African startup founders are succeeding all over the world. Although in faraway Australia, Jamila Gordon’s Lumachain has just raised $3.5 million in a funding round led by the CSIRO-linked venture capital investor Main Sequence.

Lumachain’s founder Jamila Gordon previously held senior roles at Qantas and IBM after immigrating from her native Somalia in east Africa. The company is helping businesses in the food supply chain ensure they are ethically sourcing produce following the introduction of new laws against modern slavery in Australia.

Here Are What You Need To Know

When Jamila Gordon was a five-year-old in Somalia she was forced to work instead of receiving an education — fast forward several decades, and she has just raised $3.5 million to grow a business she hopes will help in the fight against modern slavery.

Gordon — a former chief information officer at Qantas and senior executive at IBM — helms Lumachain, a software-as-a-service company with a big social purpose.

The investment comes as businesses across all sectors in Australia are under pressure to ensure they are not profiting from forced labour or other forms of modern slavery.

Earlier in July, Australian retailers Cotton On, Target and Jeanswest announced they were investigating their own processes after an ABC Four Corners report found the companies were linked to factories in China where forced labour could be occurring.

Two brothers were jailed in the UK in January after being found guilty of breaching the country’s modern slavery laws for exploiting Polish workers in a warehouse owned by athletic wear retailer Sports Direct.

Companies in the food business might want to look to blockchain to avoid a similar fate.

What The Company Does

The company’s product uses blockchain technology to find and track items in the food supply chain which could be unethically sourced or the product of forced labour.

This function is not just good for society, but good for business, as it can help reduce waste, avoid recalls and — for companies with revenue of more than $100 million per year — ensure they stay compliant with the Modern Slavery Act introduced in Australia in 2018.

That might be part of the reason Gordon has been able to raise millions from private investors, including some heavy hitters like Main Sequence Ventures, which manages the CSIRO’s, Innovation Fund.

“The way goods move within the supply chain is still very basic, which means there’s still a lot of waste, inefficiency and risk,” Gordon said in a statement announcing the successful funding round.

“With growing demand for better quality food products and ethical and transparent business processes, plus a rising middle class across Asia, we see tremendous opportunity to improve the productivity, security and safety of what we eat.”

Main Sequence partner Mike Zimmerman said in the same statement that “absolute trust, verification, and efficiency” are needed in the global food supply chain and that Lumachain is “best positioned” to provide it to the industry.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Ethiopia is on course to liberalize its economy. Apart from opening bids for its first-ever privately owned telecom license, foreigners who are not citizens of Ethiopia may soon get a law that would allow them to set up and run insurance services as well as set up microfinance banks.

Here Is The Deal

Two draft bills that aim to restructure the country’s existing business law governing insurance companies and microfinance institutions have been passed by Ethiopian Council of Ministers.

The bills would definitely scale through and be passed into law since they were developed by the National Bank of Ethiopia and endorsed by the Ethiopian Council of Ministers.

What is just remaining is for the Ethiopian House of People’s Representatives, the Ethiopian parliament’s lower house, to which it had been forwarded to, to put its final ratification on it.

Under the new law, all that is needed, among other things, for a foreigner to set an insurance or microfinance business is for the foreigner to be a foreign national of Ethiopia.

This is part of restructuring Ethiopia’s current laws on insurance and microfinance sectors, according to the Ethiopian PM’s office.

The decisions to amend the East African country’s existing business laws governing insurance companies and microfinance institutions were made in line with recent and ongoing “large-scale” reform measures in the sectors, the Ethiopian Prime Minister’s Office revealed in a statement.

Here Is The Change These New Laws Are Bringing To The Table

Article 656 of the Ethiopian Commercial Code provides that the law shall determine the conditions under which physical persons or business organizations may carry on insurance business.

Recourse is however made to other parts of the commercial code and other laws to find out as to who may undertake insurance business and the conditions under which it may be undertaken in Ethiopia.

Accordingly, Article 513 of the commercial code provides that banks and insurance companies cannot be established as private limited companies, i.e., a private limited company cannot engage in banking, insurance or any other business of similar nature.

Similarly, Article 6(1) of the Licensing and Supervision of Insurance Business Pro No 86/1994 provides that no person may engage in the insurance business of any type unless it applies to and acquires a license from the National Bank of Ethiopia for the particular class or classes of insurance.

Furthermore, Article 4(1) and Art 2(3) of the same proclamation provide that such person has to be a share company as defined under Article 304 of the commercial code.

These requirements/conditions in effect prevent foreigners from engaging in the insurance business and foreign banks from opening branches and operating in Ethiopia.

The most probable reason for this position is the need to protect infant domestic insurance companies which do not have the desired financial strength, know-how, and human resources to be able to compete with foreign banks which have the superior capacity in these areas.

The new laws, therefore, are preparing to change all these.

Under the new law, all that is needed, among other things, for a foreigner to set an insurance or microfinance business is for the foreigner to be a foreign national of Ethiopia.

Freeing Up The Economy

Ethiopia has also recently announced that government would no longer be monopolizing its telecom sector. At the moment, there is no MTN, Airtel, Safaricom, Vodafone or any other mobile telecom operator in the East African country of Ethiopia, but that will no longer be the case before this year ends. The country is set to award its first set of telco licenses to multinational mobile companies by the end of 2019.

Before this happens, Ethiopia’s government has continually monopolized the country’s telecom industry. Hence, this is expected to end a state-wide monopoly and open up one of the world’s last major closed telecoms markets.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Founders have to be resilient and thick-skinned. Prepare yourself to exhaust your network of investors, and accept the fact that fundraising is going to take time, even if that’s a hard pill to swallow.

Securing a fresh injection of investment capital can drastically accelerate your startup’s growth, so it’s good to know that there’s no shortage of money up for grabs these days. According to a recent venture capital report from Magnitt, nearly US$800 million in investments were made in the MENA region last year.

But just because the money is out there doesn’t mean the fundraising process will be a breeze. The reality is that investors are picky and often guided by strict criteria to fit their investment thesis. When you seek them out, most will reject you, that’s just part of playing the game. Luckily, there are some rules that can make the process a bit more predictable. Odds are you get a “no”.

Taking into consideration the media’s infatuation with writing articles on multimillion-dollar investments into startups on a daily basis, it can look like these deals happen overnight. They don’t.

In fact, most entrepreneurs will openly tell you about what a struggle the fundraising process can be. Author and business guru Steve Schmitz puts this in perspective in the context of his own fundraising journey.

He wrote: “We raised $40 million of equity from 63 investors. We contacted more than 1,000 prospects. That’s about 6%. That means 94% of the people said no.”

Blackstone CEO Steve Schwarzman had the same 6% hit rate when starting out, too, and his company now manages more than $500 billion of capital.

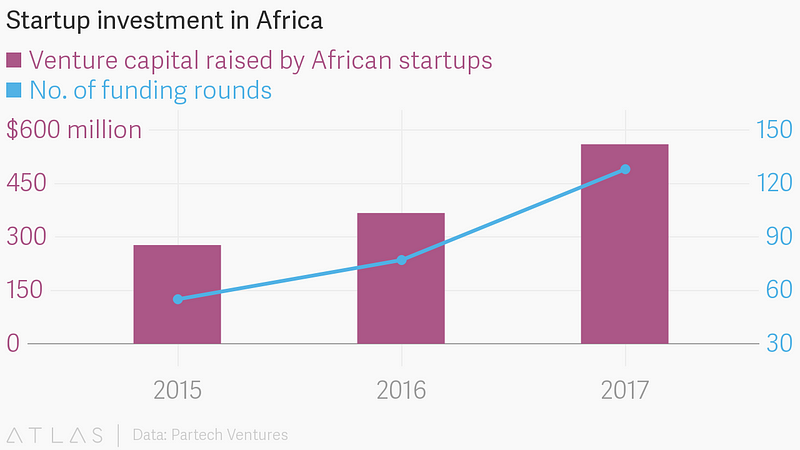

Startup investment in Africa (2015–2017). Credit: Quartz/Partech Ventures

Think of it this way: let’s assume you’re raising a $600,000 seed round, and the average check size for your investors participating in the round is $100,000. This would mean you’d need six investors in on your round. If you operate under the 6% rule, you would have to meet with 100 investors to close your round.

Keep in mind that the 6% rule holds up for qualified investors who cut checks of the size you’re seeking at companies that are at the same stage you are. If you hit up the SoftBank $100 Billion Vision Fund for a $50,000 unit size, that wouldn’t count as an investor. Being told “no” is normal.

Famed speaker and author Tim Ferriss has an excellent podcast episode about just how critical it is to learn from every “no” we get. One of his guests mentions that she heard “no” at breakfast, at mid-morning coffee, at lunch and twice during the afternoon, before ever getting to dinner (where she heard it again).

Founders have to be resilient and thick-skinned. Prepare yourself to exhaust your network of investors, and accept the fact that fundraising is going to take time, even if that’s a hard pill to swallow.

How To Secure The Magic 6%

The 6% rule can apply in any part of the world, but some places will have to stretch outside their borders to make it work. In the MENA region, fundraising often forces founders to go outside their hometowns and home countries to complete fundraising. Online crowdfunding platforms have been instrumental in removing geopolitical borders stateside, and this will surely benefit the 344 million households in the developing world, too. Regardless of where your investment comes from, you can set workable goals to achieve success under the 6% rule.

Here’s How:

1. Use your unit size to set your investor target list size.

It’s easiest to break the total investment you’re seeking into smaller units for starters. Think back to the example above of the $600,000 investment. If you were aiming for $50,000 units, the 6% rule would require you to talk with 200 qualified investors (assuming each investor bought one unit in the worst-case scenario), or 100 investors at $100,000 unit sizes. You can use the rule and your unit sizes to determine the size of your investor target list.

Egyptian startup Swvl did this when it secured five investors for its $8 million Series A round in April 2018, and the Series B that followed at the end of the year.

Once you determine your list size, create a pitching schedule. Assuming it’s not Ramadan -which tends to bring the investment world to a screeching halt- start pitching five times each week for 20 weeks. Factor in eight weeks of researching targets and eight weeks for term sheets to close the deal, and you’re looking at 36 weeks minimum from start to finish.

2. Be ready with prepped materials.

I always have the staples ready to go during fundraising time. Read Venture Deals by Brad Feld to get your lingo down, and understand the basics, it’s VC 101. Then, put together a pitch deck, a term sheet, a clean cap table, a data room, accurate and up-to-date financial statements, and a financial forecast. Preparation is key to secure and close deals, and doing this homework in advance shows that you know what you’re doing.

Verifiable forecasts coupled with a concrete plan to reach them is what secured Wuzzuf its $8 million investment.

This Egyptian startup bootstrapped its job site and recruiting platform in the aftermath of the 2011 Egyptian revolution.

Having survived the toughest economic conditions, the company is now one of the fastest-growing internet companies in Egypt, with more than 250 employees expecting to help 1 million people get hired by the end of this year.

3. Lose the materials when it’s more about relationships.

Pitch decks are great for angel group presentations and pitch competitions, but I’m not a big fan of bringing all of that to one-on-one pitches. If you’re meeting an investor at your nearest Costa Coffee, pitch without materials.

Building a personal connection is what got Jamalon its $10 million Series B investment, not a stack of papers.

Founder Ala Alsallal credits the mentorship he received from Fadi Ghandour, Aramex founder and Wamda Capital chair, with his success, saying relationships made the difference in getting him where he is today. So put away your computer, break the ice, share your story, and dive into your big vision. If the person shows interest, you can talk about materials.

4. Maintain a pipeline, and take your time.

Organize your resources and manage the investors you talk to in a customer relationship management system or a spreadsheet, just as you would a sales pipeline.

Take a note from the Sandler Training book, and use the “submarine trick,” which is inspired by World War II movies in which crews handle attacks on their submarines by closing the door to each compartment behind them.

Salespeople should close each step completely as they go, that way there’s no risk of needing to turn around, and go back on something that’s already been decided. Never forget that a signed term sheet is engagement, not a marriage.

Definitive documents take time to prepare. Wires take time to transfer. Plan ahead so you don’t run out of cash before you complete your raise.

Ultimately, you won’t fundraise for your startup overnight. And rejections will come. Period. Just remember that even if 94% of investors say “no,” 6% will give you the “yes” you need to make the grind pay off.

Zach Ferres is the CEO, Coplex, a Venture Builder that partners with industry experts and innovative enterprises to start high-growth tech companies.

The startup recently announced a $2.5M equity financing round. The Series Seed Round was led by DFE, the family office of Bennett Dorrance of Campbell Soup fame; and AZ Crown, the family office of Insight Enterprises Co-Founders Tim and Eric Crown.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Fintech is where the money is. Africa’s fintech companies have raised $320 million in funding since January 2015 and the ecosystem has surged 60% in the last two years. Africell understands these statistics and is willing to use its wide reach to give it a shot. With $100 million funding from the OPIC, the US government’s private investment fund, the African telecom company is more than ready to continue the disruption game.

Here Is The Deal

The Uganda-headquartered Africell’s new funding is more than $100 million and part of this would be used by the company to expand access to telecommunications in Africa.

The countries Africell is targeting are Uganda, DRC, Gambia and Sierra Leone.

Apart from this $100 million funding, Africell has set aside $300 million to spend on a new market like Angola within the first year of commencing business if they secured a license.

Africell would bid to become the fourth operator in Angola, which was expected to reissue a tender in the next two months after the original tender for the license was annulled in April.

A larger part of the $100 million would be spent on fintech.

The unbanked population is what Africell is targeting here.

Global fintech funding rose to $111.8 billion in 2018, up 120 percent from $50.8B in 2017 and that is a huge opportunity Africell is hoping to tap into.

To make this happen, Africell is looking at expanding its fintech services, such as mobile payments, micro-insurance, and micro-finance.

Mobile money payments, pioneered in Kenya, have expanded rapidly in other African nations where many people do not have bank accounts.

The 18-year-old company has 15 million subscribers across its four African operations.

The Game Is In Competing Profitably And Not Just Expanding

“We are looking only at markets where we can make a difference,” said Africell founder and chief executive Ziad Dalloul indicating this included Angola and Zimbabwe.

He said Angola was attractive because the country’s state-owned Angola Telecom had a large market share that could be vulnerable to a more aggressive private operator like Africell.

“Day one, we can just change the whole thing…drop market prices, expand into rural areas, provide faster, better service on internet. These are the things we know how to do. So that’s why we are keeping an eye on Angola,” he said.

And Africell Is Turning Its Eyes On Fintech For Reasons More Business Than Charitable

“No space has quite the potential impact of the fintech space when it comes to impact — and profits — in Africa, with startups operating such platforms able to significantly address the major issue of financial exclusion on the continent and thus promote development in all sorts of other areas,” saysDisrupt Africa co-founder Tom Jackson.

Nigeria led the investments in 2018 with 58 startups raising $94,9 million, followed by South Africa with 40 businesses that raised $59,9 million, and Kenya was third.

Fintech investment was still the most popular, bringing in 39.7% of total funds “South Africa, Nigeria and Kenya remain the main three markets, with 141, 101 and 78 active ventures respectively, accounting for 65.2% of Africa’s fintech startups,” Jackson says.

US fintech investment for 2018 more than doubled to $52.5B, from $24B in 2017, across a record 1,061 deals.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

The Germany Africa Business Forum (GABF) announced Thursday a multimillion-Euro funding commitment to investing in German energy startups that focus on Africa.

The GABF, based in Berlin and Johannesburg, South Africa, said the funds are the first of their kind for the advocacy group seeking to advance German partnerships with the continent.

“Our initial goal is to support the investment in German companies and to start with funding allocations by the end of this year,” said Sebastian Wagner, co-founder of the GABF.

The news was welcomed by Cameroonian business leader NJ Ayuk, the CEO of Centurion Law Group based in Equatorial Guinea. “The future of Africa’s energy industry will depend on technology and innovation. When German startups and Africans work together, we can build something unique for both our peoples,” Ayuk said. “I applaud the GABF for this well-thought-out initiative. I believe it is in line with the goals of the G20 Compact with Africa, driven by Germany.”

That compact, launched in 2017, is open to all African countries and has 12 nations participating to date. They include Benin, Burkina Faso, Côte d’Ivoire, Egypt, Ethiopia, Ghana, and Guinea, along with Morocco, Rwanda, Senegal, Togo, and Tunisia. The compact places renewable energy and rural employment as priorities for African investment.

The GABF also launched in 2017, with a parallel vision to facilitate German investment in Africa by connecting top African business and political leaders with their African counterparts.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Kenyan agritech startup Taimba has joined the league of African startup fundraisers. US impact investor Gray Matters Capital is committing $100 000 in the Nairobi-based B2B agritech startup to help it scale its operations.

Here Is The Deal

The investment from Gray Matters Capital was made through its gender lens early-stage fund GMC coLabs.

The startup explained that the markets it wants to take on in Nairobi are Umoja, Kayole, Pipeline/Imara Daima, Kawagware/Waiyaki way, Kahawa west/Githurai, and Southlands/Langata.

Last year, Taimba was one of 15 startups selected to join the Make-IT accelerator.

The startup also emerged the winner of the inaugural Disrupt Africa Live Pitch Competition which was held in Nairobi last year. Taimba also won $10 000 at the 2018 Food+City Challenge Prize at SXSW.

The deal also marks GMC coLabs fourth investment in Africam with investment ticket sizes of up to $250 000. The impact investor’s other investees include Rwanda’s African Renewal Energy Distributor (ARED), Ghana’s Redbird Health Tech and Nigeria’s Sonocare.

In addition, the investor has also supported two other start-ups from the continent — Kenya’s parent advisory turned e-commerce start-up MumsVillageand Sierra Leone based Mosabi as part of its global digital accelerator program — GMC Calibrator earlier this year.

A Look At Taimba

Taimba is a mobile-based platform that connects rural small scale farmers to urban retailers, restaurants, hospitals, and schools in Nairobi.

The startup was founded in 2017 by Dominique Kavuisya and Joan Kavuisya

Taimba aims to remove middlemen, shrink the agricultural value chain, cut wastage and make products more affordable.

Gray Matters Capital said the startup currently works with 2000 farmers as well as 15 farmer savings and credit co-operatives that sell products that include potatoes, tomatoes, cabbages, and carrots.

Informal greengrocers make up the bulk of Taimba’s 310 customers at 85%, this while restaurants and cafes make up 10% of its customer list, with schools and hospitals located outside of Nairobi making up 5% of its clientele.

“The funding is a shot in the arm for us to strengthen our warehouse infrastructure by setting up cold storage facilities and also our delivery logistics so that we can cater to six new markets within Nairobi,” noted Taimba’s CEO Kavuisya.

Outside of Nairobi, Taimba is planning to launch a pilot in Mombasa and Kisumu City by next year. In addition, the startup is also looking to produce new products that include fruits, nuts, and eggs as part of its farm product catalogue.

The startup also has plans to replicate its model in Tanzania, Uganda, Ethiopia, and Rwanda over the next five years.

GMC coLabs portfolio manager Jennifer Soltis said Taimba has built a solution that can be replicated in other markets in East Africa “with minimal tweaks”.

The startup’s first deal which was signed last month marks Taimba’s first investment. The company currently employs a team of seven permanent staff and five part-time workers.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

For those who have used Facebook, Twitter, Instagram or any other social network in the past few days, there are huge chances that they might have come across their friends, family members, acquaintances and countless others who have suddenly and mysteriously become grandparents with wrinkles and greyed hair or who have simply gotten younger, grown a beard or changed their appearance in any other more or less obvious way. The magic behind this sudden alteration in looks is FaceApp, a mobile app that uses machine learning (AI) to manipulate faces on digital photographs. FaceApp has gone viral after a couple of celebrities and influencers posted impressively accurate images of their future selves on social media. But behind all the frenzy is CEO Yaroslav Goncharov who had no idea that FaceApp’s virality would be so overwhelming for him.

FaceApp

“We have success, but very unusual success,” says Goncharov, who owns 100% of the business.

Here Is How It Happened

As the following chart below shows, FaceApp had a moment in the limelight before, but the 2017 hype around the app was much smaller than the current craze.

According to estimates from Priori Data, the app clocked nearly 30 million downloads in July, catapulting it to the top of the app store charts on both Android and iOS.

In fact, currently, FaceApp has been downloaded (although not active users) revealed on Google Play, in excess of 100 million.

Yaroslav Goncharov Had Been Digging and Tilling At FaceApp Since 2016

Russian Goncharov’s success is a case of building momentum and mastering the art and game of his industry. He has worked on Windows Mobile for Microsoft and co-founded a company which was sold to Russia’s Google, Yandex, in a reported $38 million deal that made him wealthy.

“I worked at Microsoft in Redmond, U.S., and in the evenings I wrote [code for] a bot with whom one could play poker. The neural network was only a small, evaluative part of this bot — at the time, there were no ways to create a solution entirely based on the neural network,” Goncharov said in a 2017 interview with the Russian Afisha Daily

Upon leaving Yandex in 2013, he invested his time and resources on creating his own products. His first output is a hotel Wi-Fi testing tool that garnered some success. Goncharov, however, desired to create a product from face-generating algorithms, he starting working on FaceApp in 2016. FaceApp launched in 2017, still in what Goncharov describes as a beta version. Even in its basic form, it went viral for the first time after a “hotness” filter made people prettier.

“FaceApp was born at the junction of two important trends. The first is the ever-growing value of photos and videos. There is an opinion that stories from Snapchat, Instagram and their analogs will soon kill news feeds like Twitter. Facebook is already moving in that direction,” Goncharov told Afisha two years ago.

With millions of users in love with the app, Goncharov was quick to draft a business plan. He envisioned a reality where people would pay for an automated photo editor, so he added a paid-for subscription offer that would remove the FaceApp watermark and irritating ads, as well as add some premium features. Goncharov’s hope was that FaceApp would replace PhotoShop editors with AI.

“The second trend is neural networks. That’s what they call the simplified analog of the human brain implemented in computer code. To create it, they build a huge network of software simulations of neurons and synapses capable of analyzing and storing information. Such technologies underlie machine learning, artificial intelligence, cybernetics, and much more. I have been doing this for quite some time now. I trained the first neural network about ten years ago.”

Cashing Out Big

It has since paid off, according to the CEO.

Without providing substantiating data, he claims FaceApp has been profitable since the first launch two years ago, with “good” revenue and growth figures. “We’re very profitable,” he says.

“I could easily have got investment from Silicon Valley… but we had enough to grow organically.”

While Goncharov has no need for Silicon Valley investors for now (he says he may approach VCs in the future), others in the bubbly business of photo apps have either taken big funding rounds or been acquired.

Snapchat snapped up Looksery for a reported $150 million in 2015 and Teleport for $8 million in 2018 to help grow its library of AI-powered filters, while Oakland-based photo app VSCO raised $90 million over two rounds.

FaceApp makes money from nothing more than a paid-for subscription service. But the founder has not disclosed how much revenue that it is scooping in or how many paying customers he has. He is also secretive about user numbers.

Goncharov does, however, disclose that the paying customer base was roughly 1%. Even taking a conservative estimate of 100 million users across Android and iOS, and just 1% signing up for a single month’s premium use at $3.99, the company is making at least $4 million per annum, and potentially a lot more if it’s locking in more users. (It’s also possible to pay $20 for a year’s access or $40 for lifetime use). Goncharov declined to comment on that estimate. But it’s not bad for a 12-employee business that’s been profitable for two years, by Goncharov’s account at least.

What’s Next?

Though other companies like Snapchat already do what FaceApp does with live filters, Goncharov doesn’t want to launch something that’s anything less than “magical.” He’s hoping that magic isn’t diminished by another privacy panic.

But Yaroslav Goncharov’s biggest success (and stress) has come with a company that’s minuscule by comparison: FaceApp. Leading a staff of just 12, the geeky, excitable 40-year-old has created what’s currently the world’s hottest (and possibly most controversial) app, which uses artificial intelligence-powered filters to gender-swap or radically age selfies.

“We only upload a photo selected by a user for editing. We never transfer any other images from the phone to the cloud,” FaceApp was quick to state. “We might store an uploaded photo in the cloud. The main reason for that is performance and traffic…Most images are deleted from our servers within 48 hours from the upload date.”

Goncharov said those terms were so broad because he had planned earlier to turn FaceApp into a “social network for faces.”

“To do this kind of product, our privacy policy had to be very similar to what Instagram had. Our current privacy policy is very similar to what Instagram has … but nobody blames Instagram, because it’s Instagram,” he adds.

Besides, it’s not FaceApp that users should be worried about when it comes to privacy, but all the other apps they’re already using, Goncharov argues.

“There are so many other apps that collect much more data,” he says. “We just don’t.

The App topped the download charts for both Android and iPhone this past week after millions followed celebrities like Dwyane Wade, Drake and Iggy Azalea in doing the “FaceApp Challenge.” The “challenge” was simple: take a photo, apply the aging filter and post an image on Instagram, Twitter, wherever, of the older you.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Indeed, this could be ground-breaking. No more waiting for years and centuries for startup IPOs to happen. With this new deal, once startups raise funds through equity crowdfunding in South Africa, the startups’ shares automatically become tradable on the floors of South Africa’s Stock Exchange. Money more here!

Here Is How Everything Is Going To Happen

Today, Africa’s first equity crowdfunding, Uprise.Africa, and South African alternative exchange ZAR X have come to an agreement that will see the mini stock exchange list any up-and-coming entities, which have already successfully raised capital via crowdfunding, and freely trade their shares on the open market.

Not only could the arrangement be the funding gap filler that fledgling South African entrepreneurs desperately seek, but it could bring the local capital market to the people.

The partnership also solves the fundamental flaw of all other pre-IPO models, Nel says, namely that once a company has issued the shares they remain fairly illiquid, with investors having their funds tied up until that company looks at going public.

Tabassum Qadir, co-founder, and CEO of Uprise.Africa says they plan to conclude at least three deals a month.

“We are simplifying venture capital through this mutually beneficial partnership for both entrepreneurs and investors,” says Qadir

“It means, when you have a business idea, you can leverage the Uprise.Africa platform to potentially raise capital quickly and ultimately list on a licensed stock exchange, making the shares tradable,” she says.

Etienne Nel, CEO of ZAR X, agrees that equity crowdfunding democratizes start-up financing by enabling entrepreneurs to raise additional capital, but also allows more people to invest in local businesses and in listed equity.

“Furthermore, it gives crowdfunding investors liquidity in their investments, which ultimately drives financial inclusion and job creation,’ he adds.

He says it gives this new generation of investors the same opportunities as high-net individuals and institutional investors, who can afford the investment costs of larger stock exchanges.

Not only are lower minimum investment amounts possible, but certain transaction fees and regulatory costs also don’t apply.

For example, the alternative exchange community is not subject to the Financial Services Conduct Authority (FSCA) protection levy and doesn’t charge for the custody of funds.

“It is also no secret that the ‘incumbent’ is more focused on institutional money that the interests of retail investors,” Nel says.

Equity crowdfunding is gaining much popularity across the globe, and it doesn’t look like it will slow down soon.

The World Bank, for instance, estimates that the global equity crowdfunding sector will be worth more than $93-billion by 2020.

Upraise.Africa is also putting the funding model on the map. It made headlines recently by facilitating a R34-million capital raising exercise for Intergreatme — a business that describes itself as a “platform that provides users with a secure, simple and effective way to share personal information with anyone”.

Qadir says the platform enables the trust to be built between investors and entrepreneurs and in doing so creates a supportive business ecosystem.

“And now crowdfunding investors can trade their holdings on the ZAR X platform,” she says.

“We have cracked the code. We have now derisked the proposal. We give investors the option to exit by allowing them to sell their shares at will. Usually, and in the current format, investors are tied up in an equity crowdfunding investment for between 6–8 years.

“We also aim to disrupt the country’s traditional funding landscape,” she adds, “which is rather limited and restrictive at that.”

As the IPO model certainly remains very viable for certain businesses of size wishing to launch into the public markets, it is not for everyone.

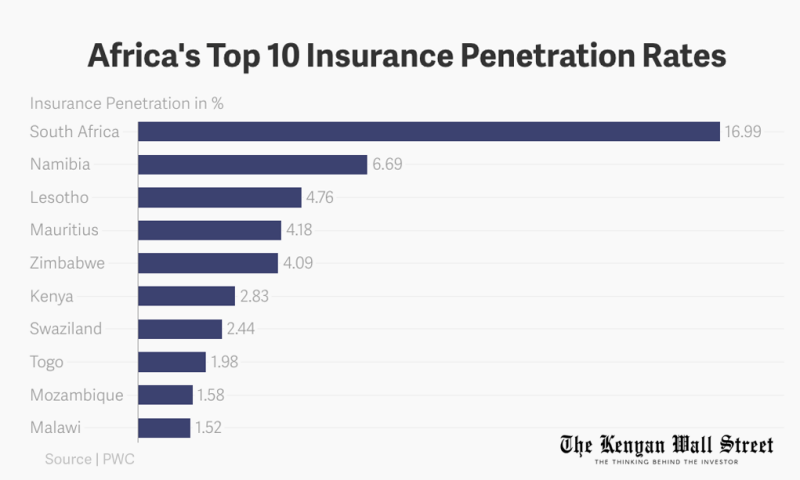

After these stock exchanges, the next biggest stock market in Africa is Mauritius, followed by Tunisia and Namibia.

Business Maverick had reported recently that it is a capital-raising method on the decline, and Nel says that they “are simply seeing more opportunities for investors and founders looking for methods that better fit their needs than what the traditional incumbents are offering”.

“The compliance costs of being listed on the bigger boards are devastating, and private money and smaller enterprises just find some of the disclosure requirements too cumbersome and restrictive,” he adds.

The Financial Sector Conduct Authority,(FSCA), (the South African market conduct regulator of financial institutions that provide financial products and financial services, financial institutions that are licensed in terms of a financial sector law, including banks, insurers, retirement funds and administrators, and market infrastructures) is still in the process of finalising regulations pertaining to crowdfunding, after releasing its draft proposals in mid-2017. The lack of regulation has been cited by some in the sector as the reason why equity crowdfunding has not taken off in South Africa as it has in more advanced economies.

But ZAR X and Uprise.Africa thinks their deal could be the catalyst needed to kick-start it all.

The World Bank believes the potential market for crowdfunding is significant.

It estimates in its report: Crowdfunding’s Potential for the Developing World that there are up to 344 million households in the developing world able to make small crowdfund investments in community businesses.

“These households have an income of at least $10,000 a year, and at least three months of savings or three months savings in equity holdings. Together, they have the ability to deploy up to $96-billion a year by 2025 in crowdfunding investments,’’ the report noted.

South Africa’s ZAR X Is Not As Small As You Think

ZAR X, one of South Africa’s newest stock exchanges, was granted an operational license in 2016 to operate by the Financial Services Board (FSB). ZAR X commenced operations on Monday, 5 September 2016.

Etienne Nel, ZAR X CEO, says the approval signifies a new era in tech-friendly and user-focused share trading. He said:

“ZAR X creates choice and offers corporate South Africa and the public at large a new opportunity to reduce unnecessary red tape, speed up transaction times and open up equity-based wealth creation to sectors of the South African population that for far too long have been largely excluded from full participation in the financial markets.”

ZAR X listings requirements are largely principles-based, enabling the process of a more flexible and efficient listing. ZAR X will initially offer a primary board for conventional company listings, an investment entities board that will cater for structured products and exchange-traded funds, and a ‘restricted market’ for BBBEE shares, Agri shares and other restricted securities which can only be traded within a clearly defined investor base.

Senwes and Senwesbel were the first companies to list on the Exchange commencing trading on Monday, 3 October 2016.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Optimetriks, the Kenyan sales force automation startup has just defied odds and gone after debt finance. A whole $330,000 debt facility (loan) to grow its customer base and add new features? For a startup that was founded in 2016, this appears a life-saving option. But then, why not fund-raising?

Here Is The Deal

Debt financing came from French commercial banks.

The startup intends to use finance to grow its customer base and add new features.

Optimetriks currently serves more than 25 companies across 16 countries in Africa, with its clients operating in sectors such as beauty, telecommunications, food, and professional services. Last month, it took on EUR300,000 (US$335,000) in debt financing from commercial banks in France to fund its growth, with Langlois-Meurinne saying this will go towards product development.

Why Debt Financing?

Although debt financing is an option for fundraisers, so much remains to be said about the strong terms under which loans are given. Optimetriks does not appear to be desperately resorting to borrowing as the nearest funding alternative to remaining in business, however.

The Kenyan startup has previously received grant funding from the GSMA in 2017 and took part in the Francophone Africa-focused L’Afrique Excelle accelerator program earlier this year and has bootstrapped until now. It could also take on Series A investment soon.

“As our company has matured, and based on our existing traction, we are now considering fundraising in the coming months, to benefit from strategic investors, knowledge of East Africa, and consumer goods distribution,” said Langlois-Meurinne.

Founded in 2016, Optimetriks has developed a sales force automation platform that helps consumer goods companies and distributors digitize their workflows and operations.

“Typical use cases are route management, defining where the sales representatives need to pass, checking on visits and productivity, providing guidance and background information on the retailers they engage with, outlet management, checking on stock levels, and things like that,” said Paul Langlois-Meurinne, the startup’s co-founder and chief executive officer (CEO).

Optimetriks, which makes money from license and service fees, was launched in a bid to solve key problems in African distribution.

“First, the lack of reliable market information and the costs and limitations that exist when trying to collect and analyse data at a large scale,” Langlois-Meurinne said.

“Second, the fact that there are information asymmetries and sometimes misaligned interests between the actors of the ecosystem. Finally, the fact that middlemen take unnecessary margins at the expense of retailers, and distort the value chain.”

The Optimetriks platform aims to bring more transparency and visibility to the distribution space, and help companies better understand how their resources are being employed.

“We help our clients implement scientific distribution that is data-driven, where every action is logged in the system, and can be tracked. Our clients access our platform either through the mobile app for the field users, or the web app, for office users who need to navigate in the reporting dashboards and configure the deployment.,” said Langlois-Meurinne.

“Our ambition is to be the reference platform that connects directly and on a daily basis consumer goods brands with the millions of African retailers that distribute their products on several key dimensions.”

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

No option but to give the glory to them. 700 drivers. R2.3 in personal funding, former South African prison warden and former South African former security guard warden have teamed up to launch Taxi Live Africa — South Africa’s latest in a long string of e-hailing apps — and claim to have invested R2.3-million of their own money in the startup so far. The Durban and Cape Town-based company is South Africa’s latest in a number of the ride-hailing company, following the launch earlier this year of “Sushi King” Kenny Kunene’s Yookoo Ride and Ridver, launched by Opynio Media and Technology, a black woman-owned company (see this story and this one).

Here Are The Details

Former prison warden Luvuyo Ntshayi and Soyiso Qotyiwe, a former security guard turned taxi driver, last month launched the app to residents in Durban.

Ntshayi said the company — which he says he’s spent two years researching and developing — has signed up over 700 drivers in Durban and more than 100 in Cape Town, where the company aims to expand to next (see also this story by our sister site Memeburn).

Luvuyo Ntshayi, former prison warden and Soyiso Qotyiwe, a former security guard, claim they have invested R2.3m in Taxi Live Africa

The ride-hailing startup has initially focused on meter taxi drivers — to help them to compete against e-hailing sector, which was why the company kicked off operations in Durban, where Ntshayi says he received strong demand from local meter taxi drivers for the offering.

But he says this doesn’t mean the app is only for meter taxi drivers. Private drivers from the e-hailing sector are also welcome to use the app.

The company charges drivers a commission of 13%, a rate which Ntshayi says is both fair to drivers and sustainable for his business.

Ntshayi estimates that he and Qotyiwe have together invested R2.3-million in developing the company and the app. He says the amount includes the cost of traveling to Asia where he claims he visited several companies to research the idea of an e-hailing app further. He declined to name the countries and companies he visited.

The company, he says, presently has 14 employees — eight in a Durban office and six in Cape Town. It also has an outside developer team of four.

Ntshayi says in 2008 he joined the correctional services department as a prison warden. In 2012 he completed an HR Diploma before a year’s stint in 2014 as an HR officer at South Africa ‘s Department of Rural Development and Land Reform.

He left his life as a public servant after he secured a R50 000 grant in 2015 from the National Youth Development Agency (NYDA) to set up a detergent manufacturing business in Blue Downs, Cape Town.

However, he says despite help from a mentor, the business never got off the ground. He puts this down to his lack of experience in manufacturing.

Ntshayi — who says he’s had calls from those in neighbouring countries to offer his app’s service there — says however that he’s not focusing on competing with the likes of Uber and Bolt which together dominate the ride-hailing sector.

But he points out that his business’s focus on customer care, including the use of a call centre and a live online chat facility, will help it to gain acceptance in the market.

“We’re not really wanting to be better than anyone from the word goes — we just want to learn,” Ntshayi says.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

{kind=link}