The Nairobi Securities Exchange has been granted approval by the markets regulator to launch the Unquoted Securities Platform (USP), an Over the counter (OTC) platform that offers unlisted companies access to long term funding through private placements. The platform will allow trading, clearing, and settlement of securities of unquoted companies. The exchange says the Unquoted Securities Platform will allow unquoted companies with a register of shareholders to enjoy price discovery and boost their stocks’ liquidity. Further, it will enable investors to view their stocks’ prices, which will be published daily. Investors will also access over the counter trading for securities of unlisted companies.

CEO of Nairobi Stock Exchange (NSE) Geoffrey Odundo

The CEO of Nairobi Stock Exchange (NSE) Geoffrey Odundo says the launch is part of the bourse’s strategic plan, including connecting capital with opportunities. “The launch offers unlisted firms an opportunity to raise capital, expand and list on the respective segments at the Exchange.”

Investors interested in trading via the Unquoted Securities Platform will open and maintain a USP trading account and buy and sell USP securities via a USP securities dealer. The launch of the Unquoted Securities Platform is part of the exchange’s efforts to woo companies to the NSE. The platform offers a saving grace for companies yet to meet listing requirements to access funds. The launch follows other efforts to rope in companies, such as the Ibuka Programme, which seeks to attract SMEs to list on the bourse. Meanwhile, the Capital Markets Authority is reviewing existing listing laws, which will be ready by June 2021.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Small businesses have been Bring Your Own Device pioneers since before BYOD became an acronym. Without large IT departments or equipment budgets, small business staff naturally use their own computers and smartphones to work when and where they need to. Sometimes there’s a formal mobility strategy, but just as often small businesses embrace BYOD organically, adding devices as they pop up.

At the same time, small businesses often look the other way when it comes to questions of security and managing BYOD access to their applications and networks. But avoiding mobile device management (MDM) is not necessarily the best approach. Taking responsibility for other people’s smartphones seems like a tall — and expensive — order, but it’s not: There are MDM solutions for small businesses that increase BYOD smartphone security without breaking the bank.

Today’s smartphones are pretty secure to begin with. Smartphone manufacturers got to watch the entire PC revolution and learned from the mistakes of those who came before. A major goal of MDM tools is simply to keep those smartphones secure, mostly by trying to override the weakest link in most security: the end user.

Small businesses can start by taking advantage of MDM features that automatically apply software updates, establish safe password and lock settings, and restrict application store choices to trusted stores. Enforcing some basic security settings doesn’t take a lot of configuration or control, and can give a huge boost in security. Just as importantly, it’s unlikely to be a cause for conflict. People want to do the right thing and when they make poor security choices, it’s usually out of ignorance or expedience rather than malice.

With basic MDM, for example, software updates can be applied soon after they’re released, which dramatically reduces the security risk from a smartphone. End users who don’t know how to install updates aren’t a problem anymore: MDM policies take over and ensure that devices are running the latest software releases. MDM tools can also provide status information on each device, so if something is wrong and software isn’t being updated, the IT manager can see this and make a visit to resolve the issue.

Mobile device management for beginners

Security isn’t the only reason for small businesses to adopt MDM — another is time savings. MDM enables email, Wi-Fi and virtual private network (VPN) configurations to automatically update on enrolled smartphones, reducing aggravation and confusion for BYOD users. As the small business networking, email and security environment changes, MDM tools make it easy to get those configuration changes pushed to devices. The end result is a happier user community, and fewer panicked phone calls if someone didn’t get the memo on a configuration change.

Choosing MDM solutions for small business

Small businesses interested in MDM should be thinking along the lines of four major criteria: price, features, management model, and platform support.

Price

Small businesses are rightly budget conscious, and the good news is that basic MDM definitely won’t be expensive. Most products are priced per user per month, and IT managers can easily find excellent choices for about $1-$2/user/month. Some products offer a “lite” version for free to get you started. Others bundle lite MDM with other products, so if you’re already buying an existing product (such as Microsoft Office 365), you may be able to activate a minimal MDM at no additional charge.

Generally, the larger the feature set, the higher the price, but even high-end MDM aimed at small business comes with a reasonable price tag and delivers a lot of value for pennies a day.

Features

It’s not necessarily true that a longer feature list is better than a shorter one, so IT managers should focus on the settings they’ll actually use. A dozen settings might be all that’s needed, along with reporting and lost device controls, to find the perfect MDM solution.

Small businesses should focus on features in four key areas: security (including lost device features such as remote wipe and remote lock); software and application controls (including patching and update settings); configuration push for email, networking and VPN; and simple reporting on device status and inventory.

Management model

Small business IT managers should start with cloud-delivered MDM solutions. It doesn’t matter how lightweight or simple an on-premise solution is — there’s virtually nothing a small business gains from running the MDM solution on their own servers.

The only exception to this is if Active Directory (AD) integration is a critical part of BYOD — which it rarely is for small businesses. However, if AD integration is really needed, then it’s usually easier to integrate an on-premises solution than try and link your AD to a cloud-based service.

Platform support

It almost goes without saying that whatever MDM you choose should support your users’ devices, but there are some constraints. All the common products work well for the two main smartphone operating systems: Android and iOS. However, small businesses that have Windows phones or BlackBerry devices will find a more limited selection — and higher prices. It’s not usually a big deal, but taking a survey of what smartphones people are actually using before picking an MDM solution is a good idea to avoid showstoppers later on.

Another platform issue to research is enrollment: how the MDM tool gets its client downloaded to the user’s smartphone. Many products have a variety of techniques that allow remote and self-service enrollment. IT managers responsible for highly mobile employees should make sure that getting smartphones connected to the MDM solution won’t be a burden or logistical foxhunt.

Cloud-based MDM solutions let small business IT managers gain big-business security for mobile devices without unwelcome complexity or high costs. Spend a little time now, and save a lot of time later by gaining better control of, and delivering better support for, smartphones and tablets.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Startups in Morocco now have a central portal that will enable them benefit from a range of subsidies, guarantees, financing, tax advantages and customs procedures. Called the national entrepreneurship support portal (Al Moukawala), the portal is a “one-stop-shop” bringing together all of the public effort in the area of entrepreneurship and aimed at project leaders, very small businesses, SMEs, startups, cooperatives, farmers, individuals, auto-entrepreneurs and clusters. The portal was unveiled during a ceremony organized on December 17, 2020 by the country’s Ministry of the Economy, Finance and Administrative Reform. — Department of the Treasury and External Finances.

This project, designed in partnership with GIZ (German cooperation) and various stakeholders in the entrepreneurship sector, centralizes information on public support instruments and offers dedicated to entrepreneurs.

Based on the observation that around a hundred ways of supporting entrepreneurship remain unknown to project leaders, this platform would therefore aim to strengthen access to information and promote communication in the different regions of Morocco between project leaders and other stakeholders in the entrepreneurial ecosystem.

The offers presented by this portal include subsidies, guarantees, financing, tax advantages and customs procedures. Likewise, the search engine offered by this tool allows each category of entrepreneurs to access offers corresponding to their profile, life cycle and their needs.

This platform has specific features designed as a compass for entrepreneurs and project leaders in order to guide them towards support solutions suited to their ambitions.

Other objectives are also assigned to this platform such as the production of statistics, surveys and studies on the sector, support for new initiatives, and capacity building of entrepreneurs. In addition, there is the annual collection of instruments to support entrepreneurship, which supplements the content of the existing offer on this site.

In addition, a digital application (Al Moukawala) for viewing instant offers has been set up with a range of 90 project support measures. It can be downloaded from the App Store or Google Play.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Algeria has a new decree for startup and it is not making wave, but the first wave of innovative projects, startups and incubators, benefiting from labeling issued by a multisectoral commission set up under the decree, is scheduled for the end of December-beginning of January, said Tuesday in Algiers, the Minister Delegate to the Prime Minister responsible for Knowledge economy and startups, Oualid El-Mahdi Yacine.

Oualid El-Mahdi Yacine

On the occasion of the installation of the Commission for the labeling of “Startups”, “Incubators” and “Innovative projects”, the minister considered that “the timing (of the start of labeling) is rather correct” since it will coincide with the implementation of the 2021 finance law which introduces “new tax exemptions for startups.”

Labeling will thus allow the startup to benefit from these exemptions.

The minister announced that this commission will meet periodically “on average twice a month” and will allow to study the requests which will be received “exclusively” on the portal www.startup.dz which was also launched Tuesday.

The choice of all digital in the administrative procedures for obtaining the label is motivated, according to the minister, by his determination to put an end to the “bureaucracy which has taken root in our administrations” and which is “the major obstacle which has hindered the completion of hundreds of projects “.

Obtaining the “Startup” label is conditioned by two essential factors: innovation and non-linear growth, explains Noureddine Ouaddah, an executive at the ministry.

While the granting of the “Innovative Project” label will depend essentially on “the growth of the project and its business plan”, adds. Mr. Ouaddah.

Finally, the “Incubator” label requires the presentation of services such as coaching and training, a good qualification of the team as well as convincing results as to the outcome of the projects monitored, continues the executive.

Algeria Officially Launches Its First Ever Fund For Startups

In October this year, Algeria launched the country’s first ever Fund for Startups, at the International Conference Center (CIC) in Algiers during the National StartUp Conference “Algeria Disrupt 2020”.

According to the country’s Minister Delegate to the Prime Minister in charge of the knowledge economy and start-ups, Oualid El-Mahdi Yacine, the new financing mechanism, called the “Algerian start-up fund”, is based on investment in capital and not on classic financing mechanisms based on credit”, stating that investment in capital induces a notion of risk and this is a very important.”

Executive Decree 20–254 of September 15, 2020 creating the national committee for the labeling of “startups”, “innovative projects” and “incubators” was published in the last issue of the Official Journal.

During the meeting of the Council of Ministers held in January 2020, the President of the Republic ordered the development of an emergency program for startups and small and medium-sized enterprises (SMEs), in particular the creation of a special fund or a bank intended for their financing.

He also insisted on the imperative of a “deep reform” of the country’s tax system with all that follows in terms of regulations and tax incentives for the benefit of startups and SMEs.

The 2020 Finance Law provides for new measures in the form of tax incentives for the benefit of startups, in particular those who are active in the field of innovation and new technologies.

These are tax exemptions concerning taxes on profits and on value added (VAT) in order to guarantee the sustainability of these businesses and to achieve sustainable economic development in the medium term.

Customs exemptions during the operation phase and facilitated access to land as part of the extension of investment projects have also been instituted under the 2020 Finance Law.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

A stakeholders’ meeting had come to an end on Friday December 11, 2020 at Kenya’s Energy and Petroleum Regulatory Authority (EPRA)’s office in Nairobi, and all parties have known each other’s positions. But the bottom line now is that a new set of rules, Energy (Solar Photovoltaic Systems) Regulations, 2020, would be enacted after all. In a sweeping move, the Energy and Petroleum Regulatory Authority (EPRA) intends, through the proposed regulation, to regulate the solar energy sector in Kenya, a move seen to try and protect Kenya Power from competition, as revenues continue to fall despite the company enjoying monopoly. Many stakeholders have also described the move as an attempt by EPRA “to police the sun”.

Epra Principal Renewable Energy Officer Caroline Kimathi,

“We are not here to protect Kenya Power. We are licensing people who are going to install the solar panel. If the stakeholders call for a reduction of the fees to be paid then we are going to adopt that, but in no way is this going to shield Kenya Power,” said Epra Principal Renewable Energy Officer Caroline Kimathi, at the meeting.

What Do The Proposed New Rules State?

The rules are launching a strict licensing regime for the solar energy sector in Kenya. For instance, the rules state that a person shall not engage in the importation, manufacture, sale or installation of solar PV systems or solar PV system components without a valid license issued by EPRA.

The rules further go ahead to empower the Authority to from, from time to time, determine by publication of a notice, the types of solar PV components and solar PV systems to which the regulation applies. But as a general rule, all the products must also conform to the Kenya Standard.

“A manufacturer or importer of solar PV systems, components, and consumer devices shall ensure that the products conform to the relevant Kenya Standard set out in the Seventh Schedule or any other subsequent or applicable Kenyan Standards,” the regulations read in part.

Apart from the above, solar energy companies in the country must also first register all consumer devices with the authority. The implication of this is that manufacturers or importers of solar PV consumer devices shall have their products registered by the authority on meeting the requirements of relevant Kenya Standard or other equivalent international programmes for such products. EPRA will also determine which products are allowed into the Kenyan market, by the rules.

High Licensing Fees And Increase In Cost Of Doing Business For Solar Energy Companies

If the rules sail through at the end of the day in parliament, it may spell doom for existing and yet-to-exist solar energy companies as the cost of doing business will most certainly increase.

For instance, under the rules, a solar technician is required to pay between Sh2,250 and Sh6,000 ($20 to $54k) to obtain and renew a license.

Similarly, a contractor will pay between Sh3,000 ($27k) and Sh6,000 ($53k) for a licence, which will be valid for three years, with practitioners required to apply for renewal one month before the expiry.

Both technicians and contractors will also be required to obtain insurance policies for their licences of between Sh1 million and Sh10 million ($9000 to $90,000), based on their respective licence categories.

A fine of Sh50,000 ($450), per day, will be imposed on anyone practicing with an expired licence.

The stringent proposed regulation also includes a Sh10,000 ($90) fine if individuals delay renewing their license and Sh20,000 ($180) if they do not issue a completion certificate for a project or warranty for installation.

Additionally, penalties on failure to provide data to EPRA or providing false data will range between Sh5,000 and Sh1 million.

Licenses are based on the capacity of the system to be installed. License classes SPW1, SPW2 and SPW3 are for solar systems with a capacity of not more than 400 watts, 2kW and 50kW respectively. Only SPW4 technicians will be allowed to install solar grids of any capacity.

Investors have poured nearly $1 billion into the development of off-grid solar energy and retail technology companies in Africa such as M-kopa, Greenlight Planet, d.light design, ZOLA Electric and SolarHome. Most of these companies are located in Kenya.

To know more about the proposed rules, click here (PDF).

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Late August this year, one of Nigeria’s leading telecom companies, 9mobile, announced it has acquired the first ever payment service bank license from the country’s central bank, alongside Hope PSB and Moneymaster PSB. The payment service bank license will, among other things, enable it to launch a range of products, including mobile money services, among others. Barely four months after that event, the Central Bank of Nigeria (CBN) is back with yet another set of rules, this time relegating every fintech company still basking in the euphoria of possessing a “do-all” license to their respective playing fields.

“The Central Bank of Nigeria, in line with its commitment to promote a strong and credible payment system has approved new license categorisations for the payments systems,” a circular released by the CBN reads, in part.

What Do The New Rules State?

The new rules are nothing short of sending all fintech startups currently operating broadly using the Payment Service License into their respective territories, and then streamlining them according to what they can do and cannot do. Accordingly, four new groups have emerged, namely: switching and processing payment service providers; payment service providers involved in mobile money (MMOs); payment service providers involved in payment solutions (PSSs) ; and payment service providers under the regulatory sandbox.

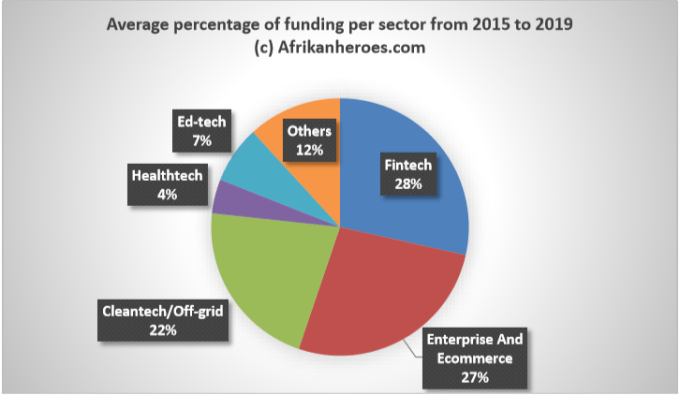

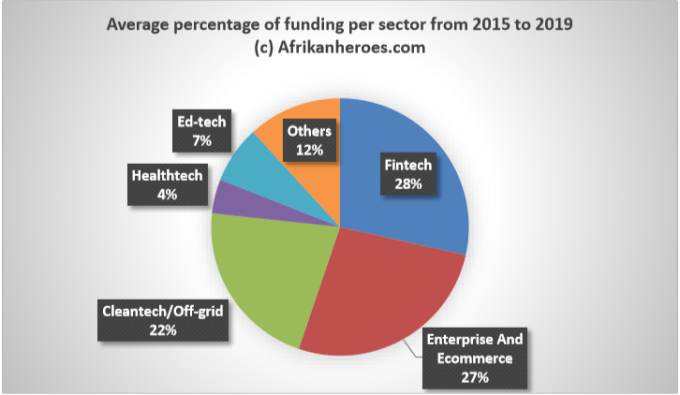

Sectorial VC funding, Africa. Data adapted from Partech

In Simple Terms, What May These New Groups Do And Not Do?

The implication of this new grouping is that one group may be forbidden from doing what other groups can do. To that effect, if you are a fintech startup under any of the groups, here is what you need to know:

Out of all the groups, only holders of a mobile money license can hold customer funds with them. Others cannot hold customer funds. In other words, mobile money services, at least to some extent, have the same status of a bank.

Where your startup wants to do both switching and mobile money operations at the same time, (like Interswitch doing mobile money together), your startup will need to set up a holding company, and make the companies engaged in switching and mobile money operations, separate subsidiaries (arms) of the holding company.

Companies which are payment solution service providers can hold a combination of payment service provider license, a payment terminal service provider or a super-agent at the same time.

The rules also state that before any startup within the group above can partner with any bank in Nigeria as regards the startup’s products and services, it must further get the approval of Nigeria’s central bank.

Type of License

Example Of A Fintech Company In Nigeria With This Type Of License

What Can Your Fintech Startup Do With This License?

What Is The Minimum Amount Required To Obtain The License?

Payment Solutions Services (PSSs)

Activities related to Super-agents, payments terminal service providers, payment solutions service providers

₦250 Million ($528K)

Super-agent

Innovectives; Flutterwave.

Recruit and manage agent networks, among other activities provided for in the Regulatory Framework for Licensing Super Agents in Nigeria

₦50 million ($132K)

Payment Terminal Service Provider (PTSP)

4ITEX Intergrated Systems

Deploys POS terminals; Own POS terminals; train merchants and agents

₦100 million ($264K)

Payment Solutions Service Provider (PSSP)

Paystack; Flutterwave

Offers gateway or portals for processing payments; Offers general payment solutions or develop payment applications software; or offers merchant services, aggregation or collection of payments

₦100 million ($264K)

Mobile Money Operation

MTN MoMo; 9PSB

Issues e-money; create and manage wallet, as well as manage pool accounts.

The Regulatory Sandbox Category is aimed at encouraging innovation and deepening financial inclusion. The CBN says it will review the products and solutions of applicants once the implementation of the Sandbox regime begins.

Not applicable

1 Dollar=₦380(official), December 11, 2020.Last Updated, Tuesday, May 25, 2021(9:00 AM)

The Implications Of The Above Tabulated Categories

According to CBN’s new rules:

A fintech startup in Nigeria can obtain a singular license called a Payment Solution Services License at ₦250 million, and this will allow the startup to do agency banking (Super Agent License); own POS terminals (Payment Terminal Service License) or own a payment processing portal ( Payment Solutions Service License). However, if the fintech startup does not have enough funds (₦250m) to go for the singular license that combines the three separate services, it can go for any of the three licenses (Super-Agent; PTSS; PSSs) separately.

Again, since a licensed mobile money fintech startup in Nigeria can hold customer funds , it is treated as a bank. Thus, where a startup wants to combine a mobile money banking license with any other type of licenses, it must set up a “non-operating” holding company. The holding company holds these other licenses, including a mobile money license under a subsidiary structure.

It is also possible for a startup under a holding company structure to acquire all types of licenses at the same time, provided that it maintains the minimum authorized capital thresholds for each of the licenses and obtains a no objection letter from the CBN’s Payments System Management Department created in 2018.

For startups without funds, the Regulatory Sandbox Category seems a sure bet, but CBN is yet to come clear on what criteria it will use to license fintech startups in this category.

It is worthy of note nevertheless that fintech startups in Nigeria have relied mostly on microfinance licenses than on any of these new groups. However, the new categorization rules are more particularly true for startups focused on mobile money services, switching, card processing and agency banking.

The deadline for complying with this new categorisation is 30th June, 2021.

To know more about the procedure for the new license categories, download CBN’s latest application guidance here (.pdf)

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

In September this year, pioneer fintech startup in Nigeria, Paga, announced that it was done doing business with the island of Mauritius and had relocated to the UK. Part of the startup’s reasons is that Mauritius is no longer a tax haven, and has been declared so by the Organisation for Economic Cooperation and Development (OECD). However, it seems that Paga is not alone. India, which used to record the highest foreign direct investment (from any country) from Mauritius is reporting a major shift in foreign investors’ preferred offshore territories. According to a new report, investors are going through Cayman Islands more now (instead of Mauritius and Singapore) in order to invest in India, even though Cayman Islands does not have a double taxation treaty with India (Mauritius has).

Tax

The east African country of Mauritius, which till last year contributed the second highest FDI inflows to India, was behind Cayman Islands, with FDI inflows worth $2.1 billion coming from Cayman Islands in first half of 2020 alone. Only Singapore ($8.3 billion) and US (7.12 billion) were ahead. This British overseas territory is now the third most preferred source of investments into India — it was 7th in FY19 and 5th in FY20.

“Unlike most countries, the Cayman Islands doesn’t have corporate tax, making it an ideal place for multinational corporations to base subsidiary entities to shield some or all of their incomes from taxation. In addition to having no corporate tax, the Cayman Islands impose no direct taxes, whatsoever on residents. They have no income tax, no property taxes, no capital gains taxes, no payroll taxes, and no withholding tax,” said Amit Jindal, co-founder, Felix advisory.

“The lower cost of operations and lower compliance requirements makes Cayman Islands more attractive. There has been dip in FDI inflows from Mauritius & Singapore and Cayman Islands with lower operating cost is increasingly replacing the same. Increasing regulations and cost of operations in Singapore and grey listing of Mauritius is an additional factor leading to investments being routed through Cayman Islands. Increase by nearly 300 per cent of FDI from Cayman Islands would keep the taxman in India on their toes,” says Divakar Vijayasarathy, Founder and Managing Partner, DVS Advisors LLP.

A Look At What Changed For Mauritius

Mauritius Tax Rules Have Changed For International Companies Using The Country As Their Headquarters In Order To Benefit From Low Tax

Under the former regimes operational in Mauritius, the Global Business Licence Category 1 (GBL 1), for instance, granted Holding Companies (majority of which were foreign companies with their headquarters in Mauritius) certain tax benefits, including an 80% foreign tax credit, which reduced the effective tax rate of such companies from 15% to 3%. This was also the case with Global Business Licence Category 2 (GBL 2) which granted tax exemption to companies.

By that structure, foreign companies as well as businesses operational in Mauritius profited simply by setting up Mauritian Holding Companies with little or no economic substance in Mauritius. By doing so, such companies effectively reduced their effective tax rates to a large extent.

To take care of that, Mauritius discarded the GBL Regimes in 2018, introducing a Partial Exemption Regime for Global Business Corporations (GBCs) operating in the country. This new regime provided for an 80% tax exemption on specified passive income of the GBC companies in Mauritius. To put it differently, since companies in Mauritius are generally taxed at 15%, the 80% tax exemption means that GBC companies have a tax liability of only 20% of the original 15%, meaning that they’re suffering a maximum effective tax rate of 3%.

Investments into India from foreign countries. Source: India’s Department of Industrial Policy & Promotion

However to benefit from the 80% tax exemption under the new partial exemption regime, foreign companies must meet the requirement of substance.

Under the substance feature, companies in Mauritius must further meet certain requirements to enjoy the 80% tax exemption.

Some of these requirements include that a GBC company must prove that it is centrally managed and controlled in Mauritius.

In determining what operations of a company are centrally managed and controlled, the Financial Services Commission in Mauritius usually considers whether the company meets at least one of the following criteria:

a) The company has or shall have office premises in Mauritius.

b) The company employs or shall employ on a full-time basis, at the administrative/technical level, at least one person who shall be resident in Mauritius.

c) The company’s constitution contains a clause whereby all disputes arising out of the constitution shall be resolved by way of arbitration in Mauritius.

d) The company holds, or is expected to hold, within the next 12 months, assets (excluding cash held in a bank account or shares/interests in another corporation holding a Global Business Licence) that are worth at least 100,000 United States dollars (USD) in Mauritius.

e) The company’s shares are listed on a securities exchange licensed by the Commission.

f) The company has, or is expected to have, a yearly expenditure in Mauritius that can be reasonably expected from any similar corporation that is controlled and managed from Mauritius.

In practice therefore, a South African company, for instance, may have its board of directors in Mauritius while it is managed from South Africa. In this case, the authorities could say the company is not eligible for tax residency. They will now look at the substance on the ground in Mauritius.

These countries have double tax agreements with Mauritius through which several foreign companies could previously claim enormous tax benefits. This, in part, helps to explain Paga ‘s latest choice of the UK over Mauritius

The Implication of This

The fallout of this move will be that many of the structures set up in Mauritius and claiming treaty benefits on the basis that they have tax residency certificate may now have to take a look at the structures again.

So many of the Mauritius structures may get challenged in Mauritius itself and several existing structures will be forced to increase the substance requirements within Mauritius for them to continue getting the tax benefits.

In simple terms, the consequence of not being considered tax resident in Mauritius is that the company would not benefit from the numerous tax advantages that are obtainable from doing business in Mauritius. So, it is not a case of claim benefit from Mauritius, but do business in your home country. You have to manage your business in Mauritius before you claim the benefits.

Mauritius is a tax treaty jurisdiction and has so far concluded more than 42 tax treaties which are in force with the countries listed above.

The Bottom Line

All these, nevertheless, do not mean that Mauritius no longer continues to hold the best business environment and tax regime in Africa. In terms of ease of doing business, Mauritius ranks first in Africa, and 13th in the world, ahead of countries like Australia, Germany, Canada, China, Netherlands, Belgium or Hungary.

The country also ranks first as the most innovative country in Africa and 52nd in the world according to the World Innovation Index. Globally, the Mauritian capital, Port Louis, is the 9th economy in terms of the quality of institutions and the dynamism of the markets.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

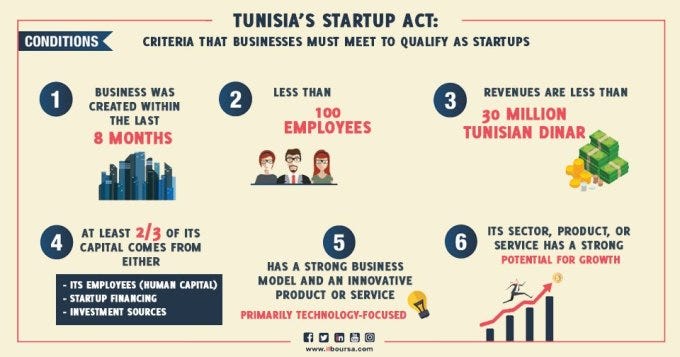

Barely two years after Tunisia passed its Startup Act, 379 startups have now been registered under the Act, the last set –twenty-six startup labels– just awarded by the Ministry of Communication Technologies. Awarding the startup label is part of the “Startup Act” program, which has as its main objective, the promotion of those starting businesses in Tunisia or foreign businesses which are settling there.

The Tunisian Startup Act Has Given Startups In The Country A Voice

Unarguably, Tunisia leads other African countries in bold startup legislations. The Tunisian Startup Act, passed in May, 2018, puts in place the following measures in favour of startups:

Tunisian Startup Act defines startups as an entity having legal existence not exceeding eight (08) years from the date of its constitution.

More than two-thirds (2/3) of Tunisian startups’ capital must be natural persons, venture capital investment companies, collective investment funds, investment, seed money and any other investment body according to the legislation in force or by foreign Startups to qualify as startups under the Act.

The business model envisaged by the Tunisian Startup Act is one that is highly innovative, utilizing cutting-edge technology.

Under the Act, any individual promoter of a Startup, public agent or employee of a private company, may benefit from the right to Startup Leave for creation of a Startup for a period of one year renewable once

Any promoter of a Startup may benefit from a Startup scholarship for a duration of one (01) year. Only three (03) shareholders and full-time employees in the relevant Startup may however benefit from the scholarship awarded.

Young graduates who create startups are free from taxation for three years.

The profits from the sale of the securities relating to the shares in the Startups are exempt from the capital gains tax.

Startup labels are also part of the innovations Tunisia’ s Startup Act has introduced.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Algerie Telecom has decided to give more opportunities to startups specializing in the ICT. On December 3, 2020, the operator unveiled new specifications for its calls for tenders. It was designed to facilitate the access of 2,300 technological microenterprises to public procurement.

Brahim Boumzar, Minister of Post and Telecommunications

Thus, the discriminatory clauses present in the old schedule have been removed. In addition, the new guide simplifies tender documents as well as procedures. It is clearer and more readable as to the needs of the public sector. The two thousand microenterprises concerned by this initiative are those already registered on the new electronic portal Safqatic, launched last August by the teams of Brahim Boumzar, Minister of Post and Telecommunications. The platform was established to ensure transparency and probity relating to public procurement and market monitoring.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Startups in Ghana are determined. Barely a month after announcing a major move to get a Startup Act, Ghana’s startup ecosystem is living to the letters of its resolution, and who knows, before the end of next year, the country may be the next in line to get an Act for startups in Africa.

Ghana’s Business Development Minister, Dr Ibrahim Mohammed Awa

“We have formed a committee working on the Startup Bill and within two months, it will be ready for the cabinet’s consideration and Parliamentary approval,” Ghana’s Business Development Minister, Dr Ibrahim Mohammed Awa was quoted as saying after the third Ghana Business Awards Night held on October 30, 2020.

“When this bill is passed it means you can start a business, and for eight to 10 years you will not pay taxes. This is to encourage young people to put back the profit and expand the business,” he further added.

What Is The Progress So Far?

A new website, http://www.ghanastartupact.org./, has been set up and it is helping to track the progress of this journey. Today, a technical working committee of the Ghana Startup Bill will hold 1 day consultative workshop for startups and young entrepreneurs to solicit their views and inputs into the Bill. The event scheduled to hold at the Accra Digital Centre, from 9am — 2pm, hopes to engage 100 startups and young entrepreneurs, selected from across the country to deliberate on the drafted bill.

The following points will be up for deliberations;

• The definition of a “Startup”

• Startup certification and Label selection processes

• Startup benefits and incentives, including Tax wavers and holidays, Startup Financing, Business support and capacity building programs, Access to markets, Intellectual Property Rights, Research and Development support, Investor and Mentor support, among others.

• Benefits of the startups to the state, etc.

The Technical Working Committee which was set up in October this year by the Ministry of Business Development, through its agency, National Entrepreneurship and Innovations Program (NEIP), has held series of stakeholder consultations leading to the drafting of the bill.

The Committee recently held a 3-day retreat with key stakeholders at Dodowa where experts reviewed the draft and made some inputs.

“This is the time to present the drafted bill to the end-user beneficiaries, which are the startups and young entrepreneurs, for them to scrutinize it, and ensure that all they need for their businesses to grow has been captured,” said Communication Director for the committee, Solomon Adjei.

Ghana Startup Act Ghana Startup Act

The Scope Of The Proposed Bill

The committee, which has a mandate to within three months engage widely with all relevant stakeholders to come out with a draft Ghana Start-up Act, will among other things deliberate to;

Set up an incentive framework for the creation and development of Start-ups in Ghana to promote creativity, innovation, and the use of new technologies in achieving a strong added value and competitiveness at the national, regional, and district levels.

Provide the legal backing for business starting and promotion of Start-ups for decent job and wealth creation, in accordance with the SDG 8, among others.

The committee will then present its final work — the draft Ghana Start-up Act, to the NEIP and subsequently to the Ministry of Business Development, Ministry of Trade and Industry, Attorney General, Parliament of Ghana, and the Office of the President, after which they will run series of advocacy to ensure the Act is passed by Ghana’s legislature.

“Startups are the basics to create jobs and wealth in this country,” Dr Awa said. “We want to help start young people grow and this Startup Bill will be able to help them [youth] own their businesses and not look up to government for job; because we all know that the jobs are not in the public sector, they are in the private sector.

“So we [government] want to create an enabling environment in the private sector that can make it attractive to young people for them to engage in,” he emphasised.

The first specific startup law globally was passed in Italy in 2012, and Africa is increasingly catching on. Tunisia and Senegal are the only countries in Africa that have passed the Act, although plans are being mulled by Rwanda, Kenya, Ethiopia, Mali to follow suit.

Ghana’s Startup Act’s drafting committee is made up of notable bodies such as Ghana’s National Entrepreneurship and Innovation Program (NIEP), Ghana Chamber of Young Entrepreneurs (GCYE), Ghana Start-up Network (GSN), Ghana Hubs Network (GHN), i4Policy and Private Enterprise Federation (PEF) with funding and technical support from GIZ Make IT.

The Technical Working Committee, made up of experts and the ecosystem enablers was equally set up to champion the advocacy action for the development and enactment of the proposed Ghana Startup Act.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer