Following on the heels of other African countries like Tunisia, and Senegal in launching a startup act, Kenya is in the process of adopting startup-specific legislation for the first time after the gazetting of “The Startup Bill, 2020”, but how does the process work, and what impact will the Act, once passed, have on the local startup ecosystem? Disrupt Africa dug into the details.

senator Johnson Sakaja

The first specific startup law globally was passed in Italy in 2012, and Tunisia and Senegal were the first two African countries to have enacted them. A host of countries, including Mali, Ghana, Ivory Coast, the Democratic Republic of Congo (DRC), and Rwanda, are expected to implement their own this year.

Kenya is the first of the “big five” startup ecosystems to publish its own proposed legislation, though there have been some movements to do the same in South Africa. “The Startup Bill, 2020” was published in the Kenya Gazette on September 14, sponsored by Nairobi County senator Johnson Sakaja, under the auspices of the Ministry of Education, Science and Technology, with most of the implementation assigned to the Kenya National Innovation Agency (Kenia).

The Bill, which aims to “provide a framework to encourage growth and sustainable technological development and new entrepreneurship employment; to create a more favourable environment for innovation; to attract Kenyan talents and capital; and for connected purposes”, will now go through both houses of the Kenyan parliament and a public participation stage before it potentially becomes law. Senator Sakaja held a first meeting with various ecosystem stakeholders on Thursday, September 24, and the first Senate reading is scheduled for tomorrow (Tuesday, 30).

There will then be 30 days of public participation, and the Bill is apparently very much open for review. After three readings and a vote, the Bill will also have to proceed through the National Assembly, as the Senate does not discuss “money” clauses. The whole process of First Reading, Second Reading, Committee Stage and Third Reading is followed again here. Once passed by the National Assembly, it will be referred back to the Senate for concurrence on any changes. Once the Bill is passed by both houses, it is referred to the President for assent, and becomes an Act once this has been granted.

So it will still be a little while before we see The Startup Bill, 2020 passed into law, if indeed that does come to pass, and whether the proposed Act retains its current character also remains to be seen. But what exactly does the Bill, at this early stage of the process, entail?

Though called “The Startup Bill”, the proposed legislation is actually primarily focused on incubators. It allows for the “the establishment of incubation facilities at the National and county levels of government”, and empowers Kenia and county executive committee members to establish a national and county incubation policy framework for the development of the business incubation sector and startup system.

Among other things, it legislates for partnerships with local and international business incubators, the launch of programmes for the certification and admission of incubators into the incubation programmes, and the creation of an enabling environment for the promotion of business incubators, including fiscal and non-fiscal incentives.

What is, and what is not, an incubator, in this case? Well, the Bill says an entity certified as an incubator can be registered as a public limited company, a non-governmental organisation, a private limited company, a limited liability partnership, or a partnership, but it must have as its principal object the “delivery of services to support establishment and development of innovative startups”. They must also have in place “facilities suitable to accommodate innovative startups”, and “adequate equipment for startup activities and innovation”, whatever they may be, and be administered by persons of “recognised competence on business and innovation”.

Legislators would also like your incubator to have established “collaborative relationships” with universities, centres of research, public institutions and financial partners that carry out “activities and projects related to innovative startups”. If your incubator meets all these requirements, it can apply to be listed with a Registrar, who will be recruited by the Public Service Commission of Kenya and appointed by Kenia.

The Bill may focus more directly on supporting incubators, but the idea is that startups across Kenya will be the beneficiaries of this. Among other things, it proposes to “support any research and development activities undertaken by startups”, “put in place mechanisms for pre-incubation of entities and for this purpose, provide training and capacity building programmes to startups registered under this Act”, “put in place mechanisms to enable access to entities from marginalised groups”, and “put in place facilitative structures that ensure the protection of the innovations of startups at the national and international level for the protection of the intellectual property”.

So far, so vague, but the Bill gets very specific when it comes to what criteria a startup must meet in order to be registered as such and qualify for any of the benefits offered by the Kenya Startup Act. To be eligible for this, and therefore admission into an incubation programme, businesses must be registered in Kenya as a company, a partnership firm, a limited liability partnership, or, a bit bizarrely, a “non-governmental organisation”. It must be majority owned by one or more citizens of Kenya.

Startups must be seven years old or less, unless they are in the biotech sector, in which case you can be up to 10 years old, and have as their objects the “innovation, development, production or improvement and commercialisation of innovative products, processes or services”. The Bill also wants you to have a scalable business model, though it doesn’t describe what it considers this to be, while a startup must have its “human resources, total assets, and annual turnover number as prescribed by the Cabinet Secretary

At least 15 per cent of the startup’s expenses must be attributed to research and development activities. Startups can also apply to be listed by the Registrar, should they meet all of those quite stringent requirements.

There is a LOT of stuff in this Bill that sounds nice in theory, but requires more explanation as to how it will be affected in reality. “Kenia and the county executive committee members shall put in place measures to support the establishment and development of startups,” it says, which will include non-defined attempts to “subsidise the formalisation of startups”, “facilitate the protection of the intellectual property of innovations by startups”, “provide fiscal and non-fiscal support to startups admitted into incubation programmes”, “provide support in the form of research and development activities”, and “provide such other support to enable the development and growth of startups”.

Most of how it will do all of this is not really clear, though the Bill does say that Kenia will put in place a programme for the training and capacity-building of startups, and also “facilitate” startups in the application for grant or revocation of patents as well as institution of legal action for infringement of any intellectual property rights. A personal favourite when it comes to the high levels of both aspiration and vagueness within the Bill: “A startup shall be encouraged to cumulatively achieve growth objectives as set out by the Cabinet Secretary by regulation”.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

A plan by young entrepreneurs in Kenya to build a golf course using Blockchain and a stable coin backed by real currency highlights the regulatory challenges facing African governments. The Young Entrepreneurs Network Africa in Nairobi is developing a stable coin known as the YENTS (Young Entrepreneurs Network Token), with the launch planned for November. The coin will initially be used within the network to pay for training or participation in sports events, says the network’s CEO Kamau Nyabwengi.

YENTS CEO, Kamau Nyabwengi

He plans to extend its use to allow investment in a planned golf course in Kenya within about 18 months. “Blockchain can help move products from the supplier to the consumer,” Nyabwengi says. “It allows more efficiency and eliminates middlemen.”

Blockchains work as decentralized databases that record digital transactions in the absence of any central administrator. They are used for crypto-currencies such as Bitcoin, or for a wide range of other uses, such as delivering government services and establishing legal claims over land. Transactions are visible to anyone within the network. Stable coins are cryptocurrencies that are backed by a reserve asset. YENTS will be backed 1:1 by the Kenyan shilling or equivalent US dollar amount.

Nyabwengi argues that potential exists to use the coin for financial services, where it could be used to aggregate small-scale pooled savings for investment projects via Blockchain. Regulations need to be improved to make this possible, he says.

Currently, a physical location is needed for a savings scheme in Kenya, as well as a constitution and board. The Young Entrepreneurs project is currently being tested in Kenya’s regulatory sandbox, which Nyabwengi says will help with the process of getting regulatory approval.

According to the Global Crypto Adoption Index 2020 from Chainalysis, Kenya is fifth in the world for crypto-currency adoption, ahead of the US. South Africa and Nigeria are in seventh and eighth places.

Pan-African Regulation

National approval for YENTS in Kenya wouldn’t be the end of the story. Nyabwengi also aims to spread the use of his stable coin to other African countries.

Blockchains are immutable, and, their proponents argue, completely secure. Yet questions over the compatibility of Blockchain technology with the prevention of money laundering and terrorism financing remain unresolved, according to a report from Smart Africa.

The report says that blockchain-based systems are, in themselves, neither compatible nor incompatible with regulation. Blockchain systems need openness, while preventing crime requires “oversight mechanisms that are difficult to maintain in an extremely open environment”, the report says.

Kenya’s regulatory sandbox is an example of a trend towards “government-driven institutionalisation of blockchain,” Smart Africa says.

That process is still largely confined to the national level and “international institutionalisation still appears to be less common.” Smart Africa argues that a pan-African Blockchain strategy needs to be developed. A consensus on regulatory goals needs to be developed, including harmonisation of data protection rules. There also needs to be a pan-African classification of Blockchain-based financial instruments, as well as a focus on interoperability of different Blockchains, Smart Africa says.

Bottom Line: Africa won’t be able to realise Blockchain’s full potential without a unified regulatory approach.

David Whitehouse is Business editor at The Africa Report

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

There is end in sight for the lingering dispute between Nigerian traders in Ghana as the country is set to revise its controversial investment law that sees each foreign retail trader paying a fee of up to $1 million. To that effect, the Ghana Investment Promotion Centre has completed its revision of the country’s investment law and presented a draft to cabinet. However, the bill for passage into law by Parliament will not be presented to Parliament before the end of this year.

Yofi Grant GIPC’s chief executive

“It is not a question of the law but a bigger issue of trade relationships between nations” says Yofi Grant, GIPC’s chief executive. “From my standpoint it is how well we can equip our traders to be competitive. Our traders are not competitive against others because the others may have cheaper sources of finance, they might have access to markets that we do not have. So for that is the real problem.”

Here Is What You Need To Know

The President Nana Akufo-Addo administration had wanted to see a new GIPC law passed before the end of its first term — to both advance its liberal economic policy agenda and have a key piece of legislation to crow about — it has backed down for now, due primarily to the fierce controversy over foreign traders being disallowed from operating in Ghana’s small scale retail space.

Ghanaweb reports that government is worried that whichever way it handles the issue in the proposed new investment code, the political opposition could create political capital out of it.

Generally, the draft of the revisions seek to further liberalize Ghana’s investment laws in order to attract more foreign investment.

The core of the investment code still in use today was drawn up in 1995, when there were still very few liberalized developing economies to compete against Ghana. Today, there are more than 100 ‘emerging/frontier’ markets in competition for Foreign Direct Investment.

However at the same time the revisions seek to facilitate greater local participation and content in industries so far dominated by foreign interests. But the strategy adopted in the draft revision of the investment code is focused more on facilitating increased local capacity and competitiveness rather than at trying to simply legislate compulsory greater local participation.

Indeed this is the approach recommended by GIPC in the draft revisions towards resolving the ongoing dispute between Ghana and Nigeria over the fate of the latter’s small scale retailers in Ghana.

It is instructive that the last time the Ghana Union of Traders Associations got government to close down foreign owned small scale retail shops in Accra, the local traders immediately took advantage by hiking their prices drastically, which indeed was part of the reason government quickly back pedaled.

Besides, pressure is mounting on government from both ECOWAS and AfCFTA to liberalize access to retail markets by nationals of member countries and with Ghana hosting the latter’s headquarters, Ghanaian trade officials fear that the country’s commitment to regionalist trade will be called into question.

Thus government is applying the temporary solution of postponing legislative debate on the revision of the investment code until its second term begins — assuming of course it wins the upcoming election — while seeking ways to ensure that Ghanaian traders would be price competitive by the time new legislation eases the restrictions.

The thinking is that from early next year, with elections not due for another four years, it will run into much less political traffic than is in place currently.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Technology is something to resist. Whether it foments antisocial behavior, cultural polarization, or wide-scale labor disruptions, technological change is a frustrating and perennial struggle facing society. The benefits largely accrue to a few oligarchs. More existentially, digital technologies rob us of our humanity, as automation and machine learning becomes a dangerous master we must serve.

At least, that’s the woeful impression you may get from some critics. Given this bleak view of affairs, it’s a wonder that anyone tolerates modern technology at all. Why allow such traumatic social shifts if nothing worthwhile comes of it?

Andrea O’Sullivan, director of the Center for Technology and Innovation at the James Madison Institute

It is true that antipathy to technological change animates many proposals for limitations or outright bans on certain applications of technology. Yet apart from a few odd countries, no governments prohibit technological innovation altogether. Why?

The truth is that many people realize that technological innovation, economic growth, and overall human wellbeing are intricately linked and that stemming our innovative capacity means handicapping our potential to progress. If we don’t allow some disruption today, then our overall quality of life will be much lower tomorrow.

Economists have tried to better understand the relationship between innovation and growth for decades. A new paper by Mercatus scholars James Broughel and Adam Thierer assembles the literature on growth theory and accounting to paint a picture of just how important technology is to long-term growth.

How We Know How to Grow

Interest in measuring and modeling the sources of economic growth increased among economists in the mid-20th century. In 1956, Robert Solow introduced what is now called the “Solow growth model,” which tries to explain economic growth using a nation’s stock of labor and capital, plus a generic technological change variable that was assumed to grow automatically. The model predicted that countries with a smaller capital stock—like underdeveloped or war-recovering countries—would grow faster in the short term than better-capitalized countries. But long-run prosperity hinged on technological change.

Just how potent is technological change? Solow’s model inspired a new field in economics called growth accounting, which attempts to empirically measure the things that stimulate economic growth. Solow estimated that almost 90 percent of US output came thanks to technological change; other studies found effects of similar magnitude.

But these early studies were a bit limited by the fact that they did not measure innovation per se. Rather, they estimated total factor productivity (TFP), which is a broader concept. TFP is a measure of a nation’s output that cannot be explained by measured inputs like labor and capital. So it includes things like scale efficiency improvements that are not new “innovations.”

Later, more fine-tuned analyses estimated that anywhere from one to two-thirds of economic growth comes from innovation. While there remains considerable uncertainty about the underlying causes of innovation, the consensus view today is that innovation is a key driver of growth.

A major limitation of Solow’s model was the assumption of automatic technological change. In more recent years, “new growth theory” has sought to explain the process of technological change that drives growth. This body of work, spearheaded and popularized by Nobel laureate Paul Romer, seeks to explain how and why businesses innovate by examining its components. In particular, ideas and new discoveries are important sources of growth in this modern class of economic growth models.

While Solow’s model saw little role for policy in stimulating or slowing growth, models like Paul Romer’s suggest just the opposite. Policies that encourage experimentation, learning, human capital accumulation, and risk-taking can pay huge dividends in the form of future economic growth.

GDP Isn’t Everything

A bit of a caveat is in order. While it is true that the weight of the economic evidence suggests innovation and economic growth are connected in important ways, there are limitations to how we can measure economic progress.

The most popular measures of economic growth are based on changes in gross domestic product (GDP), or national production. While GDP accounts for the value of final goods and services traded within the US during a particular period of time, it does not include certain important, but hard-to-measure, quality-of-life considerations like leisure time, household production, and environmental effects.

GDP also has difficulty accounting for quality improvements, which is a major form of innovation. The appliances and tools that we use today are much more efficient and capable than the ones our grandparents used. While some adjustments are made to “GDP” to try to account for how, say, ovens now come with more features, sleeker design, and “guided cooking” functionality relative to those in the past, these adjustments are far from perfect.

Nor does GDP capture gift transfers, or valuable things that are given away for free. This is especially relevant to online platforms that offer their services to users at no monetary price. If that platform sells advertisements, those sales will be counted in GDP. But the considerable consumer surplus provided to users free of charge goes uncounted in official growth statistics. Broughel and Thierer point out that GDP probably underestimates the contributions of innovation to growth because so many of its outcomes are unmeasurable.

This acknowledgment goes both ways: GDP may also not calculate many negative social consequences generated by innovation, such as the parade of horribles critics pin on technological development.

It is even possible that innovation is associated with lower GDP growth in the short term. This may have been the case during the Great Depression, which was a time of rapid innovation despite general economic decline. In fact, the introduction of particularly sweeping innovations, called “general purpose technologies,” can be “so disruptive at times that they reduce aggregate production for a period of time until the macroeconomy adjusts,” as the paper notes. For example, it’s not hard to imagine that the spread of electricity or the internet led many old business models to fail.

Regardless of these analytical limitations, the empirical association between innovation and growth is well-established in the economic literature. Policymakers who wish to foster economic growth would, therefore, be wise to foster an innovation culture.

Innovating Is Hard to Do

This can be easier said than done. While economists are confident in the association between innovation and growth, they are far less certain about what actually drives innovation. Many have offered theories describing the conditions that give rise to innovation. But the spark that lights cultural creativity is hard to synthetically recreate.

Economists have a good idea of the general ingredients. According to Daron Acemoglu and James Robinson, a nation’s institutions can make or break its capacity to promote technological change. Good institutions foster innovation, bad institutions kill it. And what do “good institutions” look like? Douglas North and Barry Weingast say good institutions protect and promote property rights, which gives people an incentive to find new ways to improve their lives. Other economists, like Deirdre McCloskey and Joel Mokyr, emphasize the role that culture plays in encouraging innovative entrepreneurship, whether through esteem among the bourgeois class or fostering a pro-innovation intellectual elite culture.

What’s harder is the recipe: how can policymakers shape their nation’s laws and cultures to cook up an environment for innovation?

The United States is actually in an enviable position as a nation that houses a thriving innovation culture. We already have the manna from heaven. Our nation’s higher education and research institutions are the envy of the world. Our nimble capital markets adapt to new investment opportunities. Our planet’s brightest minds flock here to build tomorrow. These serendipitous conditions explain why the US has given rise to some of the most successful companies today.

In our case, then, policymakers must play defense. They don’t need to discover a policy environment that can conjure up the magic of innovation. They just need to make sure our policies don’t mess up a good thing and repeal policies that threaten to do so.

This means refusing to succumb to the forces opposed to technological change. Those who are harmed in the short term by disruptive innovation should not be ignored, but neither should innovation be killed. Doing so would mean effectively eating our own seed corn. Rather, policymakers seeking to secure economic growth in the decades to come should protect and extend our innovative environment.

Andrea O’Sullivan is the director of the Center for Technology and Innovation at the James Madison Institute

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Algeria’s Minister of Post and Telecommunications, Brahim Boumzar, has said that the use of electronic payment via Electronic Payment Terminal (TPE), the QR Code or the web merchant is “completely secure” and is “free”.

Algeria’s Minister of Post and Telecommunications, Brahim Boumzar

“In order to encourage citizens to make greater use of electronic payment, financial transactions carried out by citizens via the TPE (electronic payment terminal), the QR Code (payment from a smartphone) and the internet (merchant site) will be free (without any additional fees or taxes),“ said Mr. Boumzar during an awareness day on the subject.

Here Is What You Need To Know

According to Boumzar, the last deadline for the acquisition of TPE by all traders, craftsmen and liberal professions is set for December 31, 2020.

The Universal QR code comprised squares of black and white blocks, which can be scanned by smartphones with the aim of making it easier for businesses to accept electronic payments, without additional fees or taxes.

Singapore, China and the United Kingdom had already launched the Universal QR Codes last year.

“All of these operations are carried out in close collaboration with the Ministry of Commerce and the GIE monétique”, he noted.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Kenya would soon be joining Tunisia and Senegal as the only countries in Africa where a Startup Act exists. Although similar plans are already being mulled by Rwanda, Ethiopia and Ghana, a new bill is before Kenya’s national parliament, and once approved, the East African country will make history as the number three country in Africa with a Startup Act.

“The Kenyan startup ecosystem has experienced rapid growth over the last decade. Construction of Konza Techno City, “Silicon Savannah” is expected to further positively impact the country’s tech startup ecosystem. Start-up is generally associated with young innovative tech companies or new businesses that leverages on technology to solve a problem or pain point of a population segment…[the] Bill…[will] create a more favourable environment for innovation; to attract Kenyan talents and capital…” the bill states.

Here Is What You Need To Know

What Is A Startup Under The Proposed Law?

To begin with, for a business in Kenya to qualify to benefit from the provisions of the law, two requirements must be met:

First, the business must be a startup; and

Second, the business must be registered and admitted into an incubation programme by a Registrar of Startups.

A startup? A business entity is considered a startup in Kenya under the law if all of the following conditions are met:

The business must be registered in Kenya as a: private limited company under the Companies Act; a partnership firm under the Partnership Act; limited liability partnership under the Limited Liability Partnership Act or non-governmental organization under the Non-Governmental Organizations Co-ordination Act.

The business must be newly registered or has been in existence for a period of not more than seven years from the date of its incorporation or registration and in the case however, in the case of startups in the biotechnology sector, the period shall be up to ten years from the date of its incorporation or registration.

The business has as its objects the innovation, development, production or improvement and commercialisation of innovative products, processes or services or if it is a scalable business model.

The business is wholly owned by one or more citizens of Kenya.

At least fifteenpercent of the business’ expenses can be attributed to research and development activities.

A business which is a holder, depositary or licensee of a registered patent or the owner and author of a registered software.

Therefore, once the business is established to be a startup, its startup status then qualifies it to be admitted into an incubation programme.

Established Corporates Are Shut Out!

One significant thing achieved by the law is to shut out startups owned by established corporates. Hence, under the new law, any startup business unit (whether a subsidiary or not) owned by any established company which is not itself a startup, will not be considered a startup.

Also shut out are businesses established or formed as a result of the merger or acquisition of an existing business. In other words, where an existing business was not first registered as a startup, no entity created out of it as a result of a merger or acquisition will be conferred with the status of a startup.

Many countries around the world are increasingly becoming friendlier to startups. The proposed Startup Act in Kenya will be a game changer in Africa as far as VCs’ interests are concerned. Source: Forbes

Once a startup is registered under the law, a few things are required in order for it to continue to maintain its startup status. That is to say, the registered startup must:

Maintain proper accounting and submit its annual financial budgets to the Agency no later than thirty first day of March in each financial year, as well as;

Inform the Kenya National Innovation Agency of a change in its structure, composition or object within a period of one month from the date of the change.

Failure to do all of these will lead to the de-registration of such a startup.

What Special Benefits Accrue To Startups Registered Under The Law?

Access To An Incubation Programme

Under the law, only startups are allowed to take part in an incubation programme, and no other! The law has therefore gone ahead to create the legal framework for the registration and certification of incubators in Kenya, which shall have as their primary purpose the delivering of services in support of the establishment and development of startups.

Consequently, all a startup needs to do to be admitted into such incubators is to make an application for admission into an incubation programme to the Kenya National Innovation Agency or to the relevant county executive committee that manages the incubators, as the case may be. A certificate of admission into an incubation programme is issued at the end of the registration process.

The way the law is structured has further ensured that many incubators are going to spring up in Kenya soon, as a legal framework has been established under the law for the registration of incubators at both the national and county levels. Through the incubators, startups can access both mentoring, technical and funding support. The law specifically mandates incubators to assist startups to implement their ideas and form new business ventures.

Technical And Funding Support

Technical Support:

Under the law, registered startups will be assisted by the Kenya National Innovation Agency to apply for grant or revocation of patents and to institute legal action for infringement of any of the startups’ intellectual property rights.

They will also be assisted to file and register patents at the international level.

They will also be exposed to series of programmes for the purpose of their training and capacity building.

Funding Support

Creation Of A Credit Guarantee Scheme

One of the most innovative funding opportunities created by the law is a ‘Credit Guarantee Scheme’ to be established by the country’s Cabinet Secretary for science, technology and innovation. The credit guarantee scheme shall, among other things, guarantee investments for investors in Kenyan startups; offer accessible funding support to startups; provide a framework for credit guarantee for startups; make available financial and credit information to startups; and assist startups to build capacity on financial and risk management.

Inclusion Of Startups As Beneficiaries Under Kenya’s National Research Fund

The law also increases the chances of startups accessing funds through the National Research Fund of Kenya. To that effect, the law has reconstituted the Board of Trustees of the Fund to include two persons representing startups in the country nominated by the most representative organisations representing startups. The implication of this is that startups in Kenya will further be exposed to funds under the country’s National Research Fund apart from the ones they already have access to.

Tax Incentives

Although no express tax exemptions or incentives were made under the law, the law however, opens up the possibility of grant of incentives to registered startups. Accordingly, Kenya’s Cabinet Secretary for science, technology and innovation is empowered, in consultation with the Cabinet Secretary responsible for matters relating to finance, to put in place measures for the granting of fiscal incentives including tax incentives in favour of startups in the country. This will unarguably pave way for the easy categorisation, identification and grant of tax incentives to startups in Kenya.

Kenya may be joining Tunisia and Senegal as the only countries in Africa with a Startup Act

Criticisms And The Implications Of The Startup Law Generally

Criticisms

The proposed law failed to draw a line between registration as a startup and registration into an incubation programme. The law implies that a business entity shall not be called a startup if it has not been issued with a certificate of admission into an incubation programme. There should be clarity as to whether a business entity can stand on its own and still retain its startup status once it has been registered as a startup without being admitted into an incubation programme at the same time. This argument is even strengthened by the fact that the law provides that “an entity shall be eligible to be registered as a startup and for admission into an incubation programme” on the one hand; and that “an entity that qualifies for admission into an incubation programme…may submit an application, in the prescribed form,” on the other hand.

The proposed law also failed to specify whether the Kenya National Innovation Agency or the relevant county executive committee shall be responsible for assigning startups into various incubation programmes.

No express provisions for tax support were made, either in favour of investors or startups. The law only promises to create rooms for tax incentives.

Implications

Combined with the recent 30% ICT policy in the country, the Startup Act, if it ever comes into effect, has the capacity of creating in Kenya the largest concentration of incubators in Africa.

The Startup Act will, also, finally separate startups from SMEs in Kenya, thereby enabling the Kenyan government to precisely target startups.

Overall, the latest proposed law will draw foreign investors more to the East African country. Kenya is famous for leading all VC investments in Africa in recent years. In 2018, the country received the highest amount of VC investments in Africa. This is even aided by the fact that the country, at 87.2%, has the highest internet penetration rate in Africa (47 million internet users out of a 54 million population).

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

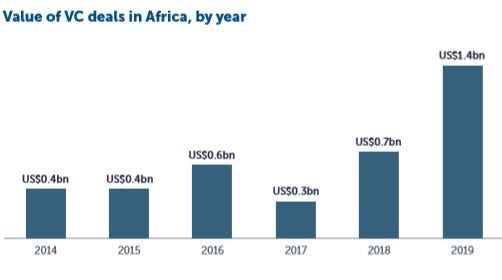

Nigeria has been at the forefront of the African startup ecosystem. According to the most recent report from the African Private Equity and Venture Capital Association, between 2014 and 2019, Nigeria accounted for 14% of all total VC funding deals done in Africa, just behind Kenya (at 18%) and South Africa (at 21%). However, even though the number of VC deals concluded on startups in Nigeria is much lower than that of South Africa or Kenya, VCs are pouring larger amounts of money into the West African country compared to South Africa or Kenya. For instance, according to the data firm, Partech Africa, in its 2019 venture capital report, Nigeria topped Africa’s VC funding landscape with US$747 Million in VC investment (37% of all funding). A similar feat was repeated by the country in 2016 and 2015, with South Africa and Kenya taking the lead, only recently in 2017 and 2018 respectively. Nigeria also houses Africa’s most valuable startup ecosystem — Lagos — which according to Startup Genome, in its Report, was worth $2 billion as of 2017. For one thing, Nigeria is Africa’s largest economy, behind South Africa with a Gross Domestic Product (GDP) of $400 billion (as at 2018) as well as the continent’s most populous country with a World Bank estimated population of 202 million people.

In view of these, it has become relevant to explore how Nigeria supports its startup ecosystem through its laws, regulations and policies.

Incentives — Tax Exemptions

A. For Venture Capital Firms

A long range of tax exemptions are given to investments made by venture capital companies in Nigeria under the country’s Venture Capital Incentives Act.

Consequently, under the Act, for every equity investment made by a venture capital company in a startup in Nigeria, there are deductions from the amounts to be paid as tax from the startup company’s income tax, each year until 5 years after each investment. For the first year, 30% will be deducted. For the second year, another 30% deduction will be made; 20% in the third year; 10% in the fourth year; while 10% deduction will be made in the fifth year.

Again, the withholding tax to be paid on dividends declared in a startup funded by a venture capital company in Nigeria is 5%, under the law, for the first five years of the investment.

Where the equity investment of the venture capital firm in a Nigerian startup company is sold or disposed of, the gains made by the venture capital firm on the equity investment is not liable to capital gains tax by the provisions of the Nigerian Capital Gains Tax.

However, to qualify to benefit from the incentives, investments by the venture capital company must make up at least 25% of the total funding required by the startup. The investment must also be specifically made in innovative companies; or for commercialization of research findings with high returns potential; or for the purposes of promoting SMEs. The venture capital company and the startup receiving the venture capital must, also, first be registered with Nigeria’s Federal Inland Revenue Service (FIRS), in charge of collection of taxes on behalf of Nigeria’s federal government, in order to benefit from the tax exemption.

Better Legal Framework For A VC Fund

Under Nigeria’s newly passed Companies and Allied Matters Act (‘The CAM Act’), it has also become easier to set up a legal structure for a VC fund. By the terms of the new law, venture capital firms in Nigeria may now be set up as limited liability partnership or limited partnership.

Previously, before the law came into being, it was normal practice to register VC firms as limited liability companies; general or limited partnerships, or as limited liability partnerships under the Partnership Law of Lagos State (Nigeria’s major economic city).

Even though under the old regime, general and limited partnerships could be registered and applied throughout Nigeria whereas limited liability partnerships only applied in Lagos, the new regime spells out definite governance framework for partnerships generally, as well as enlarges the operational scope of partnerships to cover the whole of Nigeria, and not just Lagos alone.

The essential difference between a limited liability partnership and a limited partnership under the new law is that while a limited liability partnership is a corporate body which has a legal personality different from the partnership as well as a perpetual succession, a limited partnership has no separate identity from those of the partners that make it up.

Indeed, a limited partnership under the new law captures the ideal form of most VC funds, which usually have one or more partners called general partners — responsible for the management of the funds under the partnership, and who are also liable for the debts and obligations of the partnership — as well as one or more persons known as limited partners — who contribute certain sums of money or property to the partnership and who shall not be liable to the debts and obligations of the partnership.

Apart from properly providing a clear legal framework for the operation of VC funds in Nigeria, the new partnership regime, under the CAM Act, also functions to provide some clarity about their taxation.

Under the Nigerian tax laws, dividends declared by a VC firm that is a partnership — from its investment in startups — are subject to a 5% withholding tax. Where the dividends are declared by the fund and are shared in a partnership, the amount each partner is entitled to is further taxed under Nigeria’s Personal Income Tax Act. However, where a partner who is part of the VC firm is a limited liability company, the company must pay company income tax of 30% on profits made from such earnings, including a further 2% education tax and 10% withholding tax.

Where, however, the VC firm is a limited liability company, under Nigerian laws, apart from paying a corporate income tax of 30%, they also pay 5% withholding tax and 10% capital gains tax (or zero capital gains tax where it is the equity (or shares) of the company that was disposed of).

Innovative startups in Nigeria have a range of incentives to encourage their early stage growth, even though in most instances, the process of applying for and securing the incentives are demanding, and in most instances unrealistic. The incentives include:

The Exemption Of Early Stage Startup Companies From Corporate Taxes

Under Nigeria‘s new Finance law:

Small businesses with annual turnover of less than ₦25m ($64.5k) are now exempted from Companies Income Tax. However, to benefit from such incentive, such small businesses must first register for taxation in Nigeria and must continue to file tax returns during the period their profits are below the ₦25m threshold.

A lower Corporate Income Tax rate of 20% ( as against 30%) will however apply to medium-sized companies with yearly turnover between ₦25m and ₦100m ($258k). To benefit from such incentive, the companies must first register for taxation in Nigeria and must continue to file tax returns during the period their profits are between the ₦25m and ₦100m thresholds.

The law now, also, allows a minimum tax rate of 0.5% for every turnover and this provision will only apply to small companies (less than ₦25m turnover), thus allowing companies non-resident in Nigeria for tax purposes to pay minimum tax.

Again, for companies or businesses that pay their tax dues early, a 2% deduction bonus on tax payable is given, in the case of medium-sized companies between ₦25m and ₦100m; and 1% deduction for large companies from ₦100m and above.

A Pioneer Status Tax (Free Tax) Incentive For Innovative Business Models

Although this is one of the most significant incentives available to early stage startups in Nigeria, there were only about 35 standing beneficiaries of pioneer status tax incentive in Nigeria as at March 2020, out of which only 1 is an ICT firm and 6 are agro-businesses; even though more than 125 applications were filed for the grant of the incentive during the period.

Nevertheless, by virtue of the provisions of Nigeria’s Industrial Development (Income Tax Relief) Act (“IDITRA”), the Pioneer Status is to be granted for an initial period of 3 years with a possibility of an extension for another 2-year period to companies in their first year of business or operations in Nigeria. The companies must, also, be among those on the list of pioneer industries in Nigeria. Consequently, companies or businesses older than a year would not benefit from the pioneer status incentive.

Again, businesses that have existed for several years in a particular sector may not enjoy the pioneer status, except such companies branch into new lines of business covered under a list of 27 or more new industries and products.

To qualify for the Pioneer Tax Incentive, the company must also have incurred capital expenditures of up to ₦100m ($258k). Companies granted Pioneer Status Incentives in Nigeria also enjoy tax relief on income earned during the tax holiday period and dividends paid from the profits earned during the tax holiday. The incentive also enables the company to set off tax losses incurred during the tax holiday against profits earned after the holiday, and to deduct capital expenditure in the same manner.

A Right For Startups To Partner With Large Corporates In Projects Above $1 Million

Under Nigeria’s Guidelines for Content Development in Information and Communications Technology, all indigenous or Nigerian Companies who have secured IT projects or contracts with any Nigerian Federal Public Institution or Government owned companies, of which the gross value of the project is Five Hundred Million Naira (N500,000, 000, 00)or above, shall engage on the project, a Nigerian startup or incubation team for the purpose of Research &Development on the project.

The Guidelines apply to all Federal Ministries, Departments and Agencies, Federal Government Owned Companies (either fully or partially owned) Federal Institutions and Public Corporation, Private Sector Institutions, Business Enterprises and Individuals carrying out business within the Information and Communications Technology sector in Nigeria.

An Alternative IPO Exit Route As Startups Can Now List On A Special Board On The Nigerian Stock Exchange

Nigeria also has developed a new mechanism that will allow high-growth startup companies to list on the Nigerian Stock Exchange. A fourth board on the exchange meant for small businesses and startups has now been launched, to that effect.

This has strengthened the exit alternatives available to startups in the country. That is, startups in Nigeria, apart from acquisition, may now consider IPOs (Initial Public Offerings) on the Nigerian Stock Exchange. The board, known as the Growth Board would offer them the opportunity to raise equities for their businesses.

However, it appears this is over-flogging a dead horse. A similar board, known as the Alternative Securities Market (ASeM) had previously been created by the exchange for emerging businesses — small and mid-sized companies with high growth potential. Findings show that only 9 companies (mostly in the oil and gas industry;none of which is a tech startup company), have been listed on the board.

One significant reason for this lack of interest by startup companies is the unappealing state of the Nigerian Stock Exchange, which at a market capitalisation of $ $36.91bn, is 22 times smaller than the Johannesburg Stock Exchange (at$825.66 Billion).

There are a number of government-backed funds available in Nigeria, a majority of which are by way of loans and not equity. They are listed below:

Nigeria’s Central Bank Intervention Funds

The Central Bank of Nigeria, from time to time, launches series of intervention funds, aimed at startups and small and medium scale businesses.

For instance, owners of businesses in the Nigerian creative industry may now access loan facilities as high as ₦500,000,000 (about $1.4 million). The Creative Industry Financing Initiative is targeted at:

Businesses in the fashion (including designing) industry

Businesses in the Information Technology (including e-commerce, online payment solutions, software engineering etc.)

Businesses in the Nigerian movie industry (including movie producers, movie distributors)

Businesses in the Nigerian music industry (whether as record labels, music artistes, etc.).

The businesses may get up to the following amount:

A student of Software Engineering anywhere in Nigeria may get up to ₦3 million ($ 8,294) to boost his/her education.

Movie Production businesses may get a maximum of ₦30 million ($82,943) to boost their businesses.

Movie distribution businesses may get up to ₦500 million ( $1.4 million)

Businesses in the Nigerian Fashion and Information Technology can also get funds to cover their rental/service fees (the exact amounts were not specified)

Music Businesses may also get funds to cover their training fees, equipment fees, and rental/service fees.(The exact amount is however not specified. It also appears that the funds are not extended to businesses of production of music, and other related music roles).

Other intervention funds by the central bank include the Micro, Small, Medium Enterprises Development Fund (MSMEDF); Commercial Agric Credit Scheme (CACS); Real Sector Support Facility (RSSF), etc.

To access any of the intervention funds, startups may need to go through financial institutions authorised by the central bank to disburse the funds. FCMB is an example of a Nigerian bank that participates in the scheme. Interested startups can check out its offers here.

Funds Under Nigeria’s Bank Of Industry

There are also series of funds operated by Nigeria’s Bank of Industry, the oldest and largest Development Finance Institution currently operating in Nigeria. BOI provides financial assistance for the establishment of large, medium and small projects as well as the expansion, diversification, rehabilitation of existing enterprises. Consequently, the Bank operates funds targeted at youths (Graduate Entrepreneurship Fund; Youth Entrepreneurship Support (Yes) Programms; Youth Ignite Programme); women; asset finance; as well as working capital.

To access any of the intervention funds, it may be easier to go through financial institutions authorised by the bank to disburse the funds.

FCMB is an example of a Nigerian bank that participates in the scheme. Interested startups may also check out its offers here.

Development Bank of Nigeria (DBN)

Development Bank of Nigeria exists to alleviate financing constraints faced by Micro, Small and Medium Scale Enterprises (MSMEs) in Nigeria. The DBN loan repayment duration is flexible (up to 10 years with a moratorium period of up to 18 months).

To access any of the intervention funds, it may be easier to go through financial institutions authorised by the bank to disburse the funds.

FCMB is an example of a Nigerian bank that participates in the scheme.

Interested startups may also check out its offers here.

Future Generations Fund Under Nigeria’s Sovereign Investment Authority

The purpose of the Future Generations Fund is to preserve and grow the value of assets transferred into it, thereby enabling future generations of Nigerians to benefit from the country’s finite oil reserves.

The fund is mostly available to venture capital or private equity firms, and not directly to startups.

Although Nigeria has not expressly permitted equity or loan crowdfunding, there is a proposed regulation to that effect.

Under the proposed regulation, only MSMEs (Micro, small and medium enterprises) registered as companies in Nigeria with a minimum of two-years operating track records shall be eligible to raise funds through a Crowdfunding Portal registered by Nigeria ’s Securities And Exchange Commission.

The following recommendations are, therefore, important and if properly harnessed, have the potential to unlock the continent’s largest economy:

Startup Act:

Nigeria is long over-due for a Startup Act, which has since been adopted by other African countries such as Tunisia and Senegal.

One thing a Startup Act does is to aggregate all efforts geared towards promoting and uplifting all startups in countries where the Act exists. For instance, having a Startup Act will help to tailor incentives to startups more precisely, unlike what obtains presently in Nigeria where established corporates and well-funded companies end up benefiting most from the existing tax incentives, such as the Pioneer Status Incentives.

The Senegalese Startup Act, among other things, grants special status (known as a label) to a labelled innovative and disruptive private or public company, which has been legally registered for a period of not more than 8 years; and whose strong growth potential is built on a disruptive economic model. The law also applies to any startup created by any Senegalese living abroad who owns at least 50% of the startup. This will, undoubtedly, attract more investments back home from Senegalese citizens living in foreign countries.

Enactment Of The Equivalent Of South Africa’s Section 12J

Another policy change capable of facilitating the growth of startups in Nigeria is the introduction of an equivalent Section 12J of South Africa’s Income Tax Act of 2009.

The incentive allows investors who make investments in approved Venture Capital Companies (VCC) — that then invest in qualifying small companies — a tax deduction.

Thus, by investing in a Section 12J venture capital company, the investor not only qualifies for a full deduction of the total investment amount from their taxable income in the relevant tax year, but they are also indirectly supporting the South African economy and the growth of local SMEs.

By operation, Section 12J works like this:

A tax-paying entity (corporate or individual) approaches a VCC with its investment.

The VCC accepts the investment for investments in its portfolio companies and issues the investor with a certificate for the amount invested.

With this certificate, the investor approaches the South African Revenue Service (SARS) and presents the certificate. The certificate empowers the investor to deduct the full value of the investment from their taxable income in that tax year.

Section 12J is so attractive to investors that when the investment reaches maturity and the investor withdraws from the VCC portfolio, the capital gains tax on the investment will be zero as a result of the initial benefit of the 100% tax deductibility.

This explains why there are, today, many VC firms in South Africa and why South Africa has collected more than 21% of all VC funding deals in Africa between 2014 and 2019, whereas Nigeria only received 14% of the deals, even though Nigeria is the continent’s largest economy and has more than 3 times South Africa’s population.

Although Nigeria has a venture capital legislation, there is a big difference between enticing individual and corporate investors to invest in venture funds and enticing venture funds to invest in startups. Nigeria is simply doing the latter; and because of the risk aversiveness of investors in emerging markets, the country may not get the results it desires for its local startup ecosystem any time soon.

Establishment of Equity Funds For Startups

What Nigeria currently has are credit facilities for startups. There should be government-backed equity funds that take up shares in startup companies instead of credit facilities that usually come with strong terms such as interests, modes of repayment of principal sums, etc.

Equity participation in early stage startups function to assist them to go through the difficult periods of their early years until they are mature enough to take in any type of financing.

Indeed, while Nigeria maintains little or no presence in early stage investing by way of equity funds, countries like Egypt and South Africa do not.

Top South African companies in 2016, for instance, launched the $84 million SA SME Fund, a VC fund to co-invest alongside various investors (not solely VC investors). SA SME Fund CEO Ketso Gordhan said the fund would invest about 75% of the sum in black-owned small and medium-sized enterprises, including tech startups.

SA SME Fund and the government’s Technology Innovation Agency (TIA) have, also, further announced a public-private partnership to co-invest R350 million across three venture capital funds. The partnership sees over R350 (over $23 million) invested in the three venture capital funds. South Africa’s SME Fund’s mandate to the three fund managers includes a requirement that they invest at least 50 percent of the fund into businesses owned by black entrepreneurs.

In Egypt, there is Bedaya, a government-backed incubator, established by Egypt’s General Authority for Investment and Free Zones (GAFI) in 2009. The incubator offers up to LE 150,000 (US$9,047) in funds as well as business development services, networking opportunities and manufacturing spaces to startups in Egypt. 60 percent of Bedaya’s fund is allocated to supporting startups from governorates outside of the capital, Cairo.

In Morocco, government-owned financial institution “Caisse Centrale de Garantie-CCG” also partners with the Maroc Numeric Fund to facilitate access to financing for very small and medium-sized businesses and, more recently, for innovative project developers and startups.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Nigeria’s Securities and Exchange Commission, in charge of regulating investments and securities in Nigeria has some new words for all crypto traders, including crypto advisors in the country: all crypto assets are securities and must be registered! In a new statement, the commission is challenging anybody who says that the type of cryptos they offer are not securities (and therefore should not be registered) to prove so to it. This would be a very long process, including having to go through a legal battle — in the country’s Investments and Securities Tribunal — if need be.

What Do The Rules Say?

The rules are sweeping in their entirety. First, it says that all virtual crypto assets issued in Nigeria are securities, unless proven otherwise. In Nigeria, under the Investments and Securities Act, which establishes SEC, securities simply mean any shares or other instruments offered by a company, usually to members of the public.

Who Exactly Will Be Regulated Under The Rules?

The rules say that any person who renders any form of blockchain-related and virtual digital asset services must be registered by the Commission. Such services include, but not limited to receiving, transmitting or executing any crypto orders on behalf of other persons whether on a personal account or on a public platform. Activities also covered include advising generally on cryptos; rendering crypto-related custodian or nominee services.

Are All Crypto Assets To Be Registered?

By Section 54 of Nigeria’s Investment And Securities Act, SEC is only mandated to register all securities of a public company and all securities or investments of a collective investment scheme. A public company in Nigeria is one which has more than 50 members and which can invite members of the public to subscribe to its shares. A collective investment scheme is a scheme whereby members of the public are invited or permitted to invest money or other assets in a portfolio.

It follows therefore that SEC still retains the power to register crypto assets under a collective investment scheme, even though the crypto company is not a public company and does not invite members of the public to subscribe to its shares.

In any case, SEC is not registering crypto assets held by individuals unless the individual holding it trades generally in cryptos; that is to say, the individual runs a platform or a medium for receiving and dealing in cryptos.

The most important words are that the cryptos are traded on a recognised exchange or dealt with as an investment. Therefore where it is not traded on a recognised exchange or dealt with as an investment, it may not be registered with the commission.

Generally, utility Tokens or “Non-Security Tokens” (e.g., virtual tokens, which provide users with a product and/or service) need not be registered, unless they are traded on a recognised investment platform.

By the new rules, all Digital Assets Token Offering (DATOs), Initial Coin Offerings (ICOs), Security Token ICOs and other Blockchain-based offers of digital assets within Nigeria or by Nigerian issuers or sponsors or foreign issuers targeting Nigerian investors will have three (3) months to either submit the initial assessment filing or documents for registration.

What Happens If The Issuer Of Cryptos Is Based Outside Nigeria, But Offers Cryptos In Nigeria?

By the new rules, the Commission may require Foreign or non-residential issuers or sponsors to establish a branch office within Nigeria. However foreign issuers or sponsors will be recognized by the Commission where a reciprocal agreement exists between Nigeria and the country of the foreign issuer or sponsor.

A recognition status will also be accorded, where the country of the foreign issuer or sponsor is a member of the International Organization of Securities Commissions (IOSCO).

The implication of this is that, under the new rules, it may be difficult getting foreign-based crypto issuers to register in Nigeria unless SEC forces them to open offices in Nigeria.

What Is The Process Of Registration

Registration is simple. First, the applicants are given the opportunity of proving that the virtual assets offered by them do not constitute securities by making an initial assessment filing.

However, where the finding of the Commission is that the virtual assets are indeed securities, then the issuer or sponsor must register the digital assets.

Are There Exemptions?

Yes. If the cryptos are offered through crowdfunding portals or other exempt methods.

What Happens If The Securities Are Not Registered?

Under Section 13(x) of ISA, SEC may seek judicial order to freeze the assets (including bank accounts) of any person whose assets were derived from the violation of the laws.

The Implication Of These For Crypto Startups And Traders In Nigeria

Those who will be most affected by the new rules are established Nigeria-based crypto platforms offering crypto-related services in the West African country. However, there is still ambiguity around the rules as the rules state that crypto assets are neither issued nor guaranteed by any jurisdiction, — they fulfill their functions only by agreement within the community of users of the crypto Asset. In others words, is it possible to legitimize what has no background in law? That is, shouldn’t crypto assets be treated as matters of personal contracts between parties? In any case, while the latest regulation may be an edge for platforms that are able to append the badge of legitimacy from SEC, nobody is really sure of how the government wants to wield its new cudgel. Anybody dissatisfied with the decisions of SEC may go to the Investment And Securities Tribunal.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Leading telecoms companies in Kenya such as Safaricom, Telkom and Airtel Kenya have decided to compensate customers who experience interrupted services due to network outages, reports Gadgets Africa. Safaricom, Telkom and Airtel Kenya have decided to compensate customers who experience interrupted services due to network outages. This comes shortly after the Communications Authority of Kenya (CA) issued new draft regulations “to compel telcos to either pay or offer credit equivalent to the time users are without voice, data and SMS services”.

Communications Authority of Kenya

These guidelines are said to be part of the Kenyan government’s “effort to shield the millions of subscribers across the country from poor services related to network outages which include lack of internet connections”. This is something that is expected to push telcos to step-up the quality of their services.

“A licensee shall develop and implement an outage credit policy in situations where service is unavailable due to system failure and not as a result of scheduled and publicised maintenance, or natural disaster,” reads draft rules published by the CA. “(The policy) will compensate subscribers or issue credit equivalent to usage over a similar period that outage lasted (and) compensate customers for each day that service has been unavailable.”

Safaricom is reportedly testing a new web app feature that allows users to track their airtime and data usage, according to TechWeez. Users who want to test out this feature will need to log on to the web app via their smartphone,Safaricom will then verify the users by sending an OTP to their device. Once logged in, users can track their airtime and data usage by selecting the account tab. From there, users should be able to choose to view either their data or airtime usage.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Nigeria ’s Securities and Exchange Commission, in charge of regulating investments and securities in Nigeria has some new words for all crypto traders, including crypto advisors in the country: all crypto assets are securities and must be registered! In a new statement, the commission is challenging anybody who says that the type of cryptos they offer are not securities (and therefore should not be registered) to prove so to it. This would be a very long process, including having to go through a legal battle — in the country’s Investments and Securities Tribunal — if need be.

What Do The Rules Say?

The rules are sweeping in their entirety. First, it says that all virtual crypto assets issued in Nigeria are securities, unless proven otherwise. In Nigeria, under the Investments and Securities Act, which establishes SEC, securities simply mean any shares or other instruments offered by a company, usually to members of the public.

Who Exactly Will Be Regulated Under The Rules?

The rules say that any person who renders any form of blockchain-related and virtual digital asset services must be registered by the Commission. Such services include, but not limited to receiving, transmitting or executing any crypto orders on behalf of other persons whether on a personal account or on a public platform. Activities also covered include advising generally on cryptos; rendering crypto-related custodian or nominee services.

Are All Crypto Assets To Be Registered?

By Section 54 of Nigeria’s Investment And Securities Act, SEC is only mandated to register all securities of a public company and all securities or investments of a collective investment scheme. A public company in Nigeria is one which has more than 50 members and which can invite members of the public to subscribe to its shares. A collective investment scheme is a scheme whereby members of the public are invited or permitted to invest money or other assets in a portfolio.

It follows therefore that SEC still retains the power to register crypto assets under a collective investment scheme, even though the crypto company is not a public company and does not invite members of the public to subscribe to its shares.

In any case, SEC is not registering crypto assets held by individuals unless the individual holding it trades generally in cryptos; that is to say, the individual runs a platform or a medium for receiving and dealing in cryptos.

The most important words are that the cryptos are traded on a recognised exchange or dealt with as an investment. Therefore where it is not traded on a recognised exchange or dealt with as an investment, it may not be registered with the commission.

Generally, utility tokens or “Non-Security Tokens” (e.g., virtual tokens, which provide users with a product and/or service) need not be registered, unless they are traded on a recognised investment platform.

By the new rules, all Digital Assets Token Offering (DATOs), Initial Coin Offerings (ICOs), Security Token ICOs and other Blockchain-based offers of digital assets within Nigeria or by Nigerian issuers or sponsors or foreign issuers targeting Nigerian investors will have three (3) months to either submit the initial assessment filing or documents for registration.

What Happens If The Issuer Of Cryptos Is Based Outside Nigeria, But Offers Cryptos In Nigeria?

By the new rules, the Commission may require Foreign or non-residential issuers or sponsors to establish a branch office within Nigeria. However foreign issuers or sponsors will be recognized by the Commission where a reciprocal agreement exists between Nigeria and the country of the foreign issuer or sponsor.

A recognition status will also be accorded, where the country of the foreign issuer or sponsor is a member of the International Organization of Securities Commissions (IOSCO).

The implication of this is that, under the new rules, it may be difficult getting foreign-based crypto issuers to register in Nigeria unless SEC forces them to open offices in Nigeria.

What Is The Process Of Registration

Registration is simple. First, the applicants are given the opportunity of proving that the virtual assets offered by them do not constitute securities by making an initial assessment filing.

However, where the finding of the Commission is that the virtual assets are indeed securities, then the issuer or sponsor must register the digital assets.

Are There Exemptions?

Yes. If the cryptos are offered through crowdfunding portals or other exempt methods.

What Happens If The Securities Are Not Registered?

Under Section 13(x) of ISA, SEC may seek judicial order to freeze the assets (including bank accounts) of any person whose assets were derived from the violation of the laws.

The Implication Of These For Crypto Startups In Nigeria

Those who will be most affected by the new rules are established Nigeria-based crypto platforms offering crypto-related services in the West African country. However, there is still ambiguity around the rules as the rules state that crypto assets are neither issued nor guaranteed by any jurisdiction, — they fulfill their functions only by agreement within the community of users of the crypto Asset. In others words, is it possible to legitimize what has no background in law? That is, shouldn’t crypto assets be treated as matters of personal contracts between parties? In any case, while the latest regulation may be an edge for platforms that are able to append the badge of legitimacy from SEC, nobody is really sure of how the government wants to wield its new cudgel. Anybody dissatisfied with the decisions of SEC may go to the Investment And Securities Tribunal.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer