Kingson Capital, along with AKRO Accelerate, is offering a new opportunity for South African startups. The companies, from 28 August to 29 August 2019, will host an event where 20 pre-selected ‘Proudly South African’ startups will be given the opportunity to pitch their business ideas in order to stand a chance at being selected for a two-week boot camp in the United States. There, the startup owners will have a chance to learn how to redefine their business and sustain their venture.

Here Is All You Need To Know

Kingson Capital is a South African Venture Capital Company that is said to be committed to providing venture capital for High-Growth Tech and Black-Owned SME’s.

The company claims it is passionate about clearing financial hurdles for SME’s in order to maintain and sustain their startup momentum.

Kingson Capital is backed by international investors and corporations who have interests in investing in the South African tech industry. Kingson Capital pairs investment with business support through its investment structure.

Kingson Capital claims to have invested 400 million Rand in over 60 businesses.

“Although we see a substantial rise in South African startups,’ it is unfortunate that when it comes to them sustaining that startup momentum, many fall by the wayside due to lack of support. For us, it’s all about creating venture ecosystems across the venture investment landscape. In a South African context, we are looking to build on these ecosystems, and from that growth, all players will reap the long-term benefits,” says Gavin Reardon, founder of Kingson.

“This event speaks to what is so desperately needed in South Africa: giving an outlet to startups to be heard and to be taken seriously in early-stage development, by investors. A lot of startups and founders who are the real innovators in our society, get lost between the cracks of life, as they have no idea how to get market access and investment to kickstart and sustain their growth,” said Janine Basel from AKRO.

“We want to see startups that are innovative, backed by hard-working individuals that are committed to their startup. We want startups that are addressing our most pressing challenges, using technology to address this. We believe that the businesses that solve the biggest problems will have the biggest chances of scaling and being sustainable. For this reason, our focus is on tech or tech-enabled business” added Basel.

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

At a time oil is being exhausted all around the world, the Republic of Congo is just beginning to realise that it has more oil than it has ever imagined . A new oil discovery in the country could produce nearly 1 million barrels of oil per day, possibly quadrupling the nation’s output and propelling it into the same league as Africa’s largest producers, says SARPD-OIL, a company doing the exploration.

Here Is All You Need To Know

Currently, Congo ’s oil output stands at about 350,000 barrels per day.

However, production from a new field, developed by SARPD-OIL in la Cuvette region, could dwarf that, said the company’s marketing director Mohamed Rahmani.

SARPD estimates the field holds 1 billion cubic metres of hydrocarbons, including 359 million barrels of oil, with a potential for daily output of 983,000 barrels, Rahmani said.

That, the company reckons, could bring in $10.5 billion a year into Congo, doubling the Central African country’s GDP.

Production, which will be ramped up in phases, could begin in six months.

If it reaches expected levels, Congo’s production would be close to Nigeria, which produces about 1.8 million barrels a day, and Angola, at around 1.4 million.

Currently, Congo Republic’s debt stands at 114% of its GDP but the International Monetary Fund is helping to cut it down. Alone, about 1.6 trillion CFA francs ($2.7 billion) is owed to China according to a February 2018 report by the French Embassy in Congo, which cited the Finance Ministry.

Many observers see Congo as a test case for the IMF.

A number of African countries facing unsustainable debt resulting from commercial borrowing, a boom in Eurobond issues and years of Chinese lending on the continent are expected to turn to the IMF for help in the coming years.

This is even bound to grow more because sovereign debt financing is inevitable given that African countries budgetary resources are insufficient to finance their vast development agenda.

A government spokesman did not immediately comment on the discovery.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

African free-trade deal can help boost exports to the US, says Patel

The establishment of an African free-trade zone will enable the continent to speak with one voice and potentially boost exports to the US, say South Africa’s trade and industry minister Ebrahim Patel says. Concerns have been raised about the future of the African Growth and Opportunity Act (Agoa) under President Donald Trump’s administration.

Ebrahim Patel. Picture: TREVOR SAMSON

Enacted 19 years ago, Agoa gives special treatment to 39 African countries by abandoning import levies on more than 7,000 wide-ranging products. The US president has previously made it clear he wants to protect US domestic business and manufacturing against threats from abroad.Analysts have suggested that this could mean added import duties on South African exports to the US. Trump’s foreign policy on Africa has not been clearly defined, with many observers suggesting that the continent is likely to slide down his list of foreign policy priorities.

In 2018, SA joined various other countries on the continent in signing the Continental Free Trade Area agreement that aims to create a single continental market for goods and services, with free movement of business people and investments. With about 1.2-billion people in Africa, the agreement is set to create one of the largest free-trade market zones in the world. Patel and his deputy, Fikile Slovo Majola, are attending the Agoa forum which started at the weekend and ends on Wednesday.

The Agoa forum is an annual meeting held alternately in Africa and in the US between the ministers of trade of Sub-Saharan African countries and their US counterparts. Speaking in Abidjan in the Ivory Coast during the 18th Africa Growth and Opportunity Act forum, Patel said the continent has the opportunity to align the Continental Free Trade Area (CTFA) with plans to increase access to US markets.“We have an opportunity in these proceeding to align Agoa to goals of the CFTA to enable us to speak with one voice,” Patel said of the Abidjan meeting.

He pointed out that Sub-Saharan exports to the US have been on a downward trend in recent years. Total exports from the region to the US increased from $22bn in 2000 to a high of $82bn in 2008 at the height of the commodity boom.Patel said countries in the region have to work closely together to make the most of Agoa preferences and deepen trade relations with the US.

“The US is the world’s largest economy and access to the US market and to American investment in our economy are important ways of addressing job creation and the elimination of poverty. We look forward to a constructive and positive discussion with the US trade representative,” he said

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry.

This has to be unprecedented for Egypt’s startup, Fawry, that was formed eleven years ago. Going public and getting listed on the stock exchange is one thing, but finding acceptance from Egyptian investors is the most significant thing that shows that Egypt ’s investment community is not only looking at the dividends on shares here but on the future prospects of the eleven year old company. Plus, this is the first IPO in Egypt this year and the largest IPO yet.

Here Is All You Need To Know

Eleven-year-old Egyptian electronic payments company Fawry, after months of hype, finally went public on The Egyptian Exchange (EGX) in first Egyptian IPO of the year.

The share prices were fixed at the price of EGP 6.46, but soared 31 percent to close at EGP 8.48 on the first day of trading.

With this, the company now has market capitalisation of close to EGP 6 billion or $366 million.

Middle East and North Africa (MENA) e-commerce is worth $8.3 billion and has grown by 25% annually since 2014 Source: Bain & Company

“The Egyptian Exchange’s (EGX) platform welcomed today Fawry for Banking Technology and Electronic Payment, newly listed company number 216, to its main market with a trading code FWRY.CA,” the Egyptian Exchange said in a statement.

“The private placement was oversubscribed by 16 times and the IPO by 30 times. Egyptians represented 80.3% of the IPO and 50% of the private placement. Arabs & Foreigners represented 19.7% of the IPO and 49.3 of the private,” the statement added.

Fawry raising so much money (about EGP 1.64 billion ($100 million) from the Exchange is quite remarkable given that only 36 percent (254.6 million) of its shares were made available on The Egyptian Exchange for public subscription.

The offering was comprised of a secondary sale by Netherland Holding BV.

Ashraf Sabry, CEO of Fawry, in a statement, said that the commencement of trading on Fawry in EGX is an important step for growth and will definitely support its expansion plans.

Founded in 2008 by Ashraf Sabry & Mohamed Okasha, Fawry offers over 250 electronic payment services through its network of over 100,000 service points across 300 cities in Egypt – that include ATMs, mobile wallets, retail shops, post offices, and little vendor kiosks.

The company also has its online payment gateway that allows online businesses to collect payments from their customers using different methods including cash, credit cards, and mobile wallet.Fawry was acquired by a consortium of three investors; Helios Investment Partners, MENA Long-Term Value Fund, and Egyptian-American Enterprise in 2015. The three investors had reportedly acquired 85 percent of the company at a valuation of $100 million.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

China ’s tech entrepreneurs are finding that affordable innovation appeals in developing markets.

Many Chinese companies are finding new avenues of growth.

During the past decade of breakneck economic growth, China has been a gold mine for tech startups, with the biggest internet user base in the world of 829 million.

But a new wave of Chinese entrepreneurs are now deciding to skip the country in favour of fast-growing markets in Southeast Asia, India, the Middle East and Africa, taking their innovative ideas and cutting edge business models with them.

Whether its e-commerce, short video, live broadcasting or gaming — China’s tech experts are looking to apply the lessons learned from China’s rapid tech development to a range of emerging markets, according to interviews by the Post with analysts, investors and startup founders.

“We are seeing Chinese tech companies take an increasing presence outside China in short video and social apps, video editing, shopping and gaming categories,” said Nan Lu, analyst at mobile intelligence firm Sensor Tower. “They’re looking at markets in South America and in Asia, such as India for example … territories with large, young populations.”

Lu added that the Middle East is also a target because of its advanced internet access and high demand for social media.

In Southeast Asia, Chinese apps took seven spots among the 10 highest-grossing short video and live streaming apps in the past year, with Singapore-headquartered live-streamer Bigo Live in the lead. Global short video hit Tik Tok topped the region’s download chart, according to a June report by Sensor Tower. Although revenue per user in many of these countries is lower than in developed markets such as the US, they have young, increasingly affluent populations, portending future growth.

Bigo Technologies, the company behind the live broadcasting platform, was founded by Chinese entrepreneur Xueling Li, co-founder and chief executive of Chinese live-streaming company YY Inc. US-listed YY acquired Bigo in March this year.

Although huge, China’s tech market now has relatively well-established leaders.

E-commerce heavyweight Alibaba with its Tmall and Taobao platforms, internet giant Tencent with its do-everything social app WeChat, and ByteDance with its short video app Douyin (known as Tik Tok overseas) have become leading pillars of China’s tech sector. Although there’s still room for new competition, many entrepreneurs now see a chance to grow even faster in overseas markets where there is burgeoning appetite for innovative, more affordable tech products.

The global internet scene generally remains a bipolar world.

While US behemoths such as Google and Facebook have struggled to crack China’s fire-walled internet and heavily-regulated tech sector, Chinese players (until ByteDance with Tik Tok) have largely struggled to make their offerings attractive and relevant for developed markets, such as the US.

Given this backdrop, many have turned to developing markets, where affordable innovation appeals. And some Chinese companies have struck gold with this strategy.

Transsion, a little-known company from Shenzhen, is now the biggest mobile phone supplier in Africa. TikTok, the international version of ByteDance’s Douyin, has also become one of the most-heavily downloaded apps worldwide, and one third of its overseas users now come from India, according to Sensor Tower.

Chinese Companies Have An Edge In Many of These New Market Countries

This is because they are now undergoing the same tech and development transformation that China went through over the past decade. As such, they have gained insights that has allowed them to bypass mainstream industry players.

To be sure, China may have opened the diplomatic door in places such as Africa, which is seen as a solid base of raw materials to help fuel the country’s long-term economic growth. But China’s entrepreneurs also see the potential to apply their tech know-how and lessons learned to young and increasingly affluent consumers.

For example China’s Transsion, which operates three handset brands — Tecno, Infinix, and Itel — has focused on bringing affordable smartphones and feature phones with basic functionality to developing economies since it was founded in 2006.

The average price of Transsion’s basic phones was USD 10 in 2018, while its smartphones cost around USD 66 on average — or about 5% of the cost of Apple’s flagship iPhone XS model, according to Transsion.

Also winning in African markets is Shenzhen-headquartered Simi Mobile, whose nearly two-dozen feature phone handsets are priced between USD 10 to USD 20, while its competitively priced smartphones are already on sale in Ethiopia, Uganda, Cameroon, and will soon be available in more African countries.

The continent is quietly undergoing a transition from feature phones to smartphones, driven by the availability of affordable models and increasing internet penetration. While 2018 saw a 4.1% decrease in smartphone shipments worldwide, Africa experienced year-on-year growth for the first time since 2015, according to data from research firm IDC.

The reason why some Chinese companies like Transsion managed to succeed is that they captured a niche market and established their own advantages in it, said Changqi Wu, professor of strategic management at the Guanghua School of Management of Peking University.

Transsion, for instance, attuned its camera technology and calibrated the exposure specifically for darker skin tones.

“While in general China’s technology may still lag behind the US or other developed countries, it can maintain an edge in developing markets by serving them well,” Wu said.

Catering to niche markets may not appeal to top global vendors such as Apple due to the high costs, but that is where Chinese companies can spot opportunities and be very creative, said Wu.

Africa’s e-commerce gap proved to be an opportunity for Yang Tao, who was deployed to Kenya by his former employer Huawei seven years ago to build a payments system.

Disrupting A Long Lasting Legacy

Many African countries lag behind the developed world in manufacturing due to a legacy model of exporting raw materials in exchange for consumer goods, meaning Africa has a shortage of some items and that drives up prices, said Yao.

Bugged by the inconvenience of shopping in Kenya, Yang decided to set up his own e-commerce site Kilimall in 2014, which is now the biggest online shopping website serving about 10 million users in the country. It sells electronics, clothes, home appliances, cosmetics and baby products among other things.

Now, with more smartphone users and as the infrastructure for online services such as mobile payments gradually matures, Chinese entrepreneurs are seizing opportunities generated by the continent’s social transformation and industrial upgrading.

Also tapping the tech boom in emerging markets is Akulaku, an Indonesian startup founded by Chinese entrepreneurs Li Wenbo and Hu Bo, which allows users to pay for purchases in instalments, without the need for a credit card.

“Many Indonesian consumers want to pay in instalments when they buy a new smartphone, as they may not have the purchasing power to pay for it in one go,” said Helen Wong, a partner at Qiming Venture Partners which invested in Akulaku. The Indonesian company is betting on the development of both e-commerce and fintech, which are two major trends in the region, Wong noted.

In many respects, Southeast Asia is following China’s past experience in terms of mobile internet development. The internet scene in Southeast Asia is still 5 to 10 years behind China, Wong said, adding that the mobile internet penetration rate still lags behind China but is rising rapidly.

Although Alibaba’s Taobao may dominate in China, entrepreneurs with know-how in China’s e-commerce and supply chain are in a good position to head outwards, says Wong, who is responsible for overseas investments at Qiming.

The startup ecosystem in Southeast Asia, despite a late start, is picking up with the emergence of Rocket Internet and other success cases and attracting major investors including Alibaba, which should open up more opportunities for Chinese entrepreneurs, Wong added.

To be sure, in broad sectors such as traditional social media, US giants like Facebook still have a stranglehold, leaving little space for Chinese challengers.

“Google and Facebook still dominate 70 to 80% of advertizing in the region as they control a vast quantity of data and user insights needed for precise advertizing,” Wong said.

“Monetization [making money from customers] will remain a challenge for many social media startups.”

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Traditionally, startup businesses draft a business plan for three specific reasons: to articulate their vision for the business, to document how they plan to solve key challenges, and to pitch their business idea to potential investors.

But what if I told you that business plans for startup companies are usually not worth the effort?

My many years of experience working with startups, entrepreneurs, and venture capitalists has led me to conclude that business plans are largely a waste of time for the following reasons:

They are time consuming. Thorough business plans take a long time to prepare, even if you use business planning software.

They get outdated quickly. Your business plan quickly becomes obsolete as you encounter operational and marketing issues.

Nobody has time to read them. Prospective investors and venture capitalists don’t usually have the time or interest to slog through such a document. They review hundreds if not thousands of startup opportunities, so you have to grab their attention with something much shorter.

So instead of wasting your valuable time preparing a business plan, I suggest that you do these five things instead when launching your startup:

Business plans for startup companies are usually not worth the effort. Learn what you should be focusing on instead.

1. Prepare a Great Investor Pitch Deck for Prospective Investors

Developing an engaging “pitch deck” to present your company to prospective investors instead of a business plan is the new norm. The pitch deck typically consists of 15–20 PowerPoint slides and is intended to showcase the company’s products, technology, and team to the investors.

Raising capital from investors is difficult and time consuming. Therefore, it’s crucial that a startup seeking funding absolutely nails its investor pitch deck and articulates a compelling and interesting story in the short time it has during the presentation.

You want your investor pitch deck to cover the following topics, roughly in the order set forth here and with titles along the lines of the following:

Company Overview (give a summary overview of the company)

Mission/Vision of the Company (what is the mission and vision?)

The Team (who are key team players? what is their relevant background?)

The Problem (what big problem are you trying to solve?)

The Solution (what is your proposed solution? why is it better than other solutions or products?)

The Market Opportunity (how big is the addressable market?)

The Product (give specifics on the product)

The Customers (who are the target customers? why will there be a big demand from these customers?)

The Technology (what is the underlying technology? how is it differentiated?)

The Competition (who are the key competitors?)

Traction (early customers, early adopters, partnerships)

Business Model (what is the business model?)

The Marketing Plan (how do you plan to market? what do you anticipate for customer acquisition costs vs. the lifetime value of the customer?)

Financials (actual and projected profit & loss and cash flow)

The Ask (how much capital you are trying to raise?)

Too many startups make a number of avoidable mistakes when creating their investor pitch decks. Here is a list of preliminary do’s and don’ts to keep in mind:

Pitch Deck Do’s

Do include this wording at the bottom left of the pitch deck cover page: “Confidential and Proprietary. Copyright by [Name of Company]. [Year]. All Rights Reserved.”

Do convince the viewer of why the market opportunity is large.

Do include visually interesting graphics and images.

Do send the pitch deck in a PDF format to prospective investors in advance of a meeting. Don’t force the investor to get it from Google Docs, Dropbox, or some other online service, as you are just putting up a barrier to the investor actually reading it.

Do plan to have a demo of your product as part of the in-person presentation.

Do tell a compelling, memorable, and interesting story that shows your passion for the business.

Do show that you have more than just an idea, and that you have gotten early traction on developing the product, getting customers, or signing up partners.

Do have a sound bite for investors to remember you by.

Do use a consistent font size, color, and header title style throughout the slides.

Pitch Deck Don’ts

Don’t make the pitch deck more than 15–20 slides long (investors have limited attention spans).

Don’t have too many wordy slides.

Don’t provide excessive financial details, as that can be provided in a follow-up.

Don’t try to cover everything in the pitch deck. Your in-person presentation will give you an opportunity to add and highlight key information.

Don’t use a lot of jargon or acronyms that the investor may not immediately understand.

Don’t underestimate or belittle the competition.

Don’t have your pitch deck look out of date. You don’t want a date on the cover page that is several months old (that is why I avoid putting a date on the cover page at all). And you don’t want information or metrics in the deck about your business that look stale or outdated.

Don’t have a poor layout, bad graphics, or a low-quality “look and feel.” Think about hiring a graphic designer to give your pitch desk a more professional look.

2. Focus on Building a Good Prototype Product

Build version 1 of your product. Having a prototype of your product makes it easier to sell your vision to investors. It also gives you some momentum and traction and helps you recruit partners and employees. Undoubtedly, version 1 of your product will not be as good as version 2 or version 3, but you need to start somewhere.

When starting out, your product has to be at least good if not great. It must be differentiated in some meaningful and important way from the offerings of your competition. Everything else follows from this key principle. Don’t drag your feet on getting your product out to market, since early customer feedback is one of the best ways to help improve your product.

Of course, you want a “minimum viable product” (MVP) to begin with, but even that product should be good and differentiated from the competition. Having a “beta” test product works for many startups as they work the bugs out from user reactions. As Sheryl Sandberg, COO of Facebook has said, “Done is better than perfect.”

3. Thoroughly Research the Market Opportunity and Your Competition

Make sure you are thoroughly researching the market opportunity and competitive products or services, and keep on top of new developments and announcements from your competitors. One way to do this is to set up a Google alert to notify you when any new information about those companies appears online.

Expect that prospective investors in your company will ask questions about the market opportunity and your competitors. Any entrepreneurs who say that “we don’t have competitors” will have credibility problems. So anticipate these questions from investors:

How big is the addressable market? How much of it can the company realistically capture?

Who are the company’s principal competitors?

What traction have those competitors obtained?

What gives your company the competitive advantage?

Compared to these other companies, how do you compete with respect to price, features, and performance?

It can be important to prepare detailed financial projections for the business, for the following reasons:

To determine whether the business will ultimately be profitable

To determine your cash “burn” before you get cash flow profitable, showing how much startup capital you will need

To lay out your key financial assumptions (price per product, cost of developing the product, marketing expenses, employee expenses, rent and overhead, gross margins, and much more) so that you and others can test the reasonableness of the assumptions

To have those projections ready and credible when investors inevitably ask for them

Financial projections will typically be for a 3–5 year period and will include:

Profit and loss statement

Cash flow statement

Detailed categories of income and expenses

Balance sheet

Underlying assumptions

Of course, your financial projections will not be perfectly matched with your actual results, but your financial projections can be revised as you move through the stages of your business.

5. Make Sure You Have Thought Through the Reasons Why Startups Don’t Get Funded By Investors

There are a variety of reasons why investors turn down startups and entrepreneurs. So understand these reasons and make sure they don’t apply to you:

The business idea is too small

Your executive summary or pitch deck is underwhelming

You haven’t thought through the questions that investors will likely ask

You just have an idea and you haven’t gotten any traction yet

You don’t have the right management team

You don’t understand the competition

There are already strong competitors who are well capitalized

Your financial projections are unrealistic

You aren’t convincing about the need for your product or service

You don’t articulate how you plan to cost-effectively market to and obtain customers

You don’t have a good prototype of your product

Remember, you don’t need a long business plan for your startup. There are more important things you can do to build a successful business.

Richard Harroch is the Managing Director and Global Head of M&A for VantagePoint Capital P… He writes about startups, venture capital, mergers and acquisitions and Internet companies.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Africa appears to have made its way back onto a growth trajectory with foreign direct investment (FDI) inflows to the continent expected to increase by 15% in 2019, after a rise of 11% to $46bn in 2018. As encouraging as the signs are, inflows are still below the annual average of the past 10 years of about $50m, but confidence is returning and that level could be regained by year end.

This is partly thanks to advances in regional integration and progress towards the implementation of the African Continental Free Trade Agreement (AfCFTA).

It is also being driven by Africa’s vast demand for business services, agribusiness, infrastructure, as well as information and communications technology (ICT), as the digital economy becomes a significant growth driver. Inflows into once all-important extractive industries, while still significant, continue to fade.

In several African countries, the digital economy is becoming one of the main drivers of growth, accounting for more than 5% of GDP. Technology and innovation have become the backbone of African economic success over past two decades despite internet access and penetration remaining low. Less than 30% of Africans have access to mobile broadband connectivity, compared with 79% of Americans. There are more than twice the number of internet users in Europe (501-million) than in the whole of Africa (213-million).

When it comes to digital infrastructure, Africa suffers from poor-quality and expensive services compared to other parts of the world. While the digital infrastructure and services gap in Africa remains high, there is increasing activity and investment on the continent to close the gap.

Agricultural production, or agribusiness, also plays a vital role in Africa’s economic development by contributing about 25% of the continent’s GDP and 70% of its employment.

In many countries, most crops are produced by small-scale farmers with limited mechanisation and capacity, leading to poor yields.

Fragmented markets, price controls, underinvestment and poor agri-infrastructure also hamper production. To tackle these challenges, the World Bank Group has increased its annual agriculture investment in Africa from $4.1bn to $6.1bn over the past four years.

In 2018, there were reduced FDI flows to some major economies of the continent, including Nigeria, Egypt and Ethiopia.

But these were offset by large increases into other economies — most significantly SA, which doubled its FDI inflows from $2bn in 2017 to $5.3bn in 2018, predominantly due to investment into mining, petroleum refinery, food processing and ICT. FDI inflows to North Africa increased 7% to $14bn, due to elevated investments in most countries of the subregion.

However, FDI to West Africa fell 15% to $9.6bn (the lowest level since 2006), largely due to the substantial drop in Nigeria. And lower than expected global economic growth, rising trade tensions and tepid economic growth in sub-Saharan Africa, conspired to limit the extent of the FDI increase in 2018 for the continent overall.

In terms of major players, France continues to be the largest foreign investor in Africa — due to its historical links with several countries on the continent and large investments in major hydrocarbon-producing economies, particularly Nigeria and Angola.

The Netherlands holds the second-largest foreign investment stock in Africa, more than two thirds of which is concentrated in only three countries, Egypt, Nigeria and SA.

Interestingly, the total stock of FDI in Africa from both the US and the UK has decreased in the past four years as a result of divestment and profit repatriations.

The stock of China’s FDI in Africa, in contrast, increased by more than 50% between 2013 and 2017.

FDI outflows for all African countries in 2018 dropped by 26% to nearly $10bn. Significant reductions in outflows from Angola and SA largely accounted for the drop.

• Hlophe is EY partner and Africa region government and public sector leader.

Africa-wide free-trade agreement receives major boost

The African Development Bank (AfDB) has provided a $4.8m grant to support the African Union’s efforts to roll out the continental free-trade area. The grant forms part of a series of interventions by the development bank to accelerate implementation of the free-trade agreement. The trade agreement is seen as a major force for integrating the 55-nation continent and transforming its economy. Intra-African trade remains low compared with other major regions such as the EU and Asia.

In 2018, SA joined various other countries on the continent in signing the African Continental Free Trade Area (AfCFTA) agreement that aims to create a single continental market for goods and services, with free movement of businesspeople and investments. With about 1.2-billion people on the continent, the agreement is set to create one of the largest free-trade markets in the world.

Albert Muchanga, the AU’s commissioner for trade & industry, said the AfDB grant would be used for the delivery of various protocols relating to the structure and mandate of the AfCFTA secretariat. The trade agreement is expected to expand intra-African trade by up to $35bn per year, ease movement of goods, services and people across the continent’s borders and boost agriculture and industrial exports by 7% and 5% respectively.

Speaking on behalf of the AfDB’s director of industrial & trade development department, Obed Andoh Mensah said the trade deal will help stabilise African countries, allow small- and medium-sized enterprises to flourish, promote industrialisation and lift millions out of poverty.

“If the AfCFTA is complemented by trade facilitation reforms, reduction in nontariff barriers, improved infrastructure and policy measures to encourage employment and private sector investments, it will stimulate poverty reduction and socioeconomic development across Africa,” he said.

Good news for international investors. Africa’s second most populous country Ethiopia has shown it is now open for business by granting its first ever finance license in years to a foreign-owned company, Ethio Lease.

Here Is All You Need To Know

The license was from the National Bank of Ethiopia which granted the first financial services license to a foreign-owned company, Ethio Lease.

Ethio Lease is a wholly owned subsidiary of New York-based equipment leasing firm, Africa Asset Finance Company Inc. (AAFC).

Ethio Lease will address the equipment and foreign exchange shortages facing Ethiopia by providing local businesses with access to high-quality equipment, allowing businesses to grow their operations and thereby creating jobs and increasing productivity throughout the country.

GDP of Ethiopia

Ethio Lease Is Leading The Way For Explosion In Foreign-Led Investments In Ethiopia

Indeed, this finance license is a major invitation for foreign-led businesses to come invest in Ethiopia. So expect the emergence of a vibrant startup ecosystem led by foreign investors.

The United States is already leading the pack of investors

“Ethio Lease represents an amazing opportunity — tens of millions of dollars of American capital; the latest in manufacturing, agriculture, and construction equipment technology; and a sustainable financial model that unleashes the potential of Ethiopian businesses without adding to Ethiopia’s debt burden. This is a prime example of how the United States invests in Ethiopia,” US Ambassador to Ethiopia, Michael Raynor said,

U.S.-based Africa Asset Finance Company Inc. (AAFC) is a non-banking financial services firm that provides equipment leasing and finance solutions. The firm is headquartered in New York. AAFC’s wholly-owned Ethiopian company, Ethio Lease, specializes in providing capital leases (or finance leases) to Ethiopian businesses for equipment in a range of vertical markets. For additional information, please visit www.aafc.com and www.ethiolease.com.

Here is what Ethio Lease Would Be Offering

Ethio Lease’s offerings include leases for high-quality equipment, mostly in partnership with leading Original Equipment Manufacturers (OEMs). This equipment includes:

Agricultural machinery (e.g., tractors and irrigation equipment)

Medical equipment (e.g., MRI scanners)

Food processing equipment (e.g., imaging technology for coffee sorting)

Large IT equipment (e.g., data center servers)

Drilling rigs (for water bore holes, geothermal and infrastructure)

Power generation (e.g., solar, wind, storage and energy efficient back-up power)

AAFC will provide funding, expertise, oversight and governance to Ethio Lease, which is independently managed by an experienced team of mostly Ethiopian professionals located in Ethiopia. Frans Van Schaik, Chairman and CEO of AAFC will serve as Vice Chair of Ethio Lease.

“Ethiopia is poised for growth as the government takes significant strides to create jobs and improve the quality of life for its population of more than 100 million. By providing leasing solutions to growing businesses, we believe our capital will help stimulate economic activity while generating attractive risk-adjusted returns for our lenders and investors,” noted Van Schaik

A Look At Equipment Finance and Leasing Market In Africa

There is a large, underserved market for non-bank financial institutions in Africa. While equipment finance and leasing is widely used in developed countries and has become a trillion-dollar market in the U.S. where the Equipment Leasing Finance Association (ELFA) estimates the market at 70% of all equipment purchases it’s a different story in other parts of the world. According to the latest Global Leasing Report by the White Clark Group, the Pan-African leasing market was estimated to be just USD 5.4 billion in 2015, while the International Finance Corporation (IFC) estimated the Pan-African market at USD 40 billion in 2017. AAFC believes the increased adoption of leasing will be economically transformative and accelerate the development of many African nations and companies.

“Throughout my career, I saw first-hand the importance of having high-quality equipment in sustaining and growing a business. This equipment not only makes businesses more productive, but it allows them to expand into new sectors and to hire new workers, driving overall economic growth,” Girma Wake, vice chairman of AAFC and chairman of Ethio Lease, said,

Tax War On Online Businesses: Nigerian and Kenyan E-commerce Businesses To Pay VAT

This is going to be deal breaker for online stores in these two countries. Possibly from 2020, all startups and businesses in Nigeria and Kenya that derive their revenue from the internet would have to pay 5% Value Added Tax on goods and services they sell online. Hard day also for online purchasers in both countries. Expect an extra deduction each time you purchase goods or services online, local or international.

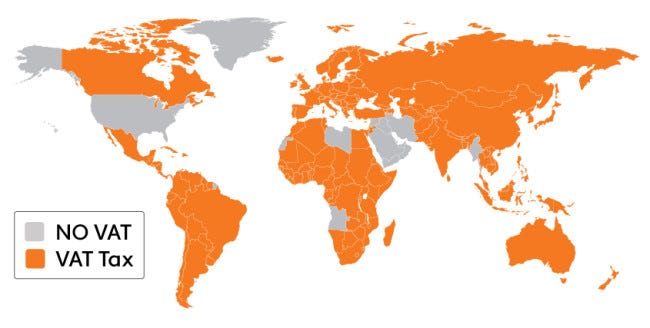

The countries that charge VAT are shown here — it’s most of the world, excluding the United States. Source: AvaTax for WooCommerce

Here Is Why

Kenya

The Kenyan Governments is seriously planning to tax online businesses through new regulations that will be introduced through the Finance Bill 2019. Should this happen online businesses in Kenya will be required to charge VAT once the bill becomes law.

Below are the relevant portions of the proposed law:

Section 3: Section 3 of the Income Tax Act is proposed to be amended by inserting the words:

(1). Subject to, and in accordance with this act, a tax to be known as income tax shall be charged each year of income upon all the income of a person, whether resident or non-resident, which accrued in or was derived from Kenya

(2). Subject to this Act, income upon which tax is chargeable under this Act is income in respect of

A. Gains or profits from:

Any business, for whatever period of time carried on;

Any employment or services rendered;

Any right granted to any other person for use or occupation of property;

B. Dividends or interest

C. a pension, charge or annuity; ii. Any withdrawals from, or payments out of, a registered pension fund or a registered provident fund or a registered individual retirement fund; and (iii) any withdrawals from a registered home ownership savings plan

D.income chargeable to tax includes income accruing through a digital marketplace

e. ‘Digital marketplace’ means a platform that enables the direct interaction between buyers and sellers of goods and services through electronic means

E. AN amount deemed to be the income of any person under this Act or by rules made under this Act;

F. Gains accruing in the circumstances prescribed in, and computed in accordance with, the Eight Schedule

G. Subject to section 15(5A), the net gain derived on the disposal of an interest in a person, if the interest derives twenty per cent or more of its value, directly or indirectly, from immovable property in Kenya; and

H. A natural resource income

Section 5 of the Value Added Tax Act, 2013 is proposed to be amended by inserting the words highlighted

1. A tax, to be known as the value added tax, shall be charged in accordance with the provisions of this Act on –

(a). A taxable supply made by a registered person in Kenya

b. The importation of taxable goods; and

c. The supply of taxable services

2. The rate of tax shall be:

A. in the case of zero-rated supply, 0% or In the case of goods listed in section B of the first schedule 8%

In any other case, 16% of the taxable value of the taxable supply, the value of imported taxable goods or the value of a supply of imported taxable services.

7. The provisions of subsection (1) shall be applicable to supplies made through a digital marketplace

8. For the purposes of this section, a ‘digital marketplace’ means a platform that enables the direct interaction between buyers and sellers of goods and services through electronic means

From the proposed law, it is not clear whether international online businesses that operate in Kenya such as Google, Facebook, Twitter and Instagram who have no physical presence in Kenya will be taxed. However, it is expected that special rules may be formulated detailing the operational mechanics of how taxation of the digital economy will be undertaken.

“Not that it is something new; it actually should be in existence.

“We will certainly follow up to make sure that every VAT that is due to becollected is collected. Soon, we will ask banks to impose VAT on online transactions for purchases of goods and services,”the Chairman of the agency, Mr Babatunde Fowler said.

‘’We Are Going After Everybody’’

The Nigerian agency has further explained that it is hustling hard to meet its N8 trillion revenue target for 2019. And it doesn’t stop with online purchasers.

The FIRS also seriously wants to increase Nigeria’s current tax population to 45 million. To do that, it would be relying on multiple information sources, Mr Fowler said. And that would include invading the country’s Bank Verification Number database and other related agencies with relevant information.

“We are going after everybody. I am sure you have heard that we have placed lien on some accounts of defaulters that have a billion naira turnover annually. So certainly, we are not leaving anyone out of the tax net,’’ he said.

“This will lead to a decline in use of cards online,” says Oluyomi Ojo, founder of Printivo, an online design and printing company. “Merchants will opt for bank transfers and customers will opt for other options. There’s no other way to look at the proposed policy than to see it as a card payment killer.,” he adds

More than 160 countries charge VAT, including China, India, and most of Europe.

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.