Digital lending startups in Kenya are not heaving any sighs of relief any time soon. In its latest move, the Central Bank of Kenya has insisted that the proposed regulations to regulate digital lending are not only necessary but need to be approved faster than scheduled.

central bank Governor Patrick Njoroge

“We would like a focus bill on unregulated digital credit providers that will avoid conflict with already regulated digital financial services providers,” said Njoroge to parliament during the defence of the regulations.

Here Is What You Need To Know

The Central Bank of Kenya (Amendment) Bill, 2020, although purports to curb the steep digital lending rates that have plunged many borrowers into a debt trap as well as predatory lending, also extends its tentacles, by its operation, to all financial technology services in Kenya.

“At least shylocks hide. These platforms shout about themselves openly while impoverishing Kenyans,” Njoroge told a Parliamentary Committee meeting in August last year.

The Implications Of The Proposed Law On Digital Financial Services Startups In Kenya

Implied Lifting Of The Ban On Credit Lending Startups

Once the new law is passed into law, its first implication would be to terminate the ban on credit lending startups in Kenya as regards submitting credit information on their borrowers to Credit Reference Bureaus (CRBs). Thus, with a renewed power to report customers for blacklisting to the country’s central credit information sharing center, it is only safe to say that the risks associated with their business model have become, once again, more manageable.

Licensing of Digital Financial Services Companies/Startups

Another direct implication of the proposed new law on digital financial services startups in Kenya is that the Central Bank of Kenya will now possess recognized power under the law to issue operational licenses to startups desiring to provide services related to a digital financial product, financial product advice, market, administrative or management services or credit under a regulated credit contract in Kenya.

What this means is that startups that offer digital banking services will now also have to maintain a minimum authorized capital of five billion shillings ($46.4 million), which may be increased by such amount as shall be determined by CBK, unless the contrary is stated by the CBK.

In other words, all the rules regulating commercial banks and other financial institutions will now have to apply to startups offering digital financial services if the bill becomes law.

The Bill is coming amid complaints that digital lenders do not provide full information to borrowers on pricing, punishment for defaults and recovery of unpaid loans.

Digital lenders have also been accused of abusing personal information collected from defaulters’ mobile phone contacts list to bombard relatives and friends with messages regarding the default and asking third parties to enforce repayment.

FinTech covers all areas of human interaction with commodity-money circulation and uses a large class of IT technologies. Source: — Aspilos.com

Regulation of Interest Rates Charged Users Of Digital Lending Services

Even though digital lenders in Kenya may still be allowed to lend, the law would however, if passed into law, see that they do not charge interests on their loans excessively. This is because the CBK could now determine the maximum rate of interest they charge their customers.

The latest move to control the activities of digital lenders follows the removal of legal cap on commercial lending rates by the Central Bank of Kenya in March 2020. The cap, established far back in 2016, which set interest rates chargeable by banks at 4%, was intended to address the issue of the affordability of credit for small enterprises and working people, as they had complained for years that high interest rates had locked them out of accessing credit.

Its removal in March this year has, however, resulted in the proliferation of digital lenders, who seek to take advantage of the business opportunities it offered. For instance, Tala, Branch, which are among top players in the mobile digital lending market in the country, offer interest rates of 152.4 percent and 132 percent per year respectively.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

As African countries grapple with rebooting their economies post-Covid-19, analysts have called on governments to make small and medium scale enterprises the engines of their economic reinvigoration effects to serve as complementary to the African Continental Free Trade Agreement (AfCTA) which comes on board in January. This they say is because the AfCFTA will not in one dramatic swoop alter existing commercial and economic realities on a vast scale, but its implementation could lead the recovery efforts from the COVID-19 crisis.

This was the submission of industry experts from across the continent who met within the week for a virtual discussion focused on resetting, retooling and restarting regional integration in Africa in the wake of the COVID-19 pandemic, underscored the importance of putting small scale traders at the heart of any initiatives. The joint webinar, organized by the African Development Bank and Korea Customs Service (KCS), looked at service sectors, e-commerce, digital platforms and value chain development as critical factors for accelerating trade and investment in Africa against the backdrop of the global pandemic. The webinar was delivered in three sessions, moderated by Stephen Karangizi, Director, African Legal Support Facility; Dr. Stephen Karingi, Director at Regional Integration and Trade Division of UNECA and Acha Leke, Senior Partner at McKinsey.

History has demonstrated the success of countries and businesses that seize new opportunities during times of crisis, said Sukhwan Roh, Commissioner of the Korea Customs Service. “The COVID-19 pandemic has completely changed health and livelihoods of individuals across the world in less than a year,” he said. “Korea wishes to share all the achievements in system enhancement utilizing new technologies with African countries.”

The workshop’s audience heard how regional integration is increasingly central to the continent’s future economic prospects and to attracting foreign direct investment. The African Continental Free Trade Agreement, (AfCFTA), already ratified by 30 countries, is expected to come into effect on 1 January, 2021. Uniting all 55 member states of the African Union, the pact will create a market of more than 1.2 billion people, including a growing middle class, and a combined gross domestic product (GDP) of over $3.4 trillion.

COVID-19 has deepened pre-existing trade frictions within the continent yet offers important growth opportunities and great stories of innovation and highlights the importance of protecting Africa’s place in local value chains, said Anabel Gonzalez, Senior Fellow, Peterson Institute for International Economics, with the need to “put small scale traders at the heart of the effort.” She urged governments to strengthen national agencies to provide support to small traders.

“AfCFTA creates a new trade and integration reality…integrating unequal partners across the continent,” said Trudi Hartzenberg Executive Director of the Trade Law Center (TRALAC). Trade facilitation enjoys specific focus within the AfCFTA, with digital, e-payments, and e-commerce particularly important, she added, citing a 2020 WTO report that emphasized education and healthcare as fundamental to industrialization.

From the outset, the African Development Bank has lent strong support to the AfCFTA, financing the set-up of its secretariat as well as supporting member countries with technical assistance to comply with a range of AfCFTA regulations, said Bank Vice President, Infrastructure, Private Sector & Industrialization, Solomon Quaynor in his introductory remarks read by Abdu Mukhtar, Bank Director, Industrial and Trade Development Department.

Still, Quaynor warned, post-crisis recovery efforts are likely to be slow. “The AfCFTA will not in one dramatic swoop alter existing commercial and economic realities on a vast scale. However, through strategic measures and the right investments, policy frameworks and political backing, intra-African trade will be enhanced. “

Presentations provided examples from Ghana and Zambia of strategies the private sector can adopt to leverage the AfCFTA within the context of the pandemic. Ghana previously imported most of its Personal Protective Equipment or PPE, but, since the pandemic, the government galvanized 14 local garment firms to manufacture PPE. These firms now produce 1,000 items daily, according to Ghana’s deputy trade minister, Robert Ahomka Lindsay. The development has created 10,000 jobs. “Traditional value chains have been challenged… it made us realise that we cannot rely on those value chains,” Lindsay said.

Some of the worst-affected sectors in Africa such as tourism, aviation and education, had shown resilience, for example, in the food industry, which harnessed e-commerce for marketing during the pandemic, noted Kenneth Baghamunda, Dir. General, Customs and Trade, East African Community Secretariat. Zambia’s success with cashless payment solutions at its border and other innovations since COVID-19 was another example of favourable results.

“We need to see which value chains need to be developed and we need to interconnect our policies with the right institutional framework,” he said.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Looking to scale your video-on-demand startup in South Africa? You must be prepared to comply with a proposed new rule which requires all streaming services in South Africa to stream 30% South African content on their platforms. In a proposal contained in the Department of Communications and Digital Technologies’s white paper on Audio and Audio-visual Content Services policy framework, DCDT wants streaming services in South Africa to ensure that 30% of their broadcast content is South African.

chief director of broadcasting policy Collin Mashile

“Where video-on-demand subscription services come and operate in South Africa, everything that they show to South Africans in terms of their catalogue — 30% of that catalogue must be South African content,” said the department’s chief director of broadcasting policy Collin Mashile during a presentation of the white paper framework to parliament on Wednesday (25 November).

“What this means is that we are trying to create opportunities for the production and creative industry sector.”

Broadcasting Services Will Now Include Streaming Services

Under the proposed new rules, “broadcasting services” would now include streaming services, regardless of the device on which they are viewed. The direct implication of this is that the services would now require the payment of a license fee to be viewed in South Africa.

“We were asked where we got the idea that South Africans are interested in this 30%,” Mashile said. “The most popular shows in every country remain the local shows.”

The White Paper proposes, among other things, to change the limitations on foreign control of commercial broadcasting ownership in South Africa. The current legislative framework prohibits a foreign firm from exercising control over a commercial broadcasting licensee by limiting financial interest, interest in voting share or paid-up capital to a maximum of 20%. Similarly, not more than 20% of the directors of a commercial broadcasting licence may be foreigners. The White Paper recognises that the regulatory environment for foreign direct investment is one of the key factors that is likely to influence the location decisions of foreign investors.

As a result and in an attempt to stimulate growth and development of the ICT sector, the White Paper proposes retaining the limitations in respect of foreign ownership of linear individual audiovisual content services (broadcasting services) but subject to them increasing to a maximum of 49% to stimulate investment. In the case of foreign firms from African Union (“AU”) member countries, the maximum of 49% should be capable of being waived so long as there is a reciprocal agreement between South Africa and the relevant AU country.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

The General Confederation of Moroccan Enterprises has announced an easing of the conditions for obtaining the Mauritanian multi-entry business visa, reserved for its member companies. The measure is part of a strengthening of business relations between the two countries.

The multi-entry business visa is obtained by submitting an application file signed by the General Confederation of Enterprises of Morocco (CGEM), with the Mauritanian embassy in Rabat. Valid for 2 years, this special visa was announced by the CGEM on November 23, and aims to ensure an economic framework favorable to business development.

Mauritania Morocco Entrepreneurs visa Mauritania Morocco Entrepreneurs visa

The CGEM, which represents private sector companies in Morocco, has around 90,000 members whom it represents and promotes. Through the support and promotion of private initiative, the CGEM aims to improve the business and investment environment, locally and internationally.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Nigeria’s laws for companies will entirely change from 2021, following the Gazette-ing of the Companies and Allied Matters Act, 2020, which was signed into law on 7th August, 2020 by President Muhammadu Buhari, more than 30 years after the old one. The announcement was made by the country’s Corporate Affairs Commission (CAC) in charge of managing the affairs of companies in Nigeria via its Twitter handle.

President Muhamdu Buhari

The Corporate Affairs Commission has officially taken delivery of a copy of the Gazetted CAMA, 2020 from the Clerk of the National Assembly on Thursday 19th November,2020 and is putting machinery in place to commence full implementation by 1st January,2021.

Here Is What Your Startup Needs To Know About The New Law

One Person Can Now Form A Company In Nigeria

Under the new law, although public companies are still required to have at least two members, a person can now form a private company. However, even though this is encouraged, the long-term prospects of the startup company should be considered, given that most startups are built for exit through IPOs or acquisitions etc., which makes a one-shareholder structure highly unsuitable for them in practice.

A Private Company May Now Transfer Its Shares

Unlike the old law where share transfer in a private company was restricted, this is not the case with with new law which gives all private companies in Nigeria the option to choose whether or not to transfer its shares in their articles of association. The implication of this is that in private companies, a structure in which most startups exist, shares can now be bought or sold at will. However, the company must obtain the consent of all its members before it sells more than 50% of the assets of the company. A shareholder in a private company is not also permitted to sell more than 50% of his shares to a non-shareholder unless he first offers to existing shareholders the shares meant for sale. He may then proceed to sell to a non-shareholder if the existing shareholders refuse. In the same way, that non-member willing to purchase the shares offered to him must also be ready to buy other shareholders’ interests in the shares offered.

Under the new law, every public or private company still needs to have a secretary. The requirement of a company secretary is only exempted for private companies which are small companies.

Annual General Meetings No Longer Compulsory For Small Companies Or Single Shareholder Companies

By virtue of the provisions of the law, small companies will no longer be mandatorily required to hold Annual General Meetings.

Under the law, a company qualifies as a small company in a year if for that year the following conditions are satisfied —

It is a private company;

The amount of its turnover for that year is not more than ₦120 million or such amount as may be fixed by the Commission;

Its net assets value is not more than ₦60 million or such amount as may be fixed by the Commission;

None of its members is an alien (a foreigner)

None of its members is a Government or a Government corporation or agency or its nominee; and

The directors hold between themselves at least 51 per cent of its equity share capital.

Small Companies Exempted from Audit Requirement

Under the new law, a company (excluding banks and insurance companies) is exempt from the requirements relating to the audit of accounts in respect of a financial year if-

(a) it has not carried on any business since its incorporation ; or

(b) its turnover in that year is not more than ₦120 million and the balance sheet total is not more than ₦60 million. In other words, the company is a smalll company.

One Person Can Now Be A Director In A Small Company

The new law also made provisions concerning directors of a company. According to it, the minimum number of directors for every company (whether public or private) shall be two directors. However, in the case of a private company which is a small company, the minimum number of a director shall be one, unless otherwise provided by the company’s articles or any applicable industry specific legislation.

Other notable provisions include that a director of a public company shall not hold position of both the CEO and the Chairman at the same time. Again, a person cannot be a director in more than 5 public companies at a time.

For the first ever, the new company law is properly defining who an independent director is. Consequently, there must be 3 independent directors in every public company, who must not be employees in the company and who have not made or received any payment in excess of N20m from the company. They must also not own more than 30% direct or indirect equity in another company transacting with (transaction sum should not be more than N20m) the company. They should also not own more than 30% direct or indirect equity in the company.

Nigeria company law Nigeria company law Nigeria company law Nigeria company law Nigeria company law

The new law is also revolutionary in that it gives wider options to places where the meetings of a company may be held. Accordingly, it states that although all statutory and general meetings of companies may be held in Nigeria, small companies or companies with a single shareholder may hold its meetings anywhere in the world. Again, a private company (and not public companies) may hold all its meetings on the internet provided that it has created room for that in its articles of association.

Electronic Communications And Ease of Doing Business

The new law now make it possible for business to be run more easily. For instance, every member can now have a right to attend any general meeting of of a private company (either physically or electronically) and to speak and vote on any resolution (physically or through electronic means) before the meeting. The certified true copies of all such electronically filed documents are now admissible in evidence.

Struggling Companies In Distress Can Now Be Rescued From Total Collapse

Under the new law, the directors of the company may voluntarily arrange with those the company is owing for a way of satisfying all outstanding debts owed by the company.

No More Common Seal For Companies

The law has also put an end to the requirement for each company to have a common seal. In its place, it states that should any document be required by any law or otherwise to be under the common seal of the company, it is enough if the documents were signed by a director and a secretary; or by at least two directors of the company; or by a director in the presence of a witness who shall attest the signature.

Better Legal Framework For A VC Fund

Under Nigeria’s newly passed Companies and Allied Matters Act (‘The CAM Act’), it has also become easier to set up a legal structure for a VC fund. By the terms of the new law, venture capital firms in Nigeria may now be set up as limited liability partnership or limited partnership.

Previously, before the law came into being, it was normal practice to register VC firms as limited liability companies; general or limited partnerships, or as limited liability partnerships under the Partnership Law of Lagos State (Nigeria’s major economic city).

Even though under the old regime, general and limited partnerships could be registered and applied throughout Nigeria whereas limited liability partnerships only applied in Lagos, the new regime spells out definite governance framework for partnerships generally, as well as enlarges the operational scope of partnerships to cover the whole of Nigeria, and not just Lagos alone.

The essential difference between a limited liability partnership and a limited partnership under the new law is that while a limited liability partnership is a corporate body which has a legal personality different from the partnership as well as a perpetual succession, a limited partnership has no separate identity from those of the partners that make it up.

Indeed, a limited partnership under the new law captures the ideal form of most VC funds, which usually have one or more partners called general partners — responsible for the management of the funds under the partnership, and who are also liable for the debts and obligations of the partnership — as well as one or more persons known as limited partners — who contribute certain sums of money or property to the partnership and who shall not be liable to the debts and obligations of the partnership.

Apart from properly providing a clear legal framework for the operation of VC funds in Nigeria, the new partnership regime, under the CAM Act, also functions to provide some clarity about their taxation. To read more on this, click here.

Bottom Line:

Remarkable, especially with the introduction of new provisions that have taken care of the difficulties necessitated by the coronavirus pandemic. However, apart from these, in practice, the law remains substantially the same with the old version. While certain provisions may look attractive given their cost-saving implications, there are several provisions which are unsuitable for companies with long-term vision.

For more on the new law and how it may affect your startup company, click here. (PDF)

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Cryptocurrencies are still not recognised as legal in South Africa, but dealing in or advising on them has now been declared a financial service requiring a license in the country. In a landmark move, the Financial Sector Conduct Authority (FSCA), the authority in South Africa in charge of regulating the market conduct of financial institutions that provide financial products and financial services, has issued a draft declaration classifying crypto assets as a financial product under the Financial Advisory and Intermediary Services (FAIS) Act. This is coming after similar moves by Mauritius and Nigeria.

Crypto Currency

“This Declaration is called the Declaration of crypto assets as a financial product, 2021,” the Declaration reads.

“This Declaration comes into effect on the date of [its] publication…on the website of the Authority,” it adds.

“Any person who, immediately before [the]…date of this Declaration…renders financial services in relation to crypto assets — (a) must submit an application for authorisation as a financial services provider…within 4 months of ….this Declaration; and

(b) [Such person] may continue rendering financial services in relation to crypto assets UNTIL— (i) the period to submit an application…has expired,” it further reads.

What Does This Declaration Mean In Summary?

Declaring crypto assets as a financial service means that any person that provides advice and/or intermediary services in relation to crypto assets must be licensed under the FAIS Act in South Africa. It also means that such person must comply with all of the requirements under the FAIS Act, the requirements of the General Code of Conduct for Authorised Financial Services Providers and Representatives, 2003 (General Code), the Determination of Fit and Proper Requirements, 2017 (F&P Requirements), etc.

“The intention behind the Declaration is to immediately capture intermediaries that advise on or sell crypto assets to consumers so as to provide adequate protection for consumers that are advised to purchase these products,” the FSCA states in an explanatory memo to the Declaration. “These protections should at least result in improved disclosures to customers that more effectively highlight the risks involved in investing in crypto assets and should ensure that a more robust advice process is adopted (including proper risk assessments) when intermediaries decide to advise customers to purchase crypto assets. Licensing of intermediaries is also necessary to improve the quality of data for policymakers and regulators about the crypto asset environment, and to consider whether there is a need for further regulatory interventions.”

Does This Mean That Cryptos Are Now Legally Recognized In South Africa?

The explanatory memorandum to the Declaration says no.

“The Declaration in no way legitimises or gives credence to crypto assets, but is merely attempting to regulate intermediaries that are selling and advising customers to invest in crypto assets,” the explanatory memo reads. “It is envisaged that this will either result in customers making more informed decisions when purchasing crypto assets or potentially in a decline in intermediaries attempting to advise on and/or sell crypto assets. It will also reduce instances of fraudulent activity where players purport to be selling investments in crypto assets but are in reality absconding with customer funds.”

How Would Affected Crypto Businesses Cope In The Meantime Before Obtaining The Required Licenses?

The FSCA states that acknowledges the impact that the draft declaration will have on businesses that are currently furnishing financial services in relation to crypto assets, and more specifically the fact that such business would not be able to operate legally unless they have obtained a FSP licence in terms of section 8 of the FAIS Act.

“For this reason, various “transitional arrangements” for businesses already operating in this space will be put in place before publication of the final declaration,” the FSCA states.

The transitional arrangements entail that such a business may continue its operations, but it must submit an application for authorisation as an FSP under section 8 of the FAIS Act within 4 months of the effective date of the final Declaration.

“The business will be allowed to continue its operations until its application for a licence has been granted or declined. If such business fails to submit an application within 4 months, it must cease its operations,” the authority further states.

According to the FSCA, any new business that wants to start furnishing financial services in relation to crypto assets after the effective date of the final Declaration will have to obtain an Financial Service Provider (FSP) licence before it can start furnishing such services.

Cryptocurrencies South Africa license Cryptocurrencies South Africa license

Is This The Final Declaration Of FSCA On This Or Is There Any More Thing?

No. This is an interim declaration. Hence, the FSCA invites the general public to comment on the draft regulations on or before 28 January 2021.

“Submissions on the draft Declaration must be made in writing on or before 28 January 2021 to the FSCA at FSCA.RFDStandards@fsca.co.za, using the submission template available on the FSCA’s website [at www.fsca.co.za],” the memo to the declaration states.

The Implication Of These For Crypto Startups And Traders In South Africa

Those who will be most affected by the new rules are established South Africa-based crypto platforms and exchanges offering crypto-related services in the country. However, there is still ambiguity around the rules as the declaration state that crypto assets are neither legitimised nor given credence to in the country. In any case, while the latest declaration may be a huge benefit to platforms that are able to append the badge of legitimacy from Financial Services Board of South Africa (FSB), now renamed to Financial Sector Conduct Authority (FSCA), nobody is really sure of how the government wants to wield its new cudgel.

“We’re not surprised by this, as we knew it was coming. We’re excited by it. A big hurdle for us is not being regulated by the FSCA, which has deterred many people from getting involved in this sector. I think regulations will help bring credibility to the crypto sector and help weed out those involved in crypto scams,” said Jon Ovadia, founder and CEO of crypto company Ovex. “At present there is no sure way of knowing who is legitimate and who is operating a scam, and the people are understandably confused by this, so we see this as a positive development.”

“VALR will always welcome prudent and appropriate regulation, particularly as it relates to consumer protection,” says VALR CEO Farzam Ehsani. “We have been working with the South African regulators for many years to inform a regulatory framework that does exactly this. It is important to note, though, that today’s draft declaration of crypto assets as a financial product under the Fais Act by the FSCA was not one of the 30 recommendations in the Position Paper on Crypto Assets that was published by the regulators in April this year.”

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

In Algeria, the national agency in charge of youth employment (ANSEJ) will soon be no more. In its place will be a national agency which would strictly cater to entrepreneurship unlike ANSEJ which was more or less a social initiative than entrepreneurial. The new agency will be called National Agency for Support and Promotion of Entrepreneurship (ANAPE).

Nassim Diafat, Minister Delegate to the Prime Minister of Algeria in charge of micro-enterprise

“We have moved away from the social approach of ANSEJ. Today we have a new economic approach which has prompted us to change the name of this organization to National Agency for Support and Promotion of Entrepreneurship (ANAPE),” Nassim Diafat, Minister Delegate to the Prime Minister of Algeria in charge of micro-enterprise said in an interview.

Algeria Ansej Algeria Ansej

Here Is What You Need To Know

The Minister Delegate to the Prime Minister in charge of micro-enterprises gave a presentation on the draft Presidential Decree amending and supplementing Presidential Decree 96–234 of 02/07/1996 on support for youth employment

The amendment introduced four new provisions, including that the government of Algeria will formally undertake to refinance micro-enterprises in difficulty; replace the formula for organizing micro-enterprises into “grouped firms” by a new formula of “grouping of micro-enterprises” as well as integrate the possibility of housing micro-enterprises in specialized micro-zones developed under rental for the production of goods and services.

These new provisions introduced will make it possible to remove the constraints encountered in the development of the support mechanism for the creation of activities by the Agency and the project leaders and thus guarantee the sustainability of investments, a decision that will alleviate the suffering of thousands of young ANSEJ promoters.

As a reminder, last August, the minister delegate in charge of micro-enterprises reassured the beneficiaries of the ANSEJ program who are unable to repay their debts.

“Young people who have benefited from financial loans from ANSEJ, and who are unable to repay their debts, will not be imprisoned,” said Diafat.

Algeria’s National Agency for Youth Employment Support ( Ansej ) is the country’s organization responsible for managing a credit fund for the creation of businesses. She participates in the public employment service .

Ansej is in charge of implementing a support system for business creation for people under 40 years of age. It manages a credit fund, granting loans at zero interest rate (0 rate loans), complementary to bank loans. Committees composed of representatives of banks and institutions grant the loans after examining the files of the promoters.

A bank guarantee fund supplements the financing instruments. Algeria ‘s Ansej advisors provide follow-up to promoters who have obtained a loan.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Internet and telephone users in Madagascar will heave some sighs of relief on their bills come 2020. The small island country, off the coast of East Africa and with a population of 26 million( only about 3 million of whom are connected to the internet) has lowered its excise tax on telecommunications. The tax, which was reduced from 8% to 10% in the 2020 finance law, to the great displeasure of telecom operators and consumers, is again showing at 8% in the 2021 finance bill.

Tax

madagascar internet tax madagascar internet tax

Here Is What You Need To Know

According to Ranesa Firiana Rakotonjanahary, the secretary general of the Ministry of Posts, Telecommunications and Digital Development (MPTDN), the drop is the result of a study conducted by the ministry. The study shows that by reducing the excise tax, its impact will be beneficial at all levels to consumers.

However, in order to avoid the same blemishes as in 2019, when the tax was still 8%, the MPTDN provided for strict control of Airtel, Blueline, Orange Madagascar and Telma. With this surveillance of operators, the Malagasy government wants to ensure that there will be a real drop in prices, and not only for users of social networks as has been the case in the past.

Ranesa Firiana Rakotonjanahary believes that the impact sought through this new tax cut should also largely benefit businesses that need Internet access for their activities.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Running a registered company in Zimbabwe? Your company has got 12 months from now to re-register or cease to exist. Whether it is a way government hopes to use to dust up old, forgotten money or not, all existing companies which were registered before February 22, 2020, are required to re-register with the Registrar of Companies within a period of 12 months under a new Companies and Other Business Act [Chapter 24:31].

Deputy finance minister, Clemence Chiduwa

“Yes, I can confirm that that the new Companies Act requires all companies to re-register, but I cannot comment on that because the registration of companies falls under the ministry of justice and their operations fall under the industry ministry. So those are the rightful ministries to comment on that matter,” Deputy finance minister, Clemence Chiduwa said in an interview.

Here Is What You Need To Know

According to the new Act which came into effect in the first quarter of 2020, companies have up to March 2021 to complete the new registration process or risk being struck off the Companies Register.

The re-registration exercise is reported to be an administrative process aimed at establishing a new and updated register of companies so that inactive companies do not appear on the updated companies register.

The new Act repeals the old Companies Act, which was crafted on April 1, 1952, and incorporated provisions of the Private Business Corporations (PBC), encouraging small to medium enterprises to register and be recognised as players in the market.

The new Act now, also empowers the Registrar of Companies to strike off defunct business entities from the register. It also stipulates that shelf or shell companies that do not file returns on the anniversary of their incorporation shall be removed from the register.

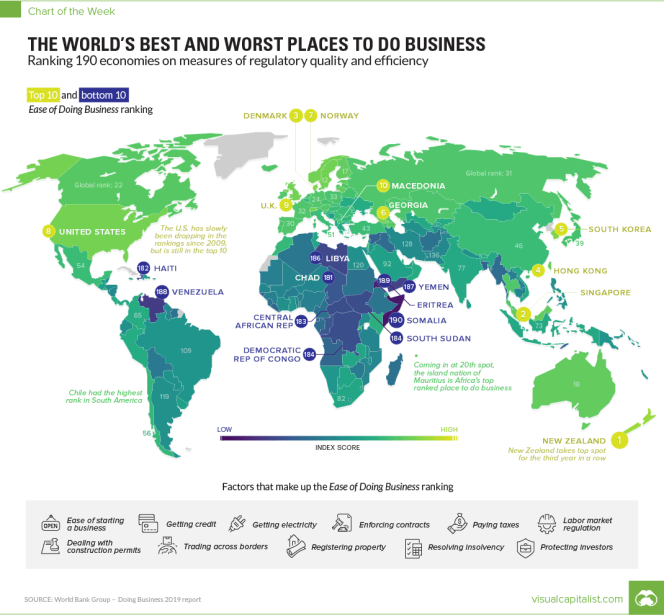

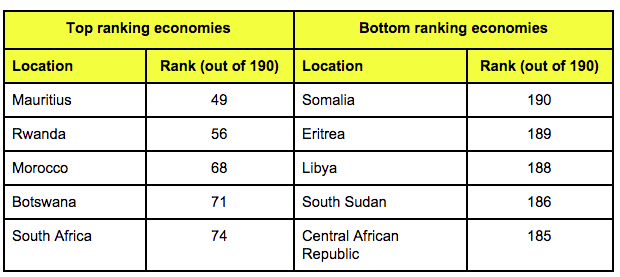

Top and bottom ranking African countries by ease of doing business. Credit: This is Africa/World Bank

“I have frequented this office for more than two months now trying to register my new company, but the chaos here is pathetic,” one businessman was quoted as saying. “To worsen the matter, I was told that they have run out of paper to print Certificates of Incorporation. That shows poor planning. How is it that they start a new thing without adequate resources?

“To be frank the Act requires commitment for it to become effective as it is already evident the implementing office is struggling with the new requirements just a few weeks since its inception,” he said.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Kenya appears to be getting set for the 2021 timeline for the commencement of the 1.5% digital tax regime in the country. To that effect, it is not leaving any stone unturned towards shoring up any loopholes that may be exploited by internet businesses should it decide to go ahead with with the plans. Thus, to forestall a situation where digital tax evaders from Kenya will run to neighboring countries, the tax authorities of Kenya, Uganda, Tanzania, Rwanda, South Sudan and Burundi, member countries of the East African Community (EAC), have agreed on November 11, 2020 to develop a common strategy for the taxation of the digital economy in the sub-region.

Tax

East Africa digital tax East Africa digital tax

In the final communiqué issued at the end of the 48th General Meeting of Commissioners of Tax Authorities of East Africa, which was held virtually, these tax authorities said they had agreed to develop a common strategy “to deal with the taxation of the digital economy by addressing the problems linked to the legal framework, in terms of definitions, identification of actors and legal mechanisms ”.

Through this united front that the members of the ECA want to present, the objective is to put pressure on the global tech giants who are making profits in their various markets. Forced to come to terms with everyone, they will not have the opportunity to take advantage of weaknesses and other gray areas of different tax systems.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer