Zimbabwe’s central bank, which is battling inflation-inducing exchange rate distortions, has shut down the country’s popular mobile money transfer service, InnBucks, for operating without a license.

InnBucks, which is operated by fast food franchisee Simbisa, is a mobile platform that uses USSD and mobile application technology to enable consumers to send and receive money as well as make purchases at fast food locations.

Mobile money has grown in popularity as a convenient way to store and move US dollar funds across the country.

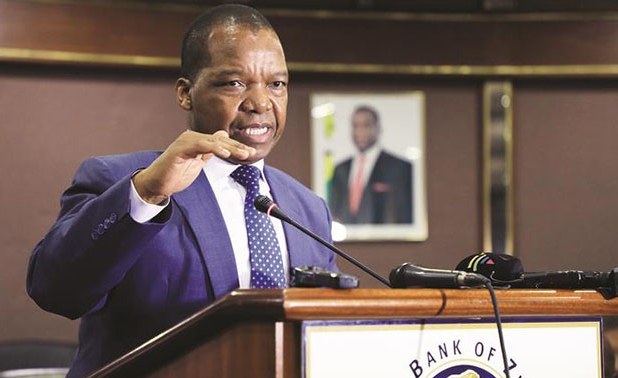

Zimbabwean central bank governor John Mangudya

However, the Reserve Bank of Zimbabwe (RBZ) has declared that it will suspend operations a week after the EcoCash mobile money platform — operated by telco Econet Wireless — got authorisation to accept foreign currency cash-in and cash-out.

“The Reserve Bank of Zimbabwe (the Bank) wishes to inform the public that it has directed Simbisa Brands (Private) Ltd to immediately suspend operations of the money transfer service branded or styled InnBucks,” Zimbabwean central bank governor John Mangudya stated on Wednesday night.

Mangudya explained that the RBZ directed InnBucks in November 2021 to “ask for and secure appropriate approvals to continue operating the service.” The RBZ is Zimbabwe’s central bank and has been putting the screws on mobile money carriers, accusing EcoCash at one point for igniting parallel market currency rates.

“Simbisa has not yet regularized the service as directed, necessitating the Bank’s inevitable regulatory involvement. Customers will no longer be able to deposit funds into their InnBucks account or transfer funds to third parties as a result of the service’s termination,” Mangudya stated.

With a huge and increasing user base, InnBucks is providing a service that was previously unavailable due to delays in approving telco-owned mobile money operators to offer foreign currency mobile money transfer services. Many still rely on traditional money transfer providers and banks, which demand exorbitant fees.

RBZ has extended a grace period to consumers, stating that “customers may redeem their balances for cash or merchandise at Simbisa Brands (Private) Ltd locations within a 30-day period” beginning yesterday.

InnBucks and Simbisa issued a statement in which they stated that they “continue engaged with the regulator regarding their license” concerns. Regrettably, an impasse has formed, and the Simbisa Board is contacting the regulator in an attempt to resolve the matter quickly and amicably.”

Charles Rapulu Udoh is a Lagos-based lawyer, who has several years of experience working in Africa’s burgeoning tech startup industry. He has closed multi-million dollar deals bordering on venture capital, private equity, intellectual property (trademark, patent or design, etc.), mergers and acquisitions, in countries such as in the Delaware, New York, UK, Singapore, British Virgin Islands, South Africa, Nigeria etc. He’s also a corporate governance and cross-border data privacy and tax expert. As an award-winning writer and researcher, he is passionate about telling the African startup story, and is one of the continent’s pioneers in this regard. You can book a session and speak with him using the link: https://insightsbyexperts.com/view_expert/charles-rapulu-udoh

OPay Egypt, the leading fintech and electronic payments startup, said that it has received preliminary approval from Egypt’s Central Bank to issue prepaid cards via its OPay app.

Prepaid cards will be distributed in partnership with the Egyptian Cards Company, the largest card distributor in the local and regional market. OPay Egypt wants to supply all electronic payment solutions in the local market with this latest step.

Hesham Ezz El-Din, Digital and Cards Business line director at OPay Egypt

Customers will be able to load money onto the prepaid cards and then use them to make cash withdrawals and purchases without needing to have a bank account.

These cards offer OPay users a comprehensive suite of financial and payment services.

“We are pleased with our cooperation with the Egyptian Cards Company to issue our prepaid cards. The new cards will provide additional paying options that will greatly contribute in our efforts to provide the best non-banking services to our customers through a smooth and easy payment system represented in the prepaid cards,” Mahmoud khedr, Director of business development and strategic partnerships for Egypt and North Africa at OPay, said. “The prepaid cards will allow our customers to use the cards in paying and purchasing, and meets their financial needs wherever they are.”

He underlined that this partnership will bolster efforts to achieve financial inclusion in Egypt, and characterized it as a practical implementation of Egypt’s National Payments Council’s plan.

In this regard, Khedr highlighted the President’s economic reform effort and the Central Bank of Egypt’s actions, which aided in drawing foreign investors to the Egyptian market, particularly in the payments and collections and fintech sectors.

He also commended the role of The Central Bank’s decisions that “guaranteed an atmosphere of competitiveness, that broadly benefits Egyptian citizens by providing them with the best financial solutions that fit all segments of the society.”

Hesham Ezz El-Din, Digital and Cards Business line director at OPay Egypt, said: “We are working hard to reinforce our presence in the Egyptian local market and offering new electronic payments and collections solutions, as well as supporting our customers through an inclusive system that helps in pushing digital transformation forward and supports financial inclusion.”

These steps, Ezz El-Din said “help us arrive at a non-cash society in light of the strategy of The Central Bank of Egypt and the directive of the Egyptian state within the 2030 digital vision.”

Ezz El-Din said that OPay’s prepaid cards will be connected with OPay’s mobile app, in order to guarantee that the service Meets the needs of the customers.

Connecting the card with the app will allow customers to request the issuance or cancellation of the prepaid card.

Ezz El-Din reiterated that the move also comes as a part of the company’s concerted efforts to expand its branches all over the country.

“OPay seeks to offer the best electronic services in the Egyptian market, while maintaining the highest levels of safety and security for its customers,” Ezz El-Din said.

OPay signed a joint cooperation protocol with the Egyptian Cards Company last year to facilitate issuing banking cards.

Charles Rapulu Udoh is a Lagos-based lawyer, who has several years of experience working in Africa’s burgeoning tech startup industry. He has closed multi-million dollar deals bordering on venture capital, private equity, intellectual property (trademark, patent or design, etc.), mergers and acquisitions, in countries such as in the Delaware, New York, UK, Singapore, British Virgin Islands, South Africa, Nigeria etc. He’s also a corporate governance and cross-border data privacy and tax expert. As an award-winning writer and researcher, he is passionate about telling the African startup story, and is one of the continent’s pioneers in this regard. You can book a session and speak with him using the link: https://insightsbyexperts.com/view_expert/charles-rapulu-udoh

Uganda has passed a law that will impose heavy penalties for vandalisation of key infrastructure. A Shs1 billion fine or a 15 years jail term awaits anyone who is found guilty of vandalizing electricity infrastructure following the passing of the Electricity (Amendment) Bill, 2022. Legislators passed the Bill on Wednesday, 13 April 2022. This passing of the bill comes at a time when the country has been experiencing vandalism of power lines, transformers, poles and other related infrastructure.

The object of the bill is to among others, provide for deterrent penalties for theft of electricity and vandalism of electrical facilities, provide for the membership and funding of the Electricity Disputes Tribunal, and to provide for additional functions of the authority; to increase funds allocated to the ERA from 0.3 percent to 0.7 percent of the revenue received from generated electrical energy.

President Yoweri Museveni of Uganda

The bill also seeks to prescribe the circumstances under which a holder of a generation or transmission licence may supply electricity to persons other than a bulk supplier to industrial parks at a tariff determined by government.

This will eliminate Umeme, the power distribution company, in service territories where it is not licensed and in effect implement the presidential directive of selling power at a tariff that eliminates the expensive distribution costs Umeme.

While presenting the report of the Committee of Environment and Natural Resources on the Bill, the Deputy Chairperson, Hon. Emely Kugonza said the penalty for interference with meters and electrical lines, vandalism and illegal connections should be increased from Shs100, 000 or imprisonment for one year to Shs4 million or a ten-year imprisonment or both for receiving vandalized electrical facilities, repeat vandalism, and interference with electrical works.

However, Members of Parliament said the punishment should be prohibitive suggesting an increase in the fines.

Hon. Milton Muwuma (NRM, Kigulu County South) said that it is necessary to increase the penalties to counter the mushrooming scrap dealers who always source their raw material from vandalism of state property.

“These people vandalize meters, poles and transformers putting the country at a loss. The penalty on vandalism should even be higher than Shs4 million,” he said.

Bugweri County Members of Parliament, Hon. Abdu Katuntu said that there is disrespect of public property calling for ‘a strong punishment on people perpetrates the act’.

Citing the vandalism of the chain link fencing constructed around the Kampala- Entebbe Expressway, Katuntu said serious punishments should be meted on the culprits.

“We need very strong and deterrent measures to curb some members of the public from vandalizing public property. These people need to be scandalized and therefore, the fine should be a minimum of Shs5 million,” Katuntu added.

The Attorney General, Hon. Kiryowa Kiwanuka said defended the need for the hefty penalties.

“The people taking down the power lines and other infrastructure are not the common people down there. These vandals are very sophisticated people. So we need to make the law very deterrent,” he said.

The Chairperson of the Committee, Hon. Emmanuel Otaala defended the penalties saying that a single electricity tower costs Shs300 million and when cut down, it affects to other towers which cost should be met by the vandal.

On the removal of monopoly of distribution of electricity, the committee observed that government owns the largest dams, transmission and distribution assets in the can by policy use the leverage to sell power to industries at a low cost as currently planned in industrial parks.

“Uganda Electricity Distribution Company Limited already has in-house capacity and thus should also be given the responsibility of distributing power to industries in the industrial parks at a tariff determined by government,” the committee report read in part adding that, ‘UMEME’s concession that has 35 months to go would not allow another distributor to enter industrial parks except by an Act of Parliament’.

Recently, President Museveni issued a directive that Presidential power should be sold directly to industries at a tariff that eliminates the expensive distribution costs of Umeme. He said this will spur economic growth through industrialization.

The committee dropped the proposal of listing the successor companies of the Uganda Electricity Board (UEB) on the stock exchange arguing that three companies continue to acquire debt and assets through financing by tax payers.

“It is therefore, inconceivable how companies that survive on tax payers loan repayments can issue shares and securities for the private sector to acquire a stake in them,” Kugonza said.

The committee also proposed an increase in funding of the Electricity Regulatory Authority.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Among the texts published in Tunisia Republic’s Official Journal on April 12, 2022, is a presidential decree outlining the general requirements for the practice of telemedicine and the areas in which it may be applied.

The new presidential decree seeks to build a regulatory framework for telemedicine, which has exploded in popularity during the pandemic.

Here Is What You Need To Know

Under the new law, code-named Decree 2022–318, the operations of telemedicine in Tunisia is now subject to prior authorisation from the Ministry of Health, after due consideration of an evaluation committee, in addition to and authorization granted by the national authority for the protection of personal data (INPDP) in Tunisia.

The Ministry of Health must respond to permit requests within 90 days after receipt of a complete file.

In the event of a refusal, the refusal must be in writing and justified.

The telemedicine platform must also be used pursuant to an agreement between the platform’s owner and the physician or dentist in question. For physicians and dentists in private practice, the agreement must be approved by the appropriate professional organization. The agreement must be endorsed by the relevant sectoral ministry for physicians and dentists practicing in the public sector.

The application for authorization to establish the telemedicine platform must include a full description of the user fees that will be charged to various user categories. The charges associated with the platform’s utilization are established in such a way that health practitioners have fair access to telemedicine services regardless of the number of procedures conducted.

There are no expenses associated with utilizing the telemedicine platform’s pharmacists to ensure the delivery of medications based on electronic medical prescriptions.

Telemedicine for patients residing abroad must be disclosed in advance to the responsible departments of the Ministry of Health and the relevant professional orders.

Under no circumstances may the telemedicine platform be used as a vehicle for advertising health items or as a means of guiding patients to any health service provider.

The data processed in the context of telemedicine acts must be housed and stored in Tunisia, either through a cloud service provider or locally, in line with applicable legislation and regulations regarding computer security and personal data protection.

Telemedicine data must be quickly transferred and saved in the patient’s electronic medical record in a central database maintained by the Ministry of Health’s technological services. The data processed in the course of telemedicine activities performed in organisations and enterprises under the Ministry of National Defense are hosted, saved, and transferred via a dedicated database.

Pharmacists who own retail pharmacies may dispense medicines to the public, except for those listed in Table B and psychotropic drugs subject to the Ministry of Health’s control, through the use of an electronic medical prescription and a secure information system that ensures the protection, security, and reliability of documents and personal data in accordance with applicable law.

All information connected to the act of telemedicine must be traceable, and personal data must be retained for at least ten (10) years. These records must be accessible, with the patient’s or legal guardian’s approval, in the event the patient contacts another doctor to undertake a telemedicine act.

Interoperability, transfer, exchange, and reversibility of acquired data, within the framework of a standard that enables their use by other responsible professional structures and/or other duly authorized platforms.

Before performing any act of telemedicine, the patient’s or, where applicable, his legal guardian’s free and informed consent must be sought, after informing him of the necessity, the interest, the consequences, and the extent of the act, as well as the means used to carry it out.

Charles Rapulu Udoh is a Lagos-based lawyer, who has several years of experience working in Africa’s burgeoning tech startup industry. He has closed multi-million dollar deals bordering on venture capital, private equity, intellectual property (trademark, patent or design, etc.), mergers and acquisitions, in countries such as in the Delaware, New York, UK, Singapore, British Virgin Islands, South Africa, Nigeria etc. He’s also a corporate governance and cross-border data privacy and tax expert. As an award-winning writer and researcher, he is passionate about telling the African startup story, and is one of the continent’s pioneers in this regard. You can book a session and speak with him using the link: https://insightsbyexperts.com/view_expert/charles-rapulu-udoh

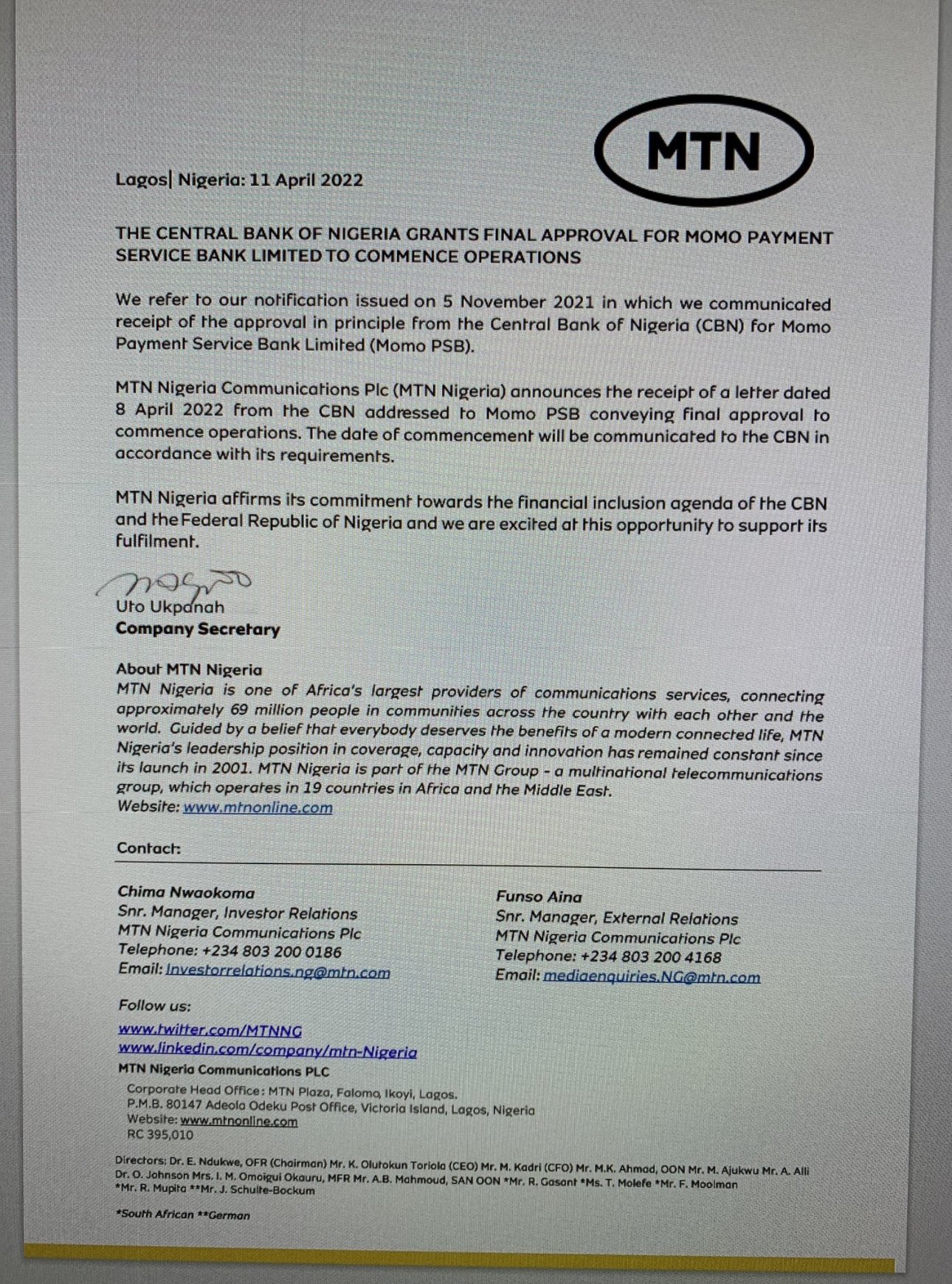

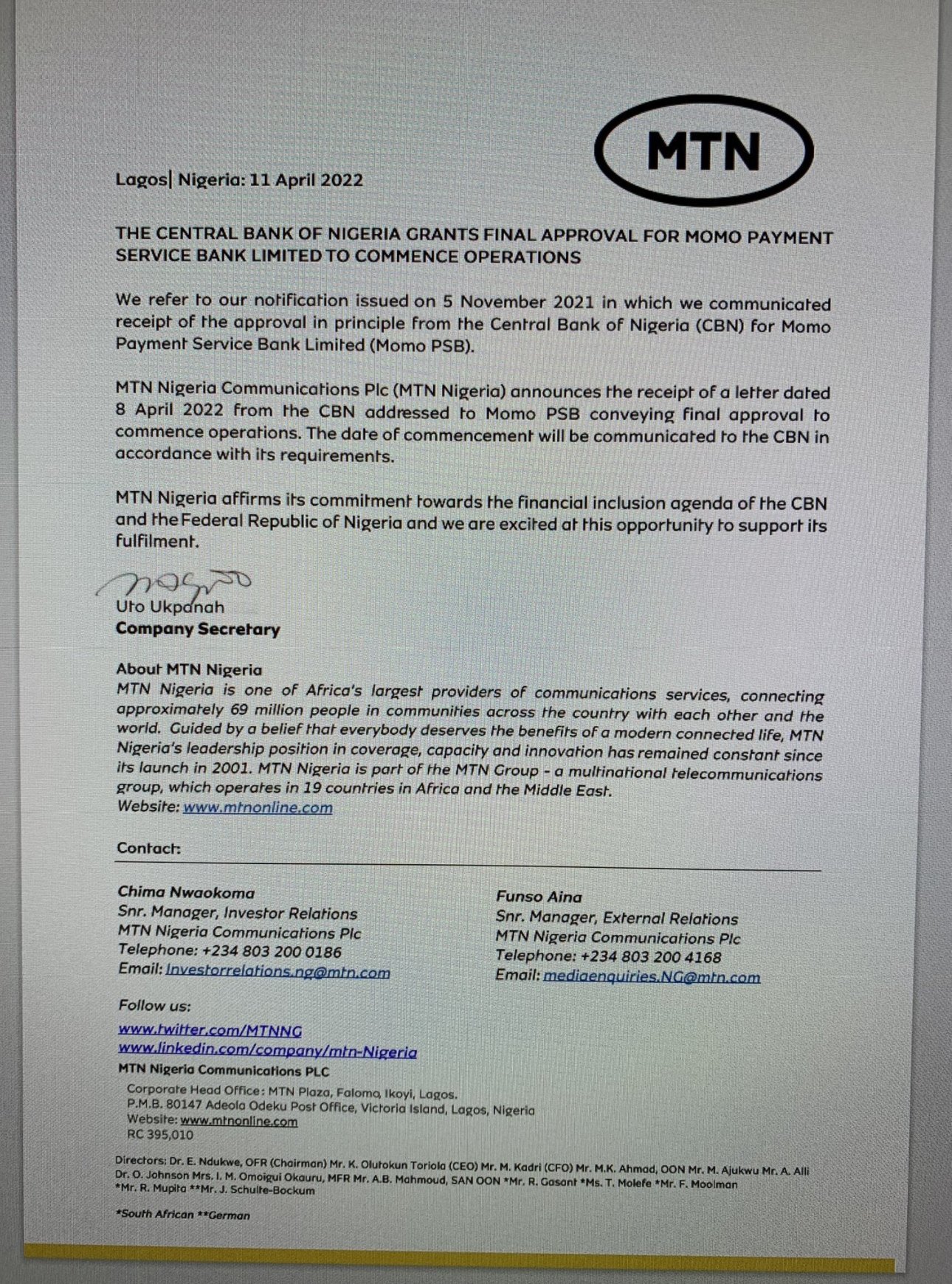

Nigeria’s largest telco by subscriber base MTN, and its immediate competitor Airtel have taken up a new business — that of attempting to beat Nigerian banks at what they know how best to do. The two have been granted one of the country’s most expensive fintech licenses, a payment service bank license, costing over $12.8m in licensing fees. Last year, 9mobile, another of the country’s leading telco, became one of the first set of licensees, alongside Hope PSB and Moneymaster PSB.

The payment service bank license is one of the many types of banking licenses a financial technology company in Nigeria seeking authorisation to operate from the country’s central bank may explore. It is different from other existing banking licenses for financial technology companies because it is one of the few types of fintech licenses that allow the licensee to operate across the country. A majority of others have geographical and structural limitations.

Nigeria’s central bank in its latest update on the payment service bank licensing rules is clear about what purpose this type of bank would serve.

“PSBs are envisioned to facilitate high-volume low-value transactions in remittance services, micro-savings and withdrawal services in a secured technology-driven environment to further deepen financial inclusion and help in attaining the policy objective of 20 per cent exclusion rate by 2020,” CBN said it in its latest rules.

The new banking license from MTN. Credits: MTNNG

But it appears that MTN and Airtel strategically delayed their license applications for the PSB license for a reason: the recently introduced mobile money licensing framework. While all hopes were high that the mobile money operational guidlines would be wider in scope, these hopes were dampened with the eventual release of the guidelines in July this year.

The mobile money guidelines heavily limited the operational capabilities of its licensees, restricting mobile telecoms operators such as MTN and others, for instance, from carrying out substantial banking activities using the model.

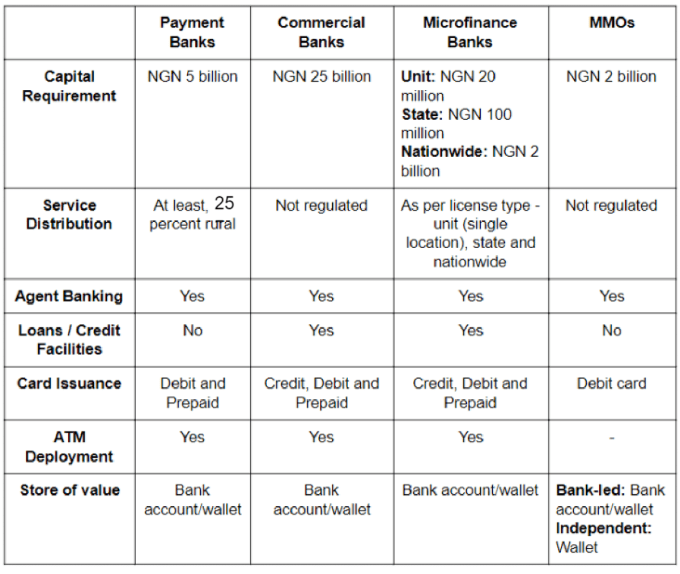

A clearer picture about the differences between Nigeria’s payment service bank and mobile money licenses is painted in the table below. The differences also capture how the payment service bank design will function in practice.

S/N

KEY REGULATORY REQUIREMENTS

PAYMENT SERVICE BANK LICENSE

MOBILE MONEY LICENSE

1

Can accept and hold deposits

YES

YES (mostly via mobile wallets)

2

Cross-border Remittance

YES ( including, inbound cross-border personal remittances)

NOT Specifically stated. Operationally improbable)

3

Deal in foreign exchange transactions

YES (only to the extent of sale of foreign currencies realized from inbound cross-border personal remittances to authorized foreign exchange dealers, only)

YES (only to the extent of sale of foreign currencies realized from inbound cross-border personal remittances to authorized foreign exchange dealers, only

4

Issue cards

YES

YES

5

Lending

NO

NO

6

ATM

YES

NOT Specifically stated (Operationally improbable)

7

Extent of participation allowed to telecommunications companies.

RESTRICTED from accepting payments from the public, apart from airtime billing.

ALLOWED (through their subsidiaries) to accept deposits from the members of the public.

8

Estimates of licensing fees

Over 5 billion naira ($12m)

Over 2 billion naira ($5m)

9

Geographical limitations

NATIONAL (provided not less than 25% financial service touch points in rural areas are set up)

NATIONAL

10

Use of network of agents permitted

YES

YES

11

Who may obtain the license?

i) Banking Agents; ii. Telecommunications companies (Telcos), through subsidiaries; 8 Classified as Confidential iii. Retail chains (supermarkets, downstream petroleum marketing companies); iv. Postal services providers and courier companies; v. Mobile Money Operators (MMOs that desire to convert to Payment Service Banks shall comply with the requirement of this Guideline); vi. Switching Companies; vii. Financial technology companies (Fintech); viii. Financial Holding Companies; and ix. Any other entity on the merit of its application subject to the approval of the CBN

Banks and corporate organisations

12

Primary Regulator

Central Bank of Nigeria

i) Central Bank of Nigeriaii) Nigerian Communications Commission

What Difference Will A Payment Service Bank License, Therefore, Make?

A Payment Service Bank (PSB) is a new category of bank with smaller scale operations and the absence of credit risk and foreign exchange operations. In addition to accounts (current and savings), PSBs can also offer payments and remittance services, issue debit and prepaid cards, deploy ATMs and other technology-enabled banking services. Think of them as basically stripped-down versions of traditional deposit money banks, with limited functionality and a focus on onboarding more of the excluded and marginalised population.

Under Nigerian central bank’s regulations, subsidiaries of mobile network operators (aka telcos), mobile money operators, retail chains (supermarkets) and banking agents are welcome to apply for the PSB license, provided they can meet certain requirements, including a 5 billion naira ($12million) capital base, and a combined 2.5 million naira ($6.4k) application and license fee (which are non-refundable).

The new banking licenses for Nigeria’s leading telcos are coming after the CBN issued an updated and revised guideline for the licensing and regulation of Payment Service Banks in Nigeria on August 27, 2020.

MTN has the largest chunk of the Nigerian telco market with over 74 million subscribers, followed by India’s Airtel with over 52 million users; locally owned Glo at 52 million; and then 9mobile with a meager 12 million users. Visaphone (which is merely an extension of MTN, having being acquired by the telecom giant in 2015 to boost its 4G capacity) comes last with just a little over 137, 000 users.

MTN bank Nigeria MTN bank Nigeria MTN bank Nigeria

Charles Rapulu Udoh is a Lagos-based lawyer, who has several years of experience working in Africa’s burgeoning tech startup industry. He has closed multi-million dollar deals bordering on venture capital, private equity, intellectual property (trademark, patent or design, etc.), mergers and acquisitions, in countries such as in the Delaware, New York, UK, Singapore, British Virgin Islands, South Africa, Nigeria etc. He’s also a corporate governance and cross-border data privacy and tax expert. As an award-winning writer and researcher, he is passionate about telling the African startup story, and is one of the continent’s pioneers in this regard. You can book a session and speak with him using the link: https://insightsbyexperts.com/view_expert/charles-rapulu-udoh

Following the proclamation of the Virtual Asset and Initial Token Offering Services Act 2021, the Financial Services Commission, Mauritius has announced to industry stakeholders and the general public that applications for the relevant crypto and other licence(s)/registration(s) under the Act may now be submitted to the FSC for consideration via the FSC One Platform.

Cryptos

In 2021, the country introduced the Virtual Assets and Initial Token Offering Services (“VAITOS”) Act 2021, which came into force on the 7th of February 2022. The Act establishes a regulatory framework for new and developing activities involving Virtual Assets (“VAs”) and Initial Token Offerings (“ITOs”) in Mauritius, as well as measures to combat money laundering and terrorist funding related with VAs.

Charles Rapulu Udoh is a Lagos-based lawyer, who has several years of experience working in Africa’s burgeoning tech startup industry. He has closed multi-million dollar deals bordering on venture capital, private equity, intellectual property (trademark, patent or design, etc.), mergers and acquisitions, in countries such as in the Delaware, New York, UK, Singapore, British Virgin Islands, South Africa, Nigeria etc. He’s also a corporate governance and cross-border data privacy and tax expert. As an award-winning writer and researcher, he is passionate about telling the African startup story, and is one of the continent’s pioneers in this regard. You can book a session and speak with him using the link: https://insightsbyexperts.com/view_expert/charles-rapulu-udoh

Ghana ’s Parliament has authorized the contentious e-levy. Prior to the voice vote, the Minority in Parliament walked out of the proceedings. The Minority asserts that they do not wish to be identified with the levy.

Haruna Iddrisu, Minority Leader, emphasized his party’s opposition to the bill and accused the government of smuggling it in.

Haruna Iddrisu, Minority Leader

“When the business statement was presented last week, it [e-levy] was not part of the business approved for the house”, he observed. “We have warned time and again and cautioned that we do not want to be taken by surprise on a major economic policy of the government. Parliament cannot be that when a side is convenient with its number, then business can go on. It cannot be. We will not accept that culture. So, when they [Majority] did not have the numbers, they weren’t ready. Now, that they have the numbers, then you say we should do business.”

The new levy is a 1.5 percent charge on the value of electronic transactions. It includes payments made with mobile money, bank transfers, merchant payments, and inward remittances. Except for inward remittances, which will be borne by the recipient, the charge will be borne by the transaction’s originator. For transactions up to GH100 (US$ 16) every day, there is an exception.

According to the Finance Minister, total digital transactions are expected to exceed GH500 billion (US$81 billion) in 2020, up from GH78 billion (US$12.5 billion) in 2016. In just five years, the company has grown tremendously.

While the premise for this new fee is to broaden the tax net, given that the bulk of the population works in the informal sector, it appears to be a simple way for the government to raise income. The news of the levy was met with anger and concerns that it might jeopardize the country’s existing digitization effort.

A Suspended 9% Communication Service Tax

Last year, Ghana’s Communications Ministry ordered Mobile Network Operators (MNOs) to stop passing on the 9% Communication Service Tax (CST) to subscribers.

In a letter addressed to the National Communications Authority (NCA), and published in full below, the Communications Ministry stated that the CST should be treated the same way VAT, NHIL, GETFUND levy and all other taxes and levies imposed on entities doing business in Ghana were treated.

Before the suspension, MTN, AirtelTigo, Vodafone and Glo were charging their customers the full amount of the revised Communication Service Tax (CST) since October 1, 2019.

The CST, which was increased from 6% to 9%, and applied to any recharge purchase by subscribers. For every GH¢1 of recharge purchased, a 9% CST fee was charged the subscriber leaving ¢0.93 for the purchase of products and services.

In 2018, the CST tax was first introduced at an Ad Valorem Rate of 6 per cent.

The Commissioner-General of the Ghana Revenue Authority, Ammishaddai Owusu-Amoah also recently said the agency had not started taxing e-commerce in the west African country.

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

The government of Cameroon has now laid before MPs a bill governing banking secrecy. The bill seeks to include microfinance and electronic payment operators in the old banking secrecy law.

“In light of the advances recorded in the financial and technology sectors, certain components of the current law, which is 18 years old, have become obsolete. Furthermore, the advancements in the financial industry are also accompanied by new hazards associated with the development of illicit activities, such as money laundering, cybercrime, and terrorism financing,” the bill’s explanatory memorandum reads.

Here Is What You Need To Know

If the bill is approved as is, microfinance and electronic payment operators, the fruits of recent financial and technological breakthroughs, will be subject to banking secrecy in the same way that traditional banks are.

According to the draft law, banking secrecy here consists in the requirement of confidentiality to which the institutions subject are bound with regard to the acts, facts, and information concerning their customers that they become aware of in the course of their professions.

However, the article emphasizes that banking secrecy also implies that institutions subject to it must engage with legal authorities that can conduct investigations or administrations that combat money laundering and terrorism financing.

A deposit of more than 5 million FCFA in a financial institution, for example, is required by law to be reported to the National Agency for Financial Investigations (ANIF) for information.

In other words, microfinance and electronic payment operators were not compelled to apply the rights (non-disclosure of bank data) and duties under the old law controlling bank confidentiality (collaboration with judicial and monetary authorities). If parliament accepts this legislation, these new players will be subject to the same laws as traditional banks in the future.

Non-compliance with this banking secrecy (rights and obligations), according to the text given for parliamentarians’ approval, is punishable by imprisonment for three months to three years and a fine of one million to fifty million FCFA, or one of these two penalties only.

The penalties are twofold if the offense is committed by the written press, radio, television, electronic communication, or any other means intended to reach the public.

There is also provision for the institution or branches utilized to commit the incriminated activities to be closed for a set period of time.

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

The Bank of Ghana has cited Spektra Technologies, the operators of the Dash App digital payment network, for operating illegally and ordered them to immediately cease operations.

In a letter dated March 9, 2022, signed by Kwame A. Oppong, Head of Fintech and Innovation at the Bank of Ghana, to Spektra Technologies’ CEO, the central bank stated that it had come to their attention that Spektra Technologies was offering services such as wallet creation, cross-border payment, holding of float balance, as well as bill and utility payment, without the necessary approval.

Governor of the Bank of Ghana, Dr. Ernest Addison

“Payment Service Providers are required to obtain the appropriate regulatory approval from the Bank of Ghana under Section 7 (1) of the Payment Systems and Services Act, 2019, (Act 987) prior to operating a payment service in Ghana,” the letter stated.

As a result, the central bank urged the company to “cease offering the above payment services with immediate effect” until the company had the necessary approval from the BoG.

Additionally, the BoG warned the company that “offering payment services in the country without a license is an offense under Section 9 (1) of Act 987.”

This comes only days after Spektra Technologies announced that it had raised approximately US$32.8 million in funding to develop connected wallets across Africa.

Since January 2019, Dash has been operating in Ghana, linking digital wallets across networks to make payments both domestically and internationally.

Meanwhile, all other Fintech firms that operate with Dash have been instructed to cease operations until further notice.

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

The Competition Commission of South Africa has referred to the Competition Tribunal for prosecution the social media giant, Meta Platforms Inc (previously known as Facebook Inc), and its subsidiaries, WhatsApp Inc and Facebook South Africa for abuse of dominance.

The Commission alleges that Facebook, in the first instance, has decided in or about July 2020 and expressed an ongoing intention to offboard Gov Chat and #LetsTalk, a technology start-up that connects government and citizens, from the WhatsApp Business Application Programming Interface (WhatsApp Business API). In the second instance, Facebook has imposed and/or selectively enforced exclusionary terms and conditions regulating access to the WhatsApp Business API, mainly restrictions on the use of data.

The WhatsApp Business API enables medium and large businesses (and government) to, among other things, message at scale, makes use of advanced automation, integrations with existing eCommerce, building chatbots and tracking metrics.

GovChat launched a platform in 2018 called the GovChat which enables the public to engage with all spheres of government — national, provincial, and local — to report a wide variety of issues such as pothole location and other service delivery requirements.

GovChat also enables government to disseminate critical information to the public en masse such as information related to Covid-19 system tracking, testing and vaccination. GovChat has also enabled the poor to apply on-line for social relief and distress grants. The GovChat has provided government with unprecedent insight into service delivery issues in real time and provides government with the ability to provide targeted solutions more efficiently.

The GovChat is dependent on its continued access to the WhatsApp Business API. The intended offboarding of GovChat from the WhatsApp Business API will harm consumer welfare by removing the efficiency of the GovChat which allows the public to communicate with multiple government bodies through a single platform and will also deprive government of the current services (and future services such as mobile payment solutions) offered by the GovChat.

To illustrate the point, the GovChat messaging traffic comprises of hundreds of thousands of messages daily, the vast majority of which relates to queries from the public to the Department of Social Development relating to social welfare grants provided for children, disabled and indigent members of society, and a significant portion of the traffic on the GovChat relate to Covid-19 information.

The Commission found that the harm to the competitive process is also clear because the decision to off-board GovChat from the WhatsApp Business API and the exclusionary terms for access to the WhatsApp Business API, including restrictions on the use of data, limits innovation and the development of new products and services.

This is in a context in which WhatsApp Messenger enjoys significant economies of scale and network effects advantages. Consequently, the Commission also found that the terms and conditions governing access to the WhatsApp Business API are designed to shield and insulate Facebook from potential competition, such as the potential competition presented by the GovChat and enormous data it has been able to harvest which enables it to develop new services and products.

The Commission has asked the Tribunal to impose a maximum penalty against Meta Platforms, WhatsApp and Facebook South Africa which is 10% of their collective turnover. In addition, the Commission has requested the Tribunal to interdict Facebook from off-boarding GovChat from the WhatsApp Business API and to declare void certain exclusionary terms and conditions for access to the WhatsApp Business API.

The Competition Commissioner, Tembinkosi Bonakele said: “Access to digital markets has now become indispensable. In turn, access to digital markets is dependent on access to digital platforms including, as in this case, access to an important digital communication platform — the WhatsApp Business API. Over and above, data is everything in digital platform markets. In view of the important services provided by GovChat, which provides real time interface between government and the public, and the benefits to competition presented by its business model, Facebook’s decision to off board GovChat from the WhatsApp Business API and its exclusionary terms of data usage are untenable.”

Background Of Facebook’s Woes In South Africa

On 20 November 2020 GovChat and #LetsTalk (complainants) filed a complaint with the Commission against Facebook alleging, among other things, that the respondents threatened to terminate the complainants’ access to the WhatsApp Business Application Programming Interface (WhatsApp Business API) due to alleged violation of the terms and conditions.

Facebook operates in the social media market through the Facebook App, and a photo and video sharing platform and social networking app called Instagram (Instagram App). In 2014 Facebook acquired and obtained sole control of WhatsApp, the firm that provides the WhatsApp Messenger messaging app (WhatsApp Messenger).

WhatsApp Messenger provides increasingly essential channels for users to communicate and for businesses and government to access customers and citizens respectively. WhatsApp Messenger provides these services using data over the internet which goes over-the-top of normal telecommunication services (OTT). It allows users on different mobile network operators, handset operating systems, and devices, to interact seamlessly on one platform that is essentially free outside of any data costs.

GovChat created a citizen-centric engagement platform (GovChat).

The GovChat provides South African citizens with a solution for engagement with the South African national government, government departments, and local government. GovChat integrated government communications to provide online real-time escalation and reporting services, creating a platform which allows government and citizens to connect and engage, with a view to improving service delivery and active citizenry.

Through the GovChat citizens can report civic issues (e.g. potholes) and the complainants are able to compile and provide insights in real time to the relevant government department or municipality. Government utilising the GovChat can visually map the specific locations of reported incidences (e.g. potholes) and can also monitor these complaints in real time via the GovChat.

In addition, by utilising the GovChat, government can disseminate critical information to citizens en masse. The COVID-19 symptom tracking and testing, as well as the provision of related information, is illustrative of this function. Among other things, during the 2020 COVID-19 related lockdown, to date, the GovChat has enabled citizens to digitally apply for social relief and distress grants. GovChat relies on the WhatsApp Business API to provide these services.

On 14 November 2020 GovChat applied to the Competition Tribunal for interim relief in terms of section 49C of the Competition Act. On 11 March 2021 the Competition Tribunal granted the interim order in favour of GovChat interdicting Facebook from offboarding GovChat from the WhatsApp Business API pending the Commission’s investigation of the GovChat complaint. The interim order lapsed on 11 March 20022, and on the same date the Commission filed its referral against Facebook.

Facebook South Africa API Facebook South Africa API Facebook South Africa API Facebook South Africa API

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer