Digital Service Tax Claims Its Latest Victim In Kenya. Startups Stranded

No more signing on of Kenyan startups wanting to set up online shops. This is what Bulgarian web-hosting firm, SiteGround, has said via its Twitter handle as it cancels out Kenya from its list of patronizing countries. The company said it had been frustrated by Kenya’s newly introduced Digital Service Tax regime, which levies 1.5% digital service tax on all digital marketplaces operating in Kenya.

The site is popular among Kenyan startups because it offers them a chance to set up their online presence on low budgets.

“Due to new local regulations (mostly tax-related), we have recently stopped offering new sign-ups for a number of countries and Kenya is one of them,” SiteGround replied to a Kenyan web designer, who had unsuccessfully sought to sign up an account for a client, via Twitter.

“Complying with said regulations would be expensive for us, making offering our product there not feasible for us.”

The Sofia-based company, which has data centers in the United States, the United Kingdom, Germany, the Netherlands, Singapore, and Australia, provides domain registration, business solutions, and email hosting for free or at a low cost.

Shrinking Kenya’s Startup Space?

Last month, global social network giant, Twitter, ditched Nigeria, Kenya, Egypt and South Africa — Africa’s leading startup ecosystems — for Ghana over its choice of African operations’ headquarters.

Read also:Why Twitter Chose Ghana Ahead of Nigeria to Set Up Africa Office

Analysts claimed choosing Ghana over other countries such as Kenya may not be unconnected with Kenya’s digital service tax which took effect from January 1st, 2021.

“The way the taxes have been structured lately, the likely effect is that they will lower the eventual tax throughput to the KRA,” Kamotho Njenga, secretary-general for ICT Association of Kenya, said.

“The taxman may think they are getting innovative, but they may be doing a disservice to their bottom line collection because not every investor will go public on why they have … left a given destination.”

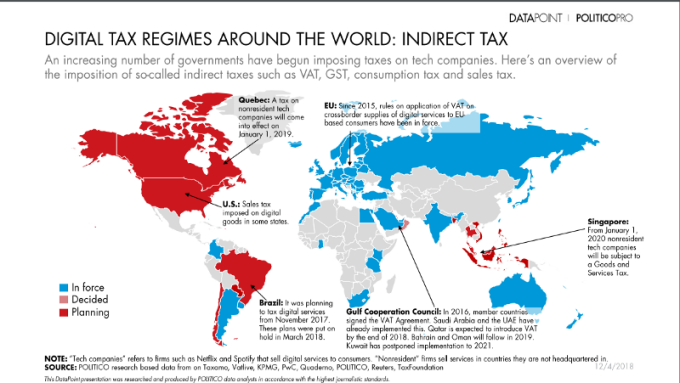

In addition to the 1.5% digital service tax, digital marketplaces (ecommerce websites) must also pay (if eligible) Value Added Tax of 14% in accordance with the provisions of Section 5(8) of the country’s Value Added Tax Act of 2013.

The 2020 Value Added Tax (Digital Market Supply) Regulations provide that failure to pay the relevant taxes will make defaulters liable to restriction of access to their websites in Kenya until such taxes are paid.

The Kenya Revenue Authority (KRA) plans to register 1,000 businesses “deriving or accruing profits” from Kenya through a digital marketplace in the next six months through June, 2021, with a target of raising Sh5 billion ($46m) in the process.

Which Digital Marketplaces (Ecommerce) Are To Pay Tax?

Under the regulations, taxable services made through a digital marketplace include electronic services under Section 8(3) of the Value Added Act and: –

- Downloadable digital content including downloading of mobile applications, e-books and movies;

- Subscription-based media including news, magazines, journals, streaming of TV shows and music, podcasts and online gaming;

- Software programs including downloading of software, drivers, website filters and firewalls;

- Electronic data management including website hosting, online data warehousing, file-sharing and cloud storage services;

- Supply of music, films and games;

- Supply of search-engine and automated helpdesk services including supply of customized search-engine services;

- Tickets bought for live events, theaters, restaurants etc. purchased through the internet;

- Supply of distance teaching via pre-recorded medium or e-learning including supply of online courses and training;

- Supply of digital content for listening, viewing or playing on any audio, visual or digital media;

- Supply of services on online marketplaces that links the supplier to the recipient, including transport hailing platforms;

- Any other digital marketplace supply as may be determined by the Commissioner.

Read also: 75% Of Kenya’s Small, Medium Businesses May Collapse Before By June — Central Bank Of Kenya

What Criteria Are To Be Used In Determining Whether The Digital MarketPlace Is Required To Pay VAT?

Under the new regulations, a digital services company (Ecommerce) rendering taxable services through a digital marketplace shall be required to register for VAT in Kenya if:

(a) the online services are offered by a business located outside Kenya to an end user in Kenya in business-to-consumer transactions.

(b) the business entity is doing business in Kenya and any of the following situations occur:

(i) the user of the services is in Kenya; or

(ii) the payment made to the business entity staying outside Kenya by the user, for the rendering of the internet-based services, starts from a Kenyan bank registered or authorized in the country; or

(iii) the user of the internet-based services, even though he/she resides outside Kenya, has business, residential or postal address in Kenya.

In any case, where the business entity staying outside Kenya to offer the business-to-customer services is not able to register for tax under the simplified Kenyan VAT registration framework, it shall appoint a tax representative to account for the VAT on their digital services.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer