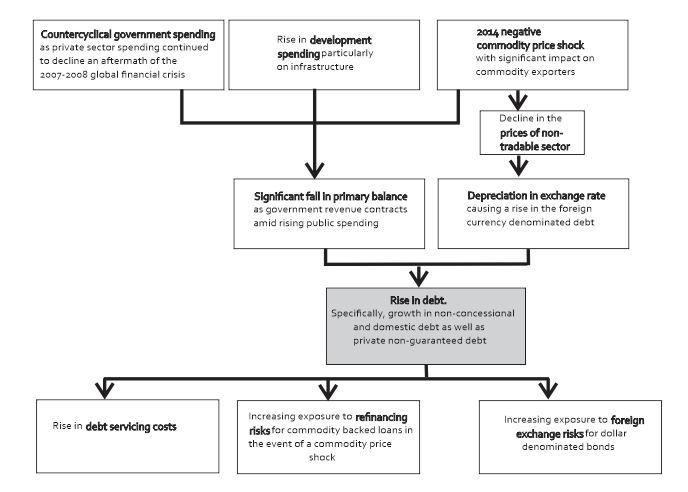

Debt Ridden Nigeria Needs to Borrow More Threatening Fiscal Flexibility

Faced with the trilemma of low oil prices and revenue, galloping inflation, and health crisis as a result of a resurgent Covid-19 pandemic, Nigeria will be borrowing more and facing tough economic choices in 2021 and the years ahead. Several factors are going to push Nigeria’s public debt higher in 2021:A resurgence in Covid-19 cases leading to a new wave of lockdowns in Europe and Nigeria; Weak oil prices and deep OPEC production cuts; Macroeconomic uncertainty; With the Nigerian account balance likely to remain in deficit for the year, one of Africa’s biggest economies will be forced to rely more on debts and grants to shore up its failing revenue.

Weakening flexibility

Analysts see this as threatening the fiscal flexibility of the country of more than 200 million people, as “high fiscal deficits are complicating monetary policy,” according to the International Monetary Fund (IMF). “The interest payments to federal government revenue ratio remained high at about 58% (21% at consolidated government level) while the debt-to-GDP ratio reached 29% of GDP in 2019,” the IMF added. Nigeria’s debt levels are much lower than those of its peers, and so an increase in the short term should not pit the government in danger.

Read also:How Nigeria’s Bank of Industry Sealed Landmark $1 billion Syndicated Term Loan

The IMF predicts that Nigeria’s GDP will drop by 4.3% in 2020 before returning to growth of 1.7% in 2021. It projects that growth will then rise to 2.5% for the next few years after that.

Nigeria plans to spend at least 24% of its 2021 N13.5trn ($35.7bn) budget on debt servicing. It will raise an additional N4.28trn in new borrowings to fund next year’s budget, thus pushing public debt to about N35trn over a four year period.

President Muhammadu Buhari presented the 2021 spending plan to Nigeria’s lawmakers on 8 October, explaining the country’s challenges: “The 2021 budget deficit (inclusive of government owned enterprises and project-tied loans), is projected at N5.2trn. This represents 3.6% of estimated GDP, slightly above the 3% threshold set by the Fiscal Responsibility Act of 2007.”

Read also:Why Central Bank of Nigeria Revokes Licenses of Seven Payment Service Providers

“It is, however, to be noted that we still face the existential challenge of the coronavirus pandemic and its aftermath. I believe that this provides a justification to exceed the threshold as provided for by this law. The deficit will be financed mainly by new borrowings totalling N4.28trn, N205.15bn from privatisation proceeds and N709.69bn in drawdowns on multilateral and bilateral loans secured for specific projects and programmes”, said Buhari.

COVID-19 and weaker oil price push public debt higher

Nigeria’s debt stock stood at N31trn on 30 June 2020, according to the debt management office. The new borrowing pushes the debt profile of the cash-strapped government to N35trn.

“Covid-19 and weaker oil price will push public debt higher,” despite reforms, according to Razia Khan, the chief economist for Africa and Middle East at Standard Chartered. “Debt service as a percentage of revenue remains a concern,” Khan said.

Nigeria’s B2 negative credit rating reflects the country’s increasing exposure to fiscal and external shocks because of its very weak government finances that are constrained by an extremely narrow revenue base that hinders fiscal consolidation, according to Moody’s Investors Service, in its annual report.

Read also:Nigeria’s President Buhari Signs Long-Awaited Petroleum Industry Bill

“After this year’s economic contraction, Nigeria’s deficit will remain high and debt levels will continue to rise quickly, albeit from a moderate level,” said Aurelien Mali, Moody’s vice-president and senior credit officer. “The country’s weak institutions and governance framework also constrain the credit profile and have significantly affected both economic growth and the government’s fiscal strength,” he explained.

Additional credit challenges include, according to the Moody’s report include the following: Political risks around the conflict with Islamist militant group Boko Haram; Potential attacks on oil infrastructure in the Niger Delta;Growing income inequality.

Year-on-year oil production is expected to be negative at least in the first half of 2021 due to deep OPEC cuts, as well as new lockdowns and restrictions. Therefore, the Nigerian government will be looking to make significant progress in reducing its oil dependency.

Roadblocks ahead:

Obstacles in Nigeria’s near-term outlook include: An uncertain foreign-exchange (FX) environment; constrained productivity; Cautious private-sector investors; Socio-political threats; High inflation.

KPMG, for instance, expects Nigeria’s (FX) environment to remain under pressure and to be exacerbated by lower FX earnings in 2021 . The country is in a tough spot and still has multiple exchange rates and continues to experience FX illiquidity.

Analysts at FSDH Capital say that Nigeria’s foreign reserves are under pressure: “Limited forex inflows due to Covid-19 exerted pressure on external reserves in the year”; “Lower inflows from crude oil intensified in the second quarter when oil price fell significantly”; “Capital inflows reducing due to foreign investment inflows that dipped by 50.9% year on year to $7.15bn in 2020H1 from $14.6bn in 2019H1.”

With rising imports and capital outflows that led to growth in demand for foreign currency and the overvaluation of the naira, KPMG sees liquidity remaining a challenge in 2021.

“[A] fair-value estimation at N422/$1 [reflects] a 9% overvaluation of the real effective exchange rate. Fair value may improve but rates will still be misaligned in 2021. Liquidity is low due to the pressure on foreign reserves and sharp fall in capital importation by -78% in Q2 2020 (QoQ). Liquidity will remain challenged given oil price outlook and capital flows,” KPMG said.

A frantic central bank last month allowed diaspora remittances to be withdrawn in dollars and sold anywhere, including the black market, in a new policy that sought to improve liquidity in the FX market, with the hopes that it would strengthen the naira in the parallel market.

Stringent policy environment, constrained productivity

Ahead is the possibility of a stringent policy environment that could potentially constrain productivity in the economy. KPMG sees a “volatile, uncertain, complex and ambiguous policy environment” as having a negative impact on the overall growth in the economy.

It continues: “The nature, speed, volume and magnitude of change is not predictable e.g. rising inflation and low aggregate demand. Lack of clarity resulting in multiple and conflicting interpretations,” as well as “lack of predictability in issues and events make it difficult to see future outcomes or make decisions,” are seen as making it “difficult to see future outcomes or make decisions; a complex and intricately interwoven forces that defy the traditional cause and effect analysis.”

Monetary policy: “outlook and expectation”

With the need to drive economic recovery, the Monetary Policy Committee (MPC) will likely cut the benchmark rate in 2021, say analysts at FSDH Capital. “The MPC will also be concerned about the misalignment of interest rates in the fixed-income market. This could further support rate cuts in 2021,” FSDH Capital said.

Credit growth, despite persistent high inflationary pressure

Despite structurally high inflation, the Economist Intelligence Unit projects that the Nigerian central bank will prioritise credit growth in its monetary stance. “A low interest rate environment points to further devaluations of the naira, with the current account remaining in deficit over 2021, further adding to inflationary pressure and impeding an economic recovery. A meaningful rise in oil prices from 2022 will lay the groundwork for quickening medium-term real GDP expansion,” it said.

This was originally published in the Africa Report

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry