The Central Bank of Kenya (CBK) has reportedly ordered commercial banks to ration dollars after a shortage in the US currency. Banks have already started imposing these rations. A number of currency traders and importers say they have imposed a daily cap on dollar purchases as firms struggle to obtain adequate forex to meet their obligations, according to Business Daily. Sources say that some businesses are restricted to a daily cap of $50 000.

CBK says they have been also working on containing panic buying of the dollar and protecting reserves amid the global outlook that has worsened in the recent months following Russia’s invasion of Ukraine.

CBK Governor Patrick Njoroge

“One USD (dollar) purchase transaction used to take one working day. However, due to the daily cap manufacturers now have to plan 2-3 weeks in advance, depending on the dollar requirements for specific consignments,” Mucai Kunyiha, the chairperson of Kenya Association of Manufacturers (KAM).

“Planning in advance for foreign currency payments has resulted in an increase in working capital,” Kunyiha added.

Multiple banks have reportedly accepted the order by CBK. However, none have come forward to admit it to the media because of fear of reprisal from CBK.

KAM said that the shortage is causing an increase in the cost of doing business and panic buying of the forex.

Materials ordered by importers last year amounted to Sh399.62-billion ($3.5-billion), according to data shared by CBK.

“We now have to start placing orders one or two months earlier to get our deals done in time,” said a CEO of a manufacturing firm who, according to Business Daily, did not want to be identified for fear of punishment by the CBK.

US lender JP Morgan said it was quite a stretch to complete some client transactions in Kenya due to dollar liquidity constraints.

“Clients are informed that due to ongoing issues with sourcing sufficient US dollars liquidity in the Kenyan market in recent days, client requests for repatriation of Kenyan shilling via JP Morgan’s AutoFX program may be delayed,” Morgan said.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Desperate times call for desperate measures. This is the condition of things for multifarious digital lending startups which are on the brink of extinction following a new wave of killing regulations that would require them to hold a banking license to survive in Kenya.

central bank of kenya

In a latest move to beat the regulations, “Branch”, a famous mobile loan app in Kenya has earned regulatory approval to purchase majority ownership stake in a local bank, Century Microfinance Bank Limited.

Branch International Limited was authorized to purchase 84.89 percent of Century Microfinance Bank Limited’s issued share capital, according to a gazette notice dated Friday, May 7.

“Pursuant to the provisions of section 46 (6) of the Competition Act, 2010, it is notified for general information that in exercise of the powers conferred upon the the Competition Act, the Competition Authority has authorised the proposed transaction as set out,” the gazette notice reads in part.

Here Is What You Need To Know

One of the conditions for the approval of the purchase is that Branch and Century must both keep the terms negotiated with the borrowers on all loans in their respective loan books at the time of the purchase.

Branch and Century will both, also, keep their current performing and non-performing loans in compliance with their terms until they expire, so that the terms do not violate the provisions of the Competition Act №12 of 2010.

The switch is part of Branch’s larger strategy to move into the formal lending market.

The decision came a month after parliament passed a bill aimed at regulating mobile loan rates and defaulted credit care in order to protect borrowers from abusive lending.

Century Microfinance Bank is a microfinance institution that specializes in providing financial services to micro, small, and medium enterprises. Branch is one of the most popular apps in Kenya on the Google Play Store.

In 2012, the Central Bank of Kenya granted Century Microfinance Bank a deposit-taking microfinance institution license to provide a full range of financial services, including savings accounts and credit facilities.

The Central Bank of Kenya (Amendment) Bill of 2020, although purports to curb the steep digital lending rates that have plunged many borrowers into a debt trap as well as predatory lending, also extends its tentacles, by its operation, to all financial technology services in Kenya.

In October 2020, more than 337 unregulated digital mobile lenders and micro financiers were also barred from forwarding the names of loan defaulters to Kenya’s credit reference bureaus (CRBs). This followed a statement from the Central Bank of Kenya (CBK) in a circular released in March 2020 that digital and credit only lenders will no longer submit credit information on their borrowers to Credit Reference Bureaus (CRBs).

In the statement, CBK explained that the withdrawal is in response to numerous public complaints about misuse of the Credit Information Sharing System (CIS) by the lenders and particularly poor response to customer response.

The Implications Of The New Law On Digital Financial Services Startups In Kenya

Licensing of Digital Financial Services Companies/Startups

The first direct implication of the new law on digital financial services startups in Kenya is that the Central Bank of Kenya will now possess recognized power under the law to issue operational licenses to startups desiring to provide services related to a digital financial product, financial product advice, market, administrative or management services or credit under a regulated credit contract in Kenya.

What this means is that startups that offer digital banking services will now also have to maintain a minimum authorized capital of five billion shillings ($46.4 million), which may be increased by such amount as shall be determined by CBK, unless the contrary is stated by the CBK.

In other words, all the rules regulating commercial banks and other financial institutions will now have to apply to startups offering digital financial services under the law.

FinTech covers all areas of human interaction with commodity-money circulation and uses a large class of IT technologies. Source: — Aspilos.com

Regulation of Interest Rates Charged Users Of Digital Lending Services

Even though digital lenders in Kenya may still be allowed to lend, the law would, however, see that they do not charge interests on their loans excessively. This is because the CBK could now determine the maximum rate of interest they may charge their customers.

Implied Lifting Of The Ban On Credit Lending Startups

Another implication of the new law would also be to terminate the ban on credit lending startups in Kenya which obtain CBK’s license as regards submitting credit information on their borrowers to Credit Reference Bureaus (CRBs).

Thus, with renewed power to report customers for blacklisting to the country’s central credit information sharing center, it is only safe to say that the risks associated with their business model have become, once again, more manageable.

The latest move to control the activities of digital lenders follows the removal of legal cap on commercial lending rates by the Central Bank of Kenya in March 2020.

The cap, established far back in 2016 and which set interest rates chargeable by banks at 4%, was intended to address the issue of the affordability of credit for small enterprises and working people, as they had complained for years that high interest rates had locked them out of accessing credit.

Its removal in March 2020 has, however, resulted in the proliferation of digital lenders, who seek to take advantage of the business opportunities it offered.

Some of the complaints include that digital lenders do not provide full information to borrowers on pricing, punishment for defaults and recovery of unpaid loans.

For instance, before now Tala, Branch, which are among top players in the mobile digital lending market in the country, offered interest rates of 152.4 percent and 132 percent per year respectively.

Digital lenders have also been accused of abusing personal information collected from defaulters’ mobile phone contacts list to bombard relatives and friends with messages regarding the default and asking third parties to enforce repayment.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Up until January 2021, Kenyans are invited to comment on a new policy document launched by the Central Bank of Kenya. This is the latest move by the east African country to promote the use of cashless transactions. Consequently, through the policy document, the bank is asking the providers of digital financial services in the country to work together and encourage adoption.

CBK governor, Patrick Njoroge

“Though the industry moved to enable interoperability of mobile wallets in 2018, this is limited to only P2P payments, and is yet to be expanded to both merchant and agent interoperability and even to work seamlessly at P2P,” noted the draft of the Kenya National Payments System 2021–2025 report.

Here Is What You Need To Know

The CBK’s latest policy document outlines proposals on tap that could change the way FinTechs and mobile payments firms operate.

According to the draft report, Kenya’s National Treasury and Planning agency is finalizing a digital finance policy to ensure that financial services are digitally connected.

The central goals include open infrastructure, consumer protection, regulation and more.

“Although … Kenya’s payments landscape has undergone dramatic changes in the last ten years, there are still areas with considerable opportunities and improvement such as growth of the electronic payment instruments,” the report indicated.

Kenya digitalise financial services Kenya digitalise financial services

Digital payment acceptance in the country has grown over the last five years, with several new products launched from collaborations between industry players, the report stated. One game-changer was the introduction of government-to-person (G2P) payments, which enabled mobile payments for public services.

The anticipated release of the National Integrated Identity Management System (NIIMS) and the Huduma Namba “will provide a key impetus to further deepen the adoption, safety and robustness of digital payments,” the report said.

CBK data indicates P2P payments surged 87 percent between February and October, with 2.8 million new mobile users.

The move was intended to encourage the use of mobile payments as a way to help prevent the spread of COVID-19.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

More than 337 unregulated digital mobile lenders and micro financiers have been barred from forwarding the names of loan defaulters to Kenya’s credit reference bureaus (CRBs). The CRBs say the number of firms allowed to blacklist defaulters with the bureaus has dropped to 2,254 in September from 2,332 in May last year.

CBK governor, Patrick Njoroge

Ban On Digital Lenders

According to the Central Bank of Kenya (CBK) in a statement released in March this year, digital and credit only lenders will no longer submit credit information on their borrowers to Credit Reference Bureaus (CRBs).

In the statement, CBK explained that the withdrawal is in response to numerous public complaints about misuse of the Credit Information Sharing System (CIS) by the lenders and particularly poor response to customer response.

“The withdrawal is in response to numerous public complaints over misuse of the CIS (credit information sharing) by unregulated digital and credit-only lenders, and particularly their poor responsiveness to customer complaints,” the CBK said in an earlier statement.

Under the new rules, only defaults above Sh1,000 will be shared with CRBs. Borrowers who had been blacklisted for lower amounts are now required to be cleared unconditionally.

Firms such as Tala and Branch were locked out at a time when the bulk of accounts negatively listed with the CRBs — Metropol, TransUnion and Creditinfo International — are linked to mobile digital borrowers.

In March this year, Kenyan Parliament considered a petition to launch investigations into the operations of digital money lending institutions over claims of exploitation of borrowers.

Kenya digital lending startups Kenya digital lending startups

Implications for Digital Lending Startups In Kenya:

This will continue to be a hard time for startups desiring to set up a money lending business in Kenya anytime soon. Without having the power to report customers for blacklisting to the country’s central credit information sharing center, it is only safe to say that their business model has become entirely a highly risky one.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

The coronavirus has not ended but the Central Bank of Kenya appears to be running out of patience. Once again, if you had borrowed money from any of the country’s commercial banks and default in repaying, your name risk being published in the public domain, in this case, the country’s Credit Reference Bureaus (CRB). The Bureaus had been on months-long break in compliance with the directive of the Central Bank of Kenya to cushion borrowers against the impact of the coronavirus, but is now back.

CBK governor, Patrick Njoroge

“ In terms of the measures that are ending, that I think is clear, so from October 1 the banks will begin accessing their borrowers, then you will have three months to regularize what you were not paying,” said Njoroge during the post MPC briefing.

“The point here is to just emphasize that we are going back to the normal operations and that is where we will be come October 1,” he added.

Here Is What You Need To Know

CBK governor Patrick Njoroge said the measures that were implemented by the banks 6 months ago to cushion distressed borrowers from the harsh economic environment occasioned by the coronavirus pandemic will end today.

CBK announced the suspension of CRB listing for defaulted loans in April 2020, with the relief from being blacklisted lasting for six months up to September 30.

This was part of the stimulus packaged announced by the bank regulator on March 25 to cushion borrowers where many Kenyans were facing pay cuts while about 1.7 million were issued with redundancy notices during the pandemic according to a survey by the Kenya National Bureau of Statistics.

On September 29, the Central Bank of Kenya announced that banks have restructured loans worth Sh1.12 trillion.

This represents 38 percent of the total banking sector loan book of Sh2.9 trillion by the end of August.

Personal and household loans topped the list with Sh271 billion reviewed since March.

Other sectors such as trade, manufacturing, real estate, and agriculture were offered relief of loans that amount to Sh849.9 billion.

According to the Central Bank of Kenya (CBK) in May, 2020, digital and credit only lenders will no longer submit credit information on their borrowers to Credit Reference Bureaus (CRBs).

In the statement, CBK explained that the withdrawal is in response to numerous public complaints about misuse of the Credit Information Sharing System (CIS) by the above-mentioned lenders and particularly poor response to customer response.

In March this year, Kenyan Parliament considered a petition to launch investigations into the operations of digital money lending institutions over claims of exploitation of borrowers.

Implications For Digital Lending Startups In Kenya:

This continues to be a hard time for startups desiring to set up a money lending business in Kenya anytime soon. Without having the power to report customers for blacklisting to the country’s central credit information sharing center, it is only safe to say that their business model has become entirely a highly risky one.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

The need to regulate activities of digital lenders operating in Kenya has come to the fore with calls by both operators and subscribers for a sort of formalization of the operations to create a transparent and accountable operating environment. This came even as the digital lenders have agreed that they are in support of plans by the country’s financial regulatory agencies, especially the central bank to regulate their industry amid concerns they are placing borrowers under increasing debt stress. Speaking on the development, the Digital Lenders Association said that regulations should be based on the digital lenders’ code of conduct. This according to them will promote transparency, best practices for debt collection, market-based pricing with no hidden fees.

Kenya has a relatively more developed digital lending ecosystem due mainly because the country embraced it earlier than others. It is among the first countries where digital lending, mostly using a mobile phone, went mainstream. The pioneering lenders came under the spotlight following complaints of exorbitant interest rates and bad collection methods. With dozens of apps offering short-term advances similar to payday loans, people who once borrowed mainly from family and friends are now being bombarded with advertisements for quick money and calls from debt collectors.

And because it is an unregulated system, there are no caps on interest rates, except those backed by banks that are supervised by the Central Bank of Kenya. In April, the central bank, which wants all the lenders properly supervised, blocked unregulated loan companies from some credit-reference services after public complaints that some firms were misusing information.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Are you a fintech startup in Kenya, not just a digital money lender? Are you worried by the recent proposal by the Central Bank of Kenya to regulate you like well capitalized commercial banks? You have got a chance, till August 11, 2020, to make your submission known to the National Assembly in Nairobi.

“The Departmental Committee on Finance and National Planning should investigate the operations of all mobile money lending platforms in the country with a view to stopping unregulated money lending and subjecting all non-compliant mobile lenders to applicable money lending regulations,” read the petition by MP when the proposal was first introduced in parliament in October last year.

Here Is What You Need To Know

The public has until August 11 to give their views on a proposed regulations that will empower the Central Bank of Kenya (CBK) to oversee the operations of digital financial service providers.

In a public notice, the National Assembly has asked interested individuals to email views to the clerk.

The Central Bank of Kenya (Amendment) Bill, 2020, although purports to curb the steep digital lending rates that have plunged many borrowers into a debt trap as well as predatory lending, also extends its tentacles, by its operation, to all financial technology services in Kenya.

The Implications Of The Proposed Law On Digital Financial Services Startups In Kenya

Implied Lifting Of The Ban On Credit Lending Startups

Once the new law is passed into law, its first implication would be to terminate the ban on credit lending startups in Kenya as regards submitting credit information on their borrowers to Credit Reference Bureaus (CRBs). Thus, with a renewed power to report customers for blacklisting to the country’s central credit information sharing center, it is only safe to say that the risks associated with their business model have become, once again, more manageable.

Licensing of Digital Financial Services Companies/Startups

Another direct implication of the proposed new law on digital financial services startups in Kenya is that the Central Bank of Kenya will now possess recognized power under the law to issue operational licenses to startups desiring to provide services related to a digital financial product, financial product advice, market, administrative or management services or credit under a regulated credit contract in Kenya.

What this means is that startups that offer digital banking services will now also have to maintain a minimum authorized capital of five billion shillings ($46.4 million), which may be increased by such amount as shall be determined by CBK, unless the contrary is stated by the CBK.

In other words, all the rules regulating commercial banks and other financial institutions will now have to apply to startups offering digital financial services if the bill becomes law.

The Bill is coming amid complaints that digital lenders do not provide full information to borrowers on pricing, punishment for defaults and recovery of unpaid loans.

Digital lenders have also been accused of abusing personal information collected from defaulters’ mobile phone contacts list to bombard relatives and friends with messages regarding the default and asking third parties to enforce repayment.

FinTech covers all areas of human interaction with commodity-money circulation and uses a large class of IT technologies. Source: — Aspilos.com

Regulation of Interest Rates Charged Users Of Digital Lending Services

Even though digital lenders in Kenya may still be allowed to lend, the law would however, if passed into law, see that they do not charge interests on their loans excessively. This is because the CBK could now determine the maximum rate of interest they charge their customers.

The latest move to control the activities of digital lenders follows the removal of legal cap on commercial lending rates by the Central Bank of Kenya in March 2020. The cap, established far back in 2016, which set interest rates chargeable by banks at 4%, was intended to address the issue of the affordability of credit for small enterprises and working people, as they had complained for years that high interest rates had locked them out of accessing credit.

Its removal in March this year has, however, resulted in the proliferation of digital lenders, who seek to take advantage of the business opportunities it offered. For instance, Tala, Branch, which are among top players in the mobile digital lending market in the country, offer interest rates of 152.4 percent and 132 percent per year respectively.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Going forward, if a Bill pending before Kenya ’s national parliament is passed into law, business will not be as usual for all digital lenders in the East African country. Not only would they have to play under the same rules as commercial banks, including having to seek the country’s central bank’s approval for new products and pricing, the amount they each charge their customers as monthly interest rates on borrowed facilities would now also be regulated.

“The principal objective of this Bill is to amend the Central Bank of Kenya Act to regulate the conduct of providers of digital financial products and services,” says a notice on the Bill.

“The Central Bank of Kenya will have an obligation of ensuring that there is fair and non-discriminatory marketplace access to credit.”

Here Is What You Need To Know

By the terms of the Central Bank of Kenya (Amendment) Bill 2020, the Central Bank of Kenya must approve every increase in digital lenders rates and other loan charges. Interests on non-performing loans must also, if the bill is passed into law, not be more than twice the defaulted credit.

This is the first major attempt by Kenya to regulate all digital financial services startups and companies operating in the country.

In a statement, late April, 2020, CBK explained that the ban is in response to numerous public complaints about misuse of the Credit Information Sharing System (CIS) by the above-mentioned lenders and particularly poor response to customer response.

In March this year, Kenyan Parliament also considered a petition to launch investigations into the operations of digital money lending institutions over claims of exploitation of borrowers.

The Implications Of The Proposed Law On Digital Financial Services Startups In Kenya

Implied Lifting Of The Ban On Credit Lending Startups

Once the new law is passed into law, its first implication would be to terminate the ban on credit lending startups in Kenya as regards submitting credit information on their borrowers to Credit Reference Bureaus (CRBs). Thus, with a renewed power to report customers for blacklisting to the country’s central credit information sharing center, it is only safe to say that the risks associated with their business model have become, once again, more manageable.

Licensing of Digital Financial Services Companies/Startups

Another direct implication of the proposed new law on digital financial services startups in Kenya is that the Central Bank of Kenya will now possess recognized power under the law to issue operational licenses to startups desiring to provide services related to a digital financial product, financial product advice, market, administrative or management services or credit under a regulated credit contract in Kenya.

What this means is that startups that offer digital banking services will now also have to maintain a minimum authorized capital of five billion shillings ($46.4 million), which may be increased by such amount as shall be determined by CBK, unless the contrary is stated by the CBK.

In other words, all the rules regulating commercial banks and other financial institutions will now have to apply to startups offering digital financial services if the bill becomes law.

The Bill is coming amid complaints that digital lenders do not provide full information to borrowers on pricing, punishment for defaults and recovery of unpaid loans.

Digital lenders have also been accused of abusing personal information collected from defaulters’ mobile phone contacts list to bombard relatives and friends with messages regarding the default and asking third parties to enforce repayment.

FinTech covers all areas of human interaction with commodity-money circulation and uses a large class of IT technologies. Source: — Aspilos.com

Regulation of Interest Rates Charged Users Of Digital Lending Services

Even though digital lenders in Kenya may still be allowed to lend, the law would however, if passed into law, see that they do not charge interests on their loans excessively. This is because the CBK could now determine the maximum rate of interest they charge their customers.

The latest move to control the activities of digital lenders follows the removal of legal cap on commercial lending rates by the Central Bank of Kenya in March 2020. The cap, established far back in 2016, which set interest rates chargeable by banks at 4%, was intended to address the issue of the affordability of credit for small enterprises and working people, as they had complained for years that high interest rates had locked them out of accessing credit.

Its removal in March this year has, however, resulted in the proliferation of digital lenders, who seek to take advantage of the business opportunities it offered. For instance, Tala, Branch, which are among top players in the mobile digital lending market in the country, offer interest rates of 152.4 percent and 132 percent per year respectively.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer.

At least 75 per cent of SMEs are facing closure by end of June due to lack of funds, CBK governor Patrick Njoroge has said. During a post-MPC briefing on Thursday, he said there is an urgent need to cushion them as they contribute hugely to the country’s employment and GDP.

central bank Governor Patrick Njoroge

“I wanted to underscore the urgency of … putting in place the credit guarantee scheme,” central bank Governor Patrick Njoroge told a virtual news conference. “This is extremely urgent. We cannot do this as business as usual.”

Here Is All You Need To Know

On Wednesday, the Monetary Policy Committee retained the base lending rate at seven per cent in its latest review.

Njoroge, who heads the committee, said measures adopted in March and April to cushion the economy from the Covid-19 effects were having the intended effect.

Growth is expected to worsen in the second quarter of the year (April-June), with the imposition of more stringent travel and transport containment measures, particularly in transport and storage, trade, and accommodation and restaurants.

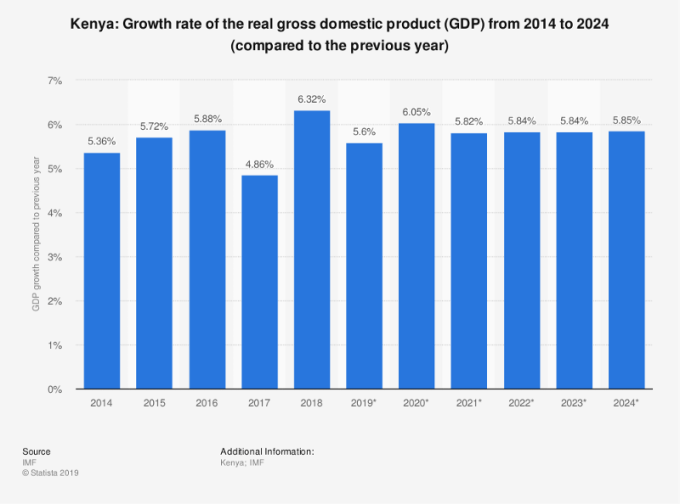

As a result, real GDP growth in 2020 could slow to about 2.3 per cent from 5.4 per cent in 2019, Njoroge said.

On Wednesday, the committee backed the Economic Stimulus Programme announced by government to cushion vulnerable citizens and businesses from the adverse effects of the pandemic and enhance economic activities.

The measures are expected to be implemented expeditiously in 2020–21 financial year and will focus on key sectors including agriculture and food security, tourism, manufacturing, education , health , ICT and MSMEs.

“The MPC concluded the current accommodative monetary policy stance remains appropriate and therefore decided to retain the Central Bank Rate at seven per cent,” Njoroge said.

He said the committee will continue to closely monitor the impact of the policy measures so far as well as developments in the global and domestic economy and stands ready to take additional measures as necessary.

In April, the MPC lowered the CBR from 7.25 per cent in light of the continuing adverse economic outlook.

This was after a reduction to 7.25 per cent from 8.25 per cent in March.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

Digital money lenders in Kenya may have to look for an alternative market elsewhere outside Kenya as the country’s central bank has banned unregulated digital and credit-only lenders from the country’s credit information sharing (CIS), and introduced new rules that compel savings and credit societies (Saccos) to share credit information on their members with the credit reference bureaus to control rising bad debts in the sub-sector.

CBK Governor Patrick Njoroge

“With immediate effect, CBK has withdrawn the approvals granted to unregulated digital (mobile-based) and credit-only lenders as third party credit information providers to CRBs,” the regulator said in a statement.

“The withdrawal is in response to numerous public complaints over misuse of the CIS by the unregulated digital and credit-only lenders, and particularly their poor responsiveness to customer complaints.”

Here Is What You Need To Know

Ban On Digital Lenders

According to the Central Bank of Kenya (CBK), digital and credit only lenders will no longer submit credit information on their borrowers to Credit Reference Bureaus (CRBs).

In the statement, CBK explained that the withdrawal is in response to numerous public complaints about misuse of the Credit Information Sharing System (CIS) by the above-mentioned lenders and particularly poor response to customer response.

In March this year, Kenyan Parliament considered a petition to launch investigations into the operations of digital money lending institutions over claims of exploitation of borrowers.

Implications for Digital Lending Startups In Kenya:

This is going to be a hard time for startups desiring to set up a money lending business in Kenya anytime soon. Without having the power to report customers for blacklisting to the country’s central credit information sharing center, it is only safe to say that their business model has become entirely a highly risky one.

Extension of Repayment Period For Credit Facilities

Banks in Kenya have also restructured Sh9.9 billion loans between March 18 and March 30 on request of customers following the effect of Covid-19 pandemic.

A number of banks in March announced a loan holiday for small and medium enterprises (SMEs) and personal banking customers to cushion them against the economic disruptions caused by the Coronavirus disease (COVID-19).

“Borrowers should endeavour to reach out to their banks, explain to them how the pandemic has disrupted your cash flow and repayment of the loan you may be servicing, don’t wait,” said CBK Governor Patrick Njoroge.

Following the outbreak of the disease, which has so far disrupted many businesses across the country, CBK in mid-March, ordered Kenyan lenders to provide relief to borrowers on their personal loans, with loans eligible from March 2 extended by up to one year.

Speaking at an online post-Monetary Policy Committee press briefing on Thursday, the governor noted the far-reaching effects of the virus on Kenya’s economy noting that it will slow growth in 2020 to 2.3 per cent or even below from 5.4 per cent growth recorded last year.

In support of his argument, the governor said already sectors such as the accommodation, transport and agriculture have contracted by 50, 10 and 2 per cent respectively. However, sectors such as ICT and health are expanding.

“We expect 2021 to be a rebound, currently the estimate is 6.4 per cent,” Njoroge told a virtual news conference. The current account deficit is seen at 5.6 per cent of GDP in 2021 compared with 5.8 per cent in 2020, he said.

The governor also expects Diaspora remittances to slow in the month of April by between 12–15 per cent down from an increase of 229 million US dollars witnessed in March. Kenyans living in the United Kingdom, United States of America sent home the bulk of the money, other destinations such as the United Arab Emirates, South Africa and Mauritius recorded a decline.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer