Africa Check in conjunction with Facebook, expands its local language coverage as part of its Third-Party Fact-Checking Programme.

Facebook’s reality checking project depends on input from the Facebook people group, as one of numerous sign Facebook uses to raise possibly false stories to certainty checkers for survey

Facebook), today with Africa Check reported that it has included new neighborhood language support for a few African dialects as a major aspect of its Third-Party Fact-Checking program – which surveys the exactness of news on Facebook and expects to decrease the spread of deception.

Propelled in 2018 crosswise over five nations in Sub-Saharan Africa, including South Africa, Kenya, Nigeria, Senegal and Cameroon, Facebook has banded together with Africa Check, Africa’s first free certainty checking association, to grow its neighborhood language inclusion over:

Nigeria, in Yoruba and Igbo, adding to Hausa which was at that point bolstered

Swahili in Kenya

Wolof in Senegal

Afrikaans, Zulu, Setswana, Sotho, Northern Sotho and Southern Ndebele in South Africa

As indicated by Kojo Boakye, Facebook Head of Public Policy, Africa, stated: “We keep on trying huge interests in our endeavors to battle the spread of false news on our stage, while building strong, sheltered, educated and comprehensive networks. Our outsider reality checking system is only one of numerous ways we are doing this, and with the extension of neighborhood language inclusion, this will help in further improving the nature of data individuals see on Facebook. We know there is still more to do, and we’re focused on this.”

Remarking, Noko Makgato, official chief of Africa Check, said “We’re excited to grow the munitions stockpile of the dialects we spread in our work on Facebook’s outsider truth checking program. In nations as semantically different as Nigeria, South Africa, Kenya and Senegal, certainty checking in neighborhood dialects is imperative. In addition to the fact that it lets us actuality check increasingly content on Facebook, it likewise implies we’ll be contacting more individuals crosswise over Africa with confirmed, believable data.”

Facebook’s reality checking project depends on criticism from the Facebook people group, as one of numerous sign Facebook uses to raise possibly false stories to certainty checkers for survey. Neighborhood articles will be reality checked close by the confirmation of photographs and recordings. In the event that one of Facebook’s reality checking accomplices distinguishes a story as false, Facebook will demonstrate it lower in News Feed, essentially lessening its dispersion.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

Nigeria’s Access Bank, which has recently gone into a merger with Diamond Bank has recently announced plans to launch an innovative portal that will allow customers to process their loan application online. The bank granted up to N37 billion loans to its SMEs customers in 2018 alone.

The Bank has also organized a sensitization programme for players in the creative industry with a view to making access to the CBN Creative Sector Intervention Fund, CIFI, more seamless.

The Central Bank of Nigeria, CBN, recently rolled out the CIFI as part of its efforts to open up the creative sector and improve its contribution to the economy.

The CBN has already earmarked N20 billion for disbursement in the first phase of the exercise with three to 10 years payback plan and a maximum of nine percent interest rate per annum.

Fidelity Bank

Fidelity Bank has recently announced a partnership with PwC Nigeria, a tax and advisory services company, to fund SMEs with N12 million grant in its Fidelity Small and Medium Enterprises (SMEs) Funding Connect Series.

The bank also said that, at the final series of the event, three finalists will be rewarded a grand sum of N2 million (1st position) and N1 million each for the 2nd and 3rd positions respectively. The Executive Director Shared Services and Products, Mrs. Chijioke Ugochukwu, disclosed this at the Fidelity SME Forum on Inspiration FM, Lagos.

The event which will kick off in Lagos on August 7, 2019, is focused on funding.

“The event is focused on funding because in the course of our work, we have realised that aside capacity issues, funding is a major issue. So we try to create a platform where the supply and demand sides of the equation would meet. Supply meaning the fund providers while the demand side means the founders/entrepreneurs,’’ she said.

The entire series will be in Lagos, Port-Harcourt, later this year and in Kano early next year and we anticipate that across the three series we will have at least 3,000 participants, 10,000 SMEs, that will come in contact with 60 founders, 60 entrepreneurs and in total we are looking at N12 million in grants and across the entire series of the six breakout session in networking cocktails.

The three capacity building sessions will be with fund providers, founders, on one hand, model entrepreneurs, founders and subject matter experts.

“The five finalists get a chance to pitch the entire forum on August 7. So the five finalists will be live at the event and they will speak to the house about their ideas and three winners will emerge. The first prize will be N2 million and two consolation prizes of N1 million each.”

“To attend the event, you are to register by visiting the dedicated website for the bank which is smeconnect.fidelitybank.ng and of course also via the event app which you can download from Google Play stores for android phone users and the RS app store for Apple users.”

Nigerian banks’ lending pattern pointing to financial exclusion of SMEs

First Bank Of Nigeria

If you own micro, small or medium agricultural enterprise, this loan facility is a special intervention fund provided by the CBN to support your business. You get this loan at a low-interest cost and enjoy long-tenured repayment structure; to assist your business in enhancing capacity for employment generation, growth, and economic development.

Trusted customers of FirstBank seeking to expand their agri-businesses using low priced credit facilities as made possible under the scheme can benefit from this loan.

Management experience of at least 3 years in the enterprise to be funded is required.

Benefits

Interest rate: 9% (all-in), no other fee can be charged.

The credit facility is available either as term loan or overdraft.

Required Documents

Formal application for a Credit Facility.

Certificate of Incorporation.

Memorandum and Article of Association (MEMART).

Board Resolution to Borrow.

Feasibility Study/Business Plan.

Who Can Apply

SMEs with at least 3yrs Mgt Experience (Max obligor limit of N50m).

GTB

Fashion Industry Credit

Tailored to your Fashion business, designed for growth. In line with the CBN creative industry loan, the bank has created a single-digit interest rate loan at 9% to provide entrepreneurs in the fashion industry with all the financing they need to grow their business.

The loan can be:

Up to N5 Million for your fashion business.

Single-digit (9% per annum) interest rate at 0.75% per month

No fees

Flexible repayment plan spread over 360 days

Customers can access up to 50% of the average annual turnover

Food Industry

The bank also grants loan to the food industry. Now you can get all the financing you need with the GTBank Food Industry Credit, which offers you a single-digit interest rate loan of just 9% per annum.

The loan can be:

Up to N2 Million

9% per annum interest rate (0.75% monthly)

Flexible repayment plan spread over 180 days

Zero Fees

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Group to benefit from efforts to give millions of Nigerians without bank accounts access to financial services.

A subsidiary of MTN Nigeria has been awarded a license by the country’s central bank that would allow it to provide financial services, the telecoms firm said on Monday.

Nigeria announced last year that it would allow telecom companies to provide banking services, aiming to give millions of Nigerians without bank accounts access to mobile money services, a policy that has been successful in Kenya.

SA’s MTN Group, which owns a majority stake in MTN Nigeria, said at the time it would apply for a mobile banking license in Nigeria and planned to launch the service in 2019. Since then, MTN Nigeria listed in Lagos in May in a 2-trillion naira ($5.6bn) debut, which turned it into the exchange’s second-largest stock by market value.

MTN Nigeria’s CEO, Ferdi Moolman, said on Monday its Yello Digital Financial Services (YDFS) unit had been granted a “full super-agent” license by the Central Bank of Nigeria.

“Through the network established by YDFS, MTN is in a position to broaden the availability of financial services for the underserved across the country. This marks a very important first step in leveraging our infrastructure to scale our fintech initiatives,” said Moolman.

“We have also applied for a payment service bank license, which will enable us in time to offer a broader and deeper range of financial services to those communities and we remain hopeful we will receive approval shortly,” he said. He did not give specifics.

MTN runs Nigeria’s biggest mobile phone network serving about 56-million people.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

Founders have to be resilient and thick-skinned. Prepare yourself to exhaust your network of investors, and accept the fact that fundraising is going to take time, even if that’s a hard pill to swallow.

Securing a fresh injection of investment capital can drastically accelerate your startup’s growth, so it’s good to know that there’s no shortage of money up for grabs these days. According to a recent venture capital report from Magnitt, nearly US$800 million in investments were made in the MENA region last year.

But just because the money is out there doesn’t mean the fundraising process will be a breeze. The reality is that investors are picky and often guided by strict criteria to fit their investment thesis. When you seek them out, most will reject you, that’s just part of playing the game. Luckily, there are some rules that can make the process a bit more predictable. Odds are you get a “no”.

Taking into consideration the media’s infatuation with writing articles on multimillion-dollar investments into startups on a daily basis, it can look like these deals happen overnight. They don’t.

In fact, most entrepreneurs will openly tell you about what a struggle the fundraising process can be. Author and business guru Steve Schmitz puts this in perspective in the context of his own fundraising journey.

He wrote: “We raised $40 million of equity from 63 investors. We contacted more than 1,000 prospects. That’s about 6%. That means 94% of the people said no.”

Blackstone CEO Steve Schwarzman had the same 6% hit rate when starting out, too, and his company now manages more than $500 billion of capital.

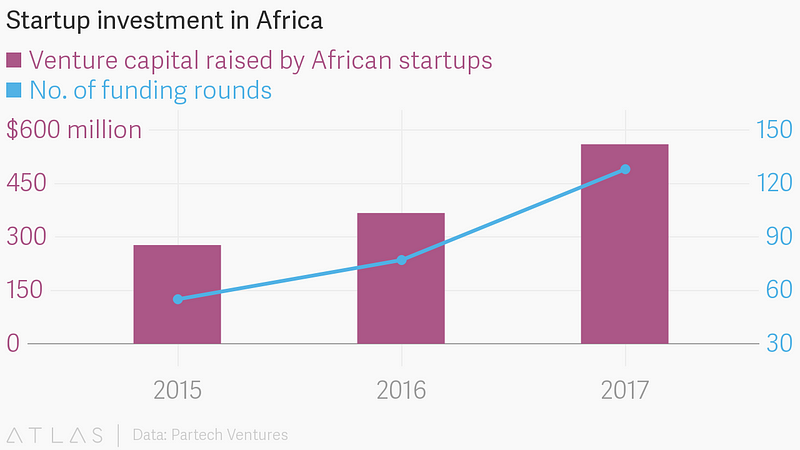

Startup investment in Africa (2015–2017). Credit: Quartz/Partech Ventures

Think of it this way: let’s assume you’re raising a $600,000 seed round, and the average check size for your investors participating in the round is $100,000. This would mean you’d need six investors in on your round. If you operate under the 6% rule, you would have to meet with 100 investors to close your round.

Keep in mind that the 6% rule holds up for qualified investors who cut checks of the size you’re seeking at companies that are at the same stage you are. If you hit up the SoftBank $100 Billion Vision Fund for a $50,000 unit size, that wouldn’t count as an investor. Being told “no” is normal.

Famed speaker and author Tim Ferriss has an excellent podcast episode about just how critical it is to learn from every “no” we get. One of his guests mentions that she heard “no” at breakfast, at mid-morning coffee, at lunch and twice during the afternoon, before ever getting to dinner (where she heard it again).

Founders have to be resilient and thick-skinned. Prepare yourself to exhaust your network of investors, and accept the fact that fundraising is going to take time, even if that’s a hard pill to swallow.

How To Secure The Magic 6%

The 6% rule can apply in any part of the world, but some places will have to stretch outside their borders to make it work. In the MENA region, fundraising often forces founders to go outside their hometowns and home countries to complete fundraising. Online crowdfunding platforms have been instrumental in removing geopolitical borders stateside, and this will surely benefit the 344 million households in the developing world, too. Regardless of where your investment comes from, you can set workable goals to achieve success under the 6% rule.

Here’s How:

1. Use your unit size to set your investor target list size.

It’s easiest to break the total investment you’re seeking into smaller units for starters. Think back to the example above of the $600,000 investment. If you were aiming for $50,000 units, the 6% rule would require you to talk with 200 qualified investors (assuming each investor bought one unit in the worst-case scenario), or 100 investors at $100,000 unit sizes. You can use the rule and your unit sizes to determine the size of your investor target list.

Egyptian startup Swvl did this when it secured five investors for its $8 million Series A round in April 2018, and the Series B that followed at the end of the year.

Once you determine your list size, create a pitching schedule. Assuming it’s not Ramadan -which tends to bring the investment world to a screeching halt- start pitching five times each week for 20 weeks. Factor in eight weeks of researching targets and eight weeks for term sheets to close the deal, and you’re looking at 36 weeks minimum from start to finish.

2. Be ready with prepped materials.

I always have the staples ready to go during fundraising time. Read Venture Deals by Brad Feld to get your lingo down, and understand the basics, it’s VC 101. Then, put together a pitch deck, a term sheet, a clean cap table, a data room, accurate and up-to-date financial statements, and a financial forecast. Preparation is key to secure and close deals, and doing this homework in advance shows that you know what you’re doing.

Verifiable forecasts coupled with a concrete plan to reach them is what secured Wuzzuf its $8 million investment.

This Egyptian startup bootstrapped its job site and recruiting platform in the aftermath of the 2011 Egyptian revolution.

Having survived the toughest economic conditions, the company is now one of the fastest-growing internet companies in Egypt, with more than 250 employees expecting to help 1 million people get hired by the end of this year.

3. Lose the materials when it’s more about relationships.

Pitch decks are great for angel group presentations and pitch competitions, but I’m not a big fan of bringing all of that to one-on-one pitches. If you’re meeting an investor at your nearest Costa Coffee, pitch without materials.

Building a personal connection is what got Jamalon its $10 million Series B investment, not a stack of papers.

Founder Ala Alsallal credits the mentorship he received from Fadi Ghandour, Aramex founder and Wamda Capital chair, with his success, saying relationships made the difference in getting him where he is today. So put away your computer, break the ice, share your story, and dive into your big vision. If the person shows interest, you can talk about materials.

4. Maintain a pipeline, and take your time.

Organize your resources and manage the investors you talk to in a customer relationship management system or a spreadsheet, just as you would a sales pipeline.

Take a note from the Sandler Training book, and use the “submarine trick,” which is inspired by World War II movies in which crews handle attacks on their submarines by closing the door to each compartment behind them.

Salespeople should close each step completely as they go, that way there’s no risk of needing to turn around, and go back on something that’s already been decided. Never forget that a signed term sheet is engagement, not a marriage.

Definitive documents take time to prepare. Wires take time to transfer. Plan ahead so you don’t run out of cash before you complete your raise.

Ultimately, you won’t fundraise for your startup overnight. And rejections will come. Period. Just remember that even if 94% of investors say “no,” 6% will give you the “yes” you need to make the grind pay off.

Zach Ferres is the CEO, Coplex, a Venture Builder that partners with industry experts and innovative enterprises to start high-growth tech companies.

The startup recently announced a $2.5M equity financing round. The Series Seed Round was led by DFE, the family office of Bennett Dorrance of Campbell Soup fame; and AZ Crown, the family office of Insight Enterprises Co-Founders Tim and Eric Crown.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Fintech is where the money is. Africa’s fintech companies have raised $320 million in funding since January 2015 and the ecosystem has surged 60% in the last two years. Africell understands these statistics and is willing to use its wide reach to give it a shot. With $100 million funding from the OPIC, the US government’s private investment fund, the African telecom company is more than ready to continue the disruption game.

Here Is The Deal

The Uganda-headquartered Africell’s new funding is more than $100 million and part of this would be used by the company to expand access to telecommunications in Africa.

The countries Africell is targeting are Uganda, DRC, Gambia and Sierra Leone.

Apart from this $100 million funding, Africell has set aside $300 million to spend on a new market like Angola within the first year of commencing business if they secured a license.

Africell would bid to become the fourth operator in Angola, which was expected to reissue a tender in the next two months after the original tender for the license was annulled in April.

A larger part of the $100 million would be spent on fintech.

The unbanked population is what Africell is targeting here.

Global fintech funding rose to $111.8 billion in 2018, up 120 percent from $50.8B in 2017 and that is a huge opportunity Africell is hoping to tap into.

To make this happen, Africell is looking at expanding its fintech services, such as mobile payments, micro-insurance, and micro-finance.

Mobile money payments, pioneered in Kenya, have expanded rapidly in other African nations where many people do not have bank accounts.

The 18-year-old company has 15 million subscribers across its four African operations.

The Game Is In Competing Profitably And Not Just Expanding

“We are looking only at markets where we can make a difference,” said Africell founder and chief executive Ziad Dalloul indicating this included Angola and Zimbabwe.

He said Angola was attractive because the country’s state-owned Angola Telecom had a large market share that could be vulnerable to a more aggressive private operator like Africell.

“Day one, we can just change the whole thing…drop market prices, expand into rural areas, provide faster, better service on internet. These are the things we know how to do. So that’s why we are keeping an eye on Angola,” he said.

And Africell Is Turning Its Eyes On Fintech For Reasons More Business Than Charitable

“No space has quite the potential impact of the fintech space when it comes to impact — and profits — in Africa, with startups operating such platforms able to significantly address the major issue of financial exclusion on the continent and thus promote development in all sorts of other areas,” saysDisrupt Africa co-founder Tom Jackson.

Nigeria led the investments in 2018 with 58 startups raising $94,9 million, followed by South Africa with 40 businesses that raised $59,9 million, and Kenya was third.

Fintech investment was still the most popular, bringing in 39.7% of total funds “South Africa, Nigeria and Kenya remain the main three markets, with 141, 101 and 78 active ventures respectively, accounting for 65.2% of Africa’s fintech startups,” Jackson says.

US fintech investment for 2018 more than doubled to $52.5B, from $24B in 2017, across a record 1,061 deals.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

The total money owed by Nigerian governments, whether federal or regional now stands at more than $69 billion (N24.97trn) in the first quarter of 2019. This is more than the value of all money (GDP) made by Ghana last year.

A Break Down Of The Figures

Figures from the Nigerian Bureau of Statistics say Nigerian States and Federal Debt Stock data as at 31st March 2019 showed that the country’s total public debt portfolio stood at N24.95trn.

Further disaggregation of Nigeria’s total public debt showed that N7.86trn or 31.51% of the debt was external while N17.08trn or 68.49% of the debt was domestic.

Similarly, total domestic debt was N3.97 trillion with Lagos state accounting for 13.64% of the total domestic debt stock while Yobe State has the least debt stock in this category with a contribution of 0.68% to the total domestic debt stock.

Remember that Congo recently got a major bailout from the International Monetary Fund (IMF) to help it service its debt obligations with its creditors.

Government debt as a percent of GDP for African countries, 2017. Source: IMF, 2018. Regional Economic Outlook

This bailout potentially set a precedent for other nations struggling under the weight of large debts to China.

It appears that what IMF has succeeded in doing is to alert other countries borrowing from China that China would never cut off any percent from any borrowed sum, but may instead, prolong the period of repayment.

Many observers see Congo as a test case for the IMF. A number of African countries facing unsustainable debt resulting from commercial borrowing, a boom in Eurobond issues and years of Chinese lending on the continent are expected to turn to the IMF for help in the coming years.

This is even bound to grow more because sovereign debt financing is inevitable given that African countries budgetary resources are insufficient to finance their vast development agenda.

“The IMF is tacitly accepting that China will not take a haircut on debts to African governments,” said one banker, who has followed the negotiations.

The IMF is also advising Congo’s government to restructure high-interest debt it contracted with oil traders including Glencore (GLEN.L) and Trafigura despite a previous pledge to the Fund that it would not engage in oil-backed borrowing.

“I think they’ve learned their lesson as to the costs of these kinds of practices,” Alex Segura, IMF mission chief for Congo, told Reuters.

IMF Is Also Pitching Its Stakes And Leaving African Countries At Their Own Mercy

All that bailout would not just happen without a reciprocal deal. For instance, the IMF said in November that Congo’s government must take a series of steps before the lender agrees to a bailout, including reforms to improve governance and transparency, adjustments to the state budget. It’s also requested “explicit financing assurances,” including debt relief, from creditors before it considers a bailout.

With all these, African countries with heavy debt burdens may all be sitting on a time bomb.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Kenyans living abroad are sending more money back home than their counterparts living in Uganda, Tanzania, Rwanda, Burundi, South Sudan, and Ethiopia put together. World Bank data says Kenya’s Diaspora remittances in 2018 stood at Sh280 billion (about $2.7 billion), while a total of Sh242 billion was sent to the rest of Eastern Africa — comprising Uganda, Tanzania, Rwanda, Burundi, South Sudan, and Ethiopia.

However, this does not stop there. In the first five months of 2019, Kenyan Diaspora remittances stood at Sh118.9 billion, a 3.8 percent increase in the same period in 2018.

Here Are The Facts

A World Bank unit known as the Global Knowledge Partnership on Migration and Development prepared the report released in April 2019.

With these figures, remittances in Kenya have now become the biggest source of foreign exchange for Kenya, far more than Kenya’s tourism, tea, coffee and horticulture exports.

With these figures again, it means that in terms of contribution of remittances to the GDP of a country, Kenya’s now stands at (three percent), Uganda (4.5 percent) and Rwanda (2.4 percent) in the region, while Ethiopia saw the least contribution (0.5 percent) and Tanzania (0.8 percent).

This report is significant because it shows that between 2017 and 2018, the rate at which Kenyans sent money back home grew by 39%. The rate has even further increased in the first five months of 2019. Between January and May 2019, a total of Sh118.9 billion, representing a 3.8 percent increase on the same period in 2018, was sent back to Kenya

The money came from about 3 million Kenyans living abroad, many of whom have attained tertiary education and are working in the formal sector jobs.

North America, particularly the United States accounts for much of the Kenyans abroad remittances. At least, 45 percent of all the remittances came from that region. This is followed by Europe at about 23 percent while the rest of the world accounts for about 32 percent.

The US is a popular destination for Kenyans looking for greener pastures and further education, with the latter mostly remaining in the destination countries for work after graduation.

In recent years, however, the Middle East and China are also emerging as a choice destination for those looking for external work opportunities, in line with the rapid economic growth in these regions.

Why So Much Is Being Sent Back Home

Perhaps Kenyans are sending more back home because it has become easier to do so.

The Central Bank of Kenya has, for instance, identified the ease of sending money back home as a major factor in the sharp growth of Kenyans abroad remittances.

Local banks have entered partnerships with remittance service providers that allow them to handle larger volumes of inflows.

The expansion of the popular M-Pesa service beyond Kenya’s borders is also helping, with direct cash transfers on mobile making it easier for the millions who actively use mobile money to receive money instantly from relative abroad.

One of the biggest impediments to inward African remittances has over the years been identified as cost, partly attributable to the lower than global average penetration of formal banking in the continent.

The World Bank report shows that remittances to sub-Saharan Africa remain the most expensive across the different regions of the world.

“The cost was the lowest in South Asia, at five percent, while sub-Saharan Africa continued to have the highest average cost, at 9.3 percent.

“Remittance costs across many African corridors and small islands in the Pacific remain above 10 percent,” said the World Bank in the report.

It also helps if a country has a well-developed banking sector, which opens up formal channels of remitting money back home and reduces the cost of doing so.

Ease of movement of capital also helps. Countries that do not restrict the movement of hard currency are, therefore, likelier to attract foreign investment flows, which encourage the setting up of more robust support infrastructure for remitting money.

Kenya Is Fifth On the Continent As A Whole

Looking at the wide continent, Kenya was fifth last year in terms of volume of money remitted.

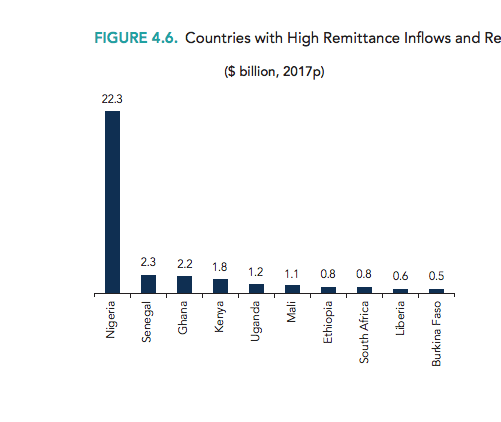

Egypt and Nigeria, which are two of Africa’s most populous countries and boast of a large diaspora, led the continent with inflows of Sh2.98 trillion ($28.9 billion) and Sh2.5 trillion ($24.3 billion) respectively last year.

Morocco and Ghana saw remittances of Sh760 billion (7.38 billion) and Sh391.4 billion ($3.8 billion) respectively to also come in ahead of Kenya on the list.

In East Africa, remittances stood at Sh128.4 billion for Uganda, Sh44.3 billion for Tanzania, and Sh42.4 billion in Ethiopia. Rwanda and Burundi had remittances worth Sh23.7 billion and Sh3.7 billion respectively, while there was no data available for South Sudan and Somalia for 2018 in the World Bank report.

“Remittances to sub-Saharan Africa were estimated to grow by 9.6 percent from $42 billion in 2017 to $46 billion in 2018. Projections indicate that remittances to the region will keep increasing but at a lower rate, to $48 billion by 2019 and to $51 billion by 2020,” World Bank noted in the report.

“The upward trend observed since 2016 is explained by strong economic conditions in the high-income economies where many sub-Saharan African migrants earn their income.’’

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Analysts have started exploring opportunities inherent in the proposed single currency for the West African region; The Eco. It could be recalled that leaders of the 15 member states of the Economic Community of West African States (ECOWAS) met in Abuja, Nigeria, and formally agreed on the name of the planned common currency the “ECO” The currency according to a release from ECOWAS Secretariat Abuja, would be based on a flexible exchange rate regime, coupled with a monetary policy framework focused on tackling inflation.

Observers say there seems to be a sense of urgency in this latest efforts, maybe being buoyed by the recently signed Africa Continental Free Trade Agreement (AfCTA). This is because the target launch date for Eco has been postponed several times; in 2005, 2010 and 2014; since the concept first arose in 2003. Now the Economic Community of West African States (ECOWAS) is planning to launch the currency in 2020, with member states agreeing to name it the ‘ECO’ there seem to be a new sense of urgency.

Reports indicate that governments in the region are keen on more integration and a single currency will facilitate trade, lower transaction costs, and payments amongst ECOWAS’ 385 million people.

Currently, eight of ECOWAS countries i.e. Benin, Burkina Faso, Guinea-Bissau, Ivory Coast, Mali, Niger, Senegal, and Togo jointly use the CFA franc while the remaining six members have their own independent currencies.

Some analysts are of the view that the single currency if properly implemented will improve trade by allowing specific countries to specialize at what they are good at, and exchange it for other goods that other countries in the bloc produce more efficiently.”

A report by the African Development Bank Group (Afdb) indicates that the 2020 deadline for the single currency will most like be postponed again unless the region can align with its monetary and fiscal policies.

Countries are required to meet a ten convergence criteria, set out by the West African Monetary Institute (WAMI), by the 2020 deadline. The primary four beings: a budget deficit of not more than 3%, an average annual inflation rate of less than 10%, Central Bank financing of budget deficits should be no more than 10% of the previous year’s tax revenue and gross external reserves worth at least three months of imports.

The six secondary criteria to be achieved by each member country are: Prohibition of new domestic default payments and liquidation of existing ones, tax revenue should be equal to or greater than 20 percent of the GDP, wage bill to tax revenue equal to or less than 35 percent, public investment to tax revenue equal to or greater than 20 percent, a stable real exchange rate and a positive real interest rate.

However, reports indicate that although countries may meet the criterion by the deadline they fall behind thereafter thus posing the main difficulty in inconsistencies.

As at today, only five countries, viz; Cape Verde, Ivory Coast, Guinea, Senegal and Togo of the region’s fifteen countries currently meet the single currency’s criteria of a budget deficit not higher than 4% and inflation rates of not more than 5%, as noted by Charlie Robertson, chief global economist at Renaissance Capital.

Additionally, while ECOWAS says the integration will be gradual as countries meet the criteria, it’s unlikely that a 2020 launch date is feasible as there is no significant progress in the design, production, and testing of the currency notes.

Given that various economies in the region are at “dramatically different levels of development,” the leadership of ECOWAS is being unrealistic in both its timing for the currency’s launch and expectations of what it might achieve, Robertson says. “You’ve got very different levels of debt, interest rates, and budget deficits. Trying to align these countries to operate as one is extremely difficult,” he says. “What currency policy is right for two such divergent countries like saying Ghana and Burkina Faso?”

There is also the glaring disparity in the economic size of Nigeria in the region. For example, Nigeria is 67% of ECOWAS’ GDP, so really this isn’t a single currency for 15 countries, this is the Nigerian Naira plus a few countries.

How the leaders hope to close all these gaps between now and next year remains to be seen.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

West African businesses can now benefit from seamless trading across West African borders. This is because the Heads of State and Government of countries in the region have finally adopted ECO as the name of the single currency to be issued in January 2020.

Here Are Things To Know About The New Currency

The currency would fully be in use from January 2020.

The currency would be used for trade across West African countries.

The ECO will work this way: shops, hotels, and restaurants, particularly in the larger cities in Ghana, for instance, may now display prices in both the Ghanaian Cedi and ECO currency and many are likely to accept payment in ECO. However, as the official currency is Ghanaian Cedi, no establishment is under no obligation to accept payment in any other currency apart from Cedi.

Consequently, the introduction of ECO may serve as an alternative to the legal tenders in the countries of West Africa who have met all the requirement to start using ECO.

In simple terms, for people living in Nigeria, this means that you can now carry, in addition to Naira, ECO, and ECO can be used to buy or sell anywhere in Nigeria as long as the other party is willing to accept so.

The West African Monetary Agency, the body of ECOWAS in charge of money and finance across the region has said the currency would be based on a flexible exchange rate regime, coupled with a monetary policy framework focused on checking inflation.

In Which Countries Can You Use The Currency?

The currency can be used across the whole of West African countries from January 2020. However, ECO would be used only in the countries that have met the requirement for its use. That is, for any country in the West African sub-region to start using ECO, it must first meet the following requirements:

It must have a single-digit inflation rate at the end of each year

It must have a fiscal deficit (liabilities) of no more than 4% of the GDP

Its central bank must have deficit-financing of no more than 10% of the previous year’s tax revenues

The country’s gross external reserves must give import cover for a minimum of three months.

Additionally, each country must:

Prohibit new domestic default payments and liquidate existing ones. (That is, all domestic debts must be paid off first)

Have a tax revenue base which should be equal to or greater than 20 percent of the GDP.

Have its wage bill to tax revenue equal to or less than 35 percent.

Have its public investment to tax revenue equal to or greater than 20 percent.

Have a stable real exchange rate.

Have a positive real interest rate.

Right now, it appears Ghana is the only country in West Africa that has met all of the above requirements.

“The single currency for 2020 vision is: let’s find two, three or four countries that are ready. Once they meet up, we follow through with the others cascading in,”said Ken Ofori-Atta, Ghana’s finance minister, at a meeting of West African ministers in Accra recently.

The seriousness of the ECOWAS leaders on ECO is buried in this communique issued after the 55th Ordinary Session in Abuja:

‘‘The single currency would be issued in Jan. 2020.’’ the communique reads. “We have not changed that but we will continue with assessment between now and then. We are of the view that countries that are ready will launch the single currency and countries that are not yet ready will join the programme as they comply with all six convergence criteria.”

The leaders also instructed the commission to work with West African Monetary Institute and the central banks to accelerate the implementation of the revised roadmap with regard to the symbol of the single currency.

“It [the communique]further directs the commission to ensure implementation of the recommendations of the meeting of the ministerial committee held in Abidjan on June 17 and June 18 as well as preparation and implementation of the Communication Strategy for the single currency programme. The Authority takes note of the 2018 macroeconomic convergence report. It noted the worsening of the macroeconomic convergence and urges member states to do more to improve on their performance in view of the imminent deadline.”

Most of the eight currencies used in the 15 countries of the West Africa region are not convertible. Convertibility is defined as the possibility to freely exchange a country’s currency for foreign currencies. Where they are convertible, their rates are highly volatile ($2 in the morning, $5 dollars in the afternoon) Hence, ECO will help to address the issue of multiple currencies and exchange rate fluctuations that affect intra-regional trade.

West African countries have the least developed financial sectors in the world. The ratio of bank credit to GDP there is very low. There is no much money in their financial markets, through which money can easily flow across the region. Unlike the Eurozone where payment can be made and settled by banks using Euros and cheques. Payment and settlement systems in several West African economies are still marked by the predominance of cheques in noncash payments. In 2013, for instance, the whole money available in the West African regional market only represented 13% of GDP of the whole of the West African countries put together — this is like 8.5% of GDP for Ghana and 21% for Nigeria, against an average of about 65% for Sub-Saharan Africa. Hence, ECO will open up the market a bit.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

“References to the currency of Zimbabwe shall, with effect from the 24th of June 2019 be construed as references to the form of legal tender and the electronic currency with which the term Zimbabwe dollar is.’’

The above statement is from the Zimbabwean government as the country begins a new journey to reshape its bad currency.

Henceforth, international and regional currencies such as the rand, US Dollar, Botswana Pula, and British Pound will no longer be acceptable in Zimbabwe as legal tender. Zimbabwean Finance Minister has gazetted mandatory and sole usage of the Zimbabwe Dollar for all local transactions.

‘It is hereby notified that the Minister of Finance … has made the following regulations; Zimbabwe dollar to be the sole currency for legal tender purposes,” reads a part of the Statutory Instrument issued today.

“With effect from the 24th June 2019, the British pound, United States Dollar, South Africa rand, Botswana Pula and any other foreign currency whatsoever shall no longer be legal tender alongside the Zimbabwe dollar in any transactions in Zimbabwe.”

The Statutory Instrument states that “references to the Zimbabwe dollar are coterminous with references to the following and to no other forms of legal tender or currency — (1) the bond notes and coins, 2.) the electronic currency that is to say the RTGS$”.

Zimbabwe has been using multiple currencies since 2009 when hyper-inflation ravaged the country’s local unit.

In 2016, the central bank of Zimbabwe introduced bond notes which traded at par with the US Dollar but have quickly been losing value.

Zimbabwe Is Poised To Have Its New Currency Now Or Never

Earlier this year, Zimbabwe introduced a new currency, the RTGS$ with President Emerson Mnangagwa and the Finance Minister, Mthuli Ncube, saying in the past few months that Zimbabwe was set to have a substantive currency of its own.

It also says the current bond notes and RTGS$ are at par with the Zimbabwe dollar. This has been viewed as an effective introduction of a new currency for Zimbabwe, which is currently battling a severe financial crisis.

Free For All

Companies such as Old Mutual have been accused by allies of President Mnangagwa for fueling informal market currency rates which have spiked out of control. Early Monday morning, the bond notes were trading around 1:10 against the US Dollar while the official interbank market rate is around 1:6.2.

Other listed companies in Zimbabwe have been facing accounting challenges and several have sought permission from the Zimbabwe Stock Exchange to delay financials following the introduction of the RTGS$ in February this year.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.