Algeria’s government, aiming to ease the impact of the coronavirus lockdown on state and private firms, will freeze the payment of taxes, the finance ministry said on Monday. Algeria’s government, aiming to ease the impact of the coronavirus lockdown on state and private firms, will freeze the payment of taxes, according to the country’s finance ministry.

“Those measures aim to alleviate the repercussions of the health crisis and ensure the revival and preservation (of firms’) activities,” the finance ministry said in a statement.

Here Is What You Need To Know

The move, which comes amid growing pressure on state finances due to a drop in energy earnings, follows a decision earlier this year to suspend the implementation of penalties on companies for delays in carrying out projects.

The government has also approved a measure to defer or reschedule loan payments for firms suffering losses due to restrictions meant to limit the spread of the pandemic.

OPEC member Algeria’s economy has been significantly hit because of a fall in global crude oil prices since the coronavirus outbreak which pushed down demand on international markets.

Oil and gas account for 60% of the state budget and 93% of total export revenue as the authorities have failed for now to diversify the economy away from energy.

Lockdowns aimed at reining in infections have further affected production in the North African nation of 45 million people.

The economy contracted 3.9% in the first quarter of 2020 compared with a 1.3% growth in the same period last year, according to official data.

But that situation has not prevented the government from taking steps to help firms with the aim of maintaining output and jobs mainly in the non-energy sector.

Source: Reuters

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

No more parallel exchange rate in Zimbabwe as a new set of regulations have been approved to compel businesses in the country to use a single exchange rate for pricing goods and services as the country seeks to control surging costs.

John Mangudya, governor, central bank of Zimbabwe

“Any person who provides goods or services in Zimbabwe shall display, quote or offer the price for such goods or services in both Zimbabwe dollar and foreign currency at the ruling exchange rate,” the government said in gazette on Friday.

Here Is What You Need To Know

Anybody who fails to comply with the new regulations will face fines.

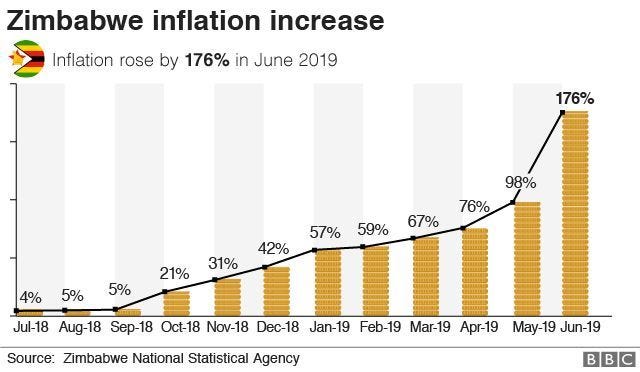

The Zimbabwe dollar has weakened to 72.14 per U.S. dollar on its new foreign currency auction system after a currency peg of 25 was dropped last month. Rates on the parallel market are weaker in the southern African nation, where inflation has climbed to 737% and food and fuel are in short supply.

John Mangudya, the central bank governor, has previously said some businesses were using parallel exchange rates of as much as 100 per U.S. dollar when pricing goods and services, even after getting foreign exchange through the weekly auction.

On June 26, government announced the suspension of transactions on phone-based mobile money platforms and suspended trading on ZSE as part of a series of “prudent and coordinated interventions to deal with malpractices, criminality and economic sabotage” amid allegations the platforms were fueling the rout of the local currency.

Government spokesperson Nick Mangwana alleged there were “fake counters” on ZSE which are epitomized by the Old Mutual Implied Exchange rate (OMIR).

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

There is hope for startups in the West African country of Guinea. The country’s ministers in charge of Higher Education, Posts, Telecommunications and Investments have made a joint communication on digital transformation and the capacity for innovation of the public and private sectors in the country, part of which is that the country would soon formulate a comprehensive policy (Startup Act, possibly?) that would create labels for startups as well as support them.

“Industrial revolutions are always marked by structural changes which generate big winners and big losers. Current changes are already disrupting the classic world economic order following new economic models, which arise from disruptive technologies such as “uberization”, artificial intelligence, the sharing economy, massive data processing, digital financial inclusion, e-commerce, social networks, etc…Guinea is condemned to innovate if it does not wish to continue in underdevelopment,” the ministers said in a joint communique.

Here Is What You Need To Know

According to the ministers, the challenge for Guinea is to move from the position of a simple consumer to that of an actor capable of producing goods and services (machines, applications and content) and to improve its capacity to innovate to accelerate transformation. digital economy.

Consequently, the ministers proposed to create an incentive policy through the creation and promotion of startups, label them and support them, promote innovative private investments particularly in the modernization of their administration and to adopt a law, as well as hold the Transform-Africa Summit on digital technology in Guinea.

Created to take charge of ensuring the implementation of this is an enlarged inter-ministerial technical committee that will harmonize and coordinate government actions in the field of innovation. The work of this committee would lead to the development of a national innovation strategy by involving representatives of civil society.

Priorities, according to the ministers, would be given to sectors with high potential, which include: agriculture, mobility, health, electronic and mobile commerce and electronic payment and mobile.

Generally, the ministers called for the adoption of a policy to promote innovation.

This policy, according to them, could be structured around the following three axes:The definition of project selection criteria by priority sector; The strategic reorientation of public investments; Promotion of the private sector to make it the engine of innovation.

They underlined that for reasons of efficiency and economic pragmatism, the innovation promotion policy must define priority sectors in which it would be more relevant to concentrate investments because of their economic or social importance and the capacity to reach them.

The Ministers indicated that Guinea still has the possibility of being a technological relay country. The objective is to make the national territory a technological oasis of the sub-region by promoting the emergence of hubs and an ecosystem that creates innovation in agriculture, health, education, transport, electronic commerce and electronic banking.

Given the importance of digital issues, they further recommended the establishment of an innovation working group representative of the ecosystem.

Guinea is richly endowed with minerals, possessing an estimated quarter of the world’s proven reserves of bauxite, more than 1.8 billion metric tons (2.0 billion short tons) of high-grade iron ore, significant diamond and gold deposits, and undetermined quantities of uranium.

The proposed policy would have the effect of adding Guinea to the list of African countries with favorable legal frameworks for their startups.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer.

Startups in Tunisia can now legally raise funds through crowdfunding, courtesy of a new crowdfunding law. With a majority 127 votes to no opposition or abstention, the country’s parliament, the Assembly of the Representatives of the People (ARP), has finally passed the bill on crowdfunding into law. The law was on January 31st 2020, sent in to the parliament by the country’s Council of Ministers for final adoption. The implication of this adoption is therefore that the bill has finally become law, and is now available to the country’s startups to utilise.

Iadh Elloumi, chairman of the finance, planning and development committee

“This law will solve some of the economic problems that the country is going through, by introducing new means of financing projects,” said Iadh Elloumi, chairman of the finance, planning and development committee, at the end of the plenary meeting.

Here Is What You Need To Know

Members of parliament voted for the law, which has 65 articles, in its entirety.

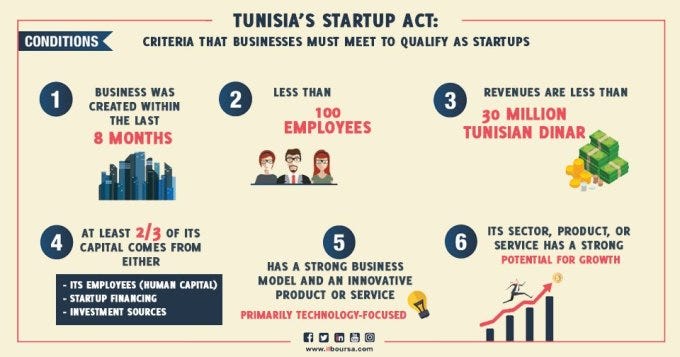

Tagged bill n ° 26 of the year 2020, the new crowdfunding law aims to organize the activity of crowdfunding in order to provide the necessary financing for projects and companies in order to stimulate investment.

The finance, planning and development committee under the ARP, the BCT and the CMF have however agreed to set up a funding control mechanism in order to fight against suspicious funding which the new law would occasion.

According to the Tunisian Minister of Industry and SMEs, Slim Feriani, early February 2020, the new law is a new mechanism for alternative financing for startups in Tunisia. He said the law meets international standards and can support investment.

‘‘Despite the financial facilities granted by the State to SMEs to cover their financial needs, the SMEs often encounter enormous difficulties in accessing finance, which hinders their development and threatens their sustainability,’’ he said.

The two types of crowdfunding under the law are equity crowdfunding which will help finance the capital of startups and innovative projects lacking equity; and one which is based on the granting of loans.

Funding through donations was also added to the crowdfunding law before final adoption by Tunisia ‘s parliament.

Slim Feriani also highlighted the role of the Tunisian Agency for the Promotion of Industry and Innovation (APII) which, in coordination with the European Union, had helped to set up the new mechanism in the spirit of improving the Tunisian business climate and by the way of also improving Tunisia’s ranking on the World Bank Ease of Doing business index.

The Global Crowdfunding market was valued at 10.2 billion USD in 2018 and is expected to reach 28.8 billion USD by the end of 2025, growing at a CAGR of 16% between 2018 and 2025.

Tunisia ‘s new crowdfunding law will encourage the country’s nascent startup ecosystem. Source:-Company.com

Crowdfunding refers to raising money from the public (who collectively form the “crowd”) primarily through online forums and social media.

Crowdfunding models include: Donation-based crowdfunding (in which donors are not typically granted anything in return for their donation)

Rewards-based crowdfunding (in which backers contribute funds in exchange for some reward–in many cases the item produced by the campaign)

Equity crowdfunding (Equity crowdfunding refers to raising money from small public investors (who collectively form the “crowd”) primarily through online forums and social media. In exchange for relatively small amounts of cash, investors get a proportionate slice of equity in a business venture).

Debt/lending crowdfunding (in which lenders provide money and expect their loan to be paid back with interest).

Crowdfunding means, according to the said law, a financing formula based on the collection of funds from the public, through a platform on the Internet, reserved for this purpose, in order to finance projects and companies.

The interventions of the deputies revolved around the scope of the said law, given that it represents one of the financing tools for small and medium-sized enterprises.

It should be noted that crowdfunding is considered to be a new mechanism for the development of investment and the creation of businesses. This law comes after the adoption of the bill on the solidarity and social economy.

As a reminder, this committee held hearing sessions with the Minister of Industry and SMEs and representatives of the BCT and the CMF, to examine the bill made up of 65 articles after having been 56 articles during its presentation.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer.

Going forward, if a Bill pending before Kenya ’s national parliament is passed into law, business will not be as usual for all digital lenders in the East African country. Not only would they have to play under the same rules as commercial banks, including having to seek the country’s central bank’s approval for new products and pricing, the amount they each charge their customers as monthly interest rates on borrowed facilities would now also be regulated.

“The principal objective of this Bill is to amend the Central Bank of Kenya Act to regulate the conduct of providers of digital financial products and services,” says a notice on the Bill.

“The Central Bank of Kenya will have an obligation of ensuring that there is fair and non-discriminatory marketplace access to credit.”

Here Is What You Need To Know

By the terms of the Central Bank of Kenya (Amendment) Bill 2020, the Central Bank of Kenya must approve every increase in digital lenders rates and other loan charges. Interests on non-performing loans must also, if the bill is passed into law, not be more than twice the defaulted credit.

This is the first major attempt by Kenya to regulate all digital financial services startups and companies operating in the country.

In a statement, late April, 2020, CBK explained that the ban is in response to numerous public complaints about misuse of the Credit Information Sharing System (CIS) by the above-mentioned lenders and particularly poor response to customer response.

In March this year, Kenyan Parliament also considered a petition to launch investigations into the operations of digital money lending institutions over claims of exploitation of borrowers.

The Implications Of The Proposed Law On Digital Financial Services Startups In Kenya

Implied Lifting Of The Ban On Credit Lending Startups

Once the new law is passed into law, its first implication would be to terminate the ban on credit lending startups in Kenya as regards submitting credit information on their borrowers to Credit Reference Bureaus (CRBs). Thus, with a renewed power to report customers for blacklisting to the country’s central credit information sharing center, it is only safe to say that the risks associated with their business model have become, once again, more manageable.

Licensing of Digital Financial Services Companies/Startups

Another direct implication of the proposed new law on digital financial services startups in Kenya is that the Central Bank of Kenya will now possess recognized power under the law to issue operational licenses to startups desiring to provide services related to a digital financial product, financial product advice, market, administrative or management services or credit under a regulated credit contract in Kenya.

What this means is that startups that offer digital banking services will now also have to maintain a minimum authorized capital of five billion shillings ($46.4 million), which may be increased by such amount as shall be determined by CBK, unless the contrary is stated by the CBK.

In other words, all the rules regulating commercial banks and other financial institutions will now have to apply to startups offering digital financial services if the bill becomes law.

The Bill is coming amid complaints that digital lenders do not provide full information to borrowers on pricing, punishment for defaults and recovery of unpaid loans.

Digital lenders have also been accused of abusing personal information collected from defaulters’ mobile phone contacts list to bombard relatives and friends with messages regarding the default and asking third parties to enforce repayment.

FinTech covers all areas of human interaction with commodity-money circulation and uses a large class of IT technologies. Source: — Aspilos.com

Regulation of Interest Rates Charged Users Of Digital Lending Services

Even though digital lenders in Kenya may still be allowed to lend, the law would however, if passed into law, see that they do not charge interests on their loans excessively. This is because the CBK could now determine the maximum rate of interest they charge their customers.

The latest move to control the activities of digital lenders follows the removal of legal cap on commercial lending rates by the Central Bank of Kenya in March 2020. The cap, established far back in 2016, which set interest rates chargeable by banks at 4%, was intended to address the issue of the affordability of credit for small enterprises and working people, as they had complained for years that high interest rates had locked them out of accessing credit.

Its removal in March this year has, however, resulted in the proliferation of digital lenders, who seek to take advantage of the business opportunities it offered. For instance, Tala, Branch, which are among top players in the mobile digital lending market in the country, offer interest rates of 152.4 percent and 132 percent per year respectively.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer.

It is now becoming clearer that Ecocash, a mobile banking solution which holds about 97% of the country’s mobile banking market share and which is owned by the country’s dominant telecom company Econet Wireless Ltd might have been the target of the recent ban by the Zimbabwean government on mobile banking. Police in the Southern African nation have accused Econet Wireless Ltd., of money laundering, demanding a list of its subscribers and issuing a search warrant against it.

RBZ governor John Mangudya,

“In accordance with the provisions of the National Payment Systems Act [Chapter 24:23] and the Banking (Money Transmission, Mobile Banking and Mobile Money Interoperability) Regulations, Statutory Instrument 80 of 2020 (the Regulations), the Reserve Bank of Zimbabwe (the Bank) wishes to advise the public that it has designated Zimswitch as a national payment switch with immediate effect,” RBZ governor John Mangudya, had earlier announced in a statement in July.

“All mobile money transmission providers and mobile banking providers are hereby directed to be connected to Zimswitch as provided for by section 4 of the Regulations.”

Here Is What You Need To Know

This is the latest of the clash between the government and Econet whose money transfer service, Ecocash, facilitates more than 97% of transactions in the southern African country. Zimbabwe government says the activities of the mobile banking service are contributing to the rapid depreciation of the national currency.

In an order against the company, the police accused the company of creating fictitious mobile money, converting it to cash and then buying foreign currency on the black market before sending it out the country.

On June 26 the country banned most of those transactions and has now said it plans to force Econet’s Ecocash unit to use a government-run money-transfer platform. While Econet competes with state-owned companies, its market share dwarves theirs.

GDP of Zimbabwe

Switch To A “National Mobile Banking Grid” Or Cease To Exist

According to governor John Mangudya, “To ensure seamless integration, all money transmission providers and mobile money providers must complete the necessary installation or deployment or commissioning of infrastructure and connection protocols, credentials and documentation for connection to Zimswitch by no later than 15 August 2020.”

Zimbabweans have been using social media to question if Zimswitch is not another scam meant to benefit the elite.

A quick check on the Zimswitch website gave the following results:

Zimswitch is the National Electronic Funds Switch for ATM’s and POS of Zimbabwe that serves not only the financial institutions who are its members and users but also provides an essential service to their customers; the Zimbabwean public. Zimswitch is also the oldest and most successful national switch in Africa outside of South Africa.

Zimswitch was formed upon the signing of a partnership agreement of 8 local financial institutions dated 7 March 1994, to facilitate the shared use of automated teller machines (ATM’s) and point of sale (POS) facilities throughout Zimbabwe. • On the 31 March 2001 Zimswitch converted to a private company, incorporated in Zimbabwe. A newly formed company, Zveringa Systems (Private) Limited, was purchased for this purpose. This conversion to a company was undertaken both to enable faster decision making and to allow for the introduction of a business partner. • In February 2002, after an extensive evaluation, the partners awarded the business to Fintech — the technology arm of the Loita group at the time, represented in Zimbabwe by the Loita Company, EFTCorp. The In 2002 the replacement of the existing proprietary technology with the new version of an EFT solutions platform called Postilion was undertaken. This platform enables growth and development of the business as required to meet the new challenges. EFT Corp also provides the necessary consultancy, services and ongoing support to Zimswitch in respect of the EFT software. Zimswitch is 100% operated by LXS and majority owned.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer.

It appears, Kenyans are saying, that SportPesa, the Kenyan sport betting company, was frustrated out of market with a hike in gambling tax rates from 7.5 to 35 percent in order to make way for other external replacements. The Football Kenya Federation (FKF) President Nick Mwendwa has just announced that Betking, a Nigerian betting firm, had struck a deal with the federation.

Football Kenya Federation (FKF) President Nick Mwendwa

Here Is What You Need To Know

By the terms of the new deal, the Nigerian company agreed to offer KSh 1.2 billion ($11 million) sponsorship to Kenya premier league clubs for a period of five years. The announcement by the Kenya Football Kenya Federation (FKF) President Nick Mwendwa that Betking, a Nigerian betting firm, had signed a KSh 1.2 billion sponsorship deal for the local league raised eyebrows and instantly sparked rage on social media.

Tuko Media reported that disgruntled Kenyans trooped to social media pages to express anger and bitterness following entry of a foreign betting firm months after a homegrown company was banned.

Both Sportpesa and Betin stopped doing business in the country due to what they saw as a hostile tax environment.

The government in Nairobi hiked gambling tax rates from 7.5 to 35 percent.

Although a Kenyan High Court initially blocked collection of the tax, the Kenyan Revenue Authority and Betting Control and Licensing Board agreed on 1 July, 2019 to withdraw the licences of 27 companies who failed to pay the levy, including SportPesa and Betin.

After, the Kenyan government ordered telecoms company Safaricom to block banking services to the 27 companies, leaving customers unable to deposit funds — a move SportPesa said violated a court order — SportPesa ended its sport sponsorships in Kenya and placed its 453 employees in the company on leave.

A SportPesa spokesperson told iGamingBusiness.com in early September, 2019 that the company believed it was heading towards the resumption of normal operations after constructive talks. However, on 19 September, the Kenyan Parliament’s Finance Committee proposed a new 20% excise tax rate on betting stakes in the 2019/20 budget, an increase from the 10% stake proposed by the treasury in June.

In response, SportPesa said that it would not operate in the country until the rate was changed, and laid off its Kenya-based employees.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer.

The Zimbabwe Stock Exchange (ZSE) will resume the trading of shares next week minus three fungible securities, nearly a month after the local bourse was forced to suspend trades on allegations of speculative trading which resulted in the devaluation of the local currency.

Zanu-PF acting spokesperson Patrick Chinamasa

The three fungible securities that will not be allowed to trade are Old Mutual, PPC and Seed Co International which will have to trade on a to-be established foreign currency exchange, according to people familiar with the developments. The trio’s fungibility was suspended for a year in March.

“All is set for the resumption of trading. There are meetings underway to work out modalities on how the fungible shares will be traded on a foreign currency exchange,” a source said.

Here Is What You Need To Know

Modalities on how the trades in the fungible securities will work are being worked out with a series of meetings being held this week, sources told Business Times.

On June 26, the government announced the suspension of transactions on phone-based mobile money platforms and suspended trading on ZSE as part of a series of “prudent and coordinated interventions to deal with malpractices, criminality and economic sabotage” amid allegations the platforms were fuelling the rout of the local currency.

Government spokesperson Nick Mangwana alleged there were “fake counters” on ZSE which are epitomised by the Old Mutual Implied Exchange rate (OMIR).

Business Times heard yesterday that a series of meetings were held this week where it was resolved that trading resumes on Monday.

The resumption of trading comes after the ruling Zanu-PF proposed the delisting of Old Mutual from the bourse and allow the counter to Zanu-PF acting spokesperson Patrick Chinamasa said fungibility has created an opportunity for the determination of foreign exchange rate in Zimbabwe to be determined from activities emanating from actions of speculators operating on the stock exchange.

Source — businesstimes

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer.

Efforts by governments of the East African region to hasten the economic integration of the region had an added boost with the setting up of a one-stop border post between Tanzania and Kenya, two of East Africa’s biggest economies. This will help eliminate the hindrances to trade among both countries. The One-Stop Border Post project is also advancing regional cooperation, facilitating cross-border dialogue and the signing of treaties between EAC member countries. It supports the ongoing work of the Facilitation of Cross-Border Movements Committee, set up in 1998 by the EAC Commission to address passports, travel documents for business people, visas and other matters identified in the Tripartite Agreement on Road Transport.

The land border between these two East African countries now has just a single border post. This project, the One-Stop Border Post, was set up at Namanga, a town of 16,000 inhabitants that straddles Longido District in Tanzania and Kenya’s Kajiado County in Kenya. By cutting the crossing time to a maximum of half an hour, the One-Stop Border Post project has boosted trade and tourism between Kenya and Tanzania. To set up the border post, the African Development Bank in 2007 approved $185 million in funding, of which $108 million went to Kenya and $77 million to Tanzania. The Bank co-financed the project with Japan International Cooperation Agency. The development has boosted the regional economy by streamlining, along with improved roads, the movement of people and goods across the border. According to Kenneth Bagamuhunda, Director-General, Customs and Trade of the East African Community (EAC), “The idea now is to reproduce this initiative on other borders, such as that with Ethiopia, the Democratic Republic of the Congo and Zambia.”

One driver who has been plying that route for over 20 years said that “Customs clearance used to be a real challenge here, because there were two borders. You had to go through at the Tanzanian immigration office, and then repeat the exercise on the Kenyan side. It used to take between one and a half and two hours,” he said, smiling. “That’s all changed now. When passengers arrive, it doesn’t matter which side they come from, a single checkpoint does all the administration and they are able to carry on across the border.”

“Thanks to the new crossing point, road traffic has increased,” said Edward Wilson Lyimo, the owner for more than 20 years of a hotel on the Tanzanian side of Namanga. “Businesses have become profitable and this new crossing has really helped us. Now, we can do business in both countries.”

The African Development Bank is working to support regional integration, cross-border trade, tourism, the socioeconomic development of the region and poverty reduction.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

On Wednesday, July 8, 2020, the Reserve Bank of Zimbabwe announced that it has designated Zimswitch as a national payment switch with immediate effect. According to the statement, all mobile money transmission providers and mobile banking providers were directed to be connected to Zimswitch.

RBZ governor John Mangudya

“In accordance with the provisions of the National Payment Systems Act [Chapter 24:23] and the Banking (Money Transmission, Mobile Banking and Mobile Money Interoperability) Regulations, Statutory Instrument 80 of 2020 (the Regulations), the Reserve Bank of Zimbabwe (the Bank) wishes to advise the public that it has designated Zimswitch as a national payment switch with immediate effect,” said RBZ governor John Mangudya, in a statement on Thursday.

“All mobile money transmission providers and mobile banking providers are hereby directed to be connected to Zimswitch as provided for by section 4 of the Regulations.”

According to governor John Mangudya, “To ensure seamless integration, all money transmission providers and mobile money providers must complete the necessary installation or deployment or commissioning of infrastructure and connection protocols, credentials and documentation for connection to Zimswitch by no later than 15 August 2020.”

Zimbabweans have been using social media to question if Zimswitch is not another scam meant to benefit the elite.

A quick check on the Zimswitch website gave the following results:

Zimswitch is the National Electronic Funds Switch for ATM’s and POS of Zimbabwe that serves not only the financial institutions who are its members and users but also provides an essential service to their customers; the Zimbabwean public. Zimswitch is also the oldest and most successful national switch in Africa outside of South Africa.

Zimswitch was formed upon the signing of a partnership agreement of 8 local financial institutions dated 7 March 1994, to facilitate the shared use of automated teller machines (ATM’s) and point of sale (POS) facilities throughout Zimbabwe. • On the 31 March 2001 Zimswitch converted to a private company, incorporated in Zimbabwe. A newly formed company, Zveringa Systems (Private) Limited, was purchased for this purpose. This conversion to a company was undertaken both to enable faster decision making and to allow for the introduction of a business partner. • In February 2002, after an extensive evaluation, the partners awarded the business to Fintech — the technology arm of the Loita group at the time, represented in Zimbabwe by the Loita Company, EFTCorp. The In 2002 the replacement of the existing proprietary technology with the new version of an EFT solutions platform called Postilion was undertaken. This platform enables growth and development of the business as required to meet the new challenges. EFT Corp also provides the necessary consultancy, services and ongoing support to Zimswitch in respect of the EFT software. Zimswitch is 100% operated by LXS and majority owned.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer