The Ethiopian Communications Authority has commenced three consultations on the process for licensing entrants to the country’s liberalised telecoms market.

Having opened (28th April), the consultations will run till 11th May, with the regulator also set to disclose draft frameworks relating to consumer rights and disputes. Stakeholders will be able to offer their feedback on the length of the licences and the method for determining successful applicants.

The ECA will also issue documents relating to the provision of fixed and mobile service. These will provide recommendations on infrastructure sharing, interconnection, service quality and universal access obligations.

In 2019, the regulator held consultations on its proposed liberalisation of Ethiopia’s telecoms sector. It had scheduled the issue of two licences for Q1 2020 and floated the possibility of private firms investing in the state-owned Ethio Telecom.

While these plans have been delayed by the ongoing pandemic, the regulator is evidently keen to press ahead with them. Several groups with a strong footprint in Africa have stated their interest in the Ethiopian market, including Econet Global, MTN, Orange, Safaricom and Vodacom.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

Startup Genome shows how many startups are in trouble.

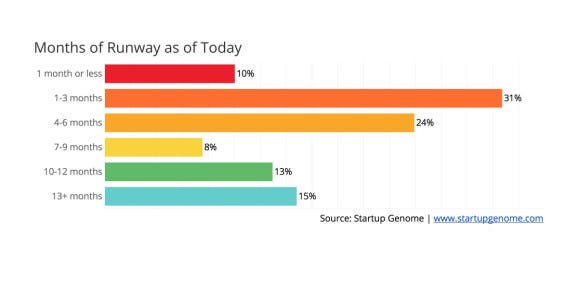

Startup Genome has reported that 41% of global startups have less than three months’ worth of cash available. That’s one of the grim statistics of the pandemic, and it suggests the startup ecosystem is fragile.

Startup Genome CEO J.F. Gauthier

The report was based on a survey conducted by the Startup Genome, which interviewed 1,070 respondents across 50 countries from March 25 to April 17. Startup Genome CEO J.F. Gauthier and chief innovation officer Arnobio Morelix wrote the report.

The survey found 41% of startups globally are threatened — in what the report called the “red zone” — with only up to three months’ worth of cash runway left. Many very young startups have only a few months’ worth of cash — 29% were already in that situation before the crisis — but the pandemic put 40% more of them into that precarious position.

Focusing on startups that have raised series A, B, or later rounds, 34% have less than six months’ worth of cash — a danger zone in the current situation, as fundraising has become more difficult.

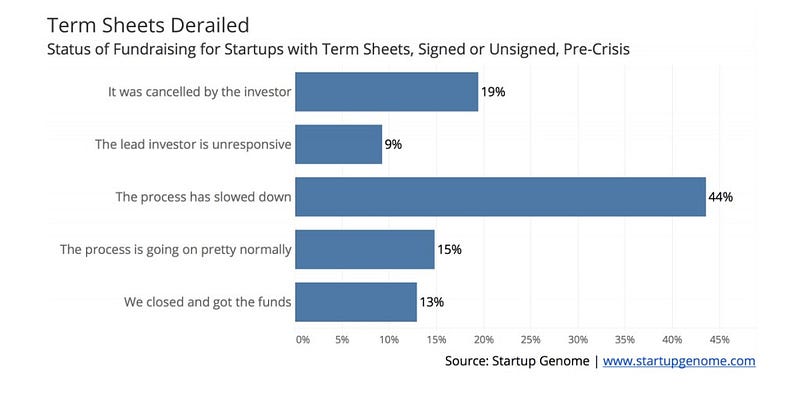

Of startups that had a term sheet before the onset of the crisis, nearly 20% have had the term sheet pulled by the investor and 53% have seen the process slow down significantly or have faced an unresponsive lead investor. Only 28% have had the process continue normally or secured the funds.

Talent and jobs

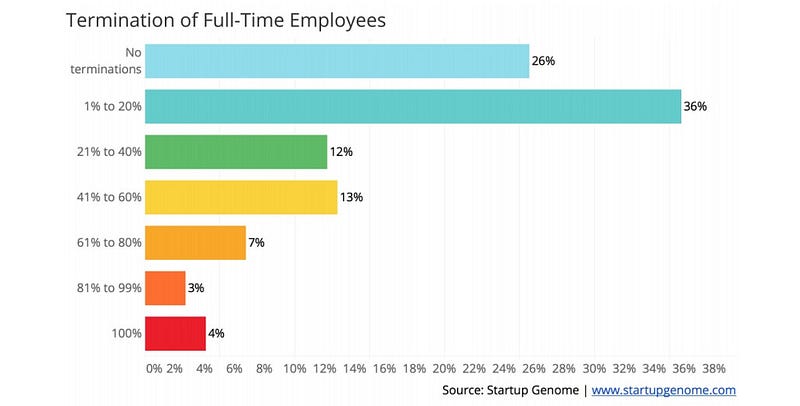

Above: Startup Genome says most startups are cutting jobs. Image Credit: Startup Genome

Since the beginning of the crisis, 74% of startups have had to terminate full-time employees, while 39% of all startups have had to lay off 20% or more of their staff and 26% have had to let go of 60% of employees or more. When the share of startups that had to terminate full-time employees is broken down by the top three continents for startup activity, North America has the biggest share of companies reducing headcount (84%), followed by Europe (67%) and Asia (59%).

Meanwhile, 74% of startups have seen their revenues decline since the beginning of the crisis. The most common type of change in revenue is a relatively modest decline. However, a sizable share of companies were very heavily hit: 16% of startups saw their revenue drop by more than 80%. A major reason for the drops in revenue is the effect of the crisis on industries those startups serve. Three out of every four startups work in industries severely affected by the COVID-19 pandemic.

Market growth

Above: Startup Genome says most companies can still operate in the pandemic. Image Credit: Startup Genome

At the same time, a small minority of companies are actually experiencing growth. In fact, 12% of startups have seen their revenue increase by 10% or more since the beginning of the crisis, and one out of every 10 startups is in an industry that’s actually experiencing growth. Indeed, every crisis creates opportunities. For instance, over half of Fortune 500 companies started during a contraction, and over 50 unicorns were created during the Great Recession alone, as Startup Genome data shows. The COVID-19 crisis will likely prove no exception.

But the damage and growth are not evenly distributed. On the positive side, B2C startups are about 3 times more likely to be in industries experiencing growth during the pandemic compared to B2B startups. On the negative side, B2B startups serving large enterprise clients are more likely to be in industries adversely affected than B2B startups serving small and mid-sized enterprises, and B2C startups are the least likely to be experiencing an increase in sales.

Operations and management

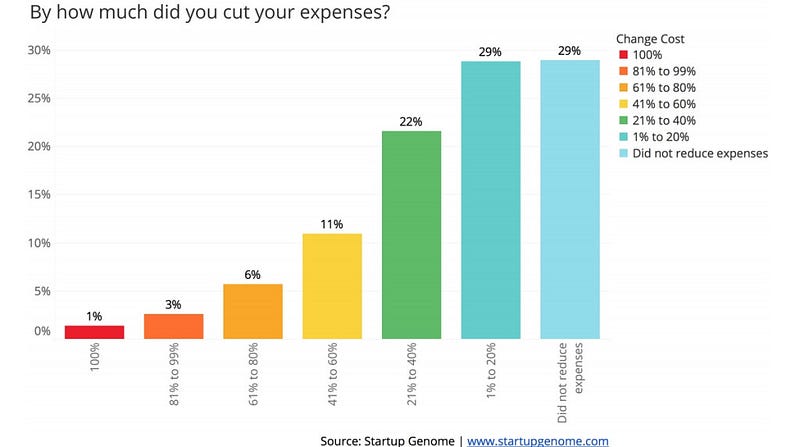

Above: Startups are slashing expenses. Image Credit: Startup Genome

Over two-thirds of startups have reduced their expenses since December 2019, with the lion’s share of those making relatively small cuts. Some companies, however, cut costs very aggressively, with more than one out of every 10 companies cutting costs by over 60%. Out of those startups cutting costs, 76% have started making cuts since the beginning of March — indicating that most of the cost-cutting is directly related to the pandemic.

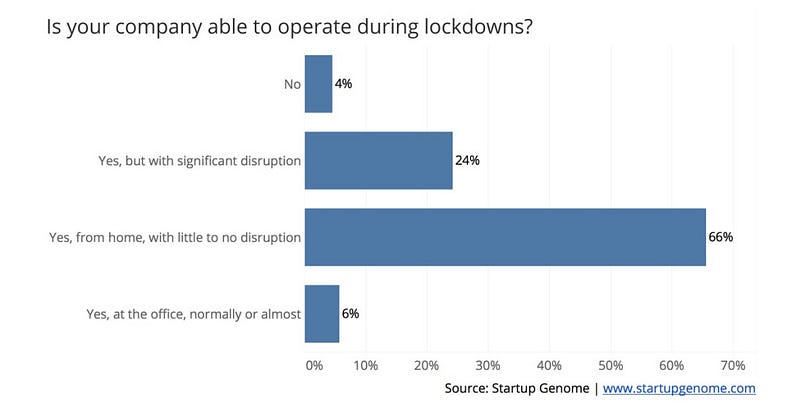

Nonetheless, tech startups are uniquely situated to continue operating even in lockdown scenarios. Unlike many traditional businesses, 96% of startups responded that they have continued working during the crisis, even if they are experiencing significant disruption.

Policy suggestions

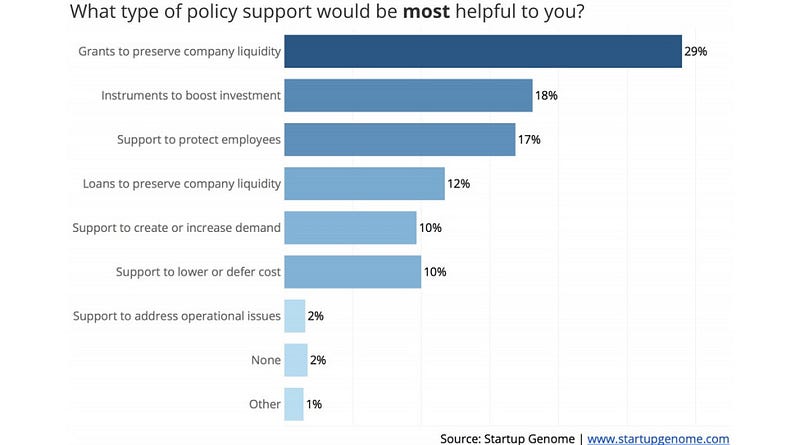

Above: Policy suggestions from startup founders and executives. Image Credit: Startup Genome

About 38% of startups have not received assistance and do not expect to be helped by policy relief measures related to the pandemic. At the same time, 16% are not currently supported but expect to be helped by a policy measure soon. The remaining 46% of startups are currently receiving some form of assistance.

Executives say the top four most helpful policy responses for their businesses would be:

Grants to preserve company liquidity (29%)

Instruments to boost investment (18%)

Support to protect employees, like payroll supplementation grants (17%)

Loans to preserve company liquidity (12%)

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer

The coronavirus pandemic will be remembered as a world-reordering event. Like the Great Depression, the fall of the Berlin Wall, and the 2008 global financial crisis, it will accelerate social and economic changes that would otherwise have taken years to materialize.

Emma Rose Bienvenu, Co-President of the McGill Business Law Association and the host of ‘Arbitration Profiles’, a podcast of the McGill Journal of Dispute Resolution

However long it will take, we will eventually beat back this virus, and our economies will eventually recover from the punishing recession it will have brought about. But when the dust settles and the masks come off, the pandemic will have permanently reshaped our social and economic behavior. Here are a few outcomes that seem increasingly likely.

1. Companies that traffic in digital services and e-commerce will make immediate and lasting gains

With people isolated indoors and away from other people, short-term winners will be those who provide goods and services without needing to come into physical contact with their customers.

Winners in this category will be cloud computing providers (for example, Amazon Web Services), remote work services like Zoom, Slack, Microsoft Teams, virtual reality companies like Oculus, streaming services like Netflix, and esports organizations like Cloud9.

Social media traffic will soar, but advertiser revenue will suffer from weak demand in a crippled economy. Coca-Cola has already pulled all social media ads; as its peers follow suit, the sharp overall decrease in ad spend will reverberate down to production companies, advertising agencies, and TV and radio stations.

In the short term, e-commerce platforms, food delivery services, and logistics companies will also be winners. When the economy does eventually improve, these gains will mostly endure thanks to entrenched shifts in consumers’ buying habits.

Employees who are suddenly working from home by necessity are experiencing a change in their work style that spares them the suit and commute and gives many of them greater flexibility with their schedules and demands outside of work. Many will find they prefer working remotely and, when the crisis recedes, it will become hard and expensive for some companies to deny them that option, while others will want to take advantage of this new preference. Remote work technology will improve, enabling the sort of mingling previously thought to require in-person meetings. This will cause a severe downturn for commercial real estate as companies drastically cut the size of their workspaces.

Coupled with stricter travel restrictions and mandatory quarantines for foreigners entering certain countries, this will also put severe strain on industries reliant on business travel. It will also lead to an exodus of white-collar workers from big cities — once companies’ remote work routines have been smoothed out, their newly remote-capable employees will have the flexibility to move out of dense cities and into lower-cost areas.

3. Many jobs will be automated, and the rest will be made remote-capable

To survive the crisis, firms will need to lay off their least-productive workers, automate what can be automated, and make the rest remote-capable. Those who do this effectively will emerge leaner and more efficient. They will also have no incentive to return to their pre-crisis head count — and many of those whose functions have been automated will lack the skills to compete in the new, post-crisis economy. Labor force participation will suffer. In the medium and longer term, these companies will also realize that the functions they have made remote-capable can also be performed by highly skilled workers in lower-cost countries. In short, jobs will first move from in-person to remote-domestic, and in time they will go from remote-domestic to remote-overseas.

4. Telemedicine will become the new normal, signaling an explosion in med-tech innovation

In a matter of weeks, regulatory barriers to telemedicine in the U.S. have largely fallen. Doctors in the U.S. now perform remote visits across state lines, can email and video-chat patients in compliance with HIPAA, and Medicare and health insurance providers have to now reimburse telemedicine services. Though these measures were announced as temporary, those who have now had firsthand experience with the convenience and cost-effectiveness of telemedicine will not want to forgo it. Once the crisis recedes, health care will begin to be provided remotely by default, not necessity, allowing the best doctors to scale their services to far more patients. Already, shares in Teladoc and similar companies have surged on the expectation that the pandemic will provide long-lasting tail winds for the telemedicine industry.

The human and economic cost of the pandemic will inject Department of Defense-level spending into telemedicine, medical imaging companies, diagnostics companies, and virology research. Telehealth offerings will improve and proliferate, with better at-home testing and diagnostics products and the ubiquitous adoption of wearables that continuously monitor for symptoms. Major cities will put in place permanent pandemic surveillance systems, and many businesses and sports stadiums will perform real-time threat monitoring by screening for symptoms and temperature-checking attendees.

5. The nationwide student debt crisis will finally abate as higher education begins to move online

The pandemic has forced numerous universities to move classes online, prompting calls from students for reimbursements of tuition and expenses. If, come fall semester, universities are still teaching online, what percentage of those students will re-enroll at pre-crisis tuition levels? The worldwide remote learning experiment that is currently underway may demonstrate that higher learning can function effectively at a fraction of in-person costs. If it does, it may lead to a reckoning that transforms the delivery of higher education, particularly for less-selective universities, as students re-weigh the costs and benefits of a four-year residential experience.

Universities will also face pressure to cut costs from the severely cash-strapped state governments that fund them. Many will eventually adopt hybrid models that limit face-to-face learning to project-based assignments and student working groups. These will dramatically cut costs, while allowing the best instructors to scale their insights to more students. They might also make a compelling case for broadening access to elite universities, whose small cohorts have historically been justified on the basis of physical constraints inherent to classrooms and campuses.

6. Goods and people will move less often and less freely across national and regional borders

Countries will retreat into themselves, borders will become less porous, and international trade will slump. To bolster their ability to survive extended periods of economic self-isolation, governments will push to strengthen domestic manufacturing capacity and step in to inject adequate redundancy in critical supply chains. Even before the pandemic struck, higher wages in China, international trade wars, and the rise of semi-autonomous factories had already prompted firms to reshore manufacturing, bringing it closer to domestic research and development centers. The coronavirus crisis will accelerate this trend: Increasingly, corporations will favor the resiliency of centralized domestic supply chains over the efficiency of globalized ones. Lacking support to protect the shared gains of worldwide economic integration and globalized supply chains, the multilateral institutions of global governance established in the 20th century will, if temporarily, begin to fray.

Governments that adopted emergency powers to manage the crisis and police their borders will be loath to relinquish them when it recedes. Governments will conduct more widespread and more intrusive surveillance and claim broader authority to monitor and respond to viral threats. Checkpoints at national and regional borders will use biometric screening to detect deadly viruses in real time and impose mandatory quarantines on travelers entering from certain countries. This will create significant friction for all kinds of travel. Airlines, hospitality, and tourism will experience a severe slump in demand in and beyond the immediate aftermath of the crisis.

7. After an initial wave of isolationism, multilateral cooperation may flourish

After an initial retreat from globalization, countries might come to recognize that technological and viral threats are existential, and therefore require international cooperation. Adopting a sense of pragmatic internationalism, countries would develop international norms, monitoring and reporting systems, and coordinated response and contingency plans. When the next pandemic strikes, global monitoring and reporting systems would detect it earlier. A coordinated global response would make self-isolation orders effective, shortening the economic shutdown and hopefully sparing lives.

Emma Rose Bienvenu is the Co-President of the McGill Business Law Association and the host of ‘Arbitration Profiles’, a podcast of the McGill Journal of Dispute Resolution

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

Small-scale businesses and companies in Kenya with annual sales of below Sh500,000 ($4,718.52) will be exempted from paying the one percent sales tax as part of a series of measures as part of measures to cushion them from the impact of the Coronavirus pandemic, according to the tax reliefs draft bill that the Kenyan Treasury has presented to Parliament for approval.

Nikil Hirra, tax expert at Bowmans

“Raising the floor to Sh500,000 will offer relief to small traders, but raising the cap to Sh50 million will expand traders who could not be paying their fair share of taxes,” said Nikil Hirra, a tax expert at Bowmans Kenya.

Here Is All You Need To Know

The sales tax, which was reintroduced in January, will not capture the smallest of traders after the State increased the cap for those liable to pay the levy from the current Sh5 million annually — or Sh416,600 per month — to Sh50 million per year.

That means Small and Medium Enterprises (SMEs) will be liable to pay the one percent turnover tax (TOT)

The review of the sales tax is contained in the Tax Laws (Amendment) Bill, which offers legal backing to the tax reliefs announced by President Uhuru Kenyatta last month, which include lower income tax for salaried employees in the formal sector and a reduction in corporate tax for large organisations.

Traders operating small and mid-sized businesses will also now pay one percent tax on their sales to the Kenya Revenue Authority (KRA), down from the three percent rate introduced in January, a move that looks set to ease the pain for enterprises struggling with low revenues.

The exemption of traders with revenues of less than Sh500,000 per month in sales will be a relief for those who run kiosks, grocery stores, salons or any other mini and small scale family businesses. Since January 1, these traders have been paying three percent of their sales to KRA, irrespective of whether they are selling at a profit or loss. This meant for every Sh1,000 they generated as revenue, they had pay Sh30 to the taxman at the end of the month.

The small traders will also be spared the presumptive tax at the rate of 15 percent of the value of annual single business permits issued by county governments if the MPs approve the changes in the Bill. The House reconvenes next week to deliberate on the bill.

The tax changes are geared at lowering the cost of basic items while providing workers with additional income for spending to boost consumption and sales of traders.

The small and mid-sized businesses remain the backbone of the Kenyan economy and the largest contributor of new jobs in an economy where big corporates have frozen hiring while some have shed jobs or scaled down operations to protect profits.

When it was introduced, analysts faulted the three percent turnover tax, saying it would saddle small traders with additional operating costs. The sales tax was expected to provide the KRA, under pressure to collect additional revenue, with a fresh avenue for raising taxes from players this segment, the majority of whom have not been paying State levies.

The Treasury had in 2018 dropped the turnover tax due to its poor performance as most traders failed to make revenue disclosures. It replaced the sales levy with a presumptive tax at the rate of 15 percent of the single business permit fee issued by county governments. The presumptive tax allowed KRA to gather additional data on small traders, setting the stage for the return of the turnover tax.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

He could be contacted at udohrapulu@gmail.com

Below are what the Nigerian proposed regulation on crowdfunding is all about.

1. What Categories Of Businesses Can Raise Funds Through Crowdfunding?

Under the regulation, only MSMEs (Micro, small and medium enterprises) registered as a company in Nigeria with a minimum of two-years operating track record shall be eligible to raise funds through a Crowdfunding Portal registered by the Securities And Exchange Commission.

Once these funds are raised, the investors are issued corresponding shares, debentures, or such other investment instrument by the startup or MSMEs.

In this case, the startup or MSMEs wishing to offer or sell securities or other investment instruments in Nigeria does not need to first register such securities such as shares, debentures with the Securities and Exchange Commission.

However, the startups or MSMEs are only allowed to raise a maximum of the following amounts within a 12-month period: i) The maximum amount which may be raised by a Medium enterprise shall not exceed N100Million ($260k); ii. The maximum amount which may be raised by a Small enterprise shall not exceed N70Million ($182); iii. The maximum amount which may be raised by a Micro enterprise shall not exceed N50Million ($130k).

The only type of startups totally exempted from the maximum crowdfunding amounts are startups that run digital platforms that connect investors to specific agricultural or commodities projects for the purpose of sponsoring such projects in exchange for a return (such as FarmCrowdy)

Entities prohibited from raising funds through a Crowdfunding Portal include(a) complex structures (an entity without immediate transparency of ownership and/or control thereby making it difficult to immediately ascertain the beneficial owners of the entity) ; (b) public listed companies and their subsidiaries; (c ) companies with no specific business plan or a blind pool; (d) companies that propose to use the funds raised to provide loans or invest in other entities.

2. How Can Startups Crowfund Under The Regulation?

For startups in Nigeria desiring to raise funds under the crowdfunding regulation, the following steps must be followed:

The startup must fall under the categories of businesses described above.

Application for registration as an issuer to a crowdfunding portal (similar to Uprise.Africa in South Africa). A Crowdfunding Portal is a company having a minimum paid-up capital requirement of N100 million which runs a website, portal, intermediary portal, application, or other similar module that facilitates interaction between fundraisers and the investing public.

Due Diligence is then conducted on the startup or MSMEs by the Crowdfunding Portal. The due diligence exercise will focus on background checks on the startup or MSMEs to ensure fit and properness of the issuer’s board of directors, officers and controlling shareholder(s); (ii) the business proposition of the issuer; and (iii)compliance with all relevant KYC, and AML/CFT regulations as stipulated by the SEC.

Once the application has been accepted by the Crowdfunding Portal, the startup will then proceed to raise funds from the public, in return for a corresponding shares in the business.

Every eligible startup or MSMEs seeking to raise funds through a Crowdfunding portal shall issue an offering document, containing information such as (i) warnings to investors (ii) the name and address of the issuer, directors and officers; (iii)holders of more than 5% of the issuer’s securities; (iv)description of the business of the issuer; (v) principal risks facing the business of the issuer; (vi)use of proceeds; (vii) target offering amount (and a deadline to reach the target offering amount); (viii) risk factors; (ix) related party transactions (x) exit options for investors

Only plain vanilla bonds/debentures, ordinary shares and other investment instruments as may be determined by the Commission can be issued in return for the investors’ funds by the startups or MSMEs.

The startups or MSMEs are thereafter rigorously monitored by the Crowdfunding Portal. Accordingly, the monitoring will extend to the conduct of issuers and the Portal are empowered to take action against any misconduct of the issuer( the startup or MSMEs); (b)The Portal also monitors issuers to ensure that the fundraising limits imposed on the issuer are not breached. (c) The Portal will also monitor investors to ensure that the investment limits imposed on the investors are not breached and ascertain the classification of prospective investors into relevant investor categories; (e) The Portal is also expected to file reports about the startups or MSMEs with the Commission.

3. What Happens When Investors Invest In Your Startup Through The Crowdfunding Portal?

Under the Regulation, investors may be allowed to invest in companies hosted on the Crowdfunding Portal subject to the investment limit specified by the Commission from time to time, which in the meantime is that retail investors may not invest more than 10% of their annual income in a calendar year; and that (ii) Sophisticated, High Net worth and Qualified Institutional Investors are not subject to any limits.

A startup or MSMEs shall not host an offer concurrently on multiple Crowdfunding Portals.

Investors will be given a cooling off period of 48 hours from the date of close of the offer within which they may withdraw their investment.

If there is a material adverse change, affecting the project or the issuer, the investors will be given the option to withdraw their investment if they choose to do so within 7 days after the said notification.

Where an investor cancels the offer or agreement to purchase securities or investment instruments, all funds which may have been debited from or blocked in the account of the investor shall be refunded or released within 48 hours of the request to cancel.

Nigeria ‘s proposed crowdfunding regulation hopes to put the country back on Africa’s crowdfunding map

4. How Funds Invested Through The Crowdfunding Platform Are Treated

Under Nigeria ‘s proposed new crowdfunding regulation, every Crowdfunding Portal shall appoint a custodian who shall establish and maintain a separate trust account for each funding round on its platform with a financial institution registered by the Commission as a Custodian

Funds invested will be maintained by the Custodian in a trust account and will only be released to the startup or MSMEs after specified conditions are met.

Funds raised would only be released to the startup or MSMEs if the target amount or the minimum threshold of funds to be raised is met.

A funding project shall remain live on a Crowdfunding portal for not more than (60 days).

Where the minimum threshold is not reached at the end of an offer, the Crowdfunding portal shall effect a refund to all investors within 48 hours.

Investors shall have the right to withdraw any offer or agreement to purchase the securities or investments instruments 48 hours after the closing date stated in the startup or MSMEs’s offering materials.

Thereafter, an investor is only able to cancel in the event of a material change to the offering.

Where the funding target is reached, the Crowdfunding portal shall make funds available to the startup or MSMEs within 24 hours of the cooling off period provided that where the Issuer is a public company or a public company by default, the portal shall require evidence of registration of the securities with the Commission prior to transferring the funds to the Issuer (where applicable);

Where the amount raised meets the minimum amount but falls short of the target amount, the issuer shall provide a revised plan for the proposed use of funds to the investors and the portal. Provided that the underlying project(s) to the proposed use of funds can be downscaled and executed independently without negatively impacting operations of the startup or MSMEs.

Investors shall not transfer their securities or investment instrument for a period of one year except if a transfer is: (a) to the issuer of the securities or investment instrument; (b) to an institutional investor; or (c) part of an offer for sale registered with the Commission;

The issuer’s articles of association shall provide for the right of retail investors to withdraw from the company or to sell the stake, in the event that controlling shareholders transfer control of the company to third parties within three years from the conclusion of the offer.

A crowdfunding portal shall take all reasonable steps and establish measures by which it is able to verify that the proceeds raised from its platform are utilized for the stated purpose.

For an offer to be successfully completed, the minimum amount indicated in the offering document which must be sufficient to accomplish the business objectives of the issuer must have been subscribed for.

NB:

Micro Enterprises in Nigeria are those enterprises whose total assets (excluding land and buildings) are less than Ten Million Naira with a workforce not exceeding ten employees.

Small Enterprises are those enterprises whose total assets (excluding land and building) are above Ten Million Naira but not exceeding One Hundred Million Naira with a total workforce of above ten, but not exceeding forty-nine employees.

Medium Enterprises are those enterprises with total assets excluding land and building) are above Fifty Million Naira, but not exceeding One Billion Naira with a total workforce of between 50 and 199

employees — Source: SMEDAN Nigeria

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

He could be contacted at udohrapulu@gmail.com

South Africa ’s Department of Small Business Development has launched its proposed debt relief fund to help reduce the impact of the economic shutdown caused by the coronavirus on startups, small, micro and medium enterprises (SMMEs). The country’s small business minister Khumbudzo Ntshavheni said that the fund is aimed at providing relief on existing debts and repayments.

small business minister Khumbudzo Ntshavheni

“As the nation grapples with the impact of the Covid-19 pandemic, the department will be guided by the National Command Council in determining the sectors that are deemed severely impacted in order to qualify for the debt relief fund,” he said.

How South African Startups Can Benefit From The Fund

According to Ntshavheni, for SMMEs to be eligible for assistance under the debt relief fund, the applicant must demonstrate the direct link of the impact or the potential impact of Covid-19 on business operations.

The facility will also assist entities to acquire raw material, pay labour and operational costs. All these interventions will be structured to match the patterns of the SMMEs cash flows, as well as the extent of the impact suffered, he said.

To strengthen monitoring and avoid abuse, businesses requiring assistance will be required to enrol on the SMME South Africa platform here.

This platform has now gone live today, Tuesday, 24 March 2020.

The department plans also to allow these businesses to use the database in the future to apply for both financial and non-financial support, access information about business opportunities, and access market opportunities.

Some of the details which companies are required to share include:

Annual turnover;

Shareholders (including current BEE standing);

Number of employees;

Employee demographics;

Sub-sectors

Launch Of ‘Business Growth/Resilience Facility’

Also launched for startups and SMEs in South Africa is a new fund called ‘Business Growth/Resilience facility’ specifically created to enable continued participation of SMMEs in supply value-chains — particularly those which manufacture or supply items which are in demand due to the pandemic.

According to the department, this facility will offer working capital, stock, bridging finance, order finance and equipment finance, and the amount required will be based on the funding needs of the business.

To participate under this programme, startups and businesses are also asked to enrol on the SMME South Africa platform.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

He could be contacted at udohrapulu@gmail.com

African countries have so far lost an estimated $29 billion to the coronavirus economic disruption, an amount equal to Uganda’s gross domestic product (GDP), according to UN estimates.

United Nations Economic Commission for Africa (ECA) Executive Secretary, Vera Songwe

“Africa may lose half of its gross domestic product with growth falling due to a number of reasons which include the disruption of global supply chains,” said United Nations Economic Commission for Africa (ECA) Executive Secretary, Vera Songwe, in a statement.

Here Is All You Need To Know

According to the United Nations Economic Commission for Africa (ECA)’s latest report, coronavirus will shred 1.4 per cent off Africa’s $2.1 trillion GDP, as a result of the widespread disruption of business on the continent and across the world by the coronavirus pandemic.

The report however forecasts that the continent’s annual economic growth is likely to drop from 3.2 per cent in February to 1.8 per cent in March, warning that it could worsen in the coming months as more countries report coronavirus infections within their borders.

Uganda’s GDP was estimated at about $28.5 billion as at the end of last year, indicating that the estimated losses so far are equivalent to the country’s annual production.

The UN agency has warned that the unfolding coronavirus crisis could seriously dent Africa’s already stagnant growth, with the continent expected to spend more $10.6 billion in unanticipated increases in their health budgets to curtail spread of the virus.

Dr Songwe in the statement observes that China, Africa’s major trading partner which is strongly hit by Covid-19, was already inevitably impacting negatively on Africa’s trade by directly affecting global supply chains.

According to the UN document, Africa’s increased interconnectedness with the rest of the world has exposed the continent to the disease, which was first reported in Wuhan, China, in December.

The continent has also seen a sharp decline in Foreign Direct Investment inflows, capital flights and financial markets instability.

Dr Songwe estimates that Covid-19 could reduce Nigeria’s total exports of crude oil in 2020 by between $14 billion and $19 billion.

Policy Alternatives

The document recommends a number of policy options to the African governments to reduce more revenue losses that could lead to unsustainable debt.

Some of the suggestions to governments include the need to review and revise their budgets to reprioritise spending towards mitigating expected negative impacts from Covid-19 on their economies, such as providing safety nets and incentives to food importers to quickly forward-purchase to ensure sufficient reserves of basic supplies.

The UN agency also calls for a need to set aside a special fund for the virus preparedness, prevention and curative facilities including logistics and to improve their health systems.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer. He could be contacted at udohrapulu@gmail.com

With the Covid-19 virus now a worldwide pandemic, if you’re leading any startup or small business, you have to be asking yourself, “What’s Plan B? And what’s in my lifeboat?”

Here are a few thoughts about operating in uncertainty.

Impact

Social isolation and a declared national emergency have had an immediate impact on industries that cluster people; conferences, trade shows, airlines/cruise ships and all types of travel, the hospitality industry, sporting events, theater and movies, restaurants and schools. Large companies are telling employees to work at home. Large retail chains are shutting down their stores. While the impact on small businesses and workers in the “gig-economy” hasn’t made the news, it will be worse for them. They have fewer cash reserves and a smaller margin of error for managing sudden downturns. The ripple and feedback effect of all of these closures will have a major impact on our economy, as each industry that gets impacted puts people out of work, and those laid off workers don’t buy products and services.

It’s no longer business as usual for the rest of the economy. In fact, shutting down the economy for a pandemic has never happened. Millions of jobs may be lost in the next few months, as entire industries are devastated, something not seen since the Great Depression of 1929–39. I hope I’m very wrong, but the social and economic impacts of this virus are likely to be profound and will change how we shop, travel, and work for years.

If you’re running a startup or small business, your first priority (after your family) is keeping your employees and customers safe. But the next question is, ‘What happens to my business?”

The questions every startup or small business CEO needs to ask now are:

What’s my burn rate and runway?

What does my new business model look like?

Is this a three-month, one-year, or a three-year problem?

What will my investors do?

Burn rate and runway

To answer the first question, take stock of your current gross burn rate: How much cash are you spending each month? How much of that goes toward fixed expenses (those you can’t change, such as rent)? And how much goes toward variable expenses (salaries, consultants, commission, travel, AWS/Azure charges, supplies, etc.)?

Next, take a look at your actual revenue each month — not your forecast, but real revenue coming in. If you’re an early stage company, that number may be zero.

Subtract your monthly gross burn rate from your monthly revenue to get your net burn rate. If you’re making more money than you’re spending, you have positive cash flow. If you’re a startup and have less revenue than your expenses, that number is negative and represents the amount of money your company loses (“burns”) each month. Now take a look at your bank account. See how many months your company can survive burning that amount of cash each month. This is your runway — the amount of time your company has before it runs out of money. This math works in a normal market …

Unfortunately, it’s no longer a normal market.

All your assumptions about customers, sales cycle and most importantly, revenue, burn rate, and runway are no longer true.

If you’re a startup, you’ve likely calculated your runway to last until you raise your next round of funding. Assuming there was going to be a next round. That may be no longer true.

Your new business model

Since the world today is no longer the same as it was a month ago, and likely will be worse a month from now, if your business model today looks the same as it did at the beginning of the month, you’re in denial — and possibly out of business.

It’s the nature of startup CEOs to be optimistic, however you need to quickly test your assumptions about customers and revenue. If you are selling to businesses (a B-to-B market), have your customers’ sales dropped? Are your customers closing for the next few weeks? Laying off people? If so, whatever revenue forecast and sales cycle estimates you had are no longer valid. If you’re selling directly to consumers (a B-to-C market), were you in a multi-sided market (consumers use the product but others pay you for their eyeballs/data)? Are those assumptions about payers still correct? How do you know?

What are the new financial metrics? Receivables — get on top of them. Days of cash left?

You need to figure out your actual burn rate and runway in this new environment now.

Is this a three-month, one-year, or a three-year problem?

Next, you need to take a deep breath and try to gauge how long this problem will last. Are the shutdowns of businesses going to be a temporary blip in the economy, or will they drive the US and Europe into a long recession?

If it’s just three months (looking more unlikely by the day), then an immediate freeze on variable spending (hires, marketing, travel, etc.) is in order. But if the effects are going to reverberate in the economy longer, you need to start reconfiguring your business. You need a lifeboat strategy. That’s a fancy phrase for figuring out the minimum your company needs to hold onto to stay alive.

A one-year problem means taking a knife to your burn rate (layoffs and elimination of perks and programs to reduce your variable expenses), renegotiating what previously seemed liked fixed expenses (rent, equipment lease payments, etc.), and putting only the essential elements for survival in the lifeboat.

If you were selling online versus in-person, you may have an advantage (assuming your customers are still there.) Or you change sales strategy.

Whatever your product/market fit was last month, it’s no longer true and needs to change to meet the new normal. Does this open new value propositions and kill others? Do you need to alter the product?

And if it’s a three-year problem? Then not only do you need to jettison everything that isn’t essential for survival, you’ll probably require a new business model. In the short term, explore whether some part of your business model can be oriented around the new rules of social isolation. Can your product be sold, delivered, or produced online? Does it have some benefits if delivered that way? (See the advice from Sequoia Capital here.) If not, can your product/service be positioned as a lifeboat for others to ride out the downturn?

As a leader, you need to plan, communicate, and act with compassion.

Revise your sales revenue goals and product timelines, create a new business model and operating plan, and communicate them clearly to your investors and then to your employees. Keep people focused on an achievable plan they clearly understand. From the perspective of having lived through the last three crashes, I’ve observed the biggest mistake CEOs made was not making draconian cuts to expenses quickly enough. They dripped out layoffs and cuts, holding onto favored projects with magical thinking that somehow this was just something that would pass. You need to act now.

If you’re in a large company considering layoffs, the first option should be to cut the salaries of the higher paid exec/employees to try to keep the people who can least afford to lose their jobs employed. (Good things will come to CEOs who first try to save everyone on the ship before they jump in the lifeboat.) If/when people need to be laid off, do it with compassion. Offer extra compensation. If in the worst case you see you’re running out of cash, under no circumstances run it down to zero. Do the right thing and have enough cash on hand to offer everyone at least two weeks or more of pay.

Your investors

One of the key elements of survival is access to capital. As a startup or small business you should realize your investors are also asking themselves how this pandemic will affect their business model. The cold hard truth is that, in a crash, VCs are running their own “What do I save in the lifeboat?” exercise. They triage their deals — first worrying about liquidity of their late stage deals, which have the highest valuations. These startups typically have very high burn rates and funding for those could fall off a cliff. You and the survival of your startup may no longer be their priority, and your interests are no longer aligned. (VCs who tell you otherwise are either naïve, lying through their teeth, or not serving the interests of their investors.) In every major downturn inflated valuations disappear and the few VCs still writing new checks find it’s a buyer’s market. (Hence the term “vulture capitalists.”)

Some investors have only lived in a booming market when valuations only went up and investment capital was plentiful. But investors with grey hair can remember the nuclear winter after the past recessions of 2000 and 2008 and can offer some historical patterns of crashes and recovery to CEOs running early stage startups. Keep in mind,# that today’s circumstances are different. This isn’t a bear stock market. This is a conscious shutdown of most of our economy, trading jobs for saving hundreds of thousands of lives, that’s causing a bear market and a likely recession.

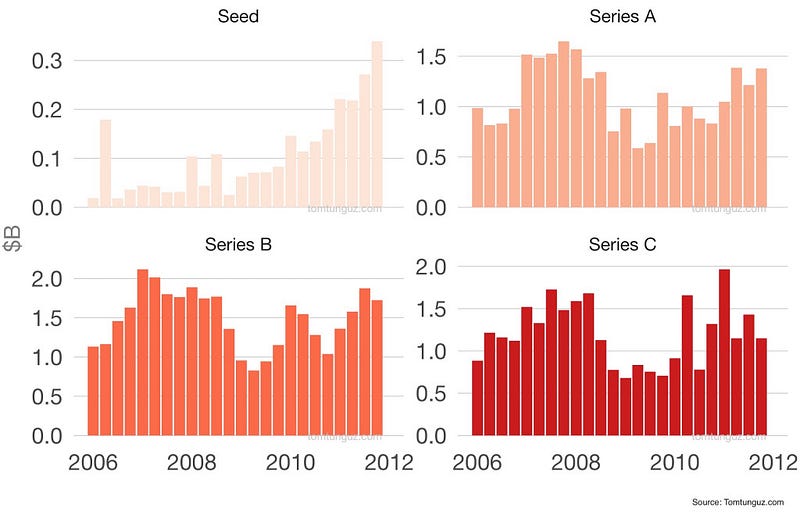

Data from the last large crash in 2008 had seed rounds recovering early, but later stage funding cratered and took years to recover. (The figure below — part of this post from Tomasz Tunguz — shows quarterly VC investments before and after the 2008 crash.)

This time around, the health of the venture business may depend on what hedge funds, investment banks, private equity firms, sovereign wealth funds, and large secondary market groups do. If they pull back, there will be a liquidity crunch for later stage startups (Series B, C…). For all startups in the short term, the deal terms and valuations will get worse, and there will be fewer investors looking at your deal.

As a startup CEO you need to know if your board is going to be screaming at you for not radically cutting burn rate and coming up with a new business model or, will they be yelling at you to stop being distracted and stay the course?

And if the latter, I’d want to know what skin they have in the game if they’re wrong. It’s pretty easy for VCs to tell you they’ll be right behind you when you need a next round, until they’re not. Unless your investors are matching their orders for “full speed ahead” with a deposit into your bank, now is not the time to be railroaded into a burn rate that is unrecoverable.

Prepare for a long cold winter. But remember no winter lasts forever, and in it smart founders and VCs will be planting the seeds for the next generation of startups.

Lessons learned

This is a conscious shutdown of our economy, trading jobs for saving hundreds of thousands of lives

It’s likely going to cause a recession

The Covid-19 virus will change how we shop, travel, and work for at least a year and likely three.

It’s inconceivable that you can have the same business model today as you did 30 days ago

Put in place lifeboat plans for three-month, one-year and three-year downturns

Recognize that your investors will act in their interests, which may no longer be yours

Take action now

But act with compassion.

Steve Blank is a retired serial entrepreneur-turned-educator who created the Customer Development methodology that launched the lean startup movement, which he wrote about in his book, The Four Steps to the Epiphany. Blank teaches Lean LaunchPad classes at Stanford University and Columbia University where he is a senior fellow for entrepreneurship.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

He could be contacted at udohrapulu@gmail.com

The heat is getting intense. Anytime soon, car-hailing companies (such as Uber, Bolt and others) in South Africa and in Nigeria’s most populated city, Lagos, may be in for a tougher set of laws which will regulate their operations.

Fikile Mbalula

‘‘UBER, Taxify, BOLT and others will be regulated by Government.

These amendments seek to provide for e-hailing services regulation, also to empower provinces to undertake new contracts which was absent in the principal Act.

Under South Africa’s National Land Transport Amendment Bill, which has been passed in parliament and sent to South Africa’s president for assent, drivers on car-hailing platforms like Uber and Bolt who do not have operating licences may incur a fine as much as R100 000 ($6000) for those platforms (Uber, Bolt and others).

In Nigerian, under a new set of regulations, which should have been in place from March 1, 2020 (but for some intense lobbying) drivers on ride-hailing platforms are required to have LASDRI card and a driver badge issued by the Department of Public Transport and Commuter Services of the Ministry of Transport.

In Ghana, from Uber to Bolt to Yango, drivers who rely on ride-hailing to sustain their livelihood would start paying a mandatory GHC 60 ($11) annual fees for ride-hailing platforms in the country, in addition to their cars undergoing roadworthy tests every six months.

Image for: South Africa issues notice to regulate Uber, others

Here Are The New Regulations In Details

South Africa

Under Section 66A of the Amendment Bill, e-hailing services are now expressly mandated to protect consumers using their platforms. According to the new law, e-hailing or technology-enabled ride-hailing companies must — (a) have the facility to estimate fares and distances, taking into account distance and time, and must communicate the estimate to passengers in advance electronically; (b) communicate the final fare to the passenger or passengers at the conclusion of the trip electronically, and (c) provide the prescribed details of the driver of the vehicle to the passenger or passengers electronically.

Where a person conducts a business providing an e-hailing software application, that person — (a) may not permit an operator to use that application for a vehicle for which the operator does not hold a valid operating licence or permit for the vehicle, or whose operating licence or permit has lapsed or been cancelled, and (b) must disconnect the e-hailing application immediately and keep it disconnected until a valid operating licence has been obtained for the vehicle.

Consequently,operating an e-hailing service without the proper operating license or permit could result in a fine not exceeding R100 000 or a period of imprisonment not exceeding two years.

The law also empowers provincial regulatory authorities in South Africa to withdraw or suspend an operating licence from an operator which has contravened the National Land Transport Act or the Roads Traffic Act.

Image for: These are examples of ride-sharing startups in Africa, (including Uber) the laws seek to regulate

Nigeria: Lagos

Although Nigeria as a country is still silent on regulating the activities of ride-hailing companies, Lagos, the most populated city in the country is reportedly mulling a set of local regulations targeting car-hailing companies operating within the city. As reported by local news media:

Under the proposed new regulations, drivers on ride-hailing platforms are required to have LASDRI card and a driver badge issued by the Department of Public Transport and Commuter Services of the Ministry of Transport.

The vehicles on such platforms must also have permits issued by the Lagos State Motor Vehicle Administration Agency and be fitted with a tag to be issued by the said department of transport.

The new regulations will also mandate third-party operators like Uber and Bolt to pay N10 million naira ($27k) and an annual renewal fee of N5 million ($13.5k) if they have less than 1000 drivers.

Third-party operators that have more than 1000 drivers will pay N25 million ($67.8k) licensing fee and N10 million annual renewal fee.

Operators who directly own their cars and employ their drivers will pay only the license fee of N5 million if such operators have below 50 drivers.

Those who have more than 50 drivers will pay N10 million for the operating license.

Under the new regulation, the state government will also earn 10% on the fee of each trip.

The new regulation (if it ever comes into effect) is coming on the heels of the Lagos state government ban on commercial tricycles and motorcycles, popularly known as okada from operating in six local governments — Apapa, Eti-Osa, Ikeja, Lagos Island, Lagos Mainland and Surulere.

Image for: Comparing Africa ‘s attempt to regulate Uber, others with the rest of the world. Source: — Daily Mail

Ghana

In Ghana, drivers who rely on ride-hailing to sustain their livelihood would start paying a mandatory GHC 60 ($11) annual fees for ride-hailing platforms in the country, in addition to their cars undergoing roadworthy tests every six months. Ghana’s Driver and Vehicle Licensing Authority (DVLA), which imposed the GH¢60 ($11) annual fee noted that the guidelines will cover the current ride-hailing platforms like Uber, Bolt, and Yango and will also cover companies who intend to operate ride-hailing platforms in Ghana in the future.

The fee is being imposed as part of new guidelines introduced by the Ministry of Transport, National Road Safety Commission, and the MTTD of Ghana Police Service.

In addition to the annual fee, owners of vehicles who use ride-hailing platforms will have to obtain a registration certificate at the Digital Transport Center at DVLA’s Headquarters in Cantonments for “verification and authentication.”

The DVLA also stated that ride-hailing cars must undergo roadworthy examinations and certifications every six months, making it twice a year roadworthy renewal.

Under the new guidelines, only vehicle owners can be represented by for purposes of such examinations and certifications. The representative must however go along with a duly signed Power of Attorney document as well as a valid national ID document.

Thereafter, a special sticker will be issued to vehicles that have completed this process to be pasted “on the windscreen at all times.”

On the other hand, drivers would have to be present at the Digital Transport Center themselves for their verification and authentication.

“Unlike in the case of the vehicle owner, the driver must be physically present for this activity…..Drivers must ensure that, at all times, they possess a valid Driver’s Licence,” Ghana’s Driver and Vehicle Licensing Authority (DVLA) noted in a statement.

The Authority also added that companies that operate the digital transport platforms must only work with drivers who have been verified by the DVLA.

“Once you are signed on, only verified and approved vehicles and drivers must be enrolled on your platform…The DVLA data system becomes the only valid source for verifying the authenticity of a driver’s license or a vehicle’s registration. Submit quarterly reports in the form as agreed with the Authority.”

The Bottom Line

Regulating ride-hailing companies such as Uber, Bolt and others in Africa is a step in the right direction provided such regulations only serve to establish a standard framework for the operations of those companies, and not to impose excessive levies and taxes or create monopolies to discourage innovation as it presently appears to be the case in the city of Lagos, Nigeria.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

He could be contacted at udohrapulu@gmail.com

Yacine Oualid is one of the biggest surprises of Algeria’s new national government. On January 02, 2020, aged only 26, Yacine Oualid became Algeria’s new Minister of Startups — a new newly created ministry under the newly elected President Abdelmadjid Tebboune’s administration.

President Abdelmadjid Tebboune

Yacine Oualid studied at the Faculty of Medicine of University of Sidi Bel Abbès.

Prior to becoming Algeria’s Minister of Startups, in June 2016, Yacine Oualid created SSH, a company specializing in cloud solutions for businesses, which would later become the first private web host in Algeria. In September 2019, he and his partner founded Smart Ways3, a startup in the field of logistics and geolocation. In December of the same year, he founded Bright Solutions, a leading IT company providing IT solutions and services, headquartered in England.

In this interview with Muriel Edjo of the Ecofin Agency, he reveals the major projects that will be his priorities and the new ambitions of Algeria as it concerns startups and Algeria’s digital economy.

As Minister of Startups, a department specially created in the context of the fourth industrial revolution, what exactly are your responsibilities?

If I have to sum it up, I would say that the New World Economy is taking shape, and that Algeria wishes, and will, become a major player. My goal, with all the players in the sector, is to participate in this transformation of the largest country in Africa.

In a more practical way, my role is first of all to set up a legal framework which is favorable to startups. Once set up, this legal framework will facilitate the creation of startups and their financing. The goal is to see it materialise in a few months’ time, Algerian champions, who will be able to offer their services all over the world. Algeria is determined to become an African pillar of innovation and we want to offer our entrepreneurs the best framework for entrepreneurship and innovation.

In addition, my mission touching on many other ministries, I also have the role of ensuring that all the other institutions adhere to this new vision, of an economy whose spearhead will be innovation and startups.

Being in this ministry is a big privilege, especially since we have the full support of the President of the Republic and the Prime Minister. This is very encouraging because, for the first time, in Algeria we have a government that has placed its trust in young people.

What actions are planned by your ministry to boost the local Startup industry?

One of the first steps will be to identify startups using a label. This label will allow access to a certain number of facilities, fiscal and non-fiscal advantages, bank accounts in foreign currency and facilities to export services. Labeled companies will also be able to benefit from the assumption by the State of the patent registration whether at national or international level.

We are also in the process of developing a new legal form for companies that is more suited to startups. It will make it possible to raise funds and make an IPO more simple and possible. We will also develop a legal framework for crowdfunding.

Finally, we are engaging with other departments on certain penalties startups in Algeria are exposed to, such as access to online payment; the quality of internet connection; the difficulties in obtaining certain authorizations; and the absence of Datacenter with international standards.

As such, I would like to emphasize that we are currently enjoying great collaboration from the other ministerial departments and that we have already obtained successes in a few weeks. For instance, the Ministry of Labor has just created an appropriate framework for the status of freelancers which will allow our startups to pool scarce resources in specific areas of development; the Ministry of Commerce has equally taken into consideration our recommendations to facilitate the export of services; and the Ministry of Housing has called on startups to digitize its services .

Can we qualify a new SME as a Startup? What criteria will prevail to identify a Startup?

A startup is above all a company that offers an innovative service or product, with strong growth potential and even if the criteria to define the startup differ from one country to another, the concepts of innovation and ” scalability” (the anglicism which translates to the fact of having a reproducible business model on large markets) are universal.

In order to award the “startup” labels, we will concern ourselves with 4 criteria: innovation, scalability, age of the startup which must not exceed 8 years, and size (turnover and number of employees)

Image for: Yacine Oualid, minister of startups, showing African startup funding by countries for the year-ended 2017

In announcing a startup ministry, the Head of State also announced a dedicated bank. Digital players like LegalPlace believe that a reliable banking system and advantageous taxation are more necessary than a dedicated bank which risks becoming a National Youth Employment Support Agency (ANSEJ) bis. What do you think ?

To begin with, there will be a fund for startups, the latter being financed more by opening capital than by debt. This fund will make it easier for startups to find financing.

In addition, our action plan provides for favorable taxation, whether for startups or investors. Our goal is not for Algeria to mass-produce startups, but rather to see the birth of Algerian champions who will conquer markets all over the world and which will lead entire sectors (developers, logistics for e- trade…).

What is the transformative potential of the Startup ecosystem on the Algerian economy?

Startups can become the spearhead of the Algerian economy, an economy which for many years has been dependent on the hydrocarbon sector and which seeks to renew itself. In the digital sector, they can quickly create jobs and wealth.

The digital economy now accounts for more than 30% of global economic growth, so we are at an important turning point in our history that should not be missed. The government’s interest in startups and the creation of a ministry dedicated to their promotion testify to the importance of this subject for the Algerian economy.

In 2019, the Ministry of Higher Education and Scientific Research announced the establishment of seven ICT incubators in 2020. What role will your ministry play in achieving the objectives of these strategic structures?

Creating solid bridges between the academic and entrepreneurial world is a great challenge for us and we are working in close collaboration with the Ministry of Higher Education so that the Algerian university facilitates entrepreneurship. These support structures within the university will allow students to acquire soft skills. Our ministry also aims to encourage the learning of programming languages in all sectors. The incubators will allow young students to get started in entrepreneurship by relieving them of many administrative and practical aspects. Through all of this, we hope to make the university an important player in the startup ecosystem in Algeria.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

He could be contacted at udohrapulu@gmail.com