. None of the ones we’ve funded have. (And not just because we make small investments; many have gone on to raise further rounds.)

The classic way to burn through cash is by hiring a lot of people. This bites you twice: in addition to increasing your costs, it slows you down — so money that’s getting consumed faster has to last longer. Most hackers understand why that happens; Fred Brooks explained it in The Mythical Man-Month.

It’s obvious how too little money could kill you, but is there such a thing as having too much?

Yes and no. The problem is not so much the money itself as what comes with it. As one VC who spoke at Y Combinator said, “Once you take several million dollars of my money, the clock is ticking.” If VCs fund you, they’re not going to let you just put the money in the bank and keep operating as two guys living on ramen. They want that money to go to work. [6] At the very least you’ll move into proper office space and hire more people. That will change the atmosphere, and not entirely for the better. Now most of your people will be employees rather than founders. They won’t be as committed; they’ll need to be told what to do; they’ll start to engage in office politics.

When you raise a lot of money, your company moves to the suburbs and has kids.

Perhaps more dangerously, once you take a lot of money it gets harder to change direction. Suppose your initial plan was to sell something to companies. After taking VC money you hire a sales force to do that. What happens now if you realize you should be making this for consumers instead of businesses? That’s a completely different kind of selling. What happens, in practice, is that you don’t realize that. The more people you have, the more you stay pointed in the same direction.

Another drawback of large investments is the time they take. The time required to raise money grows with the amount. [7] When the amount rises into the millions, investors get very cautious. VCs never quite say yes or no; they just engage you in an apparently endless conversation. Raising VC scale investments is thus a huge time sink — more work, probably, than the startup itself. And you don’t want to be spending all your time talking to investors while your competitors are spending theirs building things.

We advise founders who go on to seek VC money to take the first reasonable deal they get. If you get an offer from a reputable firm at a reasonable valuation with no unusually onerous terms, just take it and get on with building the company. [8] Who cares if you could get a 30% better deal elsewhere? Economically, startups are an all-or-nothing game. Bargain-hunting among investors is a waste of time.

14. Poor Investor Management

As a founder, you have to manage your investors. You shouldn’t ignore them, because they may have useful insights. But neither should you let them run the company. That’s supposed to be your job. If investors had sufficient vision to run the companies they fund, why didn’t they start them?

Pissing off investors by ignoring them is probably less dangerous than caving in to them. In our startup, we erred on the ignoring side. A lot of our energy got drained away in disputes with investors instead of going into the product. But this was less costly than giving in, which would probably have destroyed the company. If the founders know what they’re doing, it’s better to have half their attention focused on the product than the full attention of investors who don’t.

How hard you have to work on managing investors usually depends on how much money you’ve taken. When you raise VC-scale money, the investors get a great deal of control. If they have a board majority, they’re literally your bosses. In the more common case, where founders and investors are equally represented and the deciding vote is cast by neutral outside directors, all the investors have to do is convince the outside directors and they control the company.

If things go well, this shouldn’t matter. So long as you seem to be advancing rapidly, most investors will leave you alone. But things don’t always go smoothly in startups. Investors have made trouble even for the most successful companies. One of the most famous examples is Apple, whose board made a nearly fatal blunder in firing Steve Jobs. Apparently even Google got a lot of grief from their investors early on.

15. Sacrificing Users to (Supposed) Profit

When I said at the beginning that if you make something users want, you’ll be fine, you may have noticed I didn’t mention anything about having the right business model. That’s not because making money is unimportant. I’m not suggesting that founders start companies with no chance of making money in the hope of unloading them before they tank. The reason we tell founders not to worry about the business model initially is that making something people want is so much harder.

I don’t know why it’s so hard to make something people want. It seems like it should be straightforward. But you can tell it must be hard by how few startups do it.

Because making something people want is so much harder than making money from it, you should leave business models for later, just as you’d leave some trivial but messy feature for version 2. In version 1, solve the core problem. And the core problem in a startup is how to create wealth (= how much people want something x the number who want it), not how to convert that wealth into money.

The companies that win are the ones that put users first. Google, for example. They made search work, then worried about how to make money from it. And yet some startup founders still think it’s irresponsible not to focus on the business model from the beginning. They’re often encouraged in this by investors whose experience comes from less malleable industries.

It is irresponsible not to think about business models. It’s just ten times more irresponsible not to think about the product.

16. Not Wanting to Get Your Hands Dirty

Nearly all programmers would rather spend their time writing code and have someone else handle the messy business of extracting money from it. And not just the lazy ones. Larry and Sergey apparently felt this way too at first. After developing their new search algorithm, the first thing they tried was to get some other company to buy it.

Start a company? Yech. Most hackers would rather just have ideas. But as Larry and Sergey found, there’s not much of a market for ideas. No one trusts an idea till you embody it in a product and use that to grow a user base. Then they’ll pay big time.

Maybe this will change, but I doubt it will change much. There’s nothing like users for convincing acquirers. It’s not just that the risk is decreased. The acquirers are human, and they have a hard time paying a bunch of young guys millions of dollars just for being clever. When the idea is embodied in a company with a lot of users, they can tell themselves they’re buying the users rather than the cleverness, and this is easier for them to swallow. [9]

If you’re going to attract users, you’ll probably have to get up from your computer and go find some. It’s unpleasant work, but if you can make yourself do it you have a much greater chance of succeeding. In the first batch of startups we funded, in the summer of 2005, most of the founders spent all their time building their applications. But there was one who was away half the time talking to executives at cell phone companies, trying to arrange deals. Can you imagine anything more painful for a hacker? [10] But it paid off, because this startup seems the most successful of that group by an order of magnitude.

If you want to start a startup, you have to face the fact that you can’t just hack. At least one hacker will have to spend some of the time doing business stuff.

17. Fights Between Founders

Fights between founders are surprisingly common. About 20% of the startups we’ve funded have had a founder leave. It happens so often that we’ve reversed our attitude to vesting. We still don’t require it, but now we advise founders to vest so there will be an orderly way for people to quit.

A founder leaving doesn’t necessarily kill a startup, though. Plenty of successful startups have had that happen. [11] Fortunately it’s usually the least committed founder who leaves. If there are three founders and one who was lukewarm leaves, big deal. If you have two and one leaves, or a guy with critical technical skills leaves, that’s more of a problem. But even that is survivable. Blogger got down to one person, and they bounced back.

Most of the disputes I’ve seen between founders could have been avoided if they’d been more careful about who they started a company with. Most disputes are not due to the situation but the people. Which means they’re inevitable. And most founders who’ve been burned by such disputes probably had misgivings, which they suppressed, when they started the company. Don’t suppress misgivings. It’s much easier to fix problems before the company is started than after. So don’t include your housemate in your startup because he’d feel left out otherwise. Don’t start a company with someone you dislike because they have some skill you need and you worry you won’t find anyone else. The people are the most important ingredient in a startup, so don’t compromise there.

18. A Half-Hearted Effort

The failed startups you hear most about are the spectacular flameouts. Those are actually the elite of failures. The most common type is not the one that makes spectacular mistakes, but the one that doesn’t do much of anything — the one we never even hear about, because it was some project a couple guys started on the side while working on their day jobs, but which never got anywhere and was gradually abandoned.

Statistically, if you want to avoid failure, it would seem like the most important thing is to quit your day job. Most founders of failed startups don’t quit their day jobs, and most founders of successful ones do. If startup failure were a disease, the CDC would be issuing bulletins warning people to avoid day jobs.

Does that mean you should quit your day job? Not necessarily. I’m guessing here, but I’d guess that many of these would-be founders may not have the kind of determination it takes to start a company, and that in the back of their minds, they know it. The reason they don’t invest more time in their startup is that they know it’s a bad investment. [12]

I’d also guess there’s some band of people who could have succeeded if they’d taken the leap and done it full-time, but didn’t. I have no idea how wide this band is, but if the winner/borderline/hopeless progression has the sort of distribution you’d expect, the number of people who could have made it, if they’d quit their day job, is probably an order of magnitude larger than the number who do make it. [13]

If that’s true, most startups that could succeed fail because the founders don’t devote their whole efforts to them. That certainly accords with what I see out in the world. Most startups fail because they don’t make something people want, and the reason most don’t is that they don’t try hard enough.

In other words, starting startups is just like everything else. The biggest mistake you can make is not to try hard enough. To the extent there’s a secret to success, it’s not to be in denial about that.

[2] Ironically, one variant of the Facebook that might work is a facebook exclusively for college students.

[3] Steve Jobs tried to motivate people by saying “Real artists ship.” This is a fine sentence, but unfortunately not true. Many famous works of art are unfinished. It’s true in fields that have hard deadlines, like architecture and filmmaking, but even there people tend to be tweaking stuff till it’s yanked out of their hands.

[4] There’s probably also a second factor: startup founders tend to be at the leading edge of technology, so problems they face are probably especially valuable.

[5] You should take more than you think you’ll need, maybe 50% to 100% more, because software takes longer to write and deals longer to close than you expect.

[6] Since people sometimes call us VCs, I should add that we’re not. VCs invest large amounts of other people’s money. We invest small amounts of our own, like angel investors.

[7] Not linearly of course, or it would take forever to raise five million dollars. In practice it just feels like it takes forever.

Though if you include the cases where VCs don’t invest, it would literally take forever in the median case. And maybe we should, because the danger of chasing large investments is not just that they take a long time. That’s the best case. The real danger is that you’ll expend a lot of time and get nothing.

[8] Some VCs will offer you an artificially low valuation to see if you have the balls to ask for more. It’s lame that VCs play such games, but some do. If you’re dealing with one of those you should push back on the valuation a bit.

[9] Suppose YouTube’s founders had gone to Google in 2005 and told them “Google Video is badly designed. Give us $10 million and we’ll tell you all the mistakes you made.” They would have gotten the royal raspberry. Eighteen months later Google paid $1.6 billion for the same lesson, partly because they could then tell themselves that they were buying a phenomenon, or a community, or some vague thing like that.

I don’t mean to be hard on Google. They did better than their competitors, who may have now missed the video boat entirely.

[10] Yes, actually: dealing with the government. But phone companies are up there.

[11] Many more than most people realize, because companies don’t advertise this. Did you know Apple originally had three founders?

[12] I’m not dissing these people. I don’t have the determination myself. I’ve twice come close to starting startups since Viaweb, and both times I bailed because I realized that without the spur of poverty I just wasn’t willing to endure the stress of a startup.

[13] So how do you know whether you’re in the category of people who should quit their day job, or the presumably larger one who shouldn’t? I got to the point of saying that this was hard to judge for yourself and that you should seek outside advice, before realizing that that’s what we do. We think of ourselves as investors, but viewed from the other direction Y Combinator is a service for advising people whether or not to quit their day job. We could be mistaken, and no doubt often are, but we do at least bet money on our conclusions.

NB: This content was originally published on Paulgraham.com.

The author has reproduced it here in the interests of startups desperately in need of mentors.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Getting your startup up and running can be one of the most demanding tasks every startup founders can face. The experience could be overwhelming, but seeking advice from the right mentors could make the work less cumbersome.

Below, we share the experience of most startup owners on how they got started.

Mostapha Kandil — SWVL, (Egyptian Startup)

‘‘Obviously, I am very happy about the fact that my team and I have reached this far in such a small amount of time. When we first came into this space, everyone thought we are crazy. They thought we are taking on Careem & Uber and we wouldn’t be able to survive. No investor was willing to take us seriously. This investment by Careem proves that we can actually make it.

But happiness is not the only feeling. I am scared as well. All this hype and attention we’ve been getting esp. after Careem’s investment comes with a lot of responsibility towards all our stakeholders; captains, customers, everyone. We are trying to build something that even some governments struggle to do; a public transportation system.

It’s one of the most difficult things for countries to build a public transportation system in emerging markets and we are some 24-year-olds trying to take on this challenge so yeah it’s scary. Normally public transportation is a loss making machine in these countries as it requires huge infrastructure. What we are trying to achieve is a sweet spot between quality and pricing.

‘‘I think the biggest risk was to shift from being Petroleum Engineer to doing something else. It was not easy to study something and then end up doing a completely different thing. Also, your parents could never really understand what you’re doing. When I called my mom to tell her how I made it to Forbes after Careem’s investment. She was like ‘good for you’

For every startup, he advises:

Don’t over-engineer everything, just get it done. You’ll figure it out on the way. 2) Take risks because what you’re already doing is a risk in its own. You probably left a job to start a business so you’re already taking it. Make sure you keep doing it onwards a well. 3) Learn more by learning faster. If you do 9 experiments a week vs your competition doing 10 experiments then your competition ends up learning 52 times more over a year.

Gregory Rockson — mPharma, (Ghanaian Startup)

Gregory Rockson is the Co-founder and CEO of mPharma, a drug benefits startup in Africa. He holds a Bachelor’s Degree in Political Science from Westminster College.

mPharma works with drug manufacturers, service providers, and third-party payers to develop products and services that improve the access and affordability of high-quality drugs for patients across the continent. He shares his experience as a startup:

‘‘It was an early morning in downtown San Francisco a few months ago and I was sitting in a Starbucks, thinking about what next to do with my life. After two successful interviews with Google, I had a good feeling that I would receive a job offer, but something just did not sit right with me. Around 9am, I received an email from a friend which had a link to an investigative article titled “Dirty Medicine” on CNNMoney. It tackled the issue of criminal fraud in Ranbaxy Laboratories, an Indian multinational pharmaceutical company. This article marked my return to Africa and my quest to use big data to help African governments develop better drug surveillance and monitoring systems.’’

At that moment, all I could think about were the 84 children who died in Nigeria in 2008 after consuming adulterated baby teething mixture and the many other families who have lost a loved one due to substandard/fake drugs. I was frustrated by the silence on the part of drug regulators in Africa.

I moved from asking myself why to thinking how. How do we develop technology solutions to address the challenges with pharmacovigilance in Africa?

Grant Brooke — co-founder, Twiga Foods (Kenyan Startup)

Three years ago, on the stage of an international pitch competition, I stood in front of judges and a thousand entrants with a single PowerPoint slide of a banana, which simply stated: “This is a Banana”. Its simplicity got a big laugh.

When in the African e-commerce space players were aiming for tens of thousands of stock-keeping units (SKUs), our banana revenue alone made us one of the largest tech commerce players in Kenya. While we are doing more than bananas now, it is worth keeping in mind that the average Kenyan household buys about 50 different consumer products a month.

To build a unicorn startup in Africa — a relatively small consumer economy — you had better be in a segment with a lot of spending.

Say no: We are good at saying no as an organisation. Lots of people want to partner with us, use us to distribute their products, to build things on our platform, to photo op with us, and so on. We are not easily distracted from our core objective of ‘selling bananas’. I was once given the academic advice: “Early in your career, say something specific about something specific, and once you do that, you can say it all.” The same holds for business: do something specific about something specific, and a few years down the line you can do it all.

Founded in 2014, Twiga Foods is a business to the business food distribution startup that builds fair and reliable markets for agricultural producers and retailers through transparency, efficiency, and technology. The startup is one of the best-funded on the continent,

Deji Oduntan, former CEO Gokada, (Nigerian Startup)

Build a Base then Tell Your Story

There’s a phrase that goes, ‘Build it and they will come’. I’m here to tell you it’s a lie! Build customer confidence and loyalty in your product(s)/service and once you do, tell your story with pride. Gokada had a strong organic social media following of tens of thousands before we began any serious PR work. The story is sweeter when the customer base is already in existence and it’s this customer-centricity that has sprouted significant investor interest in the industry and Gokada specifically, as news of this recent funding round indicates.

Be Laser Focused

Prior to Gokada, I led Customer Experience efforts at Jumia, where I imbibed a very important lesson: Know your target market and be laser focused. No service can work for the entire market, or indeed Nigerians, as we are a diverse people. Thus, identify a target customer segment and accelerate to product-market fit in the shortest possible time. To do this requires a lot of qualitative research and hypothesis testing. Don’t be afraid to spend time and resources into gathering insights quickly and effectively. It could be make or break.

Bank on Trust

Behavioral change was critical to the branding efforts I drove at Gokada. How do you take a nascent and almost non existent industry and turn it into an industry with promise of a sustainable future in Nigeria? I led with trust, by using operational excellence and social media to position Gokada as a brand worth trusting. We dispelled a lot of mistrust in the market about motorcycle taxis by promoting safety, cleanliness (we introduced disposable hair nets to the sector after recognizing the concerns and superstitions people had about sharing helmets) and verified drivers. This trust system was central to Gokada’s success over the past 14 months.

Nigerian Lagos-based on-demand motorcycle taxi app Gokada has proven to be up to the game. The startup has raised US$5.3 million in Series A funding with a plan to expand the number of its motorbikes and available drivers, increase its daily ride numbers as well as grow the startup ‘s team.

Onyeka Akumah — Founder, Farmcrowdy, Nigeria

In 2015, I was looking at investing in Agriculture. I wanted to work with a farmer and trying to decide which farmer to work with, which one I would be able to invest in and he would get the work done so I can get the return on investment after the harvest. I got in touch with one of my co-founders (Ifeanyi Anazodo) and asked if he could help me identify someone to work with. We met a lot of farmers. While they were talking, I noticed that they had certain challenges they were facing — access to funding, technical know-how to improve their yields, and market access to sell whatever it is they produce. That became for me an opportunity to see how I could connect these farmers with so many other people interested in investing in agriculture beyond me, that were constantly told by this (Nigerian) administration to invest in agriculture.

He advises every startup to shun these common mistakes:

One mistake was that we raised money and felt like we could change the model immediately. It’s a mistake that many people make when they raise money or have a bit of breakthrough. It’s advisable to create your niche and stay on it. And even if you raise money, just amplify the efforts of what it is you’re doing.

One of the things that happened with Farmcrowdy is, even when we raised money, the 5 farms we started with remain the 5 farms we run till today. Although we are in a better position to scale our operations into other things and add new farms. Don’t change your model, especially if what you’re doing is working. You can add one or two things, but it’s important that you maintain what you’re doing that is working.

The second thing is, as much as I had brilliant people working with me, I was the only founder. I didn’t have people to bounce ideas off, rather I had people I only dished out instructions to execute what I had spent my time working on. Do not travel alone, that’s something I would tell everyone. You need people with complementary skill sets.

Three is when you raise money, you have to raise more. Even if you don’t have an active window for investors to come in, you need to be providing updates to potential investors that want to come in. So, it’s not when you want to raise money that you start having conversations. Let people already know your business before you have those conversations.

The other thing is, I promised myself that whatever I do again, it must be something that is making money from the onset. I’m not going to wait 3 years before I look at how to make money with any business. It must be something that I can see the margins already. It doesn’t have to make us profitable from day one, but at least I know that if we are able to get to a certain level in our operations, we will break even.

Save up as much as you can and network like your life depends on it. Tap into your network and finally, go to as many workshops as you can to brush up on your business knowledge. Always remember why you started when things get tough.

You are defined by the actions you take not the dreams you make. Because your actions are the antidote to fear, just feel the fear and do it anyway, be extraordinary in your thinking and your actions to stay relevant and to stand out in the crowd. As entrepreneurs we define the game we want to win, we are only limited by our imagination, so think bigger, and then think bigger than that.

Finally, as Nelson Mandela said, there is no passion to be found playing small, in settling for a life that is less than the one you are capable of living. Because when you are uber passionate about your WHY then your goals become non-negotiable.

Jason Njoku, Founder Iroko Tv, Nigeria

In mid 2015 I had a problem. We were months away from running out of money and needed to do something. There was no commercial solution. We needed to invent our way out of this. We had an Android app that sucked and needed to reallocate capital to product and engineering in NY in order to try and invent the future. We had just launched the channels with StarTimes and they were totally pissed at us for under performing and being a dysfunctional organisation. The deal was at real risk. Our foray into linear TV was turning into a total nightmare. Terrible start. I was living in NY, trying to lead the efforts to build our Android app.

For someone untuned to the sometime chaos of creation, IROKO was a mess. To make matters worse, I wasn’t even in Lagos. I was causing all this havoc from NY. I would drop in unannounced for a few days and retrench entire divisions. Rumours of a coup d’etat were reaching me from Lagos.

This was right in the middle of the due diligence for the $19m content and capital fund raise that closed a few months later. If I was a seasoned executive with experience, I probably would have found a way to not give people the impending sense of gloom and implosion over at IROKO, whilst negotiating the biggest deal of my life. Alas, I am not sophisticated like that. I am a simple man. I needed to reallocate capital.

But hey. It could also fail. Woefully. Nonetheless. It’s all about that deep experimentation nature and being comfortable with the 90% failure rates. But what I know now is if that were to happen, we at IROKO would fully embrace it. Accept our role in it. Do a full autopsy and then institutionalise it.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Norrsken has entered the East African startup market. The foundation is now open for startups and ventures in East Africa to have access to investment as well as mentorship for their businesses.

Nature and The Size of Norrsken’s Fund

Originally from Sweden, Norrsken Foundation is a coworking space and investment fund based in Stockholm. The new tech fund and entrepreneurship hub opened today in Rwanda will support ventures across the region.

Norrsken’s location in Kigali, Rwanda is former École Belge campus. The startup will be making seed investments of between $25K to $100K for early-stage startups in all sectors starting this year, Norrsken CEO Erik Engellau-Nilsson said in a press release.

However, Norrsken’s size is still being determined and Norrsken Kigali will extend the fund to larger series-stage investments from $100K to $1 million in the future.

Norrsken’s foundation’s move into Rwanda is strongly connected to the organization’s focus on the power of tech entrepreneurs to solve problems and generate capacity.

“We believe the single most important thing we can do here is to help people get wealthy, because if that happens, more investors will start to look at this region and see there are business opportunities and bring more capital,” said Engellau-Nilsson.

“The aim is to build the biggest hub for entrepreneurship in East Africa. Startups that receive Norrsken funding from its Kigali center will receive mentorship and support of the overall Norrsken organization and network. That includes unicorn founders, leading tech founders, and developers. We also look to expand that network to local accelerators and incubators.” said Engellau-Nilsson.

Why This Launch Is Important For East African Startups

This launch of Norrsken’s Kigali center is so important and significant for startups in East Africa because this is Norrsken’s first launch outside of Sweden. The organization is hoping to open up 25 markets globally over the next decade.

Formed in 2016 by Niklas Adalberth, the founder of Swedish payments solutions unicorn Klarna, Norrsken aims to support impact-driven, early-stage ventures. Engellau-Nilsson was an executive with Adalberth at Klarna from 2013 to 2017.

“We wanted to use our experience and tech to solve real problems instead of finding another way to do things like deliver burrito’s faster,” said Engellau-Nilsson.

Norrsken has already invested in 17 ventures, including three Africa-focused startups- agtech company Wefarm, digital publisher Kognity, and weather forecasting firm Ignitia. Over 340 entrepreneurs and 120 companies currently work out of Norrsken’s Stockholm location.

Why Rwanda?

Norrsken said it chose Rwanda as the base for its East Africa because of the country’s progress over the last decade on infrastructure, increasing internet penetration and improvement in its business environment.

Rwanda’s ease of doing business has significantly improved in 2019. The country ranked higher than any African country on the World Bank’s Ease of Doing Business list — 29th, even before Spain.

Even with a relatively small population (12 million) and tech scene, the government of Rwanda has prioritized tech events and development in the country. This includes becoming a leader on drone delivery and regulatory systems, working most notably with San Francisco based UAV startup Zipline.

Of the East African countries from which Norrksen will source investments, Kenya stands out as one of the continent’s top hubs for tech startup formation, VC, and exits.

African startups are gradually being funded

How To Pitch For Norrsken’s New Fund

Startups or ventures in East Africa desiring to pitch for Norrsken’s new fund may do by clicking the informational and contact link Norrsken posted for its Rwanda hub today.

“If there are entrepreneurs who want to reach out to us, we’re ready to go,” said Engellau-Nilsson.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

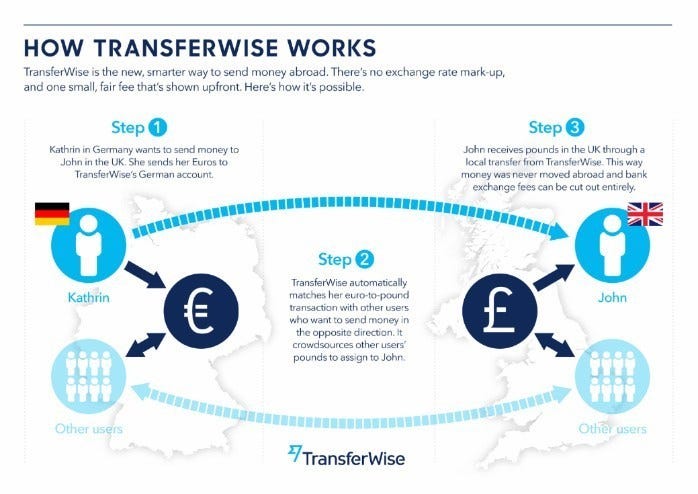

Barely 8 years since its life began in 2011, TransferWise, the UK-based money transfer startup launched by Kristo Käärmann and Taavet Hinrikus with headquarters in London and offices in a number of cities including Tallinn, New York, and Singapore, recently reached a $3.5bn valuation and made 33 new millionaires of its workers. Here are a few lessons to learn from Europe’s most valuable startup and its recent valuations.

TransferWise Is Partnering With Its Employees To Grow Its Value

Indeed, this is unlike other businesses where employees are expected to show up at workplaces, work, go and get paid. Over 1,600 employees at Transferwise collectively own around 2 million vested options, according to last year’s company filings. The latest valuation means that all these employees are now worth $250,000 per employee on average. Collectively, TransferWise’s employees and its alumni (so-called “Wisers”) are now armed with more than $70m to start up their own ventures. In total, 33 new millionaires from its employees’ figures were made millionaires. This brought the total number of employees or investors with six-figure holdings in the payments company to more than 150.

Now the startup is not insisting that the employees must stay back or reinvest their new wealth in the business. is encouraging those employees to go and start up their own ventures.

TransferWise’s Head of Recruitment, Ben Craig, said the startup actively encourages employees to channel their “entrepreneurial mindset” into other projects, through initiatives like a six-week paid sabbatical after four years with the company, even though this can lead to “Wisers” leaving TransferWise to focus on starting their own businesses.

“Our old employees are totally advocates of our brand and we’re advocates of their companies as well,” he says, referencing formal partnerships between TransferWise and Plum, and another potential partnership with Dataminer. “They’ve used our offices, we use their offices, we’re all in constant communication,” Craig adds. “We encourage employees who go out and start their own companies to lean on the skills of the two entrepreneurs who founded TransferWise, and to use the expertise of everyone who has worked with us over the last seven years to TransferWise to where it is today.”

The result of this is that the startup has now become the most valuable startup in the whole of Europe with its recent valuation at $3.5bn. Hundreds of its employees and early backers sold shares to new investors and existing stakeholders. Already more than a dozen former TransferWise employees have gone on to start their own businesses including Victor Troukoudes, chief executive of personal savings AI assistant Plum.

The wider diffusion of wealth to employees and investors is set to be a shot in the arm for the wider European ecosystem, as typically money from a successful startup is plowed back into other startups.

TransferWise Is Build On A Model So That It Not Only Allows Its Customers To Transfer Funds But Also To Buy Shares On Stock Exchanges

TransferWise allows its customers to open an online brokerage account and invest their savings in stocks of companies. Opening an online brokerage account is just as quick and easy as opening a digital bank account. The startup also allows its customers to find a cheap and reliable online broker via our broker recommendation tool.

For users of its online transfer services, there are 44 currencies they can use to exchange money between, within the app. They can also top up their Transferwise accounts in 18 currencies. The startup is also available in 144, almost all countries. At Transferwise, you can open an account for free and also maintain your account for free. There is no monthly cost to that.

Once your account has been opened, you can have your Transferwise ATM card delivered to your address for free. Unlike traditional banks, the startup does not charge any cost for the card. In fact, withdrawing money with Tranferwise from any ATM is free up to £200 / month and costs only 2% above this amount.

Also transferring money in the same currency as your Transferwise account has a flat fee. This will vary depending on your currency. The international transfer fee is €0.5–2.

Its only shortcomings are that it offers no interest on your savings; you cannot set up direct debits; overdrafts are not possible; joint accounts are also not available.

In short, TransferWise charges less than 1% on many currency transfers, compared to what the World Bank estimates is an industry average of more than 7%, thereby undercutting the fees charged by the big banks.

All these make TransferWise an uncommon success. Unlike many of its fintech peers, it has registered two straight years of profits, posting £6.2m in post-tax profits for its fiscal 2018 on £117m in revenue.

TransferWise Has Successfully Shown A New Way Startups Can Succeed Without The ‘Distraction’ of IPO

The founders of Transferwise, Taavet Hinrikus, and Kristo Kaarmann, said this week that they sold “much less than 20%” their own holdings, which are worth $1.3bn at the new valuation. Other big shareholders include Andreessen Horowitz with $65m worth and IA Ventures with $267m worth. Hinrikus said the $292m sale would allow some of the company’s earliest backers to realize the substantial gains on their investments, without forcing it through the “distraction” of an initial public offering.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Even though e-commerce is seriously gnawing at physical shops. Physical shops with a messy environment would most definitely get a little crumb of what is left. Of the 70% of consumers surveyed in a study commissioned by ServiceChannel, a facilities management platform, and who said they had once experienced messy stores, over two-thirds have walked out of stores because of the way they looked.

The study suggests that struggling retailers who neglect stores to cut costs hasten their demise by turning off shoppers. The survey was carried out on 1,521 consumers and 70% of them said they recently have had a negative experience with a messy store.

Over two-thirds admitted they have walked out of stores because they were messy or disorganized.

Four out of five shoppers said they would rather have a clean store than ones with the newest tech, and two-thirds said retailers are forgetting the basics—like clean floors and well-stocked shelves—in the rush to add tech.

“The vast majority of purchases are still being done by people walking into a location. And their experience of that location has never been more important,” Buiocchi, the CEO ServiceChannel said in an interview.

“If you look at folks like Allbirds or Warby Parker, Bonobos or Soul Cycle or Shake Shack, their locations are so comfortable and well laid out and so well maintained. You would never walk into a Warby Parker or a Shake Shack and say ‘Man this place is messy.’ Or the lights are dim or it’s too cold in here. They just don’t let that happen.’’

ServiceChannel is in the business of selling software and services that allow retailers to manage store maintenance, connect with and pay contractors, and track invoices, so it is no surprise that it is touting a survey that concludes store cleanliness is crucial. But he has a point that is often overlooked by retailers.

With ServiceChannel, retailers can book contractors and manage maintenance jobs on mobile phones.

“Much like when you get an Uber or Lyft ride and the entire ride is digitally recorded, the transaction is digitally recorded so someone 3,000 miles away can go fix a toilet for you at a Banana Republic and you will know based on the GPS coordinates when that person got there, how long they stayed, whether they showed up on time, and they can send you a picture,” Buiocchi said.

ServiceChannel is seeing that many of the new online brands that are opening stores are quick to recognize the value of rigorous maintenance and are signing up as customers.

“There are the people that get it, and there are the people that don’t get it,” Buiocchi said. “Five years from now what are the chances that the people who don’t get it are going to be in business?”

Buiocchi says reports of a retail death end are overrated. As stores close, new retail disruptors are opening locations and expanding.

“Good progressive retail is investing in their brick-and-mortar experiences and enjoying the benefits of that,” he said. “Bad retail is not and they’re unfortunately being penalized for that.”

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Looking to raise capital for your startup through equity crowdfunding? No loans? Just some hard currency from some money messiahs? That is what South African businesses are turning to now. Intergreatme has recently succeeded in raising over R32.7 million ($2.2 million) by simply putting up an online request for equity funding on Uprise.Africa and getting overwhelmed by public contributions. This was a big moment for the startup looking to help ordinary people get rid of the daily pain associated with submitting forms and documents through an innovative technology platform.

The startup was founded by a team of young South Africans three years ago and is now valued at about R120m. The team envisions a world where personal data can easily and securely be shared among a host of applications. As long as an activity requires a person’s information, Intergreatme sees a market.

How The Startup Scaled The Hurdles and Raised The Funds

Narrating how the startup raised the funds through equity crowdfunding, Intertreatme CEO said in a recent interview:

We had no idea how successful it was going to be. We thought it was going to be like a 60 day campaign of climbing Mount Kilimanjaro. We needed to get 250,000 that day and we hoped to just do some cold calls. I printed out my full contact list on my phone and my whatsapp list, my email list, and we thought it’s going to be a campaign. But we had no idea that the demand was more than that. We thought that we could raise the 24 million and we thought that we were going to procure a common amount ever.

For startups looking to use crowdfunding to raise capital, he says they are not just going to put a pretty video online and hope people come and invest. They need to do the hard job behind the scenes.

‘‘There are billions and trillions of dollars of money waiting to be deployed,’’ he says. ‘‘People get paid money to invest money. But your business fundamentally needs to be right. Your team needs to be right. What you plan to do needs to be right. So do those things right. And then you can just sample your user base. Just run a poll on Facebook or Instagram or Twitter, just saying, ‘‘Hey, if we rank car, would you invest? And if so, how much will you? You’ll get, you will get an answer. I don’t think you need to do a lot of work to get those answers.

On the pattern of investing, he said about 402 people turned up and contributed to the startup through equity crowdfunding.

We had minimum commitment of 1000 rand and a maximum commitment of 5 million. We had about five, five millions. Wow. We had a couple of millions. It was so cool. We didn’t expect it. And it was just people. We started by saying, if you’ve used our technology before and you sure that you had the wow moment, would you like to invest in this? Tick this box, if you want. But ultimately they, they invested in us as people.

Before that, we had a very successful launch party, which I think was key to the fundraising, where we had a private donation from our whatsapp list. This was two weeks before that. And we’ve got about 120 investors there. And then we had about 250 people at our launch party when the startup was first started. We used that time not to sell the technicalities of the business, but to sell out emotional stories as founders to show that it’s normal for us to overcome unrealistic odds.

He said the crowd bought into the human stories and not the technicalities.

‘‘We said it’s normal for us to overcome adversity and challenges, that it doesn’t matter what comes our way. It’s normal for us. We will find a way to succeed. And so people bought into the emotional story. They always say, you shouldn’t invest in a business. You should invest in people. And yeah, basically people bought the founder’s shares, in the founder’s energy, in the founder’s vision. And so literally everyone in that room at the launch party made us the first 27 million. And so we sold apps 27 millions in the first 72 hours and there were just a frenzy of people trying to jump on and grab the last time.

I think if you look inside now, it is 32 million, 409,000 rands. So they’ll have to be some refunds for some people who just came in and about a hundred people came in on the last day, like before three o’clock.

On Why They Choose Uprise.Africa to Raise The Funds

He says Uprise.Africa has direct exposure to all the upsides and downsides of the business

‘‘I didn’t know who they were,’’ he says. ‘‘We made it a conference. I related with its CEO as a founder. She said cool. They have a framework and are licensed to do it. So effectively it’s as good as a payment gateway. So if you’re running an ecommerce business and pay fast or need paypal or visa, mastercard go to them for a widget. They can accept payments, but they’re relying on how good your business is .

One of my favorite little proverbs is if a bird is sitting on a tree on the branch, it’s not worried about the branch snapping. It has faith and confidence is in its wings. Crowd funding is an easy way to take money from the crowd, but there’s a context to it. If we show the analytics of the money we raised, everyone is within one or two steps of our network. And so accountability is really your socially accountable tool to your community and your network. If they believe in you, you’re not going to have a much bigger responsibility to them.’’

He says Uprise.Africa will own a 25% stake in the startup.

‘‘They will also have an independent board member. Uprise.Africa will be representing the crowd and yeah, fix me. But there are voting rights and things. So Uprise.Africa has the stake on behalf of the people who invested in the initiative. I think they manage it for about 12 months or so and then they give it to us. They have also put automated technology in place for the share registers and the certificates and the reporting.’’

On Why More Black Women Invested In The Startup Through The Crowdfunding

‘‘I think maybe it’s because we spent a lot of time with Uber drivers and optimistic ladies and all security guards and receptionists. They used our technology and they’re like, sweet, I can get my license renewed. Daily visits to the management system are amazing. So it is just crazy for us because we actually thought that we were so proud that we managed to get 30% black female ownership. They were like, this company’s plan is going to dilute that potentially down to 22%. We had signed agreements to become level two. And so it was a concern. It was just, again, a miracle from the universe that it actually ended up swinging way better than we could give. I’ve imagined it. So I think that’s the beauty of opening it up to the crowd. If you’re focusing on one or two high net worth individuals, you’re kind of going for a specific target.’’

Other Startups In South Africa Are Also Resorting To Crowdfunding