The plan is not only to allow international operators to enter Ethiopia’s telecom market, it also involves letting state-owned telecom company, Ethio Telecom go international. This is what the country’s latest regulation modifying the rules establishing the telco has stated. The new Ethio Telecom Establishment Regulation approved by the Council of Ministers two weeks ago, apart from allowing Ethio Telecom to explore the country’s financial services industry, would also enable the firm to explore the international market.

Frehiwot Tamiru, CEO of ethio telecom

“The regulation will boost our capacity and expand our reach both locally and internationally,” said Frehiwot Tamiru, CEO of ethio telecom.

“There has been unmatched growth of our assets and paid-up capital. Our total assets grew by 42 percent using IFRS reporting standard, while our paid-up capital remained unchanged at 40 billion Birr before the regulation came into effect,” Frehiwot added.

Here Is What You Need To Know

In addition to allowing Ethio Telecom to invest locally in the mobile banking sector and provide digital finance services, the new Establishment Legislation grants Ethio Telecom the freedom to participate in various sectors of the global market.

The regulation also increased the paid-up capital of Ethio Telecom from Birr 40 billion (USD 1 billion based on current market price) to Birr 400 billion (USD 10 billion), making it Ethiopia’s most capitalized state-owned enterprise.

“We want to provide mobile banking services as long as our telecom infrastructure permits,” said Frehiwot, of the new regulation which also permits Ethio Telecom to venture into financial services. Frehiwot, however, said it would not outsource future mobile money services to third parties. “We may consider partnerships after utilizing our full potential,” he said.

In the first half of the current financial year, the telecommunications provider, which aspires to become the preferred telecommunications operator among customers and partners in Ethiopia, said it posted revenues of Birr 25.5 billion ($646m) , achieving 95 percent of its target. It also said there was a 12.3 percent rise in sales compared to the same time last year.

Although mobile voice contributes to almost half of the company’s sales, 26 percent contribute to data and internet, and the rest comes from foreign market, value-added services, and other sources. During the first six months of the 2020/21 financial year, Ethio Telecom also generated USD 80.2 million in forex marketing new revenue streams.

Last week, the telecom provider invited telecom providers bidding to obtain a license in Ethiopia to share its infrastructure, with 50.7 million subscribers and a regional reach of 85.4 percent. Orange, MTN and Safaricom have shown an interest in leasing ethio telecom properties so far and are exploring new business models and agreements on how to do so.

“We want to benefit more from leasing our telecom infrastructure. We must diversify our source of income that mostly comes from voice call and internet,” Frehiwot said.

Plans have been on since October 2019 to allow private companies (mostly foreign companies: two out of either Etisalat, Axian, MTN, Orange, Saudi Telecom Company, Telkom SA, Liquid Telecom, Snail Mobile, and Global Partnership for Ethiopia, a consortium of telecom operators comprising Vodafone, Vodacom, and Safaricom) to take up to 40% stake in Ethio Telecom.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

The Republic of Benin is the first country in the world for the ease of setting up a business from your mobile phone. The small West African country ranks the same as Estonia but is ahead of New Zealand, Georgia, Hong Kong and China. Many young Africans, bombarded daily by the Africa-bashing of mainstream media, will not believe it. Yet that is what Iran Richard, Economic Affairs Officer in the Investment and Enterprise Divisions of the United Nations Conference on Trade and Development (UNCTAD) has said.

In an article published in November in the Inter-Press agency and taken up by UNCTAD, Ian Richards maintains that the creation of a business in Benin is done in ten minutes on the platform mon.entreprise.bj managed by the Agence de Promotion des Investments and Exports (APIEx).

“The procedure is simple in Benin to create your own business. You just have to log in and provide your information, photograph and upload your ID documents and pay the subsequent fees. A few hours later, an e-mail is sent to you with the documents of incorporation of your company,” affirms the economist in comments reported by www.24haubenin.info.

Benin business registration Benin business registration

World Bank Ease of Doing Business, 2020. Source: World Bank

The various reforms were registered by Benin since the arrival of President Patrice Talon to power in 2016. The country’s Minister of Finance, Romuald Wadagni, was recently awarded with the trophy of Best Minister of Finance on the sidelines of the third edition of the Financial Afrik Awards. The country also recently celebrated the issuance of its latest eurobond, (the first for an African country in 2021) a few days ago on the international financial market.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

The Kenya Revenue Authority (KRA) has declared that the newly imposed Digital Service Taxes would have to be paid by all influencers doing business on digital platforms. The taxman noted in a public notice that there is a rising number of influencers who do not file tax returns or pay transaction taxes.

Kenya Revenue Authority (KRA)

“Social media influencers will be liable to pay digital service tax since their income is derived from or accrued from the provision of services through a digital marketplace or by providing digital advertising services in Kenya,” the statement read in part.

Here Is What You Need To Know

An influencer is a person who commands a follower through a media network through the goods or services they use or participate in to drive sales or popularity, says to the taxman.

DST on sales from services offered through the digital marketplace in Kenya was implemented by the Finance Act 2020 and will be applied to the gross transaction value at 1.5 percent (exclusive of VAT).

“Kindly note the tax will be collected and remitted by agents appointed by the commissioner of Domestic Taxes,” KRA added.

The authority said last week that it was targeting more than 1,000 companies and individuals under the new digital taxes.

It added that, at the time of the transfer of payment for the service to the service provider, the tax is due.

Already, the plan to tax social media influencers has generated controversies across different social media platforms. Below are some of the conversations:

They must pay tax. Pesa iko. A gig can go for 200k. Besides,Some have turned into deadly propaganda machine, promoting impunity and trending government and political hashtag that are utterly detrimental. They'll promote any hashtag. Paying tax will create a form of responsibility

Follow the discussions, including who will be appointed tax agents (whistle blowers) against media influencers, on Kenya Revenue Authority’s Twitter handle here.

The new 1.5% ‘Digital Service Tax’ (DST) imposed on the gross transaction value of services is due at the time of payment.

Additionally, under Kenya’s new 2020 Value Added Tax (Digital Market Supply) Regulations, digital marketplaces (ecommerce websites) that fail to pay Value Added Tax (at 14%) pursuant Section 5(8) of the country’s Value Added Tax Act, 2013 shall, in addition to the penalties prescribed under the law, be liable to restriction of access to their websites in Kenya until such tax is paid.

“A digital marketplace supplier from an export country who is required to register under the simplified VAT registration framework shall apply to the Commissioner for registration within thirty days from the publication of these regulations,” the regulation reads in part.

Under the regulation, any person offering taxable services through a digital marketplace (ecommerce) shall be required to register for tax in Kenya.

The new tax now means that if, for instance, you are are taking an Uber and the cost of the trip is KES 100, the digital service tax is KES 1.5. If the fee is KES 200, the tax is KES 3.

The Kenya Revenue Authority (KRA), in charge of implementing and enforcing taxes in Kenya, has said it has created a special unit to track transactions and tax multi-nationsl using data-driven detection.

One will be subject to DST if one provides or facilitates provision of a service to a user who is located in Kenya.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

The Algerian government is increasingly showing great friendship with the country’s startup ecosystem. Apart from recently tearing down the boundaries hitherto restricted startups from participating in Algerie Telecom’s public procurement processes, the country’s Minister of Post and Telecommunications, Brahim Boumzar, has announced the official launch of a partnership project between Algeria Post and startups.

Minister of Post and Telecommunications, Brahim Boumzar

Here Is What You Need To Know

According to Mr. Boumzar, the objective of the partnership is to support the postal sector to accelerate the popularization of electronic payment.

The minister explained that the leaders of startups will be certified as approved financial agents after meeting the conditions specified in the specifications.

The startups will also be responsible for supporting economic operators in the procurement process with Algeria Post, until various means of electronic payment are obtained.

The minister also said that the startups can use payment services such as the QR Code, as well as the installation and maintenance of equipment.

This approach is part of the realization of the commitments of the President of the Republic, who attaches great importance to young entrepreneurs to revive the national economy.

A Country Greatly Supporting Startups In Recent Times

In December 2020, Algerie Telecom, Algeria’s state-owned telecom operator, unveiled new specifications for its calls for tenders. The new specifications would facilitate access of over 2,300 technological microenterprises to public procurement.

Labelled startups and incubators in Algeria would also be the greatest beneficiaries of the country’s newly passed finance law. The 2021 Finance Bill which was submitted to the country’s Council of Ministers on Sunday 04 October 2020, provides for changes in taxes (Tax On Professional Activities, TAP; and Value-added Tax VAT). Under the law, companies in Algeria with a startup label will be exempt from several taxes, starting with the TAP (tax on professional activity) and the IBS (tax on corporate profits. companies) for a period of 2 years from the date of obtaining the said label.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Promoters of ailing businesses founded by young people in Algeria will now benefit from the refinancing of their companies, says the Algerian ministry in charge of micro-enterprises, referring to a presidential decree published in number 1 of the Official Journal (JO). In a press release, the ministry specified that the new scheme is covered in decree N 20–441 of December 30, 2020 which amended and supplemented presidential decree N96–234 of July 2, 1996, relating to support youth employment.

startup

Under the terms of the said decree, “young promoters can now benefit from the refinancing of their companies in difficulty”.

To qaulify to benefit, the amount of the investment may not exceed ten (10) million Algerian dinars ($75k). The investment threshold is also cumulative according to the number of young promoters, especially when the project is carried out in the form of a consortium. This is with a view to promoting synergy between micro-enterprises.

According to the decree, “the investments must have been made by young promoters either individually, collectively or in the form of a group, in accordance with the laws and regulations in force.”

Under article 09 of the same decree, “young developers can equally benefit from the use of premises in specialized micro-zones set up as rental, for the production of goods and services”.

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Ethio Telecom, Ethiopia’s only telecommunication company’s rollercoaster ride in the country is far from over. Apart from recently being granted a mobile money license, the country’s Council of Ministers has amended the law establishing the telecom company to enable it to render financial services in Ethiopia. A statement from the Council of Minister on January 8 hinted that the amendment would enable Ethio Telecom to catch up with the industry’s fast development and to provide additional or related services by using its infrastructure.

Ethio Telecom

Before now, the existing regulation that was amended only allowed Ethio Telecom to provide and make accessible next generation network-based, world-class information technology services; to engage, in accordance with development policies and priorities of the government, in the construction, operation, maintenance and expansion of telecommunications networks and services; and to provide domestic and international voice, data, video, and other related value-added services.

What Would The New Amendment Mean For The Proposed Sale Of 40% Stake In Ethio Telecom To Foreigners?

The new amendment is already throwing up controversies. Plans have been on since October 2019 to allow private companies (mostly foreign companies: two out of either Etisalat, Axian, MTN, Orange, Saudi Telecom Company, Telkom SA, Liquid Telecom, Snail Mobile, and Global Partnership for Ethiopia, a consortium of telecom operatorscomprising Vodafone, Vodacom, and Safaricom) to take up to 40% stake in Ethio Telecom. But then banking, insurance, brokerage services, legal consultancy and other financial services still remain off limits for foreign investors, according to a new set of investment rules published on the Ethiopian Investment Commission’s website.

“Since the enterprise’s 40 percent share would be owned by foreign investors indirectly it will allow foreign companies or individuals to be involved in the financial sector, which is exclusively reserved for Ethiopians and Ethiopian Diasporas,” argued a source cited by Capital, a local media outlet.

However, another source explained that the amendment would not have any effect and that the privatization process would be undertaken as per the given schedule.

“The cabinet decision is only amending the regulation that the telecom operators demand to expand its business on other sectors,” an expert who is familiar with the case explained.

“Due to that, it will not be related with the privatization process. It will be clear when the privatization process and negotiation are finalized in the future. So far, Ethio Telecom is a public enterprise and you may not reject its demand to expand its operation and revenue,” the expert added.

In October 2020, after series of negotiations and deliberations, the National Bank of Ethiopia (NBE) finally granted a license to the company to start mobile money service in the east African country.

In April 2020, the National Bank of Ethiopia issued a regulation called Licensing & Authorization of Payment Instrument Issuers. For the first time in Ethiopia’s history, the regulatory regime will allow mobile money transactions. However, there is a caveat: any company interested in the new financial service regime must set up a trust account with a deposit money bank in Ethiopia.

“As part of the application process,” the directive read, in parts, “the National Bank, may request for a preliminary meeting and demonstration of the intended payment instrument to be issued, its related services, products as well as operation. Based on requests made and written approval of the National Bank, a payment instrument issuer may be allowed to provide cash-in and cash-out; local money transfers including domestic remittances, load to card or bank account, transfer to card or bank account; domestic payments including purchase from physical merchants, bill payments; over-the-counter transactions; and inward international remittances services.”

The regulation has also opened up the country’s financial services sector to include that a licensed payment instrument issuer may, with the relevant agreement with regulated financial institutions and pension funds, be allowed to provide micro-saving products; micro-credit products; micro-insurance products; or pension products in the country.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Financial technology companies in Nigeria that do not have the financial capacity to go for any of the license categories recently introduced by the Central Bank of Nigeria can now heave some sighs of relief. This is because the central bank has finally released a framework for regulating sandbox operations in the country. Unlike other fintech categories, such as agency banking or mobile money that require thousands of dollars in application fees to obtain licenses, no such fees are required for the grant of the regulatory sandbox license.

CBN Governor Godwin Emefiele

“The Sandbox encourages innovation that can improve the design and delivery of payment services and is therefore, also suitable for proposed products, services or solutions that are either not contemplated under the prevailing laws and regulations, or do not precisely align with existing regulation,” the new framework states.

“Innovative products or services previously rejected shall be considered for sandbox trials on a case by case basis. However, products and services that are outrightly unlawful under the laws of the Federal Republic of Nigeria shall not qualify for sandbox trials,” it adds.

Who Do The Rules Apply To?

Two categories of innovations are considered under the licensing regime.

First are innovative payments product or service produced by companies (fintech) already licensed by the central bank as well as other local companies (technology or telecom). The license given under this group will enable them to test a new product or service outside the purview of the existing financial regulations already put in place by the CBN.

Secondly, the rules will apply to companies proposing non-regulated financial products and services using emerging technologies, that is, innovators whose proposed solutions involve technologies which are currently not covered under any existing CBN regulations. This is where startups that have not been previously regulated by the Central Bank of Nigeria fall under.

Applications will be accepted on a yearly basis and the participating startups will be grouped into cohorts. Fintech solutions granted the license can choose, in any case, the duration of their operations in the sandbox, subject, of course, to the approval of the Central Bank of Nigeria. CBN has, to this effect, given a hint that the Regulatory Sandbox license can last for as long as 5 years. In any case, the testing period is subject to extension upon application by the fintech company. However, it should be noted that a regulatory sandbox license is not a permanent ticket to escape CBN’s regulatory eyes as upon completion and on exiting the sandbox, the successful entity is expected to meet relevant legal and regulatory requirements to still remain in business.

What Do The Rules State On Qualification For The License?

The rules state that to be considered qualified to obtain the license, the product or service of innovation must be so innovative as to improve accessibility, customer choices, efficiency, security and quality in the provision of financial services; or enhance the efficiency and effectiveness of Nigerian Financial Institutions management of risks; or address gaps in or open up new opportunities for financial benefits or investments in the Nigerian economy. It should be noted that this requirement is entirely subjective and will thus, depend on the whims and caprices of Nigeria’s central bank.

Once the above conditions have been established, the fintech solution must then proceed to show:

A business plan which will disclose that the product, service or solution can be successfully deployed after exit from the sandbox.

An assessment report to show the usefulness and functionality of the product, service or solution and the associated risks which should be devoid of adverse effect to existing structures and consumer experience.

Evidence (bank statement, etc.) that the fintech solution has resources and expertise to mitigate and control potential risks and losses arising from offering of the product, service or solution;

A statement that the fintech solution will provide the proposed project within a limited transaction (value and volume) for better risk management and mitigation. The limits shall not be exceeded during the testing period.

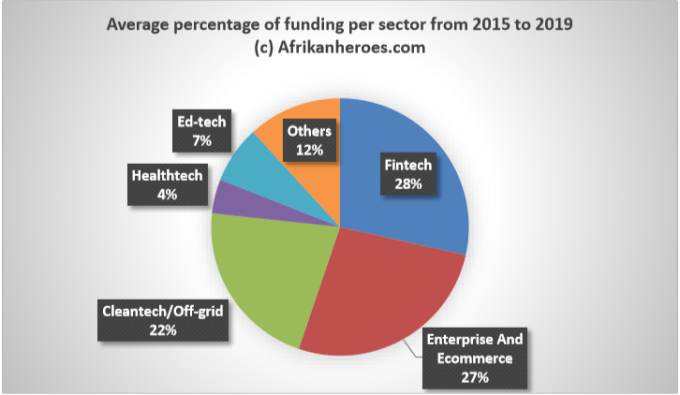

Sectorial VC funding, Africa. Data adapted from Partech

In Summary, What Can A Holder Of A Regulatory Sandbox License Do And Not Do?

In summary, the sandbox regime will enable fintech startups to mostly “test” their products, and no more. Basically, the testing will include doing a range of activities done by established fintech companies, including dealing with customers, transacting with customers or even holding customers’ cash. However, since the license covers only testing, the extent to which the fintech startup may go with customer acquisition, transaction or holding of cash may be severely limited. Fintech startups relying on the sandbox license will also have to vigorously report on their operations, as failure to do so may lead to their disqualification from participating in the sandbox regime.

How To Apply For The License

Applications to the sandbox process would involve an invitation placed on the CBN website, and local newspaper advertisement. The details of the advert would include the minimum eligibility criteria to shortlist applicants who qualify to be absorbed into the sandbox. Receipt of application shall be acknowledged to applicants within 5 working days after submission.

Firms wishing to enter into the CBN’s Regulatory Sandbox shall apply to the CBN through the Regulatory Sandbox online application platform accessed via the CBN’s official email address — Sandbox@cbn.gov.ng .The application must be submitted with a cover letter signed by an authorised signatory of the entity and addressed to the Director, Payments System Management Department, Central Bank of Nigeria, Abuja.

The Bank will inform an applicant of its eligibility and approval to participate in the sandbox, 45 working days after the closure of the application window. A Letter of Approval (LoA) would be issued to the Innovator which would allow Sandbox participants to test their innovation upon entry into the sandbox.

Click here to find out more, including documents to submit and other procedures.

Type of License

Example Of A Fintech Company In Nigeria With This Type Of License

What Can Your Fintech Startup Do With This License?

What Is The Minimum Amount Required To Obtain The License?

Payment Solutions Services (PSSs)

Activities related to Super-agents, payments terminal service providers, payment solutions service providers

N250 Million ($658K)

Super-agent

Innovectives; Flutterwave.

Recruit and manage agent networks, among other activities provided for in the Regulatory Framework for Licensing Super Agents in Nigeria

N50 million ($132K)

Payment Terminal Service Provider (PTSP)

4ITEX Intergrated Systems

Deploys POS terminals; Own POS terminals; train merchants and agents

N100 million ($264K)

Payment Solutions Service Provider (PSSP)

Paystack; Flutterwave

Offers gateway or portals for processing payments; Offers general payment solutions or develop payment applications software; or offers merchant services, aggregation or collection of payments

N100 million ($264K)

Mobile Money Operation

MTN MoMo; 9PSP

Issues e-money; create and manage wallet, as well as manage pool accounts.

The Regulatory Sandbox Category is aimed at encouraging innovation and deepening financial inclusion. The CBN says it will review the products and solutions of applicants once the implementation of the Sandbox regime begins.

Not applicable

New license categories introduced by the CBN in December, 2020 1 Dollar=₦380(official), December 11, 2020.

What Are The Implications Of Acquiring The Regulatory Sandbox License?

On the surface, it looks like a regulatory sandbox license is the cheapest of all the licenses rolled out by the CBN, but it is not. The only cheap thing about it is that it has no official licensing application fees. Holders of this license would still have to heavily spend on meeting application requirements as well as on reporting and on meeting CBN’s other requirements while the testing lasts.

A regulatory sandbox license is not a permanent license like other CBN licenses which can only be revoked once compliance is not made on extant laws. A holder of a Regulatory Sandbox license would still have to apply and obtain other CBN licenses (if then applicable) upon the expiration of the sandbox license.

A regulatory sandbox license appears to be the final bait from the country’s central bank on fintech startups that are still dodging its regulatory fangs. Hence, with a Regulatory Sandbox license, the stage may be set for the full-flung regulation of Nigeria’s financial ecosystem by the CBN. Therefore, it is safe to say that the era of “unregulated fintechs” may be over in Nigeria.

In essence, for technology companies building financial products or services not yet regulated by the CBN, this is the right path to toe towards appending some legitimacy or legality to their operations.

Finally, this is probably the only rules from the CBN currently in place in Nigeria which has tried to encourage technology-enabled innovations within the financial services industry.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Apart from passing a set of data protection rules last year, Kenya is, again, set to confront the activities of data collectors under its jurisdiction. According to the office of data protection commissioner Kenya, in a draft guidance note published on Tuesday, entities must issue consent forms to individuals before embarking on collection of personal data.

President Uhuru Kenyatta

“Under no circumstances should the data collected be sold to third parties or transferred out of the country, unless the concerned individual consents to the transfer. The transfer of personal data to another country shall only take place where sufficient proof has been given on the appropriate safeguards with respect to the security and protection of the personal data,” the draft guidance policy reads.

Here Is What You Need To Know

Under the proposed new rules, mobile applications requesting access to personal data shall publish policies on the information being collected.

Again, any person who requests for personal data will be required to enter into a data protection and sharing agreement with the entity or person having the control of data.

Under the proposed rules, public entities are also expected to channel all personal data requests to their respective ministries and state agencies.

Furthermore, the commissioner will require entities to endeavor to collect personal data in an anonymized format ensuring that individuals cannot be re-identified.

The new policy is coming on the heels of the Data Protection Act passed at the end of 2019. The Act is Kenya’s first piece of legislation on personal data.

The draft guidance note is geared at responding to the increased need for personal data under the COVID-19 pandemic.

“For instance, health data and geo-location may be necessary for contact tracing. Innovations built in response to pandemic including apps and related services, may request some access to personal data from a government or private entities to enable the development of a product,” added the note.

What Are The Implications Of This For Startups In Kenya?

For consumers or data subjects in Kenya, this is a welcome development in an era of intense data mining. For startups, there is now an official regulatory hurdle to leap over, although application play stores such as Google Play Store and App Store already require such consent to be obtained from the data owners before the data are collected. However, the new rule will, notably, change what happens to the data after they have been collected. For instance, once the rules are effective, it will no longer be enough to obtain consent at the point of the initial collection, neither would it be enough to just insert in the privacy policy or terms of use of the app a clause that data collected may be shared with third parties. It is now going to be mandatory, especially for data auditing purposes, that the sharing entity seek the data subject’s consent as well as execute a data share agreement with the third party seeking to collect data. This is coming in the wakes of several data scandal and compromises, including the recent incident of Facebook — Cambridge Analytica.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Authorities in Uganda have blocked all access to social media. The move comes at the very end of a tense campaign for presidential and legislative elections to be held this Thursday, January 14.

The decision fell like a chopper on Tuesday, when a coalition of NGOs had just asked the Ugandan authorities not to touch internet access before and during the elections.

According to a letter viewed by AFP and Reuters, the director of the Uganda Communications Commission, Irene Sewankambo, ordered operators to “immediately suspend all access” to all social networks and messaging services until further notice.

director of the Uganda Communications Commission, Irene Sewankambo

This Tuesday, in the middle of the afternoon, the network monitoring organization Netblocks confirmed the blocking.

“Real-time measurements show that Twitter, Facebook, WhatsApp, Instagram, Snapchat, Skype, Viber, Google Play Store, some Telegram servers and some link shortening services are among a long list of social media prescreened and not available through major Ugandan cellular network operators,” the network noted.

NGO open letter

The day before, in an open letter, 54 member organizations of the #KeepItOn coalition had asked President Museveni, candidate for a sixth term, as well as telecom operators, to guarantee that “the internet, including social media and other digital communication platforms, remains open, accessible and secure throughout Uganda for the duration of the [President-elect] elections and investiture.”

The Ugandan authorities have in fact been repeatedly pinned down by defenders of digital freedoms for attacks on free expression on the internet. During the previous general elections in February 2016, the country experienced a similar cutoff, justified by “security reasons”. More recently, last September, the Ugandan telecoms regulator imposed an official authorization before posting content online.

In a televised address this Tuesday evening, President Museveni confirmed the blocking measure, explaining that it had been taken in retaliation for the closure, the day before by Facebook, of several accounts belonging to government officials or supporters. .

“I am sorry for the inconvenience for those who use these channels […], but we cannot tolerate the arrogance of those who come to tell us who is good and who is bad,” said the head of the ‘State. These social networks, if they are to operate in Uganda, must be able to be used fairly by anyone. If they want to take sides, these groups will not be able to operate [in the country]. “

Twitter for its part denounced the decision of the Ugandan power, recalling that “access to information and freedom of expression is never more important than during democratic processes, in particular elections”.

Ahead of the Ugandan election, we're hearing reports that Internet service providers are being ordered to block social media and messaging apps.

We strongly condemn internet shutdowns – they are hugely harmful, violate basic human rights and the principles of the #OpenInternet.

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Any time soon, matatus will no longer be allowed to collect physical cash in Kenya. The country’s National Safety and Transport Authority (NTSA) has awarded licenses to leading telecom company, Safaricom and 28 others to offer cashless payment services in public service vehicles (PSVs) in Kenya, paving the way for a ban on the use of cash in public transport.

matatus

Once the system is in place, all passengers will need to pay their fares through mobile money platforms, giving the government access to their identity and personal contact information needed to fight the Covid-19 pandemic.

In a statement, NTSA said the 29 licensed companies will offer a platform for the digital payment of transportation costs.

The latest development is in response to a June 16, 2020 call for tenders in which the NTSA solicited tech companies to install mobile software and web applications for nearly 200,000 matatus (minibuses) in the country.

The digital transport fee collection system will also have the technical capacity to trace the journey of passengers as part of the fight against the coronavirus disease.

The NTSA has yet to announce full details of the new digital fare payments system or a timescale for its rollout.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer