A Coronavirus Survival Strategy for Your Startup

With the Covid-19 virus now a worldwide pandemic, if you’re leading any startup or small business, you have to be asking yourself, “What’s Plan B? And what’s in my lifeboat?”

Here are a few thoughts about operating in uncertainty.

Impact

Social isolation and a declared national emergency have had an immediate impact on industries that cluster people; conferences, trade shows, airlines/cruise ships and all types of travel, the hospitality industry, sporting events, theater and movies, restaurants and schools. Large companies are telling employees to work at home. Large retail chains are shutting down their stores. While the impact on small businesses and workers in the “gig-economy” hasn’t made the news, it will be worse for them. They have fewer cash reserves and a smaller margin of error for managing sudden downturns. The ripple and feedback effect of all of these closures will have a major impact on our economy, as each industry that gets impacted puts people out of work, and those laid off workers don’t buy products and services.

It’s no longer business as usual for the rest of the economy. In fact, shutting down the economy for a pandemic has never happened. Millions of jobs may be lost in the next few months, as entire industries are devastated, something not seen since the Great Depression of 1929–39. I hope I’m very wrong, but the social and economic impacts of this virus are likely to be profound and will change how we shop, travel, and work for years.

If you’re running a startup or small business, your first priority (after your family) is keeping your employees and customers safe. But the next question is, ‘What happens to my business?”

The questions every startup or small business CEO needs to ask now are:

- What’s my burn rate and runway?

- What does my new business model look like?

- Is this a three-month, one-year, or a three-year problem?

- What will my investors do?

Burn rate and runway

To answer the first question, take stock of your current gross burn rate: How much cash are you spending each month? How much of that goes toward fixed expenses (those you can’t change, such as rent)? And how much goes toward variable expenses (salaries, consultants, commission, travel, AWS/Azure charges, supplies, etc.)?

Next, take a look at your actual revenue each month — not your forecast, but real revenue coming in. If you’re an early stage company, that number may be zero.

Subtract your monthly gross burn rate from your monthly revenue to get your net burn rate. If you’re making more money than you’re spending, you have positive cash flow. If you’re a startup and have less revenue than your expenses, that number is negative and represents the amount of money your company loses (“burns”) each month. Now take a look at your bank account. See how many months your company can survive burning that amount of cash each month. This is your runway — the amount of time your company has before it runs out of money. This math works in a normal market …

Unfortunately, it’s no longer a normal market.

All your assumptions about customers, sales cycle and most importantly, revenue, burn rate, and runway are no longer true.

If you’re a startup, you’ve likely calculated your runway to last until you raise your next round of funding. Assuming there was going to be a next round. That may be no longer true.

Your new business model

Since the world today is no longer the same as it was a month ago, and likely will be worse a month from now, if your business model today looks the same as it did at the beginning of the month, you’re in denial — and possibly out of business.

It’s the nature of startup CEOs to be optimistic, however you need to quickly test your assumptions about customers and revenue. If you are selling to businesses (a B-to-B market), have your customers’ sales dropped? Are your customers closing for the next few weeks? Laying off people? If so, whatever revenue forecast and sales cycle estimates you had are no longer valid. If you’re selling directly to consumers (a B-to-C market), were you in a multi-sided market (consumers use the product but others pay you for their eyeballs/data)? Are those assumptions about payers still correct? How do you know?

What are the new financial metrics? Receivables — get on top of them. Days of cash left?

You need to figure out your actual burn rate and runway in this new environment now.

Is this a three-month, one-year, or a three-year problem?

Next, you need to take a deep breath and try to gauge how long this problem will last. Are the shutdowns of businesses going to be a temporary blip in the economy, or will they drive the US and Europe into a long recession?

If it’s just three months (looking more unlikely by the day), then an immediate freeze on variable spending (hires, marketing, travel, etc.) is in order. But if the effects are going to reverberate in the economy longer, you need to start reconfiguring your business. You need a lifeboat strategy. That’s a fancy phrase for figuring out the minimum your company needs to hold onto to stay alive.

A one-year problem means taking a knife to your burn rate (layoffs and elimination of perks and programs to reduce your variable expenses), renegotiating what previously seemed liked fixed expenses (rent, equipment lease payments, etc.), and putting only the essential elements for survival in the lifeboat.

If you were selling online versus in-person, you may have an advantage (assuming your customers are still there.) Or you change sales strategy.

Whatever your product/market fit was last month, it’s no longer true and needs to change to meet the new normal. Does this open new value propositions and kill others? Do you need to alter the product?

And if it’s a three-year problem? Then not only do you need to jettison everything that isn’t essential for survival, you’ll probably require a new business model. In the short term, explore whether some part of your business model can be oriented around the new rules of social isolation. Can your product be sold, delivered, or produced online? Does it have some benefits if delivered that way? (See the advice from Sequoia Capital here.) If not, can your product/service be positioned as a lifeboat for others to ride out the downturn?

As a leader, you need to plan, communicate, and act with compassion.

Revise your sales revenue goals and product timelines, create a new business model and operating plan, and communicate them clearly to your investors and then to your employees. Keep people focused on an achievable plan they clearly understand. From the perspective of having lived through the last three crashes, I’ve observed the biggest mistake CEOs made was not making draconian cuts to expenses quickly enough. They dripped out layoffs and cuts, holding onto favored projects with magical thinking that somehow this was just something that would pass. You need to act now.

Read also : What Happens To Startups in a Recession?

If you’re in a large company considering layoffs, the first option should be to cut the salaries of the higher paid exec/employees to try to keep the people who can least afford to lose their jobs employed. (Good things will come to CEOs who first try to save everyone on the ship before they jump in the lifeboat.) If/when people need to be laid off, do it with compassion. Offer extra compensation. If in the worst case you see you’re running out of cash, under no circumstances run it down to zero. Do the right thing and have enough cash on hand to offer everyone at least two weeks or more of pay.

Your investors

One of the key elements of survival is access to capital. As a startup or small business you should realize your investors are also asking themselves how this pandemic will affect their business model. The cold hard truth is that, in a crash, VCs are running their own “What do I save in the lifeboat?” exercise. They triage their deals — first worrying about liquidity of their late stage deals, which have the highest valuations. These startups typically have very high burn rates and funding for those could fall off a cliff. You and the survival of your startup may no longer be their priority, and your interests are no longer aligned. (VCs who tell you otherwise are either naïve, lying through their teeth, or not serving the interests of their investors.) In every major downturn inflated valuations disappear and the few VCs still writing new checks find it’s a buyer’s market. (Hence the term “vulture capitalists.”)

Read also : South Africa’s Startup Accelerator Grindstone Raises $1.5m To Support Startups

Some investors have only lived in a booming market when valuations only went up and investment capital was plentiful. But investors with grey hair can remember the nuclear winter after the past recessions of 2000 and 2008 and can offer some historical patterns of crashes and recovery to CEOs running early stage startups. Keep in mind,# that today’s circumstances are different. This isn’t a bear stock market. This is a conscious shutdown of most of our economy, trading jobs for saving hundreds of thousands of lives, that’s causing a bear market and a likely recession.

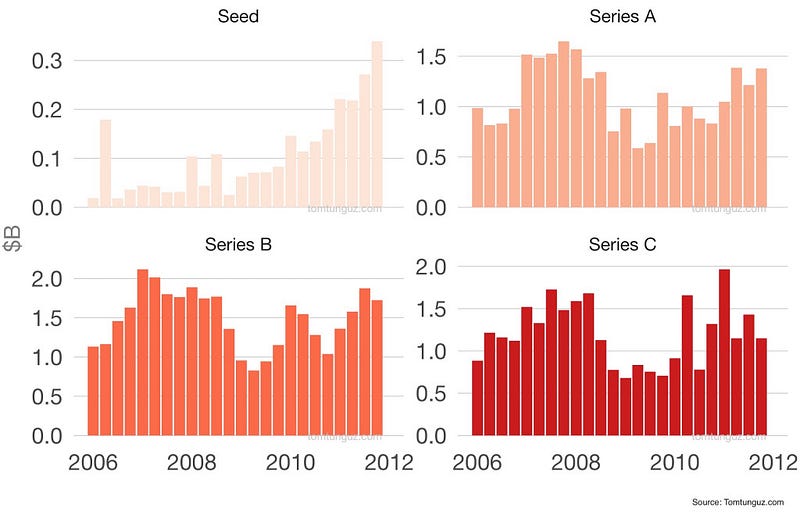

Data from the last large crash in 2008 had seed rounds recovering early, but later stage funding cratered and took years to recover. (The figure below — part of this post from Tomasz Tunguz — shows quarterly VC investments before and after the 2008 crash.)

This time around, the health of the venture business may depend on what hedge funds, investment banks, private equity firms, sovereign wealth funds, and large secondary market groups do. If they pull back, there will be a liquidity crunch for later stage startups (Series B, C…). For all startups in the short term, the deal terms and valuations will get worse, and there will be fewer investors looking at your deal.

As a startup CEO you need to know if your board is going to be screaming at you for not radically cutting burn rate and coming up with a new business model or, will they be yelling at you to stop being distracted and stay the course?

And if the latter, I’d want to know what skin they have in the game if they’re wrong. It’s pretty easy for VCs to tell you they’ll be right behind you when you need a next round, until they’re not. Unless your investors are matching their orders for “full speed ahead” with a deposit into your bank, now is not the time to be railroaded into a burn rate that is unrecoverable.

Prepare for a long cold winter. But remember no winter lasts forever, and in it smart founders and VCs will be planting the seeds for the next generation of startups.

Lessons learned

- This is a conscious shutdown of our economy, trading jobs for saving hundreds of thousands of lives

- It’s likely going to cause a recession

- The Covid-19 virus will change how we shop, travel, and work for at least a year and likely three.

- It’s inconceivable that you can have the same business model today as you did 30 days ago

- Put in place lifeboat plans for three-month, one-year and three-year downturns

- Recognize that your investors will act in their interests, which may no longer be yours

- Take action now

- But act with compassion.

Steve Blank is a retired serial entrepreneur-turned-educator who created the Customer Development methodology that launched the lean startup movement, which he wrote about in his book, The Four Steps to the Epiphany. Blank teaches Lean LaunchPad classes at Stanford University and Columbia University where he is a senior fellow for entrepreneurship.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

He could be contacted at udohrapulu@gmail.com