Going forward, telecom companies in Kenya must compensate customers whose services have been disrupted by their poor service delivery. The Communications Authority of Kenya (CA) has issued draft new regulations requiring mobile phone operators Safaricom, Airtel and Telkom Kenya to compensate businesses and customers when network outages disrupt voice, data and text services. The draft regulations have been published for public comment and seek to compel the telecommunications providers to either pay or offer credit equivalent to the time users are without voice and SMS services.

What Does The New Regulation Say?

The new rules are aimed at shielding millions of mobile phone clients from poor services related to network outages, including lack of internet connections.

The regulator is permitted by law to sanction any telecommunications company that inconveniences customers through service interruptions as a result of omission on its part.

An operator found in breach risks a fine of up to 0.2 percent of its revenues, which could run into hundreds of millions of shillings. Now, the regulator wants to include compensation to clients for mobile phone outages.

Kenya telcos compensate customers Kenya telcos compensate customers

Licensees must develop and implement an outage credit policy in situations where service is unavailable due to system failure and not as a result of scheduled and publicised maintenance, emergency or natural disaster, say the draft rules.

The policy will compensate subscribers or issue credit equivalent to usage over a similar period that outage lasted and compensate customers for each day that service has been unavailable.

Compensation will be based on how much the operator charges per minute for calls and data.

In 2019, Kenya had 55.2 million mobile phone subscribers who made 58.78 billion minutes of calls, up from 39.19 billion in 2015. Scheduled outages and those caused by factors beyond the control of an operator, technically known as force majeure, usually do not attract sanctions

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Ethiopia has a very large population, the second in Africa, just after Nigeria, with over 114 million people — 66% of whom do not have bank accounts — but the country is not ready to open up parts of its economy to foreign investors yet. Apart from refusing to allow private ownership of telephone communications companies, the country is again shutting its financial services doors against foreign investors in latest rules. In latest investment rules, the country has continued to reserve business opportunities in certain sectors, including financial services, exclusively for local investors.

Ethiopian Prime Minister Abiy Ahmed

Here Is What You Need To Know

Under the new investment rules, banking, insurance, brokerage services, and legal consultancy remain off limits for foreign investors, according to the regulations published on the Ethiopian Investment Commission’s website.

Exports of coffee, and media and security services are also exclusively for local investors.

The updated regulations are part of economic reforms by the government of Prime Minister Abiy Ahmed and include the privatization of state-owned enterprises such as sugar and cement companies.

The country has also revealed plans to finalise the partial privatisation of its telecommunications sector by February 2021. This new development comes just three weeks after the Ethiopian Communications Authority (ECA) suspended the country’s telecom privatisation plans.

The ECA had earlier announced plans to sell a 40% minority stake in the state-owned telco, Ethio Telecom. According to the ECA, bids for two mobile network operating licenses had been received from 12 global and African telcos including MTN Group, Orange, Safaricom, Vodacom.

Under the new rules also, international air transport services, which is dominated by state-controlled Ethiopian Airlines, public transport, and the import and export of power are among industries reserved for joint ventures with the government. Still, foreign investors working with a domestic partner are restricted to a 49 percent stake, according to the regulations that took effect on Sept. 2.

Several foreign banks have representative offices in the country, including Equity Group Holdings of Kenya. Lease companies, such as a unit of New York-based Africa Asset Finance Co., which pledged to bring in equipment worth $600 million after being licensed in August, can also operate there.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Barring any last minute changes, South Africa is prepared to go ahead with a new regulation that would see black people owning at least 30% equity in every tech company in the country. This is according to the country’s Independent Communications Authority of South Africa (Icasa) which says plans are ongoing to introduce new BEE regulations for the Information and communications technology (ICT) sector before the end of the 2020/2021 financial year.

‘‘The purpose of the draft regulations is to ‘promote equity ownership by Historically Disadvantaged Persons and to promote Broad-Based Black Economic Empowerment (B-BBEE),’’ Icasa said.

Here Is What You Need To Know

In a presentation to parliament on Friday (4 September, 2020), Icasa said that the draft regulations seek to impose the following regulations, amongst others:

According to the new regulation on any application, an Individual Licensee is required to provide the Authority with proof, by way of a certificate from a recognised and accreditated verification agency, confirming its ownership equity (shares) held by the Historically Disadvantaged Persons (HDG), which may not be lower than 30%.

Under the new regulations, the 30% HDG equity requirement is applicable to all individual licensees of the Independent Communications Authority of South Africa (Icasa), regardless of their size and income level.

The new 30% HDG equity requirement applies to all sorts of applications pertaining to individual licenses, including new applications, transfers, renewals and amendments.

The only class of persons to be exempted from the new regulations are a persons with class licenses and wholly owned state entities.

The proposed South Africa ‘s equity regulation defines black people as African, Coloured and Indian People who are citizens of South Africa by birth or descent or who have become citizens of South Africa by nationalization before 27 April 1994, or on or after 27 April 1994 and who would have been entitled to acquire citizenship by naturalization prior to that date.

Notably, the regulations also introduce strict punishments for non-compliance including a fine not exceeding R5 million or 10% of the company’s annual turnover.

ICASA said that compliance by existing licensees with these regulations is required within 24 months of being published.

Historical VC Investments in South Africa (2009–2018) — Source: the latest Southern African Venture Capital and Private Equity Association’s (Savca) Venture Capital Industry Survey

Data published by the South African Broad-Based Black Economic Empowerment (B-BBEE) Commission at the end of July indicates a slight change in the levels of transformation, with the overall black ownership reflecting a four percentage point increase from 25% black ownership in 2018 to 29%.

Only 3.3% of entities listed on the JSE are 100% black-owned, which was 1.2% in 2018 and 1% in 2017, the commission found.

The three worst-performing sectors on ownership in 2018 were AgriBEE (11.19%), media, advertising and communication (19.55%) and finance (21.64%).

The commission said that there are also worrying trends observed over the three-year period between 2017–2019.

“Though black ownership indicates slight change, the black ownership percentage does not always correspond with the management control scores,” it said. “For instance, an entity is able to score full points for ownership and very low on management control, which gives the impression that despite black ownership recorded, black people are not involved in the control and core operations of the measured entity. Also, the saturation of management control points is still between junior and middle management, also noting the rotation of black executive from one measured entity to another, without utilising the skills development element to create a pipeline of new black executives.”

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Security systems are only as successful as the people who sit behind them

In May 2020, the personal records of more than 24 million South Africans and nearly 794,000 companies were handed over to someone impersonating a client. The personal records, identity numbers and addresses of millions of people and thousands of businesses were given to this person because they had fooled the system. It’s a hard lesson in how important it is to embed security not just into the technology and the devices of a company, but into its people. According to Anna Collard, SVP of Content Strategy and Evangelist, KnowBe4 Africa security is not just the responsibility of IT, it is the responsibility of every single person in an organisation.

Anna Collard, SVP of Content Strategy and Evangelist, KnowBe4 Africa security

“It is critical that organisations create a culture of security in order to combat this increasingly hostile security environment,” she adds. “A successful security culture is driven by leadership, the human resources (HR) department, internal marketing & communication and ongoing security training. Truly agile and capable security is a people project, not a technology one.”

Successful security balances on three pillars: technology, policy and people. The technology is the firewalls, the anti-virus, the ongoing alerts and the endlessly evolving bouquets of solutions that are designed to give the business an edge in the war against cybercrime. Policy is what outlines the processes that people across all levels of the organisation have to follow in order to ensure that the technology can do its job, that checks and balances are in place as well as to guide people on what they can and cannot do in the digital realm. People are the key to ensuring that both technology and policy actually work.

“This is why HR has to be involved with security,” says Collard. “It is fundamental to changing behaviour within the organisation and helping to build a culture that recognises the importance and value of security. It is, of course, also the disciplinary arm that enforces policy and that ensures there are consequences when people continue to break the rules or fall for phishing scams or perpetually do the wrong things.”

Whether the organisation incentivises or punishes – security has to have consequences. Employees must see that the executive is as tightly bound by the regulations as everyone else. And they need to understand exactly what these regulations are, why they are important and the implications that failure can have on their jobs and the future of the organisation. With data protection regulations such as South Africa’s Protection of Personal Information Act (POPIA) in full effect, the cost of an avoidable mistake can result in hefty fines or even imprisonment for the directors of the company. A mistake that can be as simple as someone clicking on a phishing email, falling for a social engineering call or unleashing a ransomware virus because they didn’t recognise the risk.

This is where good communication becomes as essential as good technology. “The way we communicate, the content we use, and the way that it’s distributed can make such a difference in how an organisation creates a strong security culture,” adds Collard. “It’s a blend of HR people practice, security good practice and marketing best practice. These three elements need to be pulled together to create a cohesive security ecosystem that ensures people truly understand that their actions can have serious consequences.”

This level of engagement can be achieved in multiple ways. Empower a person who interacts with the different stakeholders across the business and who has the right support from the executive and HR. This role will then be committed to ensuring that security culture is carried throughout the company by implementing the right training platforms, incentivisation/punishment systems and driving participation.

“Success will depend entirely on the level of stakeholder buy-in, the depth of the training and a commitment to ensuring that the training is ongoing and measurable,” concludes Collard. “Security training has to be iterated and repeated constantly to ensure that people are always kept aware of its importance and any changes in attack vector or threat. Only by keeping security top of mind, all the time, can an organisation truly embed a culture that’s capable of staying secure and alert.”

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Nigeria has been at the forefront of the African startup ecosystem. According to the most recent report from the African Private Equity and Venture Capital Association, between 2014 and 2019, Nigeria accounted for 14% of all total VC funding deals done in Africa, just behind Kenya (at 18%) and South Africa (at 21%). However, even though the number of VC deals concluded on startups in Nigeria is much lower than that of South Africa or Kenya, VCs are pouring larger amounts of money into the West African country compared to South Africa or Kenya. For instance, according to the data firm, Partech Africa, in its 2019 venture capital report, Nigeria topped Africa’s VC funding landscape with US$747 Million in VC investment (37% of all funding). A similar feat was repeated by the country in 2016 and 2015, with South Africa and Kenya taking the lead, only recently in 2017 and 2018 respectively. Nigeria also houses Africa’s most valuable startup ecosystem — Lagos — which according to Startup Genome, in its Report, was worth $2 billion as of 2017. For one thing, Nigeria is Africa’s largest economy, behind South Africa with a Gross Domestic Product (GDP) of $400 billion (as at 2018) as well as the continent’s most populous country with a World Bank estimated population of 202 million people.

In view of these, it has become relevant to explore how Nigeria supports its startup ecosystem through its laws, regulations and policies.

Incentives — Tax Exemptions

A. For Venture Capital Firms

A long range of tax exemptions are given to investments made by venture capital companies in Nigeria under the country’s Venture Capital Incentives Act.

Consequently, under the Act, for every equity investment made by a venture capital company in a startup in Nigeria, there are deductions from the amounts to be paid as tax from the startup company’s income tax, each year until 5 years after each investment. For the first year, 30% will be deducted. For the second year, another 30% deduction will be made; 20% in the third year; 10% in the fourth year; while 10% deduction will be made in the fifth year.

Again, the withholding tax to be paid on dividends declared in a startup funded by a venture capital company in Nigeria is 5%, under the law, for the first five years of the investment.

Where the equity investment of the venture capital firm in a Nigerian startup company is sold or disposed of, the gains made by the venture capital firm on the equity investment is not liable to capital gains tax by the provisions of the Nigerian Capital Gains Tax.

However, to qualify to benefit from the incentives, investments by the venture capital company must make up at least 25% of the total funding required by the startup. The investment must also be specifically made in innovative companies; or for commercialization of research findings with high returns potential; or for the purposes of promoting SMEs. The venture capital company and the startup receiving the venture capital must, also, first be registered with Nigeria’s Federal Inland Revenue Service (FIRS), in charge of collection of taxes on behalf of Nigeria’s federal government, in order to benefit from the tax exemption.

Better Legal Framework For A VC Fund

Under Nigeria’s newly passed Companies and Allied Matters Act (‘The CAM Act’), it has also become easier to set up a legal structure for a VC fund. By the terms of the new law, venture capital firms in Nigeria may now be set up as limited liability partnership or limited partnership.

Previously, before the law came into being, it was normal practice to register VC firms as limited liability companies; general or limited partnerships, or as limited liability partnerships under the Partnership Law of Lagos State (Nigeria’s major economic city).

Even though under the old regime, general and limited partnerships could be registered and applied throughout Nigeria whereas limited liability partnerships only applied in Lagos, the new regime spells out definite governance framework for partnerships generally, as well as enlarges the operational scope of partnerships to cover the whole of Nigeria, and not just Lagos alone.

The essential difference between a limited liability partnership and a limited partnership under the new law is that while a limited liability partnership is a corporate body which has a legal personality different from the partnership as well as a perpetual succession, a limited partnership has no separate identity from those of the partners that make it up.

Indeed, a limited partnership under the new law captures the ideal form of most VC funds, which usually have one or more partners called general partners — responsible for the management of the funds under the partnership, and who are also liable for the debts and obligations of the partnership — as well as one or more persons known as limited partners — who contribute certain sums of money or property to the partnership and who shall not be liable to the debts and obligations of the partnership.

Apart from properly providing a clear legal framework for the operation of VC funds in Nigeria, the new partnership regime, under the CAM Act, also functions to provide some clarity about their taxation.

Under the Nigerian tax laws, dividends declared by a VC firm that is a partnership — from its investment in startups — are subject to a 5% withholding tax. Where the dividends are declared by the fund and are shared in a partnership, the amount each partner is entitled to is further taxed under Nigeria’s Personal Income Tax Act. However, where a partner who is part of the VC firm is a limited liability company, the company must pay company income tax of 30% on profits made from such earnings, including a further 2% education tax and 10% withholding tax.

Where, however, the VC firm is a limited liability company, under Nigerian laws, apart from paying a corporate income tax of 30%, they also pay 5% withholding tax and 10% capital gains tax (or zero capital gains tax where it is the equity (or shares) of the company that was disposed of).

Innovative startups in Nigeria have a range of incentives to encourage their early stage growth, even though in most instances, the process of applying for and securing the incentives are demanding, and in most instances unrealistic. The incentives include:

The Exemption Of Early Stage Startup Companies From Corporate Taxes

Under Nigeria‘s new Finance law:

Small businesses with annual turnover of less than ₦25m ($64.5k) are now exempted from Companies Income Tax. However, to benefit from such incentive, such small businesses must first register for taxation in Nigeria and must continue to file tax returns during the period their profits are below the ₦25m threshold.

A lower Corporate Income Tax rate of 20% ( as against 30%) will however apply to medium-sized companies with yearly turnover between ₦25m and ₦100m ($258k). To benefit from such incentive, the companies must first register for taxation in Nigeria and must continue to file tax returns during the period their profits are between the ₦25m and ₦100m thresholds.

The law now, also, allows a minimum tax rate of 0.5% for every turnover and this provision will only apply to small companies (less than ₦25m turnover), thus allowing companies non-resident in Nigeria for tax purposes to pay minimum tax.

Again, for companies or businesses that pay their tax dues early, a 2% deduction bonus on tax payable is given, in the case of medium-sized companies between ₦25m and ₦100m; and 1% deduction for large companies from ₦100m and above.

A Pioneer Status Tax (Free Tax) Incentive For Innovative Business Models

Although this is one of the most significant incentives available to early stage startups in Nigeria, there were only about 35 standing beneficiaries of pioneer status tax incentive in Nigeria as at March 2020, out of which only 1 is an ICT firm and 6 are agro-businesses; even though more than 125 applications were filed for the grant of the incentive during the period.

Nevertheless, by virtue of the provisions of Nigeria’s Industrial Development (Income Tax Relief) Act (“IDITRA”), the Pioneer Status is to be granted for an initial period of 3 years with a possibility of an extension for another 2-year period to companies in their first year of business or operations in Nigeria. The companies must, also, be among those on the list of pioneer industries in Nigeria. Consequently, companies or businesses older than a year would not benefit from the pioneer status incentive.

Again, businesses that have existed for several years in a particular sector may not enjoy the pioneer status, except such companies branch into new lines of business covered under a list of 27 or more new industries and products.

To qualify for the Pioneer Tax Incentive, the company must also have incurred capital expenditures of up to ₦100m ($258k). Companies granted Pioneer Status Incentives in Nigeria also enjoy tax relief on income earned during the tax holiday period and dividends paid from the profits earned during the tax holiday. The incentive also enables the company to set off tax losses incurred during the tax holiday against profits earned after the holiday, and to deduct capital expenditure in the same manner.

A Right For Startups To Partner With Large Corporates In Projects Above $1 Million

Under Nigeria’s Guidelines for Content Development in Information and Communications Technology, all indigenous or Nigerian Companies who have secured IT projects or contracts with any Nigerian Federal Public Institution or Government owned companies, of which the gross value of the project is Five Hundred Million Naira (N500,000, 000, 00)or above, shall engage on the project, a Nigerian startup or incubation team for the purpose of Research &Development on the project.

The Guidelines apply to all Federal Ministries, Departments and Agencies, Federal Government Owned Companies (either fully or partially owned) Federal Institutions and Public Corporation, Private Sector Institutions, Business Enterprises and Individuals carrying out business within the Information and Communications Technology sector in Nigeria.

An Alternative IPO Exit Route As Startups Can Now List On A Special Board On The Nigerian Stock Exchange

Nigeria also has developed a new mechanism that will allow high-growth startup companies to list on the Nigerian Stock Exchange. A fourth board on the exchange meant for small businesses and startups has now been launched, to that effect.

This has strengthened the exit alternatives available to startups in the country. That is, startups in Nigeria, apart from acquisition, may now consider IPOs (Initial Public Offerings) on the Nigerian Stock Exchange. The board, known as the Growth Board would offer them the opportunity to raise equities for their businesses.

However, it appears this is over-flogging a dead horse. A similar board, known as the Alternative Securities Market (ASeM) had previously been created by the exchange for emerging businesses — small and mid-sized companies with high growth potential. Findings show that only 9 companies (mostly in the oil and gas industry;none of which is a tech startup company), have been listed on the board.

One significant reason for this lack of interest by startup companies is the unappealing state of the Nigerian Stock Exchange, which at a market capitalisation of $ $36.91bn, is 22 times smaller than the Johannesburg Stock Exchange (at$825.66 Billion).

There are a number of government-backed funds available in Nigeria, a majority of which are by way of loans and not equity. They are listed below:

Nigeria’s Central Bank Intervention Funds

The Central Bank of Nigeria, from time to time, launches series of intervention funds, aimed at startups and small and medium scale businesses.

For instance, owners of businesses in the Nigerian creative industry may now access loan facilities as high as ₦500,000,000 (about $1.4 million). The Creative Industry Financing Initiative is targeted at:

Businesses in the fashion (including designing) industry

Businesses in the Information Technology (including e-commerce, online payment solutions, software engineering etc.)

Businesses in the Nigerian movie industry (including movie producers, movie distributors)

Businesses in the Nigerian music industry (whether as record labels, music artistes, etc.).

The businesses may get up to the following amount:

A student of Software Engineering anywhere in Nigeria may get up to ₦3 million ($ 8,294) to boost his/her education.

Movie Production businesses may get a maximum of ₦30 million ($82,943) to boost their businesses.

Movie distribution businesses may get up to ₦500 million ( $1.4 million)

Businesses in the Nigerian Fashion and Information Technology can also get funds to cover their rental/service fees (the exact amounts were not specified)

Music Businesses may also get funds to cover their training fees, equipment fees, and rental/service fees.(The exact amount is however not specified. It also appears that the funds are not extended to businesses of production of music, and other related music roles).

Other intervention funds by the central bank include the Micro, Small, Medium Enterprises Development Fund (MSMEDF); Commercial Agric Credit Scheme (CACS); Real Sector Support Facility (RSSF), etc.

To access any of the intervention funds, startups may need to go through financial institutions authorised by the central bank to disburse the funds. FCMB is an example of a Nigerian bank that participates in the scheme. Interested startups can check out its offers here.

Funds Under Nigeria’s Bank Of Industry

There are also series of funds operated by Nigeria’s Bank of Industry, the oldest and largest Development Finance Institution currently operating in Nigeria. BOI provides financial assistance for the establishment of large, medium and small projects as well as the expansion, diversification, rehabilitation of existing enterprises. Consequently, the Bank operates funds targeted at youths (Graduate Entrepreneurship Fund; Youth Entrepreneurship Support (Yes) Programms; Youth Ignite Programme); women; asset finance; as well as working capital.

To access any of the intervention funds, it may be easier to go through financial institutions authorised by the bank to disburse the funds.

FCMB is an example of a Nigerian bank that participates in the scheme. Interested startups may also check out its offers here.

Development Bank of Nigeria (DBN)

Development Bank of Nigeria exists to alleviate financing constraints faced by Micro, Small and Medium Scale Enterprises (MSMEs) in Nigeria. The DBN loan repayment duration is flexible (up to 10 years with a moratorium period of up to 18 months).

To access any of the intervention funds, it may be easier to go through financial institutions authorised by the bank to disburse the funds.

FCMB is an example of a Nigerian bank that participates in the scheme.

Interested startups may also check out its offers here.

Future Generations Fund Under Nigeria’s Sovereign Investment Authority

The purpose of the Future Generations Fund is to preserve and grow the value of assets transferred into it, thereby enabling future generations of Nigerians to benefit from the country’s finite oil reserves.

The fund is mostly available to venture capital or private equity firms, and not directly to startups.

Although Nigeria has not expressly permitted equity or loan crowdfunding, there is a proposed regulation to that effect.

Under the proposed regulation, only MSMEs (Micro, small and medium enterprises) registered as companies in Nigeria with a minimum of two-years operating track records shall be eligible to raise funds through a Crowdfunding Portal registered by Nigeria ’s Securities And Exchange Commission.

The following recommendations are, therefore, important and if properly harnessed, have the potential to unlock the continent’s largest economy:

Startup Act:

Nigeria is long over-due for a Startup Act, which has since been adopted by other African countries such as Tunisia and Senegal.

One thing a Startup Act does is to aggregate all efforts geared towards promoting and uplifting all startups in countries where the Act exists. For instance, having a Startup Act will help to tailor incentives to startups more precisely, unlike what obtains presently in Nigeria where established corporates and well-funded companies end up benefiting most from the existing tax incentives, such as the Pioneer Status Incentives.

The Senegalese Startup Act, among other things, grants special status (known as a label) to a labelled innovative and disruptive private or public company, which has been legally registered for a period of not more than 8 years; and whose strong growth potential is built on a disruptive economic model. The law also applies to any startup created by any Senegalese living abroad who owns at least 50% of the startup. This will, undoubtedly, attract more investments back home from Senegalese citizens living in foreign countries.

Enactment Of The Equivalent Of South Africa’s Section 12J

Another policy change capable of facilitating the growth of startups in Nigeria is the introduction of an equivalent Section 12J of South Africa’s Income Tax Act of 2009.

The incentive allows investors who make investments in approved Venture Capital Companies (VCC)— that then invest in qualifying small companies — a tax deduction.

Thus, by investing in a Section 12J venture capital company, the investor not only qualifies for a full deduction of the total investment amount from their taxable income in the relevant tax year, but they are also indirectly supporting the South African economy and the growth of local SMEs.

By operation, Section 12J works like this:

A tax-paying entity (corporate or individual) approaches a VCC with its investment.

The VCC accepts the investment for investments in its portfolio companies and issues the investor with a certificate for the amount invested.

With this certificate, the investor approaches the South African Revenue Service (SARS) and presents the certificate. The certificate empowers the investor to deduct the full value of the investment from their taxable income in that tax year.

Section 12J is so attractive to investors that when the investment reaches maturity and the investor withdraws from the VCC portfolio, the capital gains tax on the investment will be zero as a result of the initial benefit of the 100% tax deductibility.

This explains why there are, today, many VC firms in South Africa and why South Africa has collected more than 21% of all VC funding deals in Africa between 2014 and 2019, whereas Nigeria only received 14% of the deals, even though Nigeria is the continent’s largest economy and has more than 3 times South Africa’s population.

Although Nigeria has a venture capital legislation, there is a big difference between enticing individual and corporate investors to invest in venture funds and enticing venture funds to invest in startups. Nigeria is simply doing the latter; and because of the risk aversiveness of investors in emerging markets, the country may not get the results it desires for its local startup ecosystem any time soon.

Establishment of Equity Funds For Startups

What Nigeria currently has are credit facilities for startups. There should be government-backed equity funds that take up shares in startup companies instead of credit facilities that usually come with strong terms such as interests, modes of repayment of principal sums, etc.

Equity participation in early stage startups function to assist them to go through the difficult periods of their early years until they are mature enough to take in any type of financing.

Indeed, while Nigeria maintains little or no presence in early stage investing by way of equity funds, countries like Egypt and South Africa do not.

Top South African companies in 2016, for instance, launched the $84 million SA SME Fund, a VC fund to co-invest alongside various investors (not solely VC investors). SA SME Fund CEO Ketso Gordhan said the fund would invest about 75% of the sum in black-owned small and medium-sized enterprises, including tech startups.

SA SME Fund and the government’s Technology Innovation Agency (TIA) have, also, further announced a public-private partnership to co-invest R350 million across three venture capital funds. The partnership sees over R350 (over $23 million) invested in the three venture capital funds. South Africa’s SME Fund’s mandate to the three fund managers includes a requirement that they invest at least 50 percent of the fund into businesses owned by black entrepreneurs.

In Egypt, there is Bedaya, a government-backed incubator, established by Egypt’s General Authority for Investment and Free Zones (GAFI) in 2009. The incubator offers up to LE 150,000 (US$9,047) in funds as well as business development services, networking opportunities and manufacturing spaces to startups in Egypt. 60 percent of Bedaya’s fund is allocated to supporting startups from governorates outside of the capital, Cairo.

In Morocco, government-owned financial institution “Caisse Centrale de Garantie-CCG” also partners with the Maroc Numeric Fund to facilitate access to financing for very small and medium-sized businesses and, more recently, for innovative project developers and startups.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

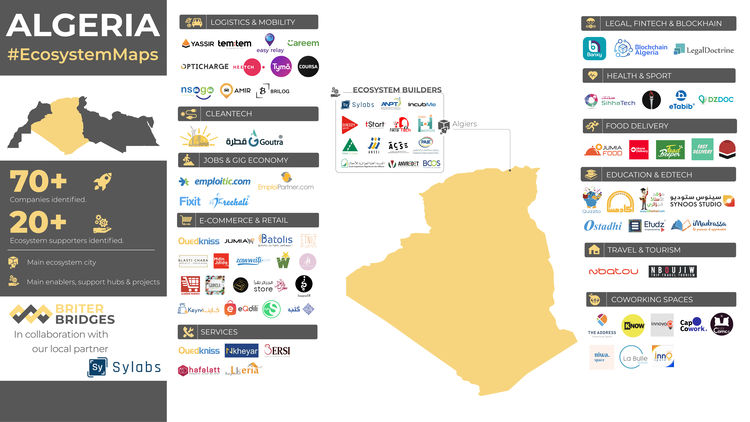

The Minister Delegate in charge of micro-enterprise in Algeria, Mr. Diafat Nassim has revealed that of the 380,000 enterprises created under the National Support Agency for Youth Employment (Ansej) system, more than 70% are in crisis.

Djafat Nassim, during his intervention on the airwaves of the radio Chaine III, assured that his department plans to help these companies in difficulty by a series of measures:

“Among these companies in difficulty, we have those who do not have the capital to restart their activities. For this category, we are going to institute, as of now, the rescheduling of debts over 5 years with a deferment of one year and the elimination of late payment penalties ”, he said.

Concerning the people, carriers of Ansej projects, “deceased” or “victims of natural disasters”, the Minister Delegate, in charge of micro-enterprise affirmed that the State intends to proceed to a partial cancellation of their debts “on a case by case basis.

Furthermore, for those who embezzled funds from the projects, the official clarified that there will be no criminal treatment for those who embezzled the funds, stating: “Even if criminal prosecution is excluded against those with” hijacked ”projects, it will not, however, be a question of erasing the slate, there will be no criminal treatment for those who have embezzled the funds. We gave them, however, a 10 or 15 year deadline to pay off their debts ”.

A Look At What ANSEJ Does

Algeria’s National Agency for Youth Employment Support ( Ansej ) is the country’s organization responsible for managing a credit fund for the creation of businesses. She participates in the public employment service .

Ansej is in charge of implementing a support system for business creation for people under 40 years of age. It manages a credit fund, granting loans at zero interest rate (0 rate loans), complementary to bank loans. Committees composed of representatives of banks and institutions grant the loans after examining the files of the promoters.

A bank guarantee fund supplements the financing instruments. Algeria ‘s Ansej advisors provide follow-up to promoters who have obtained a loan.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

To African ride-hailing startups, California’s new employment law is biting hard. No one expected Uber’s long tested business model, which was built on the basic principles of the gig economy, to change overnight, but this is happening. Under California ’s new law, nobody — drivers or gig workers — working for Uber or Lyft, or indeed any other freelance platforms now known or yet to be known, should simply be referred to, again, as an independent contractor. The new class for all of them— of course, subject to a three-pronged test — is “employees”; and this is a heavy word. Heavy because, going forward, Uber and other e-hailing companies, for instance, may be in their last throes of death defending their over $200 billion business from sinking into extinction not just in the US’ wealthiest state, but also in other states and countries inspired by California’s new path.

John Zimmer, Lyft’s president

What Is This California’s New Employment Law All About?

The quirkiest way of summarizing California’s new employment law is that it has reclassified, disrupted, removed and destroyed everything you know about the gig economy, such that if you decide to register with Uber as a driver, in say Lagos, Nigeria, for instance, you would no longer be seen as working independent of the e-hailing company, but as its employee; even though the car is yours and you command some influence on how you choose to do your work. And of course, as an employee, you’re entitled to daily or monthly wages or salaries, and are subject to Uber’s control and authority. But this is the most simplistic interpretation of the law.

In Details, Here Is What The New Law Fully States

The law, entitled Assembly B5, or simply AB5, has changed the criteria for being an independent contractor in California.

Now, for a company to classify a worker as an independent contractor, it must prove three things (you may hear this being called the “ABC Test”). If they can’t, then the worker is treated as an employee.

First, companies must prove that “the worker is free from the control and direction of the hiring entity in connection with the performance of the work.” In other words, companies can’t manage contractors the way they would employees. As an example, if a catering hall contracted a chef to prepare food events, but controlled how the chef prepared the food — giving them custom orders from customers, giving a strict schedule for production, and instituting standard procedures — they would likely not satisfy this part of the test.

Second, companies must prove that “the worker performs work that is outside the usual course of the hiring entity’s business.” This means that a company like Uber has to prove that driving users from location A to location B is outside the company’s usual course of business. Uber said as much in a press release, contending that the company is actually a “technology platform for several different types of digital marketplaces.”

Third, the companies must prove that “the worker is customarily engaged in an independently established trade, occupation, or business of the same nature as the work performed.” For example, an electrician doing contract electrical work is still a contractor. It’s unclear if ride sharing or meal delivery companies will be unable to clear this bar.

Consequently, under this new law, all of these independent contractors could earn employee status if the companies can’t satisfy the ABC test.

This is why Uber and Lyft, and others are fuming and have threatened to suspend all their operations till further notice, save for a timely reprieve from a court in California, which recently ruled that the word “independent contractors” still be tagged along with the drivers pending the determination of an appeal before it.

All the wailing ride-hailing companies know the implications of the law finally scaling through: Lyft, alone, has more than 300,000 drivers in California. Uber said in a recent blog post that its number of active drivers per quarter in California is about 209,000. Now, with the law in place, Uber and Lyft, and others are expected to cater to these drivers’ needs, as is expected of employers, including but not limited to granting them holiday and sick pay; overtime; health insurance; as well as other range of employment protection, benefits and their attendant tax implications. It would really be a serious reshaping of these companies’ finances.

One thing may likely save Uber and Lyft though: a ballot, known as Proposition 22, will be put up in November, at the same time as the US presidential election, inviting any eligible voter in California to vote, for or against, on whether Uber and Lyft be granted an exemption from the law.

Although Proposition 22 envisages some changes to give drivers minimum-wage standards, limited health benefits and flexibility, while maintaining the rideshare model, if voters disagree with it — especially as it is the labour groups that are pushing for Assembly B5 — Uber and Lyft, and other ride-hailing firms, may have to fold up — an option, not likely to be on the table as California, alone, accounts for about 16 percent of Lyft’s business, according to John Zimmer, Lyft’s president.

The companies may, alternatively, have to opt for other types of models. Already, plans are being mulled by Uber and Lyft to license their technology to those who want to operate fleets of ride-hailing cars in California, under a franchise model; but that, itself, may be too expensive. One analyst, Mr. Ives of Wedbush Securities has estimated that implementing any changes to the existing rideshare model would cost Uber $500 million a year and Lyft $200 million a year. This is even compounded by the fact that both companies have remained unprofitable, as per reports, and have also been gravely affected by lockdowns associated with the coronavirus pandemic.

Uber and Lyft drivers with Rideshare Drivers United and the Transport Workers Union of America conduct a cravan protest outside the California Labor Commissioner’s office in April. Mario Tama/Getty Images.

If Assembly B5 Finally Sails Through At The End Of The Day, It Could Have Domino Effects Across Jurisdictions

Although Bradley Tusk, president of Tusk Ventures and an early Uber investor, had told The Verge, late last year that “a domino effect [is] not just possible,” it’s beginning to look like his statement was poorly premeditated. There are already signs on the wall. Joining California Attorney General Xavier Becerra in his case against Uber and Lyft, which alleges that the ride-hailing companies have misclassified their drivers as contractors in violation of the new state law that went into effect this year, are city attorneys from San Francisco, Los Angeles and San Diego. Although these are major cities in the state of California, there are strong indications that the success of the case may send a strong signal to drivers in other US states — and across several other jurisdictions around the world, which have, until now, been looking for ways to muffle competition in an already saturated market . This may consequently necessitate major changes in their laws to accommodate their own peculiarities.

For one thing, the influence of California in the US and around the world cannot be overstated. Apart from the fact that the state is the largest of any US state — economy-wise — it is also the world’s fifth largest economy, behind Germany and ahead of India. The state is also home to “Silicon Valley” and some of the world’s most valuable companies such as Apple, Google, NetFlix, Twitter, Uber, and Facebook. A natural argument from the success of Assembly B5 at the end of the day would, therefore, be that if the tech-supported gig economy was inspired by the innovations brought about by Silicon Valley, it wouldn’t make much sense to continue to hold onto the traditional definition of the concept, when those who first laid its foundation have gone ahead to redefine it.

Although Uber and Lyft have argued that they are simply tech platforms and are not transportation businesses, the argument does not hold firm for all seasons. Uber, for example, has had to bend its operations in Germany and Spain to fit into the country’s transportation rules, which permit working with fleets, even though it is a tech platform. One thing needs to be pointed out here: although the Assembly B5 law does not apply to only rideshare business models, but to the entire gig economy, it seems, however, that the rideshare model would be the most affected given that it is often seen as being at the front lines of the economy.

“AB5 is riding two waves,” says Alex Rosenblat, a technology ethnographer and author of Uberland: How Algorithms are Rewriting the Rules of Work, to The Verve, “ a longstanding effort to restore workplace protections to misclassified workers; and it comes on the heels of the techlash.”

Rosenblat further argues that while the California law is about more than just Uber and Lyft, the drivers became the face of all workers exploited by giant tech companies. “That’s why AB5 is a symbolic and remarkable shift towards accountability, in labor and in tech,” she said.

On his part, Bradley Tusk adds that “ if the sharing-economy companies can’t radically reframe the narrative from ‘evil Silicon Valley powerhouse vs workers’ to ‘what this actually means for workers and consumers vs groups looking to profit from the changes,’ they’ll keep losing everywhere.”

Image for: Comparing Africa ‘s attempt to regulate Uber, others with the rest of the world. Source: — Daily Mail

How Does Assembly B5 Affect African Ride-sharing Startups?

There are already signs on the wall that California’s Assembly B5 law may be replicated in Africa. At least, governments of all major African countries and cities housing the continent’s gig economy ecosystems have spent the past five years caressing and testing their power to make laws that will severely touch tech startups wherever they may be located in the world. Lagos, Africa’s most valuable startup ecosystem, recently introduced a set of new regulations which will take off from August 27, 2020. The regulations, among other things, state that each e-hailing company must pay N8 million ($20.5k) per 1,000 cars as fresh licencing and renewal fees; that the companies will have comprehensive insurance for each driver while the driver is working with them; that a flat fee of N20 ($0.052) per trip, called a Road Improvement Fund, will be levied per trip.

Under South Africa’s National Land Transport Amendment Bill, which has been passed in parliament and sent to South Africa’s president for assent, drivers on car-hailing platforms like Uber and Bolt who do not have operating licences — not driving licenses — may incur a fine as much as R100 000 ($6000) for those platforms (Uber, Bolt and others), which would definitely be levied against the affected drivers directly or indirectly.

In Ghana, from Uber to Bolt to Yango, drivers who rely on ride-hailing to sustain their livelihoods would start paying a mandatory GHC 60 ($11) annual fee, in addition to their cars undergoing roadworthy tests every six months. Ghana’s Driver and Vehicle Licensing Authority (DVLA), which imposed the GH¢60 ($11) annual fee noted that the guidelines will cover the current ride-hailing platforms like Uber, Bolt, and Yango and will also cover companies who intend to operate ride-hailing platforms in Ghana in the future.

Therefore, it is only a matter of time before African governments’ regulatory attention reaches across to this spectrum. This reach would, however, be faster if California’s Assembly B5 beats naysayers at the polls on November 22, 2020.

When an issue assumes a political coloration, nothing is often guaranteed; especially as political interests, clad in sweeping powers, are almost always determined to push to protect majority interests rather than those of a few; majority interests, in this case, being the groaning drivers who command large voting powers; and the few being corporations and organisations whose barking powers are never anywhere near the ballot boxes.

Here is how the gig economy works. Source: UNNATI. Image for: Ride-hailing Uber California Africa. Ride-hailing Uber California African. Ride-hailing Uber California African. Ride-hailing Uber California African. Ride-hailing Uber California African. Ride-hailing Uber California African. Ride-hailing Uber California African

The Bottom Line

The best way to contain this impending disruption of the gig economy is to hear the gig workers out, in time, in the first place. As startups practising in the sector, never make their conditions so horrible that they begin to stick out their voices. It may be so overwhelming once everything converges to a head.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

For startups in Kenya, it appears government is finally attempting to change the status-quo. The newly launched National Information, Communications and Technology (ICT) Policy spells out a new set of policy guidelines intended to assist the East African country achieve its Vision 2030, which among many things, is anchored on helping Kenya attain the status of an industrialized information society as well as a knowledge-driven economy by 2030.

Joe Mucheru, Kenya’s Cabinet Secretary for Information, Communications & Technology

“This review of the Information and Communications Technology (ICT) Policy of March 2006 is inspired by, first, the need to align the Policy with the new constitutional dispensation in Kenya, and Vision 2030. This review specifically aims to incorporate the lessons learned from the Vision 2030,” Joe Mucheru, Kenya’s Cabinet Secretary for Information, Communications & Technology said in a statement.

“By providing local and international connectivity across the country and region, and developing in-country solutions, the Government will enable creation of online and digital jobs, markets, and quality skills allowing Kenyans to embrace the shared economy. In this way, citizens will transition from traditional ways of working to innovative, digitally enabled forms of work,” he added.

Below, we discuss how these policies would attempt to change the narrative for startups in Kenya.

A New 30% Equity Participation Rule In Favour Of Kenyans

Against the backdrop of increasing foreign participation in the Kenyan startup ecosystem, which has also seen more foreign-owned startups in Kenya funded than locally owned ones, the new ICT policy attempts to reserve 30% of ownership stake in every company registered to do ICT-related businesses in Kenya.

By the terms of the new rules, only companies with at least 30% substantive Kenyan ownership, whether corporate or individual, will be licensed to provide ICT services. In other words, foreign companies doing any ICT-related businesses in Kenya would have to give at least 30% of their ownership stakes to Kenyans. This applies immediately to foreign new comers to the Kenyan tech startup landscape. However, existing wholly-owned foreign ICT companies in the country will have until 3 years from now to meet the local equity ownership threshold. Once the three years (until 2023) expires, they may have to apply to Kenya’s Cabinet Secretary for Information, Communications & Technology for a one year extension with appropriate acceptable justifications.

To be sure that the 30% rule is not misunderstood, the rules further state that all ICT companies without majority Kenyan ownership will not be considered Kenyan. Consequently, they may not be calculated as part of the 30% Kenyan ownership calculus because they are not owned by Kenyans. Simply put, all foreign-owned ICT firms must, going forward, meet the 30% equity participation requirement.

For ICT companies listed or to be listed on the Nairobi Stock Exchange, their equity participation or distribution will be governed by the extant rules of the Capital Markets Authority of Kenya. This simply means that even though all foreign-owned startups in Kenya will have to comply with the new 30% rule, once they desire to do IPOs (Initial Public Offering) or list in any way in Kenya, the initial 30% rule will be jettisoned in favour of the prevailing rules of the Capital Markets Authority of Kenya.

Pension Funds In Kenya To Set Aside 5% Of Their Funds For Investment In Local Startup Ecosystem

This is a deal breaker, which if properly implemented, will unlock funding for startups in Kenya. By the new rules, pension funds in Kenya are encouraged to set aside 5% of their investments for the local ICT startup ecosystem. Although the language of this rule is not compelling, this will most definitely be the right push for pension funds in Kenya willing to invest in early startups.

However, it should be noted that, already Kenya has allowed private equity and venture capital firms to raise funds from pension schemes after amending the Retirements Benefits Authority (RBA) Act in 2015. Since then, this has allowed pension schemes to invest up to 10 per cent of their assets in private equity and venture capital firms (firms which, most times, invest in startups and SMEs). The new 5% rule under the new policy, however, will encourage pension funds to invest directly in startups or venture capital firms investing in early stage startups, out of the permitted 10%.

Nevertheless, it should be noted that even though the rules aim to encourage pension funds to invest in startups, under a proposed amendment to the Capital Markets Act (Cap 485A), Kenya’s Capital Markets Authority will, (once the bill is passed into law), be authorised to license, approve and regulate private equity and venture capital companies that have access to public funds. Analysts have criticized this amendment for duplicating responsibilities and multiplying the cost of running an investment firm in Kenya. For instance, Section 5(a) of Kenya’s Retirement Benefits Act already empowers the country’s Retirement Benefits Authority to regulate and supervise the establishment and management of retirement benefits schemes.

It is hoped, however, that the new 5% rule will encourage pension funds in Kenya (once valued at over KES1trn ($9.8bn), to invest in the country’s early-stage startups.

Apart from the 5% rule, there are other funding plans considered under the policy, such as a proposed “anchor fund” that will invest in qualifying Kenyan ventures for a proportionate equity consideration on a first-loss basis, thereby motivating co-funders to commit significant capital to qualified entities.

Also to be created is “a rotating venture capital fund” to be chaired by a person to be determined by the Cabinet Secretary for ICT with membership of a representative of the Kenya Sovereign Fund; the Kenya Private Sector Alliance; the CEOs of the three largest private sector pension funds at any one time; and four other members with ICT expertise as the Cabinet Secretary for ICT may from time to time determine

In as much as these are commendable, it is hoped that, like other promises and projects scattered across Africa, they are not abandoned or completely forgotten, a year from now.

Kenya ‘s ICT Policy will be a game changer given that startups founded by expats in the East African country get more funding than locals year-on-year. Source: AVCA

Increased Preference For Local Startups In Award Of Government Contracts

Kenyan startups aware of this opportunity need to show to relevant authorities the relevant portion of the new policy each time they bid for government contracts. By the terms of the new rules, government ICT procurement will now consider awards of tenders to tech startups to permit greater participation by emerging enterprises, and adopt home grown solutions. Consequently, the rules state that where there is a Kenyan solution that meets up to 70% of stated requirements, the Kenyan built solution will be accepted in preference to any other solution from anywhere else. In government defined priority areas, a 50% solution will be accepted in order to grow Kenyan capacity in those areas.

For owners of startups who are also young, this is a double advantage. Kenya’s Access to Government Procurement Opportunities (AGPO) presidential directive further guarantees that 30% of government business goes to youth and Persons-With-Disability-owned businesses. Under AGPO, all the startups need to do is to ensure that they are registered under the relevant government body and that at least seventy percent of their members are youth, women or persons with disabilities. Their leadership shall also be one hundred percent youth, women and persons with disability, as the case may be.

Encouragement Of Crowdfunding And Access To Innovation Grants And Funding

Startups in Kenya seem to have a go-ahead order to crowdfund. Under the new ICT policy, startups in Kenya are encouraged to crowdfund as well as build or participate in mentoring networks. This will be a major boost for a startup ecosystem still dependent foreign-owned venture capital firms.

There are other steps to make funding easily accessible to startups under the new policy, such as plans by government to encourage early Initial Public Offerings in the Growth Enterprise Market Segment (GEMS) of the Nairobi Stock Exchange as well as support for the growth of Permanent Listed Vehicles that build a bridge between investors and businesses that need investment to grow, but until these are executed, they remain inoperative wishes.

One other remarkable incentive under the new ICT policy is the rule that all innovation hubs and maker labs in Kenya will now be provided with grants to acquire additive manufacturing capabilities. The new rule also makes room for the protection of physibles (that is, data objects that are capable of being manufactured as a physical object using additive manufacturing processes) as intellectual property. Similarly protected is the physical realisation of physibles.

Again, all designated ICT incubation centres in each county in Kenya will now be duty free zones under the new rules. Initially also, the Kenyan government will establish 290 constituency innovation hubs which will provide work and maker spaces for the host local community.

Another incentive introduced by the policy is research grant. To that effect, the policy states that every two years, the Kenyan Government will set five (5) research priority areas and provide funding to private enterprises in the form of research grants, equipment purchase grants in the priority areas.

The Bottom Line

The new ICT policy is going to be game-changing for startups in Kenya, especially as it relates to funding available to them. For instance, according to Roble Musse in his book “Un-Silicon Valley,” 70 percent of startups in Kenya that received a million dollars or more of Venture Capital (VC) investment in 2018 were led by white expatriate founders. This is notwithstanding the fact that the expatriate community in that country make up only 0.15 percent of the population. Nevertheless, while the new rules will entirely alter the startup landscape in Kenya if fully implemented, the ball is in the yard of Kenyan entrepreneurs to play. One thing is, however, clear in all these: you can lead a horse to water but you can’t force it to drink.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

It looks like Ghana is highly uncertain about what it wants from Nigerian businessmen: outright ban on foreign retailing or simply taxes? After series of agitations against the presence of Nigerian retailers in the country last year, the West African country of Ghana is back again with a new demand, in the middle of the coronavirus pandemic. According to the Ghanaian Ministry of Trades, Nigerian traders must pay the required taxes and other fees imposed on them by the authorities. The ministry has equally rejected claims of unfair treatment to Nigerian traders in the country during the enforcement of the Ghana Investment Promotion Council regulations.

President of Nigerian Traders Union Ghana, Chukwuemeka Nnaji,

“Most of our members do not have the GIPC registration, because it requires one million dollars cash or equity and they gave us 14 days within which to regularise,’’ the President of Nigerian Traders Union in Ghana, Chukwuemeka Nnaji, was quoted as saying by News Agency of Nigeria.

“As of Thursday, they had moved to another area and started locking up shops of Nigerian traders. Nigerian life in Ghana matters. This is livelihood of Nigerians being destroyed by Ghanaian authorities. This is not being perpetrated by a trade union, but Ghanaian authorities,” he added.

“They also demanded that we must employ a minimum of 25 skilled Ghanaian workers and must not trade in commodities that Ghanaian traders have applied to trade in.The humiliation of Nigerians is getting out of hand. We are calling on the Nigerian government to come to our aid. We have legally registered our businesses and we pay taxes,” he said.

Here Is What You Need To Know

The latest development is happening despite the intervention of the presidents of Ghana and Nigeria through the Economic Community of West African States.

In one video on social media, a Nigerian trader whose shop was forcefully locked up by the Ghanaian security officials was asked to pay the $1 million registration fee.

The victim had shown the officials his business registration certificate and other documents but the enforcement team was adamant as they insisted on shutting his premises.

Covered by local radio station, Starrfm, the Head of Communications, Ministry of Trade, Prince Boakye Boateng, said Nigerian traders had failed to honour an ultimatum to meet the requirements.

“It cannot be we’ve been insensitive; if that is what they’re saying, I’ll be disappointed because I’ll rather say they have rather been unfair to us as a regulatory body because we have given them more time than enough to the extent even the Ghanaians thought that the ministry was not even on their side or the ministry wasn’t ready to even enforce the law,” he was quoted as saying.

He recalled that the shops were locked last December and later re-opened following the intervention of President Nana Akufo-Ado.

According to him, the traders complied but have not regularised their documents for verification.

Ban On Foreign Retail Trading Or Simply Taxes?

Last year November, Ghana Union Traders Association (GUTA) demanded the total closure of all retail shops belonging to foreigners, with claims that the government had not fulfilled its promise of ridding the market of such traders despite several appeals. GUTA dared foreign traders whose retail shops had been closed to sue them if they felt they were being treated unfairly.

According to them, the activities of the foreigners breach Section 27(1) of the Ghana Investment Promotion Centre’s Act (Act 865).

Citing the closure of the Nigerian border to protect its country from the smuggling of goods into their country, the Association, then, said they would not tolerate the foreigners anymore, and demanded that their shops be closed down.

The latest move is the first ever public backing of the raids on foreign-owned businesses by government since the agitations started.

A Look At The Controversial Section 27(1) of Ghana’s Investment Promotion Act

According to Section 27 (1) of the GIPC Act, a person who is not a citizen or an enterprise which is not wholly-owned by a citizen shall not invest or participate in the sale of goods or provision of services in a market, petty trading or hawking or selling of goods in a stall at any place. The list of prohibited trading activities are:

The sale of goods or provision of services in a market, petty trading or hawking or selling of goods in a stall at any place;

The operation of taxi or car hire service in an enterprise that has a fleet of less than twenty-five vehicles;

The operation of a beauty salon or a barbershop;

The printing of recharge scratch cards for the use of subscribers of telecommunication services;

The production of exercise books and other basic stationery; f. the retail of finished pharmaceutical products;

The production, supply, and retail of sachet water;

All aspects of pool betting business and lotteries, except football pool.

Consequently, enterprises eligible for foreign participation and minimum foreign capital requirement are as follows:

A person who is not a citizen may participate in an enterprise other than an enterprise specified in section 27 if that person

In the case of a joint enterprise with a partner who is a citizen, invests a foreign capital of not less than two hundred thousand United States dollars in cash or capital goods relevant to the investment or a combination of both by way of equity participation and

The partner who is a citizen does not have less than ten percent equity participation in the joint enterprise; or

Where the enterprise is wholly owned by that person, invests a foreign capital of not less than five hundred thousand United States dollars in cash or capital goods relevant to the investment or a combination of both by way of equity capital in the enterprise.

A person who is not a citizen may engage in a trading enterprise if that person invests in the enterprise, not less than one million United States dollars in cash or goods and services relevant to the investments.

For the purpose of this section, “trading” includes the purchasing and selling of imported goods and services.

An enterprise referred to shall employ at least twenty skilled Ghanaians.

How Did The Taxes Come In?

By Ghanaian law (the GIPC Act), all enterprises in Ghana with foreign participation are required to register with the Ghana Investment Promotion Centre (GIPC). Under the new GIPC Act, 2013 (Act 865), the minimum capital required for retail business has moved from US$300,000 to $1 million, while foreign investors who participate in joint venture enterprises have to show a minimum capital of $200,000 with wholly owned foreign enterprises showing a minimum capital of $500,000.

It seems clear enough that the GIPC Act states that a foreigner may engage in a trading enterprise in Ghana if that person invests in the enterprise, not less than one million United States dollars in cash or goods and services relevant to the investments. This, in no way, means direct taxes to the GIPC unless it is clearly stated under the GIPC Act. The Act does not, also, specifically mention Nigerians as being the only foreigners targeted.

These moves by the Ghanaian government may not been unconnected with the border closure tussle with its neighbouring Nigeria, which had, prior to the outbreak of the coronavirus, shut its land borders with Ghana.

Greater Accra Regional Secretary of GUTA, David Kwadwo Amoateng had on an Adom FM’s morning show, last year, said the Nigerian government had not been fair to foreign traders by closing the land borders.

In return, he expected the Ghana government to prevent Nigerian traders from bringing goods into Ghana, but that plea, he said, had fallen on deaf ears.

“Either somebody’s bread has been buttered or we are cowards. Government is not being fair to us,” he fumed.

“Let’s boycott Nigerian products as payback to their government’s action. How can we be slaves in our own country?” he added.

Mr Amoateng cited how Dangote cement, owned by Nigeria’s and Africa’s richest man, Aliko Dangote, had taken over the market while local ones, from GHACEM to others, are suffering.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Foreign companies in Kenya eyeing to do business in the country’s lucrative ICT sector will have to surrender 30 per cent shareholding to Kenyans. This is according to the National Information Communications and Technology Policy Guidelines 2020, published last week, that spell out new regulatory obligations by companies and individuals working in the ICT sector.

“The government strongly encourages Kenyans to participate in the ICT and science and technology sector through equity participation,” states the regulatory policy published last week by the ICT Ministry.

“It is the policy that only companies with at least 30 per cent substantive Kenyan ownership, either corporate or individual, will be licensed to provide ICT services.”

Here Is What You Need To Know

The move is likely to raise eyebrows among companies looking to make an entry into the country’s growing and lucrative ICT sector. It is also likely to increase compliance requirements for foreign firms bidding for long-term State tenders in the ICT sector.

“For purposes of this rule, companies without majority Kenyan ownership will not be considered Kenyan, and may thus not be calculated as part of the 30 per cent Kenyan ownership calculus,” the document reads in part.

In the recent past, dozens of companies have set up shop in Kenya, with the country appearing among the top three in Africa in terms of start-up investment.

According to investment platform Partech, which tracks equity deals in African start-ups, last year, Kenya recorded Sh5.6 billion worth of investments, emerging second in total funding and number of transactions in Africa.

The ICT policy further says foreign companies will be given three years to meet the local equity ownership threshold, and may apply to the CS for a one-year extension with appropriate acceptable justifications.

“For listed companies, the equity participation rules will conform to then extant rules of the Capital Markets Authority,” explains the policy.

The policy appears to respond to recent queries raised over the high number of tech start-ups locally with foreign boards of directors and management.

The policy, however, does not specify if the rules will apply to new foreign ICT companies making their entry into Kenya, or those already in existence.

Under the new regulations the government will also introduce a new licensing and registration regime where companies are given temporary licences that are later withdrawn if they fail to make commercial success.

“This will take the form of rules that allow companies to be licenced for certain services and only pay for the licence when they commence operations or achieve benchmark goals within predefined time frames,” explains the policy.

The State anticipates the policy will create 20 Kenyan multi-national ICT companies, 300 mid-sized firms, 5,000 small and medium enterprises and 20,000 startups.

This is expected to increase the number of startups through easing their barrier to entry. The policy also proposes a government venture capital fund that will invest in start-ups for a portion of the equity on a first-loss basis in case the startup fails.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer