Smart Capital, a management company responsible for the implementation of the national Startup Tunisia initiative, including the country’s Startup Act, has appointed a new general manager. He is Alaya Bettaieb, former Tunisian minister for international cooperation and planning.

Alaya Bettaieb, Smart Capital’s new boss

Previously, the manager was a consultant in investment and technology related activities. With a solid expertise in the financial world, the former minister had to occupy several positions of responsibility in this field. He was co-founder and former president of the Tunisian Venture Capital Association, co-founder of the Euro-Mediterranean Capital Forum, member of the BOD of Licensing Executives Society Arab Countries.

A pioneer in introducing intellectual property and technology transfer issues to the venture capital community in the MENA region, Alaya Bettaieb, 63, holds a master’s degree in physical sciences (Faculty of Sciences of Tunis), a Masters in Petroleum Engineering (University of Southern California) and a Masters in Management Economics (University of Hiroshima in Japan).

Startup Tunisia is a national initiative which aims to make Tunisia a country of Startups at the crossroads of the Mediterranean, the MENA region and Africa. It intends to rely on 3 essential pillars to succeed in this mission, namely to create a favorable legal framework and attractive investment and a favorable ecosystem.

The Fund with a target size of 200 million euros ($241m) with an expected first closing of 100 million euros aims to invest in 13 investment funds dedicated to Startups at each stage of their development.

Lessons from Tunisia’s seeming success with its Startup Act

Tunisia’s Startup Act has largely succeeded because of a collaboration between the public and private sectors. For instance, Smart Capital, the company in charge of administering the Tunisian Startup Act is privately managed, although with public shareholding. The company was approved by the Tunisian Financial Markets Council, and works with the country’s Ministry of Communication Technologies and Digital Economy and the Ministry of Finance. Smart Capital’s mission is simple and straight-forward: design and implement the Startup Tunisia initiative (including among others, the Startup Act and the Fund of Funds ANAVA), in order to make Tunisia a country of startups at the crossroads of the Mediterranean, MENA region and Africa.

Thus, handing over the administration of the Act to a private entity has saved the Act from the bugs of bureaucracy and inefficiencies that eat up most government commissions and agencies in Africa. The company has been promoting Tunisian startups and planning several launches of funds in support of startups, recently.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

The government of Mauritius is taking a bold step by encouraging local startups to express themselves fully. The east African country has announced that startups and innovative companies will lead the Public Sector Transformation Scheme which will be launched by the end of February 2021 by the Mauritius Research and Innovation Council (MRIC). The public sector transformation agenda will encourage innovative companies and startups to develop applications for the public sector. The development and implementation of the program will aim to support public sector agencies, through innovative collaborative projects that would test new approaches and technologies, to improve business processes as well as service delivery.

Mauritius Research and Innovation Council (MRIC).

By the end of this month, startups will startups, innovative companies, SMEs, incubators, incubators will start submitting proposals to the Mauritius Research and Innovation Council (MRIC).

Follow MRIC on Twitter here to keep abreast of the latest developments.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

By the stroke of a regulatory pen, Central Bank of Nigeria, the country’s apex bank, has swept away all investments made in cyptocurrency startups in the west African country. This is coming exactly a year after the country’s Lagos state government had declared a complete ban on ride-hailing services on its major highways. It is also coming barely four months after the country’s Securities and Exchange Commission, in charge of regulating investments and securities, had issued a statement, demanding that all traders in crypto assets must register with the commission. In CBN’s latest move, by a way of a letter signed by Bello Hassan Director of Banking Supervision and Musa I. Jimoh Director of Payment Systems Management Department, all commercial banks and financial institutions in the country have been ordered to close down all bank accounts associated with cryptocurrencies.

“Further to earlier regulatory directives on the subject, the Bank hereby wishes to remind entities that transacting or trading in crypto currencies or facilitating payments for cryptocurrency exchanges is prohibited,” CBN stated in the letter.

“Accordingly, all DMBs, NBFIs and OFIs are directed to identify persons and/or entities transacting in or operating crypto currency exchanges within their systems and ensure that such accounts are closed immediately.

Please note that breaches of this directive will attract severe regulatory sanctions.

This letter is with immediate effect,” the bank further added.

The End Of The Road For Cryptocurrency Startups In Nigeria?

The Nigerian cryptocurrency startup ecosystem is booming, but the worst hit by the new directive from CBN will be local cryptocurrency exchanges many of which have recently become emboldened by the recent statement from the Securities and Exchange Commission which latched some forms of order and legitimacy onto their operations. Apart from returning them to the old ways, the ban is a big dent on investments already made into the startups by investors (most of whom are foreigners). In 2020 alone, investments amounting to over $20m were poured into three Nigerian crypto-based startups— Yellow Card, Bitfxt, and Xend Finance — two of which are cryptocurrency exchanges.

Although Nigeria has been subtly regulating the country’s cryptocurrency market, this is one regulation that has hit home the hardest. The last directive from the central bank was in 2017 when it directed all Nigerian commercial banks and financial institutions never to act as cryptocurrency trading exchange. That directive, however, permitted them to host cryptocurrency trading exchanges run by companies or individuals in Nigeria as long as those exchanges or individuals complied with all rules relating to anti-money laundering and terrorism. (Worthy of note is that under both the 2017 and 2021 regulatory directives, Nigerian commercial banks were given far-reaching powers to decide who operated a cryptocurrency account or not.)

CBN’s latest move follows the most recent warning by South Africa’s Financial Sector Conduct Authority (FSCA) against the growing cryptocurrency scams in the country. The scams relate to one of the biggest Ponzi schemes pulled out by Mirror Trading International, a South African Bitcoin trading company. The company had promised investors a 10 percent monthly return on their investments in Bitcoin. However, on 22 December, 2020 in a letter posted on Telegram, the management of the company reported that they were deceived and that Chief Executive Officer Johann Steynberg of the company might have fled to Brazil. Around 28,000 local and global investors were consequently defrauded to the tune of $644 million.

Cameroon earlier this week also published its first national risk assessment (ENR) of money laundering and terrorist financing with support from the World Bank. The report indicated that over $290m cryptocurrency-linked transactions were made by ‘terrorists’ in 2018 alone.

“While certainty on the state of play of cryptocurrency activity — especially as it relates to the number of players and volume of transactions — in Cameroon is still very much limited in the absence of exhaustive report,” the report revealed, “intelligence reports on secessionist armed groups in English-speaking regions whose bank accounts had been blocked following the initiation of legal proceedings against them for financing terrorism, show that the armed bands are now using “ambacoin” cryptocurrency network to support themselves.”

“It is also not excluded that this funding tool is also used by other criminal organizations such as Boko Haram,” the report further added.

Given that Nigeria has yet to report any substantial scams involving cryptocurrencies, there are already insinuations in some quarters that the move by the central bank may not be unconnected with the recent #EndSars protests mainly waged by young people. At the peak of the protest, CEO and founder of the social media platform Twitter, Jack Dorsey, had called on his 4.7 million followers to donate Bitcoin in support, after the Nigerian government had blocked the accounts of crowdfunding platforms set up in support of the protests. By the time the protests ended, Bitcoin already constituted about 40% of the nearly US$400k raised.

The market for cryptocurrencies in Nigeria is big. According to a recent report by Paxful, a leading peer-to-peer bitcoin marketplace, Nigeria traded 60, 215 bitcoins in the last five years (2015–2016), valued at more than US$566m, making the country the second largest bitcoin market worldwide after the United States. Trade in bitcoin also surged the highest — volume (20,504.50) — in 2020, by Coin Dance’s report.

Crypto startups in Nigeria will be affected by the new rules to banks from the CBN.Paxful Nigerian naira (NGN) Volume USD Equivalent. Source: UsefulTulips.org

The days ahead would be tough for crypto startups in Nigeria who may be torn between staying back in Nigeria and going underground to the black market, or moving to other countries while targeting the Nigerian market. Paxful had stated that Ghana, Kenya, and South Africa remain its main markets in Africa apart from Nigeria. The report from Cameroon also showed that up to 31,000 units of cryptocurrency were purchased in that country by the end of September, 2018. The Financial Services Commission (FSC) of Mauritius has equally, recently, released a regulation making cryptocurrency trading exchanges now eligible for licenses. The FSC had released a 15 — page document outlining the new standards. This was the first time the government of Mauritius would be attaching legitimacy to the securities systems trading on tokens, although from the looks of the new licensing regime, the government appears not to be interested in fully regulating the market — although they still retain the power to revoke licenses and investigate fraudulent practices.

In the meantime, some facts are certain to happen: the act of trading cryptocurrencies in Nigeria will return to its black market days and a lot of staff working for the affected crypto startups may have to be retrenched. The lives of crypto trading exchanges are also hanging on the cliff: they may either opt to file for liquidation in Nigeria or explore other alternative markets. Bitfxt had already announced it is moving to Dubai, in the United Arab Emirates, which had recently passed progressive policies allowing foreigners to set up and own more than 51% of shares in companies without local sponsors —as well as shortened paths to citizenship for foreign skilled workers.

But first, the startups would have to spend some time moving their money resident in crypto-linked accounts in Nigerian banks to other destinations. That, too, would be an adventurous journey.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

crypto startups Nigeria central bank crypto startups Nigeria central bank crypto startups Nigeria central bank crypto startups Nigeria bank

When Aurik Capital, an investment company in South Africa, launched its $6.6 million investment fund for startups in the country in 2019, it knew who it was targeting. It was not targeting oversea investors on whom so much resources would have to be spent in convincing to come invest in South Africa. It was targeting South Africans who wanted to run away from the country’s heavy income tax regime. A regime so heavy that for every 1 million rand ($55k) South Africans earn, they must pay over 400,000 rand ($22k) to the South African Revenue Service (SARS), the national tax collector. As a venture capital company registered under Section 12J of the country’s Income Tax Act of 2009, Aurik would offer one best way of avoiding the payment of the humongous amount. And it works like this: if a South African chooses to invest 1 million rand into Aurik, they will pay no tax. The system has been so successful that as at 2019, over 165 of such Section 12J funds had been registered. The assets under the funds’ management had also risen from R3.2 billion ($213m) to more than R6.7 billion ($448m), in 2019 alone. The unexpected increase had been attributed to more businesses and banks in wealth management advising their customers to make use of the scheme.

Aisha Pandor, E4E Africa partner

But then, there is a big decision South Africans investing through Section 12J would have to make: the venture capital companies would, in turn, invest their funds into startups or other permitted ventures (which are usually highly risky and long-term projects). They would also have to wait for at least 5 years to get back (if at all) their earnings, alongside the accumulated profit, if any.

Simplifying Section 12J, In Full

In simple terms, Section 12J of South Africa’s Income Tax Act of 2009, allows investors who make investments in approved Venture Capital Companies (VCC) — that then invest in qualifying small companies — a tax deduction.

Thus, by investing in a Section 12J venture capital company, the investor not only qualifies for a full deduction of the total investment amount from their taxable income in the relevant tax year, but they are also indirectly supporting the South African economy and the growth of local SMEs. Section 12J is similar to Venture Capital Trusts (VCT) in the United Kingdom, which allow individuals with high net worth to save tax and instead invest in a VCT, which will then invest in startups.

A South African tax-paying entity approaches a VCC with its investment.

The VCC accepts the investment for investments in its portfolio companies and issues the investor with a certificate for the amount invested.

With this certificate, the investor approaches the South African Revenue Service (SARS) and presents the certificate. The certificate empowers the investor to deduct the full value of the investment from their taxable income in that tax year.

Section 12J is so attractive to investors that using it investors can offset any tax on capital gains incurred from the proceeds from the sale of an asset. What this implies is that if in the current tax year a South African taxpayer has a capital gains tax case, the taxpayer will use a portion of his/her income to make an investment in a Section 12J business and write off a portion or all of the tax on capital gains owed.

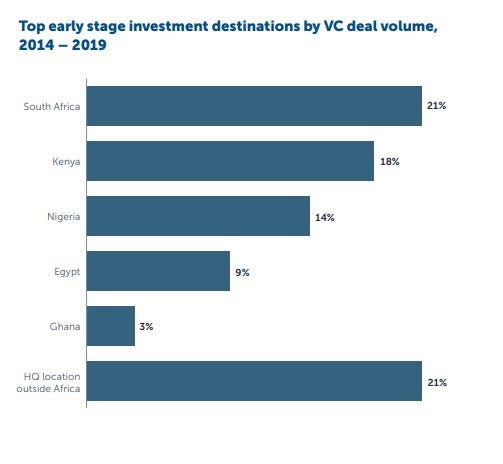

This explains why there are, today, many VC firms in South Africa and why South Africa collected more than 21% of all VC funding deals in Africa between 2014 and 2019, whereas Nigeria only received 14% of the deals, even though Nigeria is the continent’s largest economy and has more than 3 times South Africa’s population.

Section 12J is enabling more investments into startups in South Africa. Source: AVCA

Kalon Venture Partners And E4E Africa Launch New Funds Under Section 12J

Two South African venture capital funds who have announced newest funds under Section 12J are Kalon Venture Partners, a venture capital company based in Gauteng as well as the newly launched Cape Town and Johannesburg-based E4E Africa.

Kalon Venture Partners’ fund targets innovative digital technology companies/startups, and has previously invested in startups such as Yoco, Sendmarc, Ozow, FinChatBot, Mobiz, Flow and Carscan.

In July last year, Entrepreneurs For Entrepreneurs Africa (E4E Africa), got backed by the South African SME Fund, in a founding investment of R135 million ($8.2m). The VC aims to support business models that bring innovative, agile solutions to critical sectors of the South African economy, including the fintech sector, healthcare and the sustainable agriculture value chain, as well as those with the capacity to scale inside and outside of South Africa. It has also invested in the startup Enlabeler.

“It is great to be part of a structure that can really transfer the experience, skills and contacts my colleagues and I have built up over the years to the next generation of entrepreneurs,” said Aisha Pandor, E4E Africa partner, who further noted that she had been constantly approached by early-stage entrepreneurs seeking guidance, fund and general advice.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Looking to raise capital for your startup through investment-based crowdfunding in Nigeria? Nigeria ’s Security and Exchange Commission has put in place a new regulation on crowdfunding which will allow businesses and startups in the country to raise money from the public. The practice is similar to what South Africa already has. Intergreatme, a South African startup, as an instance, recently succeeded in raising over R32.7 million ($2.2 million) by simply putting up an online request for funding in return for shares on Uprise.Africa and getting overwhelmed by public contributions.

Crowdfunding

Below is what Nigeria’s new regulation on crowdfunding is all about.

What Categories Of Businesses Can Raise Funds Through Crowdfunding Under The New Rules?

Under the regulation, only MSMEs (Micro, small and medium enterprises, generally referred to as “startups”, for convenience, under this article) registered as a company in Nigeria with a minimum of two years operating track record are eligible to raise funds through a Crowdfunding Portal registered by the Securities and Exchange Commission. However, if the startup has been less than 2 years in operation, but has a strong technical partner who has been in operation for at least 2 years, the startup will qualify. The startup will also qualify if it has a core investor on ground.

However, some startups are prohibited from raising funds through a crowdfunding portal, and they include those with (i) complex structures (that is, a startup without adequate clarity about its ownership or control which make it difficult to immediately ascertain the beneficial owners of the entity) ; (ii) public listed companies and their subsidiaries; (iii ) startups with no specific business plan; (iv) startups that propose to use the funds raised to provide loans or invest in other entities.

Also, if a crowdfunding portal or any of its officers, directors, shareholders or related persons own or control more than 5% of the shares of the fundraising startup, the startup will be barred from raising funds on the portal. However, the funds may still be raised if approval of the SEC is first sought before the startup is granted access to the portal.

Who Regulates The Fundraising Startups, SEC Or The Portal?

Under the rules, SEC does not directly interface with the fundraising startups. Indirectly, SEC vets the fundraising startups’ crowdfunding applications through the submissions made by the crowdfunding portals on behalf of the fundraising startups. This leaves SEC with far-reaching powers to approve or reject. No procedure was, however, stated in the regulation for appeal against rejection.

How Much Can A Startup Raise Through The Crowdfunding Portal?

Startups are only allowed to raise a maximum of the following amounts within a 12-month period: i) The maximum amount which may be raised by a Medium enterprise shall not exceed N100Million ($260k); ii. The maximum amount which may be raised by a Small enterprise shall not exceed N70Million ($182); iii. The maximum amount which may be raised by a Micro enterprise shall not exceed N50Million ($130k).

For startups that run digital platforms that connect investors to specific agricultural or commodities projects for the purpose of sponsoring such projects in exchange for a return (such as FarmCrowdy, the maximum amount they may raise through the portal within a 12-month period is N1bn ($2.6m), which may be increased if the startup obtains approval from SEC.

How Can Startups Crowdfund Under The Regulation?

For startups in Nigeria desiring to raise funds under the crowdfunding regulation, the following steps must be followed:

The startup must fall under the categories of businesses allowed above.

Application for registration as a fundraiser to a crowdfunding portal (similar to Uprise.Africa in South Africa) is then made. A Crowdfunding Portal is a Nigerian company which must maintain capitalization to the tune of N100 million. The portal must also run a website, portal, application, or other similar module that facilitates interaction between fundraisers and the investing public.

Due Diligence is then conducted on the startup by the crowdfunding portal. The due diligence exercise will, cover, among other things, (i) background checks on the startup to ensure fit and properness of their board of directors, officers and controlling shareholder(s); (ii) the business proposition of the startup.

Once the application has been accepted by the Crowdfunding Portal, the startup will then proceed to raise funds from the public, in return for corresponding shares in the business.

However before raising the funds, every fundraising startup shall issue an offering document, which must contain information such as (i) warnings to investors (ii) the name and address of the startup, directors and officers; (iii)holders of more than 5% of the startup’s shares; (iv)description of the business of the startup; (v) principal risks facing the business of the startup; (vi)use of proceeds; (vii) target offering amount (and a deadline to reach the target offering amount); (viii) risk factors; (ix) related party transactions (x) exit options for investors, etc.

The offering document must be published to the investors through the crowfunding portal.

For now, only plain vanilla bonds/debentures, ordinary shares and other investment instruments can be issued in return for the investors’ funds by the startups.

Throughout the fundraising period, startups will be rigorously monitored by the crowdfunding portal.

Accordingly, the monitoring will extend to the conduct of the startups, and the portal is empowered to take action against any misconduct of the startups. The portal will also monitor fundraising startups to ensure that the fundraising limits imposed on the fundraiser are not breached. Furthermore, the portal will monitor investors to ensure that the investment limits imposed on the investors are not breached.

To this effect, the portal is required to file regular reports about the fundraising startups and their conducts throughout the fundraising period with SEC.

What Happens When Investors Invest In A Startup Through The Crowdfunding Portal?

Under the regulation, investors may be allowed to invest in startups hosted on the crowdfunding portal as long as they comply with the investment limits specified by SEC. For now, retail investors may not invest more than 10% of their annual income in a calendar year; and (ii) Sophisticated, High Net worth and Qualified Institutional Investors are not subject to any limits.

While fundraising, it forbidden for a startup to hold a fundraise on different crowdfunding portals at the same time.

At the end of the fundraise, investors will be allowed a period of 48 hours during which they may withdraw their investment.

If there is a big change which will affect the fundraiser, the investors will be given the option to withdraw their investment if they choose to do so within 7 days after they have been properly notified.

Should the investor decide to cancel his/her participation in the fundraise, all funds which may have been debited from or blocked in their account shall be refunded or released within 48 hours of the request to cancel.

However, once the investors have invested, their investment funds become locked in after they have been allotted shares or other investment by the startup. This remains so until after one year, except under some exceptional circumstances such as where the investors transfer their shares to other retail investors, family members, the startup itself, a high net-worth individual or an institutional investor.

In any case, retail investors are entitled to withdraw from the startup or to sell their shares, whenever controlling shareholders transfer control of the startup to third parties within three years from the conclusion of the offer.

How Are Funds Invested Through The Crowdfunding Platform Treated?

Under the new crowdfunding regulation, every crowdfunding portal shall appoint a custodian who shall establish and maintain a separate trust account for each funding round on its platform. The custodian must be a financial institution registered by SEC as a Custodian.

Funds invested will be maintained by the Custodian in a trust account and will only be released to the startups after certain conditions are met.

To begin with, funds raised would only be handed over to the startups if the target amount or the lowest threshold of funds to be raised is met.

Where the lowest threshold is not reached at the end of an offer, the crowdfunding portal shall effect a refund to all investors within 48 hours.

Investors shall have the right to withdraw any offer or agreement to purchase the securities or investments instruments 48 hours after the closing date stated in the startup’s offering documents.

Thereafter, an investor is only able to cancel in the event of a material change to the offering.

Where the funding target is reached, the crowdfunding portal shall make funds available to the startup within 24 hours provided that where the fundraiser is a public startup or a public startup by default, the portal shall require evidence of registration of the securities with the SEC prior to transferring the funds to the fundraiser (where applicable).

Where the amount raised meets the minimum amount but falls short of the target amount, the fundraiser shall provide a revised plan for the proposed use of funds to the investors and the portal, provided that the underlying project(s) to the proposed use of funds can be downscaled and executed independently without negatively impacting operations of the startup.

A crowdfunding portal shall take all reasonable steps and establish measures by which it is able to verify that the proceeds raised from its platform are utilized for the stated purpose.

For an offer to be successfully completed, the minimum amount indicated in the offering document which must be sufficient to accomplish the business objectives of the fundraiser must have been subscribed for.

How Long Does Each Crowdfunding Campaign On The Portal Run?

A funding project will run on a crowdfunding portal for not more than (60 days), although the period may be extended for a further period of not more than 30 days upon such conditions as may be specified by the portal.

As An Investor, How Are Personal Data Treated Under The Rules?

The rules make extensive provisions for the protection of personal data. Among other things, it provides that the crowdfunding portal must ensure security and confidentiality of information collected from investors. They are also required to keep all a copy of all relevant documents used on the portal for a period of at least 7 years. The fundraising startups are, themselves, required to maintain an accurate list and details of all investors after the fundraising.

Are Startups Required To Pay Any Fees Under The Rules?

Yes. Startups fundraising through the crowdfunding portals are required to pay fees only to parties involved in each crowdfunding campaign, such as the crowdfunding portal or the startups’ solicitors or accountants, provided that the total fees paid do not exceed 5% of the total funds raised in each campaign. The startups are totally forbidden from paying directly or indirectly a commission, finders’ fee, referral fees or similar payment to any person in connection with an offering other than to the crowdfunding portal.

What Are The Likely Difficulties A Startup May Face Should It Explore The Crowdfunding Option?

Under the new rules, some of the greatest barriers a startup may face should it explore the crowdfunding options include that:

The extent a startup may go with the publicity of the fundraising is largely limited. The crowdfunding portal and the startup are limited to their websites at all times, and are therefore restricted from posting about any crowdfunding campaign on other platforms, such as the social media. The crowdfunding portal is empowered to vet each marketing material that goes out through the startup. This will limit the capacity of the startup to raise funds quickly.

Compared to other jurisdictions, the largest amount available to a startup, apart from a commodity investment platform, from each crowdfunding campaign in a year is only limited to N100m. In South Africa, startups can raise as much as $2m or more. In the US, companies raising money through regulation crowdfunding can now raise up to $5 million. N100m is only about $260k, depending on the most current exchange rate of the Naira.

Again, the definition of an MSME under SMEDAN only largely worsens the case as most startups substantially lack the capital to meet the requirements of the definition. This situation does not augur well for a society interested in allowing technological innovations to flourish. Nothing stops Nigeria from going ahead to enact a “Startup Act” like Tunisia or Senegal, in this regard.

Furthermore, the process of obtaining a signed acknowledgement on disclosures on investment risks from the investor by the startup is quite unclear and, will to a large extent, deter investors from such investments. A better clarity would have sufficed.

There is no certainty as to the recommended 2-day approval period given by SEC for startups who have submitted their applications for crowfunding. Thus, this gives room for an application to last for ages before it is approved.

Again, SEC requesting to see and approve every crowdfunding application before being listed on crowdfunding platforms amounts to double (or over) regulation, and a huge disincentive to the intermediary portals who apparently look like messengers, and who are required not to charge more than 5% of the total amount of the funds raised, legal or accounting fees included. Why not ask the fundraising startups to submit their applications directly to SEC?

Finally, like always, the regulations around foreign crowdfunding portals remain largely nebulous and open-ended.

NB:

Micro Enterprises in Nigeria are those enterprises whose total assets (excluding land and buildings) are less than Ten Million Naira with a workforce not exceeding ten employees.

Small Enterprises are those enterprises whose total assets (excluding land and building) are above Ten Million Naira but not exceeding One Hundred Million Naira with a total workforce of above ten, but not exceeding forty-nine employees.

Medium Enterprises are those enterprises with total assets excluding land and building) are above Fifty Million Naira, but not exceeding One Billion Naira with a total workforce of between 50 and 199 employees — Source: SMEDAN Nigeria

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Nigeria new regulation crowdfunding Nigeria new regulation crowdfunding Nigeria new regulation crowdfunding Nigeria new regulation crowdfunding

Ghana’s technical working committee charged with producing the Ghana Startup Bill is back to work after some break.

The Technical Working Committee which was set up in October last year by the Ministry of Business Development, through its agency, National Entrepreneurship and Innovations Program (NEIP), has previously held series of stakeholder consultations leading to the drafting of the bill.

Mr. Sherif Ghali, project coordinator

What Is The Progress So Far?

Yesterday, January 29, the committee, again, held a meeting at the PEF conference room at the Ghana Institute of Management and Public Administration, Greenhill, Accra. The coordinator of the project Mr. Sherif Ghali said the committee did engage stakeholders last year to draft the act and that the project is now in the final phase.

“Currently, we have the 3rd draft of the act which have gone through lots of stakeholder engagements. We are now working to finalize it and to do our last engagements with the startups and other relevant stakeholders before we present it to sector minister ” he indicated

The committee is required to complete its work by the end of February 2021 and then send the draft bill to the Ministry of Trade and Industry, the Attorney General, Parliament and the Office of the President.

The committee, which has a mandate to within three months engage widely with all relevant stakeholders to come out with a draft Ghana Start-up Act, will among other things deliberate to;

Set up an incentive framework for the creation and development of Start-ups in Ghana to promote creativity, innovation, and the use of new technologies in achieving a strong added value and competitiveness at the national, regional, and district levels.

Provide the legal backing for business starting and promotion of Start-ups for decent job and wealth creation, in accordance with the SDG 8, among others.

The committee will then present its final work — the draft Ghana Start-up Act, to the NEIP and subsequently to the Ministry of Business Development, Ministry of Trade and Industry, Attorney General, Parliament of Ghana, and the Office of the President, after which they will run series of advocacy to ensure the Act is passed by Ghana’s legislature.

“Startups are the basics to create jobs and wealth in this country,” Dr Awa said. “We want to help start young people grow and this Startup Bill will be able to help them [youth] own their businesses and not look up to government for job; because we all know that the jobs are not in the public sector, they are in the private sector.

“So we [government] want to create an enabling environment in the private sector that can make it attractive to young people for them to engage in,” he emphasised.

The first specific startup law globally was passed in Italy in 2012, and Africa is increasingly catching on. Tunisia and Senegal are the only countries in Africa that have passed the Act, although plans are being mulled by Rwanda, Kenya, Ethiopia, Mali to follow suit.

Ghana’s Startup Act’s drafting committee is made up of notable bodies such as Ghana’s National Entrepreneurship and Innovation Program (NIEP), Ghana Chamber of Young Entrepreneurs (GCYE), Ghana Start-up Network (GSN), Ghana Hubs Network (GHN), i4Policy and Private Enterprise Federation (PEF) with funding and technical support from GIZ Make IT.

The Technical Working Committee, made up of experts and the ecosystem enablers was equally set up to champion the advocacy action for the development and enactment of the proposed Ghana Startup Act.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Barring any other plans, Kenya is set to launch a crackdown on Savings and Credit Co-operatives (SACCOs). In a notice issued on Friday 29 January by John Mwaka, CEO of the Societies Regulatory Authority (SASRA), SACCOs undertaking the stated non-deposit-taking enterprise SACCO (BOSA) were granted various deadlines for compliance with the components of the Acts and Regulations 2020.

John Mwaka, CEO of the Societies Regulatory Authority (SASRA)

“Notice is further given that upon the expiry of the transition period on June 30, 2021, no SACCO Society shall be allowed to undertake or continue undertaking the specified non-deposit taking business, unless the SACCO Society will have complied with the Act and the Regulations 2021,” the notice read in part.

Institutions are expected to include, within the next thirty days (since the date of publication of the notice), specific information and other information relating to SACCO companies by filling in the details and information of SACCO non-withdrawable deposit companies.

SACCOs that are expected to provide detailed details on the direct or indirect effect of the application of Regulations 2020 will be consulted directly by the Authority.

The SACCOs were directed to apply to the Authority, within six months of the starting date on or before 30 June 2021, for authorization in compliance with the regulations. Institutions will have access to an application template that can be downloaded from the Authority’s website or written to the Authority upon request.

SACCOs were also expected to take account of the criminal and supervisory penalties for non-compliance provided for in Regulation 96(6) of the 2020 Regulation. SASRA is the principal government agency responsible for the SACCO Society’s oversight and control in Kenya.

There are 187 registered SACCOs in Kenya with 162 licensed to conduct Sacco deposit-taking business as of 30 December 2021, while 12 have been issued conditional deposit-taking licenses and three have ceased Sacco Business deposit-taking and are therefore not allowed to accept withdrawable deposits or provide payment services from their members.

SACCOs are an integral part of Kenya’s financial system and account for an estimated 10% of deposit-taking intermediaries’ assets.

A 2017 banking report reported that three million Kenyans are provided with services by saving platforms and often provide services that can not be found elsewhere, such as in rural areas where many farmers depend on them for credit and payment services.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

The time limit for businesses to send the names of shareholders or controlling bodies to the Kenyan government has been extended by six months. The country’s Business Registration Service (BRS) said that it had received more applications from those keen to comply.

BRS Director General Kenneth Gathuma

“We had previously issued a deadline of January 31, 2021. Having taken note of the progress made in filing these registers and in the spirit of encouraging compliance with the Companies Act, BRS has in consultation with stakeholders granted a final grace period of six months ending July 31, 2021,” said BRS Director General Kenneth Gathuma in a statement.

“Failure to comply with this requirement after July 31 makes it an offence to the firm and every officer of the company who is in default. Such an officer will be liable to a fine upon conviction.”

At the end of this month, the deadline for individuals to file e-register beneficial ownership data at the Companies Registry in accordance with the Companies Act, 2015, was set.

The goal of the drive to implement the law is to increase transparency in company shareholding as the State cracks down on illegal cash flows such as money laundering and funding terrorism.

Failure to comply can lead to a fine for the company and officials of up to Sh500,000 ($4.5k).

BRS said it had initially operationalized the e-register for private limited companies and would do the same for other companies’ e-registers, but warned the public of the drawbacks.

“We advise the public to be cautious of persons soliciting money to facilitate them in complying with this requirement.”

BRS said it had initially operationalized the e-register for private limited companies and would do the same for other companies’ e-registers, but warned the public of the drawbacks.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

4 Tunisian startups have been chosen to be part of the first cohort of the sandbox of the Central Bank of Tunisia, that is to say a test environment for their products. The chosen fintech companies are Kraoun, Instaclear, TLedger and Sqoin & Coinsence. The companies will test and validate their fintech solutions in order to have them approved. The duration of the trial period is 9 months.

During the testing period, candidates will provide solutions related to customer identification, cryptocurrency, cross-border clearing and digital core money creation through cutting-edge AI and blockchain-based technologies.

A Regulatory Sandbox refers to a process that determines the development of the fintech industry in a structured way. Financial products and services are based on new technologies that can be tested in the sandbox without meeting all regulatory requirements. At the end of the testing period, all participants who meet the standards of the regulators’ test criteria can apply for authorization or approval.

This allows existing financial institutions and new entrants to experiment and innovate their financial services over a period of time.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Kenyan startups may see more investments if the Kenya Citizenship and Immigration (Amendment) Bill 2020 sails through. By the terms of the proposed new law, Kenyans living in the diaspora may receive special benefits, including wealth security, to allow them to invest back home.

Senator Irungu Kangata

“The Cabinet Secretary may liaise with financial institutions in Kenya to negotiate favourable terms on the investments of any contributions that may be made,” the Bill, sponsored by Murang’a Senator Irungu Kangata, states.

A Big Bait On Kenya’s Large Remittance Market

The proposed new law will see Kenyans sending more money home than they used to. In 2020, Kenyans living abroad defied the pandemic to send Sh337 billion ($3bn) home, according data released by Central Bank of Kenya (CBK). The figure represents a significant increase from the Sh305 billion recorded in 2019. The money sent back home in December alone went towards the festivities and into school fees funding. The voluntary savings scheme proposed by the new bill will not only allow Kenyans living in the diaspora to form associations and voluntarily contribute contribute to a saving scheme, but will also allow them to invest in Kenyan projects and programmes.

“The Cabinet Secretary, may in consultations with the Cabinet Secretary for Treasury and the governor of Central Bank, develop policies and programmes offering incentives to Kenyans living abroad to invest in Kenya,” the Bill states

Key actors under the bill will be Foreign Affairs Cabinet Secretary, who is required alongside the Central Bank governor, to establish a database setting out information on programmes and projects in Kenya for investment by Kenyans living abroad. Among other things, the Bill requires the Cabinet Secretaries and the governor to put in place measures for the prevention of fraudulent practices that hinder investment, in Kenya, by Kenyans living abroad.

The passage of the bill will most likely be a mere formality as the east African country has most recently launched its first ever Diaspora Investment Fund. The fund which is being managed by African Diaspora Asset Managers (ADAM), an investment firm that has been granted the first licence of its kind by the Kenyan Capital Markets Authority, will among other things, provide a safe and regulated investing body for Kenyans living overseas. It will also allow payments to be made using Kenya’s popular mobile money platform M-Pesa, enabling Kenyans to make investments from as little as five dollars.

“The use of technology will be the hallmark of the five diaspora funds, available to investors from all over the world as well as Kenyans. Using the ADAM mobile app, they are able to invest, check their investment balances and even sell their units in real time using VISA cards, bank accounts and MPESA,” Susan Muigai, ADAM’s head of global business development, said.

Almost three million Kenyans living in mostly North America and Europe sent an estimated $3bn in remittances to Kenya in 2019.

While remittances are usually sent to families, direct investment is also common.

“Kenyans living in the diaspora send billions home every year, but mostly for consumption and social support. A few have tried their hand in investments including real estate and farming, but without a way to establish what is happening on the ground, it has in numerous instances ended up with them losing their hard-earned money. We are delighted with this development, as all this will now be a thing of the past, as those investing through these licensed diaspora Funds will have the recourse and protection of the CMA as a regulator,” Abubakar Hassan, director of market operations at the Capital Markets Authority, said.

If the investments from the Kenya diaspora are well managed, they could be a huge opportunity for startups in the country. Despite a population of about 52 million people, about four times smaller than that of Nigeria, Africa’s most populous and richest country, startups in the east African country raised the largest funding amount in 2020 with over $194 million recorded, ahead of Nigeria’s $170 million, according to the latest data gathered by Startuplist Africa on the African Startup Ecosystem.

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer