Investors to Avoid For Your First Fundraise

First-time founders often have to raise small Angel rounds before they can get enough traction to raise serious money. Typically, such Angel investors will come from varying backgrounds — an ex-boss, a well-to-do friend, an experienced F500 executive, an ex-entrepreneur, or a family-business owner.

You will hear a lot of No’s — maybe dozens, or even hundreds — before you close your first Angel or seed round. So when a first Yes comes by, it is incredibly difficult to take a step back and assess the value of the Yes.

[Fund raising]’s filled with painful no’s: No’s that take your breath away in how quickly and rudely they’re delivered; no’s that are tied up in pretty little ribbons and disguised as “let’s keep in touch”; no’s that come in the form of deafening silence after a series of promising meetings.

Preethi Kasireddy, on What I wish I knew about fundraising as a first-time found

I’ve compiled here a list of by-no-means-exhaustive warning signs that can help you identify Angels that aren’t right for you. Most of the warning signs below assume that you’ve done your due diligence on the investor to ensure that (s)he is relevant to your business in the first place. Most Angel investors don’t like being just a cheque-book for your business — they also want to add value to your business along the way. Possibly through feedback on your product, introduction to clients, or connections to potential hires. If you’ve reached out to an Angel investor who knows she’s not the right fit, you may see all of the warning signs below.

Asks about long-term business metrics for your six-month old business.

Typically Angel investors that have not started businesses themselves are well-versed in how a large MNC operates but not as much about what a fledgling business with a few thousand dollars in the bank looks like. They may naively ask for metrics (such as customer life-time value) that don’t matter to a fledgling startup. They could mean well, but accepting that money could lead to a host of issues in the near future. Imagine struggling to meet your MNC investor’s expectations when trying to sign on the next paying customer, or deploy the next version of your app. As an entrepreneur, it is not your job to educate your Angel investor.

Is a bit too interested in your valuation and exit plans.

Counting the money too soon can ruin your business before you start.

Someone told this Angel how much money she made on an early-stage investment and our man can’t wait to make 10x on his money. Valuation, any valuation, for an early-stage business is meaningless. By default, unless it is illegal in your jurisdiction for some reason, use a convertible note (like Y-Combinator’s SAFE document) to raise your early investments.

Everyone wants an exit — heck, likely even you do! — but no one wants an investor that is in it only for the exit. Such Angels will become a pain in all the rear ends when your runway is short, and will likely try to force you to an acquihire or lowball deal to help save the $20,000 he put into your business. Be polite when showing them the door.

Is stuck on terms of the deal. Or suggests weird Board structures.

Non-standard terms in any term sheet at any round is a warning sign. Typically, Angel term sheets are overridden when you raise a Seed round from professional VCs. Most Angels who have done multiple deals understand this and won’t make a big deal of terms. Be wary of those that do.

This is rare, but once in a while you will come across an Angel that wants to see a Board with 5 Directors and an Independent Director. In those rare cases, it is ok to walk out — polite discourse be damned. While having a governance framework is beneficial, even critical at the appropriate time, it is nothing but an expensive distraction at this point.

Doesn’t respect your views or your time.

Keep reminding yourself — no one knows your business like you do. Unless you’re building the 175,345th copy of Groupon, this is probably true. If an Angel investor who’s just heard your 10-min pitch starts telling you how to run your business, you know you’re signing up for a rough ride if you take his money.

Sometimes, the investor’s perception of you is easier to observe: did he arrive late at the meeting without a viable excuse or apology? Did she get constantly distracted by her phone?

Unwilling to talk about his/her past investments.

Most investors love to talk about their past investments. Some like to talk only about their successes. Others like to talk about their failures. Still others talk about the ones they missed. No good Angel investor is unwilling to talk about past investments at all. Of course, there are exceptions and idiosyncratic characters — but most Angels haven’t earned their way into being idiosyncratic yet.

Offers to introduce you to other Angels without first committing himself/herself.

Of course, some Angel do invest with a friend or colleague — and that’s perfectly alright. Saying “I really like what you guys are doing but I typically invest with my friend, Shark. Do you mind if I connect you to him?” is legit. But if the investor looks like he’s trying to introduce you to as many people as possible to give himself more comfort around the investment, let him/her know as politely as you can that you don’t have too many spots left.

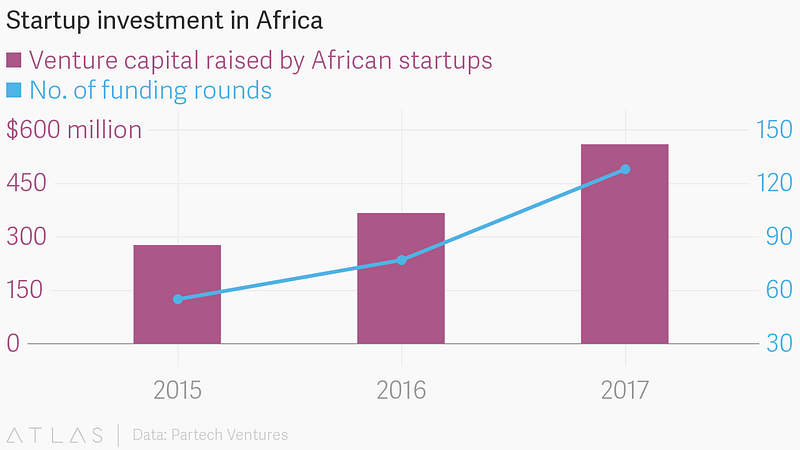

Read also:Five African Startups Secure Investment From Founders Factory Africa

Finding the right Angel investor for your business is often as critical as finding the right cofounder. Your business is the most vulnerable in the first year and the wrong investor can have a lasting impact on your long-term viability. To maximise the impact of the time you put into fundraising, start early, build ongoing relationships, and don’t be afraid to ask for introductions. And, like all good salesmen, always be closing.

Saptarshi Nath is formerly a co-founder @OvercartInc

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

He could be contacted at udohrapulu@gmail.com