Expected since 2018, law 15–18 on crowdfunding is now operational. This follows the publication of the newly passed law in the country’s Official Bulletin (BO). After the adoption of the new law by the two Chambers of Parliament, its entry into force which takes life from this publication, as specified in article 70 of the law.

Morocco’s Minister of Economy Mohamed Benchaaboun

Here Is What You Need To Know

Presented in March 2018 by the country’s Minister of the Economy and Finance, the new law is part of the efforts of authorities in Morocco to strengthen the financial inclusion of young project leaders and support economic and social development.

The bill was approved by the government council in August 2019, then presented to Parliament in December of the same year.

Three types of crowdfunding are permitted under the new law. These are loan, equity and grant crowdfunding.

The law only regulates crowdfunding portals, and goes ahead to state that to be eligible for license to own any crowdfunding portal, the applicant must:

Have themselves a prevention and risk reduction policy to identify the origin and destination of funds.

Request additional information regarding the relevant funds.

Check the banking prohibitions of the various actors.

All activities related to crowdfunding under the new law will be regulated by Morocco’s central Bank, Bank Al-Maghrib.

Nigeria’s Securities and Exchange Commission recently approved a new crowdfunding regulation. Under the new rules, startups are only allowed to raise a maximum of the following amounts within a 12-month period: i) The maximum amount which may be raised by a Medium enterprise shall not exceed N100Million ($260k); ii. The maximum amount which may be raised by a Small enterprise shall not exceed N70Million ($182); iii. The maximum amount which may be raised by a Micro enterprise shall not exceed N50Million ($130k).

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Startup funds in Egypt are the greatest beneficiary of Central Bank of Egypt’s latest policy which now allows Egyptian commercial banks to commit up to 25% of all credit facilities directed towards small and medium scale businesses in the country into funds targeting startups. According to the central bank, investments made by banks in the funds could reach as high as 70% of the total fund size of each fund in the first year of the investment; 50% in the second year of the investment; and 30% for the third of the investment.

Egypt’s central bank has been at the forefront of promoting investments in financial technology companies and funds targeting startups. Image Credits: Reuters

However, the central bank says all banks investing in the startup’s fund must be allowed to exit from the fourth year. To that effect, it mandates that each of the fund’s bye-laws must include the possibility of the fund allowing the bank to exit starting from the fourth year of the start of the fund’s business. For non-profits, a period of three consecutive years is given for such exit.

For a bank to be able to participate in the scheme, it must obtain the necessary license from the General Authority for Financial Control, responsible for regulating securities and investments in the North African country. A participating bank must also make sure that the total value of its investments into the funds does not exceed 10% of the bank’s principal capital. It must also make sure that its shareholding in the fund does not exceed 50% of the fund or company’s capitalization, unless the fund is part of the bank’s group of companies.

Finally, the central bank has now allowed banks to increase their risk exposure level on the credit facilities given to the startup funds from the previous 0% to a new 20%.

Egypt’s startup ecosystem is not only a major leader in Africa, but also in the Middle East. Source: Magnitt’s MENA Venture Investment Report

The policy is well-timed. The startup ecosystem in Egypt has been booming and has large presence of local funds — Egypt Ventures, Algebra Ventures, etc. — who will, most likely, be the greatest beneficiaries of the fund. The policy will even increase the spate of this funding.

The new policy will, also, now allow banks to float investment funds targeting startups as part of their subsidiaries.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

For regulated fintech startups in Nigeria, there is a very quick way to kill oneself: fail to comply with the regulations of authorities. This is always seen in the barrage of revocation of licenses in recent times. Just before 2020 ended, Central Bank of Nigeria, the country’s apex bank, revoked the operating licenses of 7 fintech companies. This came immediately after it did a similar thing to 42 microfinance banks — a type of banking license usually, also, relied on by most fintech companies in Nigeria. Many reasons were given for that action by the CBN, but the most salient among them is that holders of the affected licenses failed to comply with the obligations imposed upon them by the apex bank according to the relevant laws.

In Nigeria, rules around bank-fintech partnerships are tough. Such fintech-bank partnerships require the approval of Central Bank of Nigeria. Image credit: True News

One such obligation which has more recently been pronounced by the CBN is the requirement of obtaining the bank’s approval before any fintech company in Nigeria can partner with a traditional bank. According to CBN’s circular, PSM/CIR/GEN/CIR/01/22, dated 9th December, 2020, “collaborations between licensed payment companies and other financial institutions in respect of product and services are subject to CBN’s prior approval.”

The direct implication of the above rule is that all classes of fintech companies in Nigeria with payment service licenses are required to seek and obtain CBN’s license first before partnering on any products or services offered by either.

There aren’t many fintech-bank partnerships in Nigeria yet, however one such partership is that between Kuda, Nigeria’s only digital bank and GT Bank and Zenith Bank. Under the partnership arrangement with the two banks, Kuda users can make over-the-counter deposits in these traditional institutions to fund their app-based accounts. There is also an existing partnership between Kuda and Access Bank, which allows its customers withdraw cash from Access Bank’s ATMs for free. Another example is Nigeria’s Piggyvest, a savings and wealth management platform, which partners with Wema Bank to create direct deposit account numbers for the fintech’s users. Now, under the CBN partnership regime, a prior CBN’s regulatory approval would be needed before the fintech companies above and the respective traditional banks could partner on any projects.

The partnership rule particularly looks harmful for fintech startups used to innovation and agility. Thus, it could be argued that if the rule had applied to wealth management startups such as PiggyVest, it would have been harder for them to migrate their existing customers from Providus Bank to Wema Bank within 24 hours (like they did) following the recent Central Bank of Nigeria’s directive to all banks in Nigeria to block all cryptocurrency trading accounts resident in Nigerian banks.

This rule could not apply to PiggyVest because it specifically applies to all “payment companies”, unless PiggyVest had previously procured approval from Wema Bank and had to simply switch over. If the rule had applied (as it would have if it were Paystack, Flutterwave or Interswitch), the startup’s agility with the migration to Wema Bank would have been hard to come by.

Although CBN’s rule on partnership may be of industry standards or may have been well intended, it substantially affects how fintech companies in Nigeria respond to new threats and opportunities. In Singapore, even though partnerships between banks and fintechs are subject to regulatory approval, if the arrangement relates to the provision of a banking business, or other business the conduct of which is regulated by the Monetary Authority of Singapore; or a business which is incidental to any of these; then there is no need for such approval.

Below is how bank-fintech partnerships are treated in other countries in Africa and in top global fintech destinations.

S/N

COUNTRIES

HOW FINTECH-BANK PARTNERSHIPS ARE TREATED UNDER COUNTRY LAWS

CURRENT PRACTICE

1

South Africa

South Africa’s Banks Act requires approval to be sought from the South African Reserve Bank (SARB) for contractual arrangements between a bank and a non-bank entity, where the parties undertake an economic activity that is subject to their joint control.

Although approval is required by most banks, fintechs do not encounter most challenges, partnering with local banks.

Article 96 of the Egyptian Banking Law, No. 194 of 2020 now requires outsourced service providers to be registered by licensed Egyptian banks. Generally, approval for partnership is required.

Fawry recently obtained approval to partner with an Egyptian bank. Partnerships moderately common.

Fintech-bank partnerships are established after fulfilling the requirements of local state laws. More specifically, under the Bank Service Company Act (BSCA), federal banking agencies have broadened their authority to control and investigate third-party service providers. In addition, the Federal Financial Institutions Examination Council’s (FFIEC) has released guidelines on financial regulators’ authority to investigate such technology service providers to banks. The Consumer Financial Protection Bureau (CFPB) has similar inspection and regulatory jurisdiction over financial institution service providers, including FinTech companies that offer services to those institutions.

Partnerships between FinTech entities and financial services providers have become common in the US

5

Singapore

Singapore’s apex bank, Monetary Authority of Singapore, generally requires approval for such partnerships, unless the arrangement is for the provision of a banking business, other business the conduct of which is regulated by the MAS, or a business which is incidental to any of these.

Partnerships or other arrangements with traditional financial services providers are common in Singapore

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

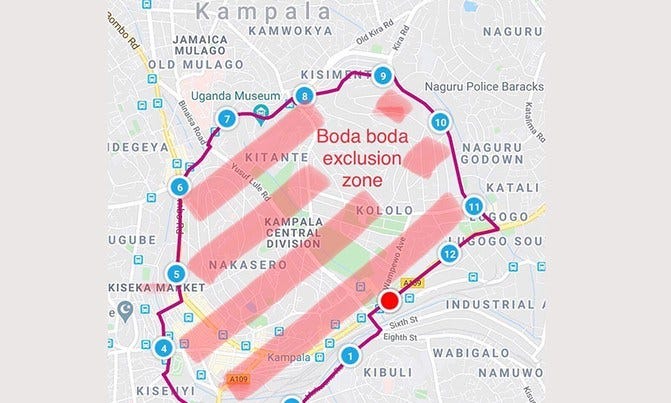

Uganda’s capital, Kampala, is no longer going ahead with its proposed plans to remove boda bodas from the city’s center. Daniel Nuwabiine, Kampala Capital City Authority (KCCA) spokesperson has come forward to say that although the plan was necessary, it was hastily concluded without consultation with the relevant stakeholders. Consequently, the plans would be returning to the shelf for now.

Daniel Nuwabiine, Kampala Capital City Authority (KCCA) spokesperson

“Engagements are ongoing. The major focus is on how we can achieve a sustainable transport system for the city without looking at only boda bodas but also other commercial vehicles in the city. We expect to have a comprehensive plan soon which will be unveiled to the public before its implementation starts,” Nuwabiine said in an interview.

“We have not abandoned the boda boda free zone corridor but it will only be implemented after we have come up with a comprehensive transport system for the entire city which is currently being worked on,” he added.

Ugandan bike-hailing startup Safeboda would have been worst hit by the proposed restrictions by KCCA. Image credits: Safeboda

In any case, it appears the city may even abandon the plans entirely, as Nuwabiine also mentioned that the government is currently considering partnering with private companies to procure buses, claiming that shuttles can transport more passengers than boda bodas.

“One of the mistakes government does is to come up with some plans or policies for the transport sector without first engaging those who are directly involved in the transport business because we understand it more than any other person and we can actually give government information that they want regarding the boda boda industry,” the chairperson of the Kampala Bodaboda Association, Mr Kiviri Kanyike, said.

Attempting To Regulate Bike-Hailing In Kampala

In exactly the same fashion, the city of Kampala, Uganda’s capital, which is home to about 1.5 million people, last year attempted to do what Nigeria’s most populous city — Lagos — did to its famously known okadas back in February this year — the city’s government banned them from operating on its highways.

A widespread agitation against the directive banning commercial cyclists from accessing the Kampala city center and surrounding places, however, led to the suspension of the proposed ban.

“In light of the presentations, KCCA in consultation with other key government agencies has come up with a roadmap that will facilitate operation of the digital companies as well as streamlining public transport. The roadmap entails a validation exercise for digital companies and make recommendations to each for the city to achieve a harmonized transport system,” the directive read in part.

“Cabinet approved Boda Boda Free Zone where All Boda Bodas are prohibited from entering/accessing,” it further read.

Uganda ‘s Cabinet approved boda boda Free Zone where all bike-hailing services or boda bodas are prohibited from accessing.

All moves came after the Ugandan government, earlier in May this year, through the State Minister for Kampala, Kampala Lord Mayor Erias Lukwago, Kampala Capital City Authority (KCCA) and the Ministry of Works and Transport, issued unimplemented guidelines expressing its intentions to force all traditional commercial motorcyclists (locally more known as “boda boda”) to go digital or cease to exist. Mr Nuwabiine revealed that KCCA has since halted all the processes, pending a final resolution that will be made by stakeholders.

Kampala is Uganda’s largest city, population-wise (1.5 million), and by far ahead of cities like Gulu, Entebbe, Lira, Mbarara or Nansana which have a combination of not up to 1,000,000 people. (Note: only about 18 million Ugandans, representing about 40.1% of the population have access to the internet.)

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Nigerian central bank has issued a statement stating that it would gift N5 for every $1 remittance sent to Nigeria. The bank said the policy is part of efforts aimed at encouraging increase in inflows of diaspora remittances into the west African country. The policy tagged “CBN Naira 4 Dollar Scheme”, targets senders and recipients of international money transfers. The scheme which takes effect from Monday 8th March, 2021, will end on Saturday 8th of May, 2021.

“Accordingly, all recipients of diaspora remittances through CBN licensed IMTOs shall henceforth be paid N5 for every USD1 received as remittance inflow,” the bank said.

“In light of this, the CBN shall, through commercial banks, pay to remittance recipients the incentive of N5 for every USD1 remitted by sender and collected by designated beneficiary. This incentive is to be paid to recipients whether they choose to collect the USD as cash across the counter in a bank or transfer same into their domiciliary account. In effect, a typical recipient of diaspora remittances will, at the point of collection, receive not only the USD sent from abroad, but also the additional N5 per USD received,” the bank further stated.

CBN’s latest step comes on the heels of its recent order to Mobile Money Operators and Payment Switch providers to suspend the receiving of remittances or the integrating of their systems with International Money Transfer Operators (IMTOs).

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Somalia is one of Africa’s poorest countries by World Bank standards, with GDP per capita of about $500, but there are some ways it is better than the rest of Africa. Apart from having the cheapest mobile data rate in Africa (US$0.50 for one gigabytes; or just ₦190 if you’re in Nigeria), the east African country has gone ahead to issue its first ever mobile money license to a private company, even ahead of its neighbour Ethiopia, which is seven times bigger than it in population.

However, granting the mobile money license does not mean that mobile money operations have not been going on in the country. For every month in the year 2018, the country recorded approximately 155 million mobile money transactions, worth $2.7 billion. Similar transactions have also been going on in the country for the past 10 years.

What the Central Bank of Somalia had merely done was to issue the country’s first ever money license to an entity, thereby ending the era of unregulated mobile money services in the country.

The license went to Hormuud Telecom, the country’s largest telecommunications provider, which runs the Electronic Voucher Card (EVCPlus) free mobile money service.

Mobile Money statistics in 2019 for sub-Saharan Africa. Source: GSMA

CBS’ license to Hormuud Telecom is a major achievement for the telecom company as it helps it to partially heave some sighs of relief from the country’s crowded telecoms market, currently made up of 11 licensed local operators.

Although Hormuud’s new license may not make much difference as there are already numerous unregulated services in operations, it may however help the telco to position itself early for post-regulation market share.

According to the World Bank 2017 report, mobile money service in Somalia has reached a penetration rate of 73% (83% in urban areas), compared to a penetration rate of 15% for formal bank accounts. Somalia’s Dahabshiil is one of the largest money transfer companies in Africa, operating in 155 countries.

Majority of Somalian households (58%) make one to four transactions each month and tend to use mobile money over cash for purchases between US$2 and $300. A mobile money account must be linked to a bank account for transactions over $300. As a result, digital money is an excellent cash replacement, and it can be used for everyday transactions such as bill payments, paycheck receipts, and merchant transactions. Nevertheless, a study by Hormuud Telecom revealed that cash-out rates on mobile money platforms in Somalia are less than 5%, indicating a greater number desires to keep money in mobile wallets rather than cash it out.

In contrast to Kenya’s well-known Mpesa mobile money transfer service, Somalia’s transactions are mostly in US dollars. Though mobile money providers are mobile network operators, they are increasingly becoming part of large conglomerates that also provide banking and money transfer services, as in Kenya.

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Algerian government has launched a startup accelerator, “Algeria Venture”, barely five months after launching its first ever fund for startups. Located at the Parc des Grands Vents (Dounia Parc) in Algiers, the startup accelerator will be “the showcase” of innovative Algerian projects on the international scene, according to the country’s Minister Delegate for the Knowledge Economy and Startups, Yacine El-Mahdi Oualid.

Dounia Parc will be a major gamechanger in Algeria’s quest to alter its startup ecosystem. Image credits: Dounia Parc

Here Is What You Need To Know

The new accelerator Mr. Oualid said, will operate according to the same management model as international accelerators. The accelerator will also be part of a network that will be woven across Algeria with other projects of the kind that are in progress in the East, West and South of Algeria.

Algeria Venture will also introduce, according to him, the concept of “Open Innovation” which will allow Algerian and foreign companies to “outsource” their innovation projects by taking advantage of products and services developed by startups in the area of interest to them.

The site for the new accelerator inaugurated in the capital Algiers can accommodate up to 30 startups for a period ranging from six to 12 months, said the minister, adding that calls for demonstrations will be “periodically” launched in order to select projects having strong growth potential and which would be “interesting” to integrate into the accelerator.

Mr. Oualid also said a little more than 300 companies between startups and innovative projects have been labeled, of which around ten startups have benefited from funding from the Algeria Startup Fund (ASF). He however highlighted the “accessibility” of the ASF which, in addition to receiving applications from project leaders who request funding, contacts startups to offer them funding.

A Country Greatly Supporting Startups In Recent Times

In December 2020, Algerie Telecom, Algeria’s state-owned telecom operator, unveiled new specifications for its calls for tenders. The new specifications would facilitate access of over 2,300 technological microenterprises to public procurement.

This followed the launch of the Algeria Startup Fund in October the same year. The launch was inspired by the statement of the President of the Republic, who during the meeting of the Council of Ministers held in January 2020, ordered the development of an emergency program for startups and small and medium-sized enterprises (SMEs), in particular the creation of a special fund or a bank intended for their financing. Following that, Executive Decree 20–254 of September 15, 2020 creating the national committee for the labeling of “startups”, “innovative projects” and “incubators” was published in the last issue of the Official Journal, Tunisia’s national gazette.

Labelled startups and incubators in Algeria have also been the greatest beneficiaries of the country’s newly passed finance law. The 2021 Finance Act provides for changes in taxes (Tax On Professional Activities, TAP; and Value-added Tax VAT). Under the law, companies in Algeria with a startup label will be exempt from several taxes, starting with the TAP (tax on professional activity) and the IBS (tax on corporate profits. companies) for a period of 2 years from the date of obtaining the said label.

Algeria Venture

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Ghana seems to be countering all recent controversial policies made by its west African neighbour, Nigeria. After giving a badge of approval on blockchain companies, and introducing a more progressive approach towards regulating crowdfunding, the bank has now rolled out a new policy on dormant accounts, aimed at protecting abandoned funds at Ghanaian banks. According to the bank, any account at a Ghanaian bank with no customer activity for a period of two years is a dormant account — three years for a fixed deposit account. After the respective periods of time, banks are then mandated to transfer all the dormant accounts to a register of dormant accounts to be kept by the banks.

Governor, bank of Ghana, Dr Ernest Addison

“An account transferred to the register of dormant account shall not attract any service charge or account related fees. Interest bearing accounts transferred to the dormant account register shall also cease to accrue any interest,” the bank said in the new rules.

What Is Interesting About The New Policy?

One interesting arm of the new rules is that Bank of Ghana has instructed banks in Ghana to take adequate steps to contact an account holder at least three (3) months before the account becomes dormant. Those to be contacted include “ Next of Kin” of the customers.

Again, banks are mandated to publish in national newspapers, including digital print media, a list of all the accounts that have been on the register of dormant accounts for three years.

Where the account holder still fails to claim the funds in the dormant account, banks are then requested to transfer the dormant funds to Bank of Ghana. However, the funds can still be claimed back by the account holders or beneficiaries from the Bank of Ghana even after they have been lodged with the apex bank.

In any case, for all the time during which account remains dormant, Bank of Ghana says the funds in them are still covered by the Ghana Deposit Protection Scheme, a form of insurance protecting customers’ funds at licensed banks in Ghana.

Nigeria Borrows From Dormant and Unclaimed Dividends Accounts

Bank of Ghana’s latest move comes on the heels of Nigeria’s Finance Act 2020, which allows Nigeria’s federal government, through its Debt Management Office (DMO), to move all such funds to a trust to be run by the office. Government can then borrow from the trust.

“If you have bank balances and unclaimed dividends that are not six years and above, this has no implication on you.

“If you have unclaimed dividends in a company, that is not a public limited one listed on the Nigerian Stock Exchange, you have no issue. If you do, you can start the process of taking back your unclaimed dividends and if it is a bank balance, go and get your bank balances.

“All these will be done in consultation with the bankers’ committee, CBN and the banks for the unclaimed bank balances and unclaimed dividends, registrars, Securities and Exchange Commission, other regulatory bodies,” said Bode Oyetunde, Senior Special Assistant to Nigerian President on Finance and Fiscal Matters and Secretary of the committee.

The total amount of the unclaimed funds at Nigerian banks and custodians has been put at more than 180 billion naira ($472 million).

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Bank of Ghana dormant accounts Bank of Ghana dormant accounts

In Kenya, rider-hailing drivers are excited. The same in South Africa. But not in the same way. In South Africa, the lines of litigant drivers are gaining distance, stretching out their elasticity. There, two law firms have inhaled some inspiration from the recent judgment of the highest court of the United Kingdom, sitting at Parliament Square, against Uber. The judgment is simple in summary: if you control drivers, they are your subordinates; and if they are your subordinates, they are your workers, not independent contractors, not any other jargons.

Uber

But even the two law firms in South Africa are different. One, Leigh Day, the renowned law firm that triggered Uber’s ordeals in UK courts — with offices in Birmingham, Chesterfield, Liverpool, London, Manchester, Newcastle — wants to migrate to South Africa, by way of assistance— allowed to do so as long as its lawyers are licensed in South Africa. The other, Mbuyisa Moleele Attorneys, based in Johannesburg’s capital and famous for the gold miners’ case, wants to lead the protest from home. The common agenda has since been set: to reclassify all South African Uber drivers as workers and not independent contractors. Therefore, they are headed for the Johannesburg Labour Court, in a class action suit.

“South African legislation relating to employment status and rights — the Labour Relations Act and the Basic Conditions of Employment Act — is very similar to UK employment law,” the two firms said in a joint statement.

“Furthermore, Uber operates a similar system in South Africa, with drivers using an app, which the UK Supreme Court concluded resulted in drivers’ work being ‘tightly defined and controlled’ by Uber,” they added.

But then, it is still a long journey from here…

Between South Africa and Kenya, there is remarkable difference on how the battle is being fought. In Kenya, it is the country’s minister of Labour and Social Protection, Simon Chelugui, who is drawing out the dagger. This week Tuesday, the issue became so overpowering that he had to call a meeting. The drivers, mostly of Uber, were bearing banners; the stage was set. But what came next was neither a rude shock nor a big relief: just some form of speaking from both sides of the mouth.

“The ruling in London on Friday, does not apply to our jurisdiction,”Chelugui said, glancing over the drivers. “We can only reference, it can only persuade us, but we cannot act on it as a country.”

And then creepily, aiming towards the rapid surge in ride-hailing apps in Kenya, he sought a balance in his statements.

“The labor laws on internet based services have not been properly developed,” he said, “and we will need an engagement as a ministry to develop regulations and guidelines on how to run such an economy.”

And that was the end, but the beginning of a new chapter.

If Drivers Kill Ride-Hailing Apps, What Would Be Left For Them?

In South Africa, Uber has been quick to issue a rather lengthy statement initiating this discussion.

“At a time when we need more jobs, not fewer, we believe Uber and other platforms can be a bridge to a sustainable economic recovery. Uber has already produced thousands of sustainable economic opportunities,” the statement reads in part.

By October 2019, there were already 13,000 active drivers in South Africa and each of them had completed 38775 trips since Uber set its foot in the country in 2013. In Kenya, the number is 12,000 drivers as at November, 2020. In Nigeria, it is 9000 as at 2018. In Egypt, 200,000 as at 2020, since it was launched in Cairo in 2014.

Now, torn between these metrics and a fair life, the drivers have found themselves floundering in a deep blue sea of choosing to quit or to stay while responding to perpetual rounds of ride-hailing requests mindlessly.

“I am suffering but those who are suffering the most are those who depend on earning a living as a ride-hailing driver using a car purchased on installments,” Hani Al-Sawi, an Egyptian Uber driver, who was working with his own private car told Ahramonline last year.

“Their revenue cannot cover operating costs, due installments, and their need for a livelihood, and so they have sold their cars to pay the installments and are now looking for another job,” added Abdel-Aziz, another Uber driver.

Last year November, Tony West, Uber’s senior vice-president, said as one of Uber’s top 10 markets globally, Egypt is “one of the most important markets for the US-based ride-sharing company in the Middle East.” His statement is evident in the $3.1bn acquisition of Careem, Uber’s Middle Eastern rival in the ride-hailing business.

Across the sea to Kenya, the stories are the same for drivers. Starting from 2016 through 2017, 2018, 2019, 2020 and now 2021, it has been endless strikes and protests for all digital taxi drivers.

“The fare prices keep on reducing because of the competition with other apps,” Denis, an Uber driver was quoted as saying during the 2018 protest. “ In the long run, it is us, the partners and drivers, who are losing. We are being oppressed,”

Paul Oyer, Stanford Graduate School of Business professor, who has written extensively about the gig economy, believes this.

“It doesn’t make a lot of sense to go out and invest a lot of money in a car for the sake of driving it for Uber — there isn’t enough money to be made for your time and the costs of car ownership,” he said.

Comparing Africa‘s attempt to regulate Uber, other ride-hailing companies with the rest of the world. Source: — Daily Mail

Redesigning A Model Free From Excessive Control

One thing is certain from all these: the days of excessive controls over drivers by digital ride-hailing companies are numbered, not with the mounting tides of pressure from drivers’ unions.

Therefore, at this stage, one particular element that the entire gig economy, especially the ride-hailing apps should consider while building their products, to run away from this precedent set by the UK’s supreme court is the element of control.

S/N

Types of Control

Conclusions by the UK Supreme Court in Landmark Case, Uber BV and others (Appellants) v Aslam and others (Respondents)

1

Can drivers determine their remuneration, in any way?

No

2

Are contractual terms of engagement with drivers negotiable?

No

3

Do drivers have absolute control over acceptance or cancellation of trip requests?

No

4

Do drivers have a choice of vehicle types, routes they follow?

No

5

Are ratings on drivers by customers used to whip drivers into performance?

Yes

6

Do drivers have any say in communications with riders, regarding pay, complaints, contact details, etc?

No

The element of control in digital ride-hailing services has become so important that it cannot be continued to be ignored. “The greater the extent of such control, the stronger the case for classifying the individual as a “worker” who is employed under a “worker’s contract”.”— the court in the case above stated.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Uber drivers kenya Africa Uk Uber drivers kenya Africa Uk Uber drivers kenya Africa Uk

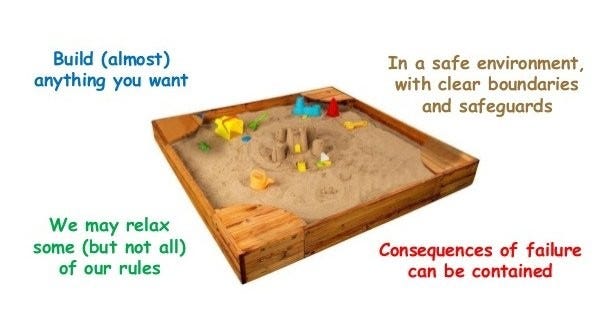

Bank of Ghana is not toeing the path of Nigeria’s central bank. Although both banks have been keeping up with the explosion in innovations, the former is taking on a more progressive approach. To that effect, the highest bank in Ghana has done the unforeseen: encouraging previously unregulated financial technology companies, especially blockchain, remittance and crowdfunding products and services, to come forward and be issued licenses under a new regulatory and innovation sandbox pilot, which it is spearheading in collaboration with EMTECH Service LLC.

Governor of the Bank of Ghana, Dr. Ernest Addison

“This is in line with its commitment to evolve an enabling and inclusive regulatory environment that promotes FinTechs and supports innovation,” the bank said.

“Within the financial sector, a regulatory and innovation sandbox is a supportive and controlled policy environment that enables firms to test innovative products, services and business models under the supervision of a regulator. Effectively, the regulatory and innovation sandbox will provide a forum for financial sector innovators to interact with the sector regulator to test digital financial service innovations while evolving enabling regulatory environment,” it noted.

Who Can Apply For The License?

The new licensing regime will be available to:

To banks, specialised deposit-taking institutions and payment service providers including dedicated electronic money issuers.

Unregulated entities and persons that have innovations that meet the sandbox requirements.

However, the entities above still need to show that:

Their digital business models are new and are not currently covered explicitly or implicitly under any regulation in Ghana.

Their digital financial service technology is still new and immature; and

Their Innovative digital financial services products have the potential of to address a persistent financial inclusion challenge.

“Within the broad categories outlined, the Bank of Ghana would give preference to products and services leveraging blockchain technology, remittance products, crowdfunding products and services, e-KYC (electronic know your customer) platforms, RegTech (regulatory technology), SupTech (supervisory technology), digital banking, products and services targeting women financial inclusion and innovative merchant payment solutions for micro, small and medium size enterprises (MSMEs),” the bank said.

In simple terms, this is how a regulatory sandbox works. Image Credits: LinkedIn

What Is The Purpose Of The Regulatory Sandbox Regime?

With the new regulatory sandbox license, Bank of Ghana seeks to:

Reduce time-to-market for unregulated products;

Allow regulators to learn about innovations faster;

Encourage innovators to formalize their business and incentivise incumbents to experiment with new ideas;

Reduce the cost of innovation for innovators; and

Provide valuable insight for regulators to evolve effective regulations.

We are honored to be a trusted partner for the pretigious @thebankofghana. This is a ground breaking project showcasing how central banks can deploy modern technology to keep up with, assess and accelerate innovation! #ghana#sandboxhttps://t.co/e7WR59tSq8

Bank of Ghana’s latest move comes on the heels of the recent blocks placed by Nigeria’s central bank on cryptocurrency trading and the facilitation of international remittances by startup companies. Apart from Mauritius and Nigeria, Tunisia is has more recently launched a regulatory sandbox regime.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer