It’s no secret that small and medium-sized businesses (SMBs) are challenged every day to balance the need to innovate with the reality that their workforce is already being stretched to its limits. To deliver an exceptional customer experience, small teams must figure out how to accomplish big things, but in a short amount of time and with limited resources.

Small businesses

For SMBs facing these struggles, taking a mobile-first approach can be a real game-changer in terms of optimizing overall business operations. From arming the entire workforce with the information they need to get the job done to acting as a critical force multiplier when free hands are few, mobile devices and apps can dramatically transform workforce productivity. However, there’s a right way and a wrong way to deploy mobile if you want to maximize capabilities and minimize cost as the business scales. That’s why we’ve developed this quick playbook to outline four key considerations for your business.

The way we think about work has drastically evolved over the past 10 years. Today, getting the job done means being able to take calls, respond to emails, collaborate with colleagues, collect data and access applications — and all of this needs to work equally well in remote settings. Entrepreneurs simply need tools that support an on-the-go workstyle and can’t be tethered to their desks if they want the business to scale as it thrives or adapts to socially distanced work.

Choose the right phone for your growing business

Smartphones are indispensable for SMBs. Leveraged effectively, they can drive significant lifts in workforce productivity and job satisfaction. However, many smaller companies have not harnessed the potential of mobile, adopting a fragmented Bring Your Own Device (BYOD) approach that makes it difficult to manage devices or deploy apps consistently across their teams. By taking a mobile-first approach to technology deployment, businesses can not only make their core mobile communications and collaboration capabilities more effective and integrated, but they can also introduce entirely new capabilities that drive greater workforce productivity.

Identifying, deploying or developing the right mobile applications that enable your teams to communicate, collaborate and track performance should be a major focus of your mobile-first strategy. Today, virtually all of the core desktop productivity applications have powerful mobile versions — from Microsoft Office 365, to Google Workspace (formerly known as G Suite) to line-of-business applications like Salesforce. Make sure your team has full access.

Messaging, collaboration and file-sharing applications are also hugely beneficial. It’s highly likely your team is already using one or more on an “unofficial” basis. Getting everyone on the same platform (and ensuring that it is secure) will help break down barriers and boost knowledge sharing. Canvasing the team to find out what they currently use and what capabilities they need is a great starting point. Lastly, find opportunities to innovate. Take a look at the existing tasks and workflows that are slowing your team down. It’s very likely that mobile can help. In fact, there’s probably already an app for it.

Be sure to check out Samsung AppStack, our one-stop-shop for best-in-class software, with discounted subscription pricing.

Select a device that lets you do more

When you consider just how much you and your team rely on your smartphones, it’s important to make sure you have a device that doesn’t slow you down. In today’s competitive market, 24/7 availability is a must — a single missed opportunity could make or break the business. It makes economic sense to invest in mobile tech that maximizes your productivity.

Screen size matters, too. With extra screen real estate, you can master multitasking, allowing you to hold a call, search for information and then grab and send screenshots, all while still on the line. Lastly, a powerful smartphone can actually replace the PC for many mobile workers, eliminating the need to purchase and manage laptops or desktops that rarely get used. When you do need a desktop, you can connect your Galaxy smartphone to a monitor, keyboard and mouse through Samsung DeX.

Have a team of frontline workers who need devices that can stand up to tough, real-world environments? Check out our lineup of rugged phones and tablets.

Shore up security to protect your data assets as you grow

While large enterprise hacks often grab the headlines, SMBs are increasingly becoming a target for sophisticated hackers, and mobile attacks are at the heart of this growing problem. Two thirds of organizations reported security concerns regarding the amount of mobile data used by their organization, according to Verizon’s latest “Mobile Security Index.”

Achieving an enterprise-grade security posture doesn’t have to be overly complicated or come with an enterprise price tag anymore. Defense-grade mobile security platforms like Samsung Knox take the guesswork out of protecting employee phones for resource-constrained businesses where the CEO, sales or human resources person may also be IT. Investing in mobile device management (MDM) pays off. A robust MDM solution can ease management and deployment with frictionless out-of-the-box setup, preconfigured apps tuned to the needs of the business and security settings that protect company data and IP. All of the leading MDM tools integrate closely with Samsung smartphones, and we also offer an affordable cloud-based enterprise mobility management solution of our own called Knox Manage.

While the benefits of mobility are clear, without an overarching strategy, costly missteps can derail the business. By building a plan with key productivity, availability and security needs at the forefront, SMBs can work anywhere to ensure they never miss a call and can move quickly on opportunities that will fuel growth.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Small businesses have been Bring Your Own Device pioneers since before BYOD became an acronym. Without large IT departments or equipment budgets, small business staff naturally use their own computers and smartphones to work when and where they need to. Sometimes there’s a formal mobility strategy, but just as often small businesses embrace BYOD organically, adding devices as they pop up.

At the same time, small businesses often look the other way when it comes to questions of security and managing BYOD access to their applications and networks. But avoiding mobile device management (MDM) is not necessarily the best approach. Taking responsibility for other people’s smartphones seems like a tall — and expensive — order, but it’s not: There are MDM solutions for small businesses that increase BYOD smartphone security without breaking the bank.

Today’s smartphones are pretty secure to begin with. Smartphone manufacturers got to watch the entire PC revolution and learned from the mistakes of those who came before. A major goal of MDM tools is simply to keep those smartphones secure, mostly by trying to override the weakest link in most security: the end user.

Small businesses can start by taking advantage of MDM features that automatically apply software updates, establish safe password and lock settings, and restrict application store choices to trusted stores. Enforcing some basic security settings doesn’t take a lot of configuration or control, and can give a huge boost in security. Just as importantly, it’s unlikely to be a cause for conflict. People want to do the right thing and when they make poor security choices, it’s usually out of ignorance or expedience rather than malice.

With basic MDM, for example, software updates can be applied soon after they’re released, which dramatically reduces the security risk from a smartphone. End users who don’t know how to install updates aren’t a problem anymore: MDM policies take over and ensure that devices are running the latest software releases. MDM tools can also provide status information on each device, so if something is wrong and software isn’t being updated, the IT manager can see this and make a visit to resolve the issue.

Mobile device management for beginners

Security isn’t the only reason for small businesses to adopt MDM — another is time savings. MDM enables email, Wi-Fi and virtual private network (VPN) configurations to automatically update on enrolled smartphones, reducing aggravation and confusion for BYOD users. As the small business networking, email and security environment changes, MDM tools make it easy to get those configuration changes pushed to devices. The end result is a happier user community, and fewer panicked phone calls if someone didn’t get the memo on a configuration change.

Choosing MDM solutions for small business

Small businesses interested in MDM should be thinking along the lines of four major criteria: price, features, management model, and platform support.

Price

Small businesses are rightly budget conscious, and the good news is that basic MDM definitely won’t be expensive. Most products are priced per user per month, and IT managers can easily find excellent choices for about $1-$2/user/month. Some products offer a “lite” version for free to get you started. Others bundle lite MDM with other products, so if you’re already buying an existing product (such as Microsoft Office 365), you may be able to activate a minimal MDM at no additional charge.

Generally, the larger the feature set, the higher the price, but even high-end MDM aimed at small business comes with a reasonable price tag and delivers a lot of value for pennies a day.

Features

It’s not necessarily true that a longer feature list is better than a shorter one, so IT managers should focus on the settings they’ll actually use. A dozen settings might be all that’s needed, along with reporting and lost device controls, to find the perfect MDM solution.

Small businesses should focus on features in four key areas: security (including lost device features such as remote wipe and remote lock); software and application controls (including patching and update settings); configuration push for email, networking and VPN; and simple reporting on device status and inventory.

Management model

Small business IT managers should start with cloud-delivered MDM solutions. It doesn’t matter how lightweight or simple an on-premise solution is — there’s virtually nothing a small business gains from running the MDM solution on their own servers.

The only exception to this is if Active Directory (AD) integration is a critical part of BYOD — which it rarely is for small businesses. However, if AD integration is really needed, then it’s usually easier to integrate an on-premises solution than try and link your AD to a cloud-based service.

Platform support

It almost goes without saying that whatever MDM you choose should support your users’ devices, but there are some constraints. All the common products work well for the two main smartphone operating systems: Android and iOS. However, small businesses that have Windows phones or BlackBerry devices will find a more limited selection — and higher prices. It’s not usually a big deal, but taking a survey of what smartphones people are actually using before picking an MDM solution is a good idea to avoid showstoppers later on.

Another platform issue to research is enrollment: how the MDM tool gets its client downloaded to the user’s smartphone. Many products have a variety of techniques that allow remote and self-service enrollment. IT managers responsible for highly mobile employees should make sure that getting smartphones connected to the MDM solution won’t be a burden or logistical foxhunt.

Cloud-based MDM solutions let small business IT managers gain big-business security for mobile devices without unwelcome complexity or high costs. Spend a little time now, and save a lot of time later by gaining better control of, and delivering better support for, smartphones and tablets.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Nigeria’s indefinite shutdown of its borders is taking its toll on small and medium scale businesses especially those that depend on cross border transactions. This was the findings of our Correspondent who visited two key border towns of Seme and Idiroko over the weekend. Many business people this Correspondent spoke with lamented that the closure has negatively impacted their businesses as what they thought would be just for two weeks or less has become indefinite leaving them in limbo.

Col. Hameed Ali, comptroller general, Nigeria customs service

Nobody seems to know when the border will be reopened even as the ECOWAS Parliament has urged the Nigerian government to reopen them. Speaking on the development, the Comptroller General of Nigeria Customs Service (NCS) Col. Hameed Ali (Rtd) said that Nigeria’s borders will remain closed until the country and its neighbours agree on existing ECOWAS protocol on movement. He stated that there is no specific time for opening the borders adding that “if they agree with us tomorrow on the existing laws, then we sign and update the existing protocol of transit, that’s all”. The Comptroller General informed that there is the likelihood that a meeting would soon take place as efforts are on top gear to have a round table discussion over the sticky issues relating to reasons why Nigeria had to shut its borders.

The Nigeria Customs Service said that it has made tremendous seizures of contraband products in recent times which necessitated government’s decisions to shut down the borders because it felt that efforts at growing the economy through import substitution is being sabotaged by people engaged in nefarious activities using the borders. Noting that by closing the borders, Nigeria was able to completely block the importation of contraband.

Reacting to the claims made by the Customs, some business people who spoke with this Correspondent said that it is a very wrong assumption by the Customs and the Nigerian government to see every product and business transactions across the borders are illegal or contraband because many businesses engage within the ambit of the law. They call on the federal government to resolve as soon as possible, whatever disagreement they have with the neighbouring countries and open the borders for businesses engaged in legal transactions.

Mr. Olufemi Johnson, a licensed customs agent said that what the government should do is to tighten the noose on smugglers while businessmen engaged in legal transactions should be allowed to continue with their businesses instead of such a blanket closure.

The Customs boss however insisted that the closure has helped Nigeria tremendously as it has led to the complete blocking of the influxes of illicit goods, and most importantly, stopped the exportation of petroleum product which is the biggest problem the country has. Also through the measure, the importation of foreign rice has stopped and the market for local varieties has risen.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

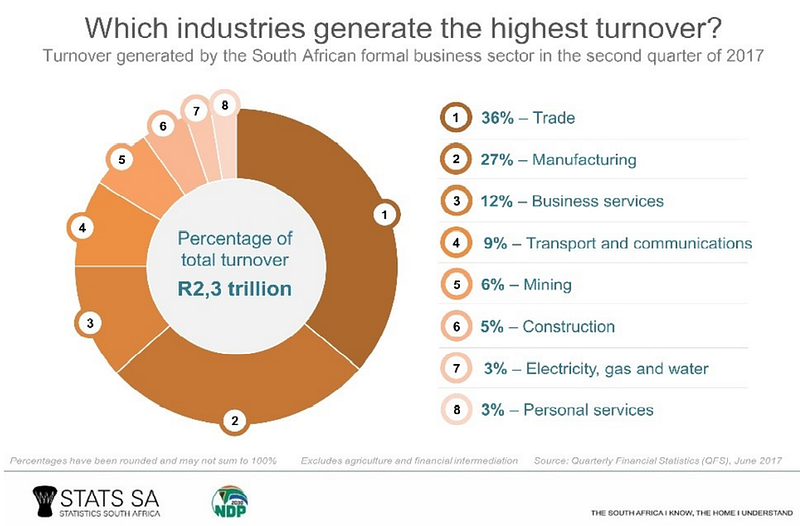

Despite the important contribution small-to-medium enterprises (SMEs) make to the economic growth of South Africa, the sector battles to access funding using traditional means.

And even though there are about 2.5 million SMEs in the country, the biggest stumbling blocks they encounter still revolve around the risk barriers and red tape associated with traditional funding products. The underwriting systems and financials required by institutions to finance small business simply do not provide a true reflection of operating conditions.

This has seen the emergence of fintech solutions and alternative funding products that have been steadily gaining momentum.

Yet most local SMEs are unaware of how and where to gain access to funding. For many, the only apparent path is to obtain funding via banks. By the time the business receives the funding (if ever), it is often too late and beyond the point where it can help the company turn things around.

However, funding entails so many different nuances beyond the traditional, and SME owners need to make themselves aware of what is available, and what will suit their specific requirements.

For their part, investors must adapt their digital strategies to engage differently with SMEs. For example, by using mobile as a platform for funding, the investor not only differentiates itself in the market, but the SME gains access to a real-time solution capable of addressing its unique needs.

This cannot happen on its own.

By partnering with a range of fintech organizations, the mobile-driven funding model provides SMEs with real-time, pre-approved offers based on turnover. And thanks to the availability of machine learning and artificial intelligence, these solutions will become more common. However, investors need to be viewed as more than just funders.

They can be true partners in working with SMEs and assisting them in positioning themselves in the market. Of course, the benefit of this is that they become part of a growing enterprise that has a direct impact on the economy of the country.

By incorporating electro-neural networks that enable the use of a sophisticated decision-making methodology requiring no human intervention, funders can more effectively identify where to invest their money. Invariably, the technology has built-in affordability metrics providing the SME with the peace of mind that funding received will not leave them over-indebted.

The graphic below shows the contribution to total turnover by all companies in South Africa in 2015, based on their size (sizes are determined by DTI, cut-offs and adjusted for Stats SA sampling purposes).

Behind-the-scenes, machine-learning algorithms have a deep understanding of business trading patterns and seasonality. This ensures the SME is unable to access more funding than what the business can afford. Such an affordability measurement is a great way to drive financial inclusion, irrespective of physical location, without leaving the SME over-indebted.

Using this sophisticated technology also enables funding to be done faster and more conveniently than before. Eliminating reams of paperwork and manual-intensive application process enable the owner to keep their focus on driving business growth.

And thanks to the ubiquity of mobile, SMEs can apply for funding irrespective of the time of day, using an environment that they are comfortable in. Funding requires no collateral, or security, and is completely unrestricted.

Depending on the funder, it is possible for SMEs to access funding with same-day pay-outs. However, for it to be truly inclusive, such a solution must be available to formal and informal businesses.

For our part, Retail Capital is driving this mobile focus very strongly to be the first to market with a platform that does exactly all of this. It is about delivering SMEs with an enabling environment to get funding using more innovative methods as quickly and effectively as possible. In fact, this smarter funding approach has resulted in mobile now representing more than 20% of the funding taken up at the organization.

Irrespective of the platform used, funding is the lifeblood of an SME. In these challenging market conditions, a multi-product approach that highlights how digital is changing access to working capital is necessary.

This creates a powerful platform for growth and the betterment of the economy, entrepreneurs and the country’s SME sector.

Miguel Da Silva is the Managing Director of Funding at Retail Capital.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

South Africa has over 2.5 million small and medium-sized enterprises (SMEs) in South Africa but not many of them have access to funding. A business idea without funding is as good as nothing. Access to funding in South Africa has however been made easier because of a growing alternative lending sector that is focused on providing funding for this market.

Below is a list of the different types of alternative financing available to South African SMEs

Fundrr uses technological innovation and automated algorithms to provide quick and efficient loans to small businesses. By the use of a simple, free and paperless application process, they are able to take the hassle away and allow you to focus more on your business. Fundrr allows small businesses to get an answer the same day and access to capital in 24 hours.

They serve businesses with at least a 12-month track record, with a minimum of R1 million turnover or asset value.

Applying is free of charge and there is no commitment or obligations to take the funds.

They provide loans from R20 000 to R500 000 ranging in duration from 3 to 12 months and repayments are made either on a daily, weekly, bi-monthly or monthly basis, depending on your cash flow.

Retail businesses interested in loans can contact Merchant Capital for their offers. The loan merchant offers cash on flexible repayment terms.

Who may obtain their offer?

Retail business owners who have been in business for more than one year and who have an average of over R30,000 in credit and debit card sales may obtain their loan.

We understand that you are the one who built this business. So we respect the fact that no one understands its ‘ins and outs’ quite the way you do. With this in mind, we don’t prescribe what you use your funds for. That said, having funded millions of Rands to thousands of South African businesses, we know a thing or two. So we highly recommend that the cash injection be used for business growth opportunities, the company noted on its website

The maximum amount of loan:

Retail business owners may obtain as much as 100% of the business’ average monthly credit and debit card turnover.

It’s a good idea to have this amount handy to better understand what you can expect. Then, as soon as we have analyzed your statements, you will be contacted with a more accurate qualification amount, the company stated.

You can use iKhoka’s card machines for as many times as you desire. However, using it for more than three months will qualify you for a custom cash advance offer.

Who May Obtain Loan From iKhoka?

The iKhoka application works on a reward system.

The iKhokha Cash Advance definitely helps take your business to the next level. Here’s how you can qualify for a custom Cash Advance offer:

Be an active iKhokha merchant

Must have traded for the past 3 months consecutively

Must trade at least 3 times a month

Must complete a minimum of 10 card transactions a month

Must have completed a card transaction in the last 15 days

Your turnover should be at least R2 500 per month

Your average monthly turnover for the last 3 months must be higher than R3 125

Check your offer in the iKhokha app and decide how much of it you need. The more you process through iKhokha, the bigger the amount you qualify for!

Maximum Amount of Loan:

The amount you get from iKhoka depends on the turnover of your business over a period of three months.

Zande Africa can order favorite brands in bulk from manufacturers at a lower cost.

The goods are delivered to one of its warehouses around South Africa.

Spaza shops owners order their stock through its driver/ sales agents.

Delivery is made within 24 hours to a Spaza Shops’ doorstep.

With Zande Africa, you can access funds to finance your trade and spaza shops.

Who May Obtain The Fund:

The target of the fund includes those who are looking to procure goods and stock for their spaza shops. In simple terms, Spaza credit supports businesses that are looking to procure inventory for their shops. Businesses desiring to go through this means can start by applying.

Maximum Amount:

Zande Africa provides finance depending on the turnover of the spaza.

Bright On Capital is an online peer-to-peer enterprise-lending platform, that serves as an online market place and allows SMEs to simply and quickly raise working capital funding from a wide range of traditional and non-traditional lenders.

These lenders include developmental funding institutions (“DFIs”), pension funds, corporate enterprise development funds, and other institutional investors.

Who May Obtain Funding From It?

Bright on Capital targets small businesses that have been trading for at least 12 months. These businesses must be supplying one or more corporates or credit-worthy public entities. They must also be expected to generate at least R1 million in annual revenues.

Complete the simple and easy application form, and submit the following documents on the website or via email or fax:

Your business’ registration documents.

Your business’ 6-month bank statement.

Your business’ tax clearance certificate.

Your business’ BEE certificate (For a business with a turnover of less than R10 million that doesn’t currently have a BEE certificate, you can complete an Affidavit and have it stamped signed by a Commissioner of Oaths. Once the Affidavit has been stamped and signed by a Commissioner of Oaths, it serves as a BEE certificate. Please click here to download the Affidavit.)

Your business’ latest audited financial statements and its most recent management accounts (optional for businesses generating less than R5 million revenue per annum).

Your business’ proof of business address.

ID copies for each director, member or partner; and

Proof of residential address for each director, member or partner.

ProfitShare Partners provides disruptive short-term capital solutions and transactional support to SMEs with valid contracts or purchase orders from reputable large organizations.

Who May Obtain Funding From It?

The fund targets SMEs with no track record, financial history or security with low performance, short-term contracts (up to 365 days) or purchasers with reputable large organizations.

Maximum Amount:

Small businesses may obtain loan from ProfitShare Partners from a minimum of R250,000 up to R5 million per transaction.

What Fincheck basically does is that it partners with South African banks, lenders and insurers to offer a live and independent means of comparing and applying for finance across 30 lenders.

Who May Obtain Loan Under It?

Generally, all business owners seeking finance in South Africa may apply for funding from the credit firm.

Fincheck Business compares business finance options for you. As the business owner — you simply need to complete the application form, which includes what you are looking for. From there, we have an algorithm that will work through your answers and match it to partner criteria* Based on these results, our engine will present you with business finance and partners that could best suit your needs. This whole process only takes a couple of minutes.

*Please note these results are not suggestions or advice from Fincheck Business or the FINCHECK group but are results based on your needs and partner criteria.

Lulelend has a strong history of lending to small businesses. The firm delivers business funding using proprietary scoring technology, which offers an instant funding decision on applications.

Who May Obtain From Luleland?

All South African businesses, no matter the industry or sector involved in trading for more than one year with annual revenue of R500,000+ can obtain funding from Luleland.

Amount: N/A

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Good news for startups and small businesses across South Africa. A new R130 million (over $9.3m) fund is at stake, targeting only 10 startups, each of which must have a black founder. The new fund is from Cape Town-based venture capital firm, 4Di Capital and the SA SME Fund.

A Look At The Fund

Cape Town-based venture capital (VC) fund with the launch of the R130-million fund aims to invest in at least 10 tech startups. Half of the R130-million will be targeted at startups with at least one black founder.

The over R1.4-billion SA SME Fund is capitalized presently by 54 JSE-listed firms and R500-million from the Public Investment Corporation (PIC). The fund was launched under the CEO Initiative. 4Di Capital is one of eight funds that the SA SME Fund has invested in (see this story).

4Di Capital partner Justin Stanford noted that R125-million of 4Di Capital Fund III’s first close of R130-million was from SA SME Fund, the rest has been committed by the VC.

“We will be looking at options in terms of raising additional capital for the fund but for now there are no fixed plans yet — in principle though the fund is still open to new investment,” said Stanford.

4Di Capital’s new R130m fund is backed by R125m from the SA SME Fund

Who Can Access The Funds?

Stanford said the fund will follow the VC’s usual modus operandi, which is to target tech startups in the early and growth stages.

The fund is vertical agnostic but the VC will look at deals for example in:

Insurtech

Fintech

Edtech

Agritech, adding that the VC will look at a spread of both early and growth stage.

“It is designed to work together with our Exponential Fund as well, so will also co-invest in certain deals that match the mandates on both sides,” he added.

He added that the fund will invest in at least 10 companies and pointed out that the first few deals are already under consideration.

A portion of the SA SME Fund capital has been earmarked for companies that have founder teams which include black founders.

When asked how much exactly would go to startups with black founders, Stanford said while it is “difficult to predict” the exact amount that will be invested in the end, the VC fund will aim to invest “roughly half” of the R130-million in such firms.

4Di Capital is an independent and specialist seed, early and growth-stage technology venture capital fund manager based in Cape Town, South Africa with an office in Atlanta, Georgia, U.S.A., focusing principally on scalable South African and African technology opportunities.

Among others, the fund has already invested in the enterprise web platform, cloud scaling infrastructure, bio-mathematical health technology, and financial technology ventures.

The SA SME Fund, on the other hand, was established by members of the CEO Initiative — a collaboration between government, labour, and business to address some of the most pressing challenges to the country’s economic growth — as an avenue of support for the SME sector.

It allocates investment capital to accredited fund managers — venture capital or growth-oriented equity funds — that invest directly in scalable small and medium enterprises with the best potential for growth and sustainable employment creation in the South African economy.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

MSMEs in Nigeria has grown to 41.543 million in 2017, according to the National Survey of Micro Small & Medium Enterprises (MSMEs). The 2017 National Survey of MSMEs covered enterprises in Nigeria employing below 200 persons, which are MSMEs and was conducted in all the 36 states of the federation and Nigeria’s Federal Capital Territory, Abuja.

Here Is A Further Break Down And The Implication Of This Number

The figures represent micro, small and medium scale businesses as at December 2017.

Nigeria had about 37 million MSME in 2013. The 41 million MSME number shows an increase of three million new MSMEs.

The statistics came from Nigeria’s National Bureau of Statistics (NBS) which launched the National Survey of Micro Small & Medium Enterprises (MSMEs) 2017 yesterday in Lagos.

The survey also showed that micro enterprises which employed less than 10 employees stood at 41.469 million, representing 99.8 percent, small enterprises employ 10 to 45 staff, 71,288 or 0.17 percent, while Medium enterprises with 50 to 199 staff were 1,793 or 0.004 percent.

According to the report, micro and small medium enterprises increased during the period under review, but medium scale enterprises dropped, which can be attributed to the economic recession the country witnessed in 2017.

From the statistics, most of the businesses are located in Lagos, Nigeria’s largest commercial city. While Lagos State had the highest numbers of enterprises across all classes, only three states, Katsina (36.4 percent), Rivers (21.7 percent) and Kaduna (18.l percent) recorded significant increases in enterprise numbers.

“There is a need for the government to pay a lot of attention to micro businesses because they have the largest share of employment, contributed to GDP growth and have the opportunity to create more jobs. During the period micro business grew to 41 million and if we can get half of them to produce one job, we will have 20 million jobs created, which is significant,” the director-general of Small and Medium Enterprises Development Agency of Nigeria (SMEDAN), Mr. Umaru Radda, said.

The survey which was supposed to be released in the fourth quarter of last year was delayed as a result of the election, according to the Statistician General of the Federation/CEO NBS, Dr. Yemi Kale.

The Small and Medium Enterprises Development Agency of Nigeria (SMEDAN) set up in 2003, was Nigeria’s government’s major response to tackling the problems of MSMEs in a coordinated fashion.

The MSME sub-sector has huge potential and the government should pay more attention to them than on large organization, by initiating friendly government policy in the sub-sector.

The figure above is so important that businesses would need to begin to readjust their strategies in order to remain in business.

With over 41 million businesses in Nigeria serving a population of over 200 million, compared the United States’ 30 million small businesses serving a population of 327.2 million, this is a significant number, in terms of competition for loans, scramble for people with buying power and other limited resources. It would boost the economy, no doubt, but businesses should begin to look at more creativity in order to retain their existence. Of course, most of the small businesses may only be existing on paper. But until that is proved, the figures still remain the facts.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Consider the case of human travel agents who were once consulted before trips bookings to foreign countries were made before digital disruption set in. The information below would serve as a guide for further analyses.

Data from Statista showed declining sales growth among travel agents in the United States since 2011.

The above is a classic case of how far digital disruption can go. An ABTA Holiday Habits Report 2018, which tracked British holidaymakers’ booking behaviour in the last 12 months and their attitudes to planning and booking holidays in the 12 months ahead, found that 81% of people booked their holiday online, compared to 22% of younger ( mostly 8–24-year-olds) and older families who booked their holiday in store.

This suggests a shift towards booking online and the gradual elimination of the use of human agents to schedule overseas travels. Simply put, the migration of the business of travel agency online and the increasing power of customers indicates that people are:

Now more knowledgeable about travel;

Now more technology savvy and have better access to devices;

Now get attracted by offers too lucrative to refuse;

Are offered more choice than ever.

Price is more transparent than ever.

Indeed, the above digital disruption in the business of travel agency could be extended to those of:

Tax accounting where software such as TurboTax has eliminated tens of thousands of jobs previously available for tax accountants.

Newspaper publication which has seen their circulation numbers decline steadily, replaced by online media and blogs.

Traditional taxi drivers and livery companies have completely been decimated by digital players such as Uber, Lyft, Bolt and other car and bike sharing apps.

Airbnb and HomeAway are doing the same for the hotel and motel industry.

Jobs previously done by bus and truck drivers, taxi drivers and chauffeurs are gradually being taken over by driverless cars, such as those being developed by Google (GOOG).

3D printing is continuously proving a threat to the manufacturing industry where the technology is becoming better and faster and in a few years, maybe deplored to manufacture a wide variety of goods on demand and at home. This will diminish the importance of logistics and inventory management.

Radio DJs are largely a thing of the past. Software now chooses most of the music played, inserts ads, and even reads the news.

Farmers and ranchers previously made up over 50% of the U.S. workforce. Today less than 2.5% are employed in this sector. Yet, more food than ever is being produced in America due to the automation in agriculture and food production.

Rapid and disruptive change is coming to your business, regardless of the industry in which you operate

75% of today’s leading brands will be gone inside a decade.

The table above shows the top 10 US companies ten years ago versus today, ranked by market value (market capitalization) in US dollars.

Getting ready for disruption would be the best thing that can happen to small businesses. Here are a few ways to stay alert:

Agility Will Allow Small Businesses To Survive

The best way to stay ahead of digital disruption is to stay agile. For a business to be agile means that it can move quickly, decisively, and effectively in anticipating, initiating, and taking advantage of change.

A Global Study of Current Trends and Future Possibilities 2006–2016 found that the best way of adapting to change is to develop organizations that are both agile and resilient. The report found that higher performing businesses tended to take a more proactive and opportunistic approach toward change.

‘‘…The average tenure of companies on the Standard & Poor’s 500 in 1958 was 61 years. That decreased to 25 years in 1980 and is just 18 years now, a number forecasted to dwindle to 14 years in 2026.What does this decreased lifespan portend for business?,’’ says Sasha Viasasha, content strategist based in Chicago. ‘‘Such a shortened lifespan points to the changing nature of business itself. The business cycle has shortened, and the accelerating pace of innovation — and competition — is disrupting the old linear model of business and replacing it with new, dynamic model. Today, agility rather than longevity is winning. In fact, characteristics that once contributed to corporate longevity and denoted a healthy culture, such as the ability to ‘stay the course,’ now could utterly sink a company.’’

Consider the five stages of a business lifespan, says Sasha:

Seed and development — ideation, feasibility and fundraising

Startup — product development, market testing, and iteration

Growth and Establishment — improved cash flow, established customer base and brand identity

Expansion — expanded offerings and new markets

Maturity and exit — every idea or product reaches a crisis stage, a point where improvement plateaus, expansion is no longer possible, and profits reach a ceiling.

Now there needs to be added a sixth stage:

Rebirth or return — in this stage, a company starts over again, reinvesting its resources in new innovation, she says.

Rahul Varshneya, co-founder of Arkenea, custom software development services for founder-led companies says the trick is to lean into technology rather than become consumed with fear, like forward-minded entrepreneurs in specific industries who love, not loathe, technological advance.

‘‘It’s time for you to get down and dirty and really investigate the demographics of your target audiences,’’ he says. ‘‘Find out what they want, what they need, where they’re getting assistance and how you can help them. By creating a psychographic chart for each of your prospective consumers, you can get a truer view of their personalities, attitudes, lifestyles, interests and so much more. Then, you can use this outline to make wiser predictions about their buying behaviors.’’

Innovate And Adapt To Technological Changes

The best way small businesses can also survive in the face of digital disruption is to innovate. Dr. John Kotter, a world-renowned change and leadership expert prefers small businesses to create a dual-operating structure that combines the best of both worlds.

‘‘Ultimately, great companies execute and disrupt at the same time. Often they disrupt themselves…Truly great companies like Apple, Google, Amazon, and Starbucks constantly find new ways to become relevant to us and remain an essential part of our lives. When analyzed closely, you can see that they are simultaneously executing and innovating. If there is not enough innovation, changes do not occur quickly enough, your people can lose their passion, your products can become outdated — and worse, your business can become irrelevant. Great leaders maintain the balance between achieving results today and innovating to seize new opportunities in the future. So if you want to avoid disruption — or even lead disruption — then you need to greatly accelerate the way you operate internally to keep pace with a rapidly changing world,’’ says Randy Ottinger an Executive Vice President at Kotter International and Professor of Leadership, Emeritus, at Harvard Business School.

The best way to adapt to this disruption, according to Robert Glazer, founder, and CEO of a global performance marketing agency, Acceleration Partners, is to put technology and data to work.

‘‘No matter what industry you try to disrupt or in what way you to try to do it, data and technology can be a huge help,’’ he says. ‘‘Technology doesn’t just revolutionize businesses, it changes how consumers behave in every aspect of their lives. If you track the market and note where interest in new technology is heaviest, you can likely foresee what areas are most ripe for disruption.’’

The most basic advice on adapting for small businesses would be to:

Small businesses can also hop on the frenzy of social media advertising. According to Ewan Duncan and Eric Hazan in their article, Digital Disruption: Six Consumer Trends, “Social networking represents almost a quarter of all Internet time (up 10 percentage points since 2008) and reaches over 75 percent of all Internet users.”

‘‘With more than 70% of Australians now using smartphones, and more than 40% of them making purchases directly from it, according to Our Mobile Planet, you’re missing out on a huge slice of the pie if you’re in e-commerce and operating without a mobile friendly site,’’ says Kwasi

Collaborative Partnership For Innovation

Small businesses can also survive technological disruption if they can partner with industries within their sectors, and where possible with the disruptors.

‘‘Companies that are better prepared for industry disruption are much more engaged in growing and broadening their ecosystem partnerships,’’ notes the Accenture Institute for High Performance. “They actively use this strategy to support innovation and research and development, as compared to only half of those who admit they are less prepared. Companies that are disruption-ready are a third more likely to partner with advertising agencies, innovation companies (26 percent more likely), design service providers (24 percent more likely) and even customers (26 percent more likely). They are also 36 percent more likely to collaborate with companies beyond their traditional industry boundaries, and 32 percent more likely to align with companies they consider direct competitors.’’

“In order to successfully navigate industry convergence and strengthen their network of alliances to build truly collaborative operating models, they must shift their mindset to compete as a ‘cluster’, not as a single company, creating shared value for their alliance partners and customers.”

Accenture Institute also goes to recommend tips for surviving disruption as follows:

Do not face digital disruption alone. Deepen and broaden partnerships with customers, providers, and a diverse array of companies in and beyond your core industry

Make yourself indispensable. Use your business’s focus and expertise to become a critical part of the integrated solutions that customers demand

Embrace operational flexibility. Consider what business changes you will need to be more collaborative and open — both in terms of your processes and your employee mind-sets

Develop New Customer Segments.

Small businesses can also confront digital disruption by developing new customer segments, instead of just defending existing business lines through cost cutting, automation, or service improvements for existing customers.

Medialaan NV As An Instance

Medialaan NV, a leading free-to-air video broadcaster in Belgium, found out that there had been a shift in video consumption by youngsters to platforms such as Netflix or YouTube. In a bold response, Medialaan bought Mobile Vikings, a mobile virtual operator with attractive data plans.

The strategy: Transform itself into the leading online social video platform for Flemish teenagers. Medialaan not only has diversified its revenue base to include data plans but also has been able to reengage with a lost segment — the teens — and now advertises its television programs to them more effectively. It is one of the few traditional broadcast companies to grow its TV audience in the youth segment.

Start Off New Business Models.

‘‘Innovative companies are experimenting with business models intended to disrupt their own legacy strategies,’’ Jacques Bughin and Nicolas van Zeebroeck in MIT Sloan Management Review said. They gave an instance of how earlier this century, Schibsted Media Group of Oslo, Norway, observed something that most media companies saw in their newspaper businesses: Print classified advertising was beginning to dry up. Rather than sit idly and witness the erosion of one of its most important revenue streams, Schibsted pulled the rug right out from under its own feet by moving its entire classified business to a free online marketplace. Today, more than 80% of the group’s earnings come from commissions on sales from its consumer e-commerce platform.

Commonwealth Bank of Australia (CBA) as an example.

Jacques Bughin and Nicolas van Zeebroek noted that when digital disruption started threatening CBA’s payment services business, Commonwealth Bank of Australia (CBA) confronted the disrupters once and for all. The bank moved from focusing exclusively on payment services to developing its Pi, an open payments platform that hosts an ecosystem of applications and devices for merchants.

The platform is open to third-party developers, and the bank developed for itself an Android-based point-of-sales terminal called Albert, which is fully integrated with the Pi payments platform. Equipped with a card reader and an integrated printer, Albert can be extended with dedicated apps, enabling it to do much more than process payments. Among the first adopters was Earthling Investments Pty. Ltd. of North Adelaide, South Australia, owner of wholesale fuel distributor Mogas Regional Pty. Ltd., also based in North Adelaide.

The company is using Albert at its fuel stations to process customer transactions, manage their payments, and receive sales data faster.11 Although the platform and its ecosystem contribute to the disruption of the traditional banking value chain, it also positions CBA to compete with digital entrants.

Similarly, while the mortgage side of the banking business is being disrupted by online search and home-financing platforms, CBA updated its digital value chain through an augmented-reality app that gives customers the ability to read a property’s sales history and community information by pointing their iPhone camera at the residence.

When they have found a property that they wish to buy, users can then file a loan application directly in the app, thus positioning CBA strongly against digital and incumbent competitors alike.

The Bottom Line

Imagine the hard work that comes with running a business, the burnt energy and the spent time, all guzzled up by fast-paced disruptive technologies? Although the general advice has always been that when businesses are faced with disruptive innovation the best and the most common-sensical things to do are to try and hold on to an existing market by doing the same thing better, or try to capture new markets by embracing new business models and technologies, a lot of businesses have gone into extinction due to a sudden ambush by mind-boggling, disruptive technologies. Only small businesses who understand these disruptions and can disrupt them could stand a chance to win.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Hard as it may seem, the era of internet disruption is already here and South African small businesses who are not prepared to take these trends seriously may soon be in for a surprise. From the recent survey conducted by GoDaddy, only half of the South African small businesses reported either having their own website (28%) or are planning to build one soon (22%), while around 42% said they rely solely on social media platforms.

The GoDaddy Global Small Business Research Survey was conducted in April and May 2019 in Australia, Canada, Germany, Hong Kong, India, Mexico, South Africa, Turkey, United States, and the United Kingdom.

The GoDaddy Global Small Business Research Survey Is Interesting In Many Ways

GoDaddy also looked at the attitudes of small business owners. Here are some of the key findings:

Small business owners in South Africa value the flexibility of running their own business, with nearly half (48%) saying it’s the best aspect of being an entrepreneur. For 13% of respondents, the money they can make is the biggest plus of running their own small business, while 12% cited helping the world to solve a problem;

On the flip-side, 32% said that the risk of failure and uncertainty about the future is the worst thing about being a small business owner;

Encouragingly, 91% of South African respondents said they would start their own business if they had to make the choice again knowing what they know now, and 84% reported they are happier since becoming an entrepreneur;

The skills shortage is a major challenge for small South African businesses, with 76% saying it is somewhat hard, hard, or very hard to find talented workers;

57% of small South African businesses serve mostly local customers (within 80 kilometers of their location) and only 10% serve mostly international customers;

41% of small business owners worked for a corporate employer before setting up their own venture; 26% were working for a small business; 16% were unemployed and 16% were students.

Right Now, Small Businesses In South Africa Say The Major Problems of Running A Small Business In South Africa Include:

Insufficient Investment

Around one third (34%) identified insufficient investment as a significant obstacle to growth, followed by failure to keep up with technology (20%) and cyber-security risks (13%).

Instability

Almost half (46%) of South African small businesses cited political instability and social turbulence as may be caused by change, including economic, technological or cultural factors as a major challenge to their growth prospects.

Cyber Attack

While few small businesses (7%) in the South African sample reported being victims of a cyber-attack, for those who did, the consequences were severe.

Those who were attacked reported that it shut down their business for some time; customers couldn’t reach them. They had to spend money to repair systems, and they lost access to accounts needed to service their customers, the survey found.

Technology and Disruptions

One of the biggest issues facing workers globally is the rise of automation, artificial intelligence and robot disruption that raises concerns about the future of jobs.

However, the vast majority of small business owners in South Africa believe they are insulated from those risks — 70% felt protected against job loss from these technology developments.

While technology disruption is likely to pose challenges, it also can reduce the barrier to entry to create a small business.

Local small businesses were least likely to have a website among the countries in the survey, and the most likely to rely on social channels, the survey noted

Research firm Savanta conducted the field research of the 4,505 small businesses in the countries. The South African respondents comprised companies with less than 25 employees.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Small businesses in South Africa now have a new source of funding to support their growth. The CDI Growth Fund, which is supported by National Treasury’s Jobs Fund of South Africa is offering small businesses a chance to benefit from its R12.8 million grant.

Who May Benefit From The Fund?

To qualify to benefit from the CDI Growth Fund, the business must specifically:

Be South African-owned business, with the controlling interest of the enterprise (51% of the issued ordinary share capital). The business must be held by South African citizens with valid a South African ID or a South African Registered legal entity itself controlled by South African citizens with valid South African ID.

Operate within South Africa, including but not limited to projects, programs or enterprises of the business.

Be an existing business, at least 1 year old (preference will be given to businesses that have been trading for 2 years or more) with turnover or assets above R1m.

Match 20% of the contribution of the Fund through a cash contribution

Must create one job for every R21,000 grant investment.

Be tax compliant

The table below gives you an idea, of how many jobs are required for a given amount of grant funding.

Additionally, you must:

Not be insolvent or currently under debt administration

Be willing to provide financial statements and all supporting documents required

Commit to training new employees

Once your application is successful, you will sign a contract and report on progress and impact to the Fund administrators on a quarterly basis during and for a two-year period after the project completion.

Application Requirements

Applications can only be made online on the CDI Capital website on or before 12 July 2019 at 17:00.

CDI Growth Fund At A Glance

The CDI Growth Fund is managed by CDI Capital, which was incorporated as a subsidiary of the Craft and Design Institute (CDI) in 2016 to catalyze funding for SMEs.

The funding has been enabled through contributions by the National Treasury’s Jobs Fund, the Technology Innovation Agency (TIA), and the Western Cape Department of Economic Development and Tourism (DEDAT).

Since its launch in 2017, it has already contracted with 38 SMEs, who have collectively created over 160 jobs.

The Fund is in the second year of a five-year disbursement period.

CDI Capital CEO Lesley Grimbeek said that the grant funding they received has had a tremendous impact on their growing business.

“We have seen really rapid growth in the past four years, and in the next two years we are determined to have a facility four times the size of what we currently have, creating between 250 and 300 jobs and bringing our amazing product right across South Africa.

“It’s been a pleasure working with the CDI’s Growth Fund, and it has been very exciting to see the impact it has made in such a short time. We have been able to purchase equipment that we could not have afforded otherwise, and through this we have been able to create more jobs.

“To date, we have created ten new jobs in the factory, and we have the intention of at least another 12 to 13 new positions by the end of the year,” said Grimbeek.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.