A panel of some of Africa’s most promising small and medium-enterprise (SME) agripreneurs gathered online to call for more selective investment, accelerated business acquisitions and increased cooperation to help Africa feed itself and the world. The African Development Bank organized the virtual session, Integrating African Food Systems through the Lens of SME Champions, as a side-event ahead of Africa’s largest agriculture conference – the African Green Revolution Forum (AGRF) – which is being held online for the first time, from 8-11 September. Webinar moderator Atsuko Toda, Bank Director for agricultural finance and rural development, said the panel members, were selected because they are using innovative solutions, tailored their business models, have a proven track record, and shown to have an impact on food systems.

Atsuko Toda, Director for agricultural finance and rural development,AfDB

“We see the importance of the roles that you play, the risks you take and the Bank wants to give you more visibility so that policy makers can understand the challenges of what you are facing and help SME Champions to grow,” Toda said. The group of African “SME Champions” – heads of SMEs across the continent’s food system production, processing, logistics, agricultural digitization and cold storage chain solutions sub-sectors, set the scene for webinar attendees, by describing the challenges and opportunities they face in trying to meet Africa’s food systems demands. Some said policy, programs and financing in Africa are geared toward larger organizations and businesses – and that there is still too heavy a focus on agricultural imports to Africa.

“Especially if you are an SME it is really challenging to penetrate the market and do something significant,” said Nicholas Alexandre, Global Head of Commercial at LORI, a Kenya-based tech-driven logistics company.

Others shared their experiences in overcoming challenges. For example, Nnaemeka Ikegwuonu, head of Nigeria-based ColdHubs, says his solar power, cold storage facility company helps farmers’ produce stay fresher, longer, reducing the need to rush product to market at less competitive prices. ColdHubs says it invested in the storage infrastructure, so that farmers could benefit from the service at a reasonable price.

“We are taking the risk out of ownership of huge cold rooms from smallholder farmers because we design, operate and maintain these cold rooms. We offer a pay-as-you-use service model,” said Ikegwounu.

Kenya’s SunCulture company, which provides farmers with solar-powered irrigation services, also uses a similar “pay-as-you-grow” service fee program. SunCulture CEO and SME Champion Samir Ibrahim told webinar attendees that there has been sufficient development and investment support to African entrepreneurs to know what works – and that it is time to step up scaling up efforts. “We know that there are proven solutions, the focus now should be to target finance and partnerships to scale those…We need donors and multilaterals to start cutting much bigger checks for much fewer interventions…so we can see the needle moving,” Ibrahim said.

Other champions said building up Africa’s agriculture sector lies in building up its agriculture value chains. SME Champion Patricia Zoundi, who started up Canaan Land, a Cote d’Ivoire-based company that trains women in rural areas in order to develop sustainable and inclusive agriculture said, “We have north-north cooperation. We have south-south cooperation. Now it is time to have SME-to-SME cooperation…On this panel, I see three SMEs with which I can collaborate in marketing…[they offer] something I need in my value chain.”

Toda closed the session by reassuring SME Champions that their insights shared would be transformed into key messages intended to reimagine policy, resulting in the accelerated transformation of Africa’s food systems. “There is so much for us to share, proven solutions for us to amplify, to bring forward to scale and consolidate through partnerships and finance.”

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

The scale of the economic impact – as in every region of the global economy – will depend on the policies put in place to keep economies afloat and trade moving across continents. That’s why the political networking and lobbying that’s taking place in Geneva right now is so important for the future of the African continent’s economy, globalisation and the chances of a rebound in global trade and business activity.

Zuneid Yousuf,Chairman, MBI Group and African Green Resources

Three African contenders

Of the eight candidates to be the next chief of the World Trade Organisation, three are from Africa. The favourite in the race, Kenya’s Amina Mohamed, is an experienced diplomat who currently serves as the country’s Cabinet Secretary for Sports, Heritage and Culture.

It is time the voices of Africans are heard at the highest levels of global trade policymaking, and there are several important ways the continent’s perspective can help drive forward a more progressive agenda.

AfCFTA

Let’s start with the African Continental Free Trade Area (AfCFTA). As trade experts point out, though the pandemic has stalled progress somewhat, the AfCFTA can contribute to a post-COVID economic recovery by improving economic resilience, and can promote investment, industrialisation, diversification and job creation across Africa.

Africa’s regional and continental institutions, such as the African Union, lead on regional trade integration, which is a vitally important endeavour. My native Zambia is one of 16 landlocked countries across the African continent, representing half of all landlocked countries globally.

As transport costs represent between 50-75% of the retail price of goods sold in Africa, it’s vital we facilitate and lower the cost of trading across borders as much as possible. This is an important agenda that should be led at the global as well as regional and local level, as we have seen through the pandemic how supply chains have broken down and the consequences for getting vital PPE equipment to where it’s needed, as well as other key concerns like food security.

Secondly, countries are finding themselves being squeezed by the superpower rivalry between the US and China, who are abandoning the rules-based trade system that Amina Mohamed has rightly emphasised as being so important. We need an independent voice for emerging and developing economies to ensure that these rules are respected and enforced so that trade is as free and as fair as possible.

African countries are home to innovative projects that are pushing the boundaries of what can be achieved when business and socio-economic development work hand in hand. As part of the UN’s Global Goals, African countries are putting sustainable development at the heart of their business and trade strategies.

Innovation

In Zambia for instance, two innovative projects have launched which show the potential for marrying sound business models with broader development goals.

African Green Resources, of which I am Chairman, is a new agribusiness that promotes value addition and food security to build a sustainable agriculture economy. It does this by providing inputs and creates markets for small independent farmers as well as more commercial ones, training them in good agricultural practices to achieve high yields.

The other is the Citizen Entrepreneur Development Programme which aims to mobilise an array of stakeholders to promote entrepreneurship and wealth creation across Zambia. Through financial and technical assistance, it hopes to help 1.2 million budding entrepreneurs realise their dreams.

Such projects need to be scaled up and delivered across Africa to provide decent work and livelihoods to millions of young people in Africa, which is expected to double its population by 2050.

Bottom line

Should Amina Mohamed secure the top job at the WTO – the first woman and the first African to do so – the international community would have a real opportunity to undertake long-overdue reforms that are so badly needed.

Africa’s share of world trade is still only 3%, but with some of the fastest rates of growth on the planet – three of the top five fastest growing economies globally are in Africa – we need a WTO chief who can reform the institution and its rules, so that trade delivers growth and better livelihoods for more.

By Zuneid Yousuf is the Chairman of MBI Group and African Green Resources.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

This year’s list of the 100 Most Influential Women in Africa has named Merck Foundation’s CEO Rasha Kelej. The List compiled by Avance Media as part of “Be a Girl” Initiative for her efforts to build health care capacity in Africa and to empower girls in education to help them reach their potential and pursue their dreams. Kelej who is also the President of Merck’s “More Than a Mother” is making it to the List for a second time, the first was when she was selected to One of Most Influential African Women by New African Magazine, UK, 2019.

Dr. Rasha Kelej, CEO of Merck Foundation

Rasha Kelej has been recognized for her efforts through Merck Foundation programs to train thousands of African doctors, to support African communities during Coronavirus lockdown and to empower girls in education so that they can reach their potential and pursue their dreams through the “Educating Linda” program. This is for the second time, as she made the 100 Most Influential Africans (women and men) in 2019 by New African Magazine, UK, for empowering women in general and infertile women in particular through the “Merck More Than a Mother” campaign, which is a historic movement that aims to empower childless and infertile women through access to information, education, and change of mind-sets.

Dr. Rasha Kelej is very well respected in the African Communities at all levels and this for her dedication and passion to unleash the potential of young Africans and her coherent strategy and implementation of serious programs that shape the Public healthcare landscape in Africa positively. More than a thousand young doctors from 35 countries have benefited from unique opportunities of specialty education in many fields such as diabetes, cardiovascular, endocrinology, sexual and reproductive medicines, respiratory, acute medicines, oncology, fertility, embryology, and scientific research.

Expressing gratitude on the recognition, Dr. Rasha Kelej emphasized, “I feel honored and proud to receive this recognition and to be included in this prestigious list among such renowned African women from all spheres of life. This is an important recognition not only for me but to Merck Foundation and our team. As an African and an Egyptian woman, I have a great passion for improving access to equitable and quality healthcare solutions for all Africans. I am very lucky to work as CEO of Merck Foundation as I am empowered by them to realize our unique vision through such successful pan African programs in partnership with African First Ladies, to contribute to the future of these girls as part of our signature campaign “Merck More Than a Mother”. I strongly believe that empowering women starts with education, to enable them to be healthier, stronger, and independent.”

“This recognition will also encourage and motivate me to empower the talented girls of my beautiful continent. I promise to use my influence to support and empower women, support girl child education, and build healthcare capacity in Africa, Asia and beyond”, added Dr. Rasha Kelej. The list has a representation of the most powerful African women from 34 countries, chosen from various career backgrounds including diplomacy, philanthropy, politics, activism, entrepreneurship, business leadership, and entertainment. It includes many famous names like; H. E. Monica Geingos, The First Lady of Namibia; H.E. Elene Sirleaf, Former President of Liberia, amongst others.

Dr. Rasha Kelej, CEO of Merck Foundation and president of “Merck More than a Mother” were recognized last year as one of most influential Africans in 2019 to acknowledge her efforts to empower infertile women through the historic campaign “Merck more than a Mother”.She has been able to work in long term partnerships with 18 African First Ladies as Ambassadors of Merck more than a Mother to build local healthcare capacity, empower girls in education and break infertility stigma across the continent.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

In Africa, wealth isn’t inherited but made, says a new report entitled The African Wealth Report, recently released by Africa’s biggest bank Standard Bank. The report found entrepreneurship to be the most common option used by Africans to create wealth. No less than 148 of 265 people surveyed in Ghana, Kenya, Mauritius, Nigeria and South Africa they made their first million dollars and continued to make more thereafter from entrepreneurship.

Chris Browne Group Head, Standard Bank Wealth and Investment

“To draw a more complete picture of the wealth sector in Africa, a total of 265 respondents were surveyed and 75 face-to-face interviews conducted across five key markets — Ghana, Kenya, Mauritius, Nigeria and South Africa — with the estimated net worth of 67% of participants in the $1 million to $5 million range. Around 16% of respondents had an estimated net worth of $5 million to $20 million, while the researchers from our partners, Intellidex, also canvassed those with $20 million to more than $100 million in net worth,” said Chris Browne Group Head, Standard Bank Wealth and Investment.

Here Is What You Need To Know

38% of high-net-worth individuals in the survey were between the ages of 36 to 50 years.

The favoured industries for entrepreneurs were real estate, construction, trade, financial services, manufacturing, oil and gas, technology and retail.

Only 71 chose an executive career. The report also found that entrepreneurship is a side hustle of respondents who have executive careers, particularly in Nigeria, Ghana and Kenya.

51 others cited the family business as a viable route to wealth creation, while less than 10% of those polled indicated that they had inherited their wealth.

Kenya (38%) followed by Mauritius (29%), Ghana (26%) and Nigeria (23%) stated tangible assets as the most favoured asset class for wealth preservation.

In South Africa, stocks or equities (51%) were by far the most popular asset class for preserving wealth, with tangible assets such as property comparatively less important (18%).

South Africans assigned the greatest portion of their estates to family (89%) followed by Mauritians (86%), Kenyans (84%) and Ghanaians (82%).

Of the five countries surveyed, respondents from Nigeria, Ghana and Kenya were far more likely to cite entrepreneurship as the main driver of wealth creation. By contrast, respondents from South Africa and Mauritius, with their more developed and sophisticated financial systems, were more likely to have opted for a traditional corporate career as a path towards achieving financial freedom. Consequently, South Africa, with the continent’s most developed financial services sector and the most liquid capital markets, has the lowest level of entrepreneurship among these five countries.

In The African Wealth ReportAfrica’s wealthy made their money most from real estate . Source: The African Wealth Report, Standard Bank

Qualities Of Africa’s Wealthy According To The Report

Entrepreneurialism

Most strikingly, entrepreneurialism stands out as the strongest trait amongst High Net Worth Individuals (HNWIs) in Nigeria, Ghana and Kenya. While most HNWIs in these countries made their wealth in one business area, after their first million they tended to expand into businesses in a host of other industries, services or sectors. These high levels of entrepreneurialism appeared to trail off among Mauritian and South African HNWIs. In these economies, with their sophisticated and well-developed financial services sectors, HNWIs were more likely to have made their wealth in their professions — and then invested this in local and global financial markets.

Eclecticism

Eclecticism is a strong feature of African entrepreneurialism. HNWIs in Africa do not restrict themselves to certain sectors. Instead, Africa’s entrepreneurs, once established, tend to be open to new ideas, regardless of whether they have had direct experience in a sector or not. Perhaps the emerging nature of most of Africa’s economies means that all fields are still wide open for Africans to develop products, services and solutions. This reflects the excitement about possibilities and opportunities that characterised our interviews with most of the HNWIs that we met.

Conservative Attitude To Spending Wealth

It is also interesting to see that HNWIs in Africa appear to have a conservative attitude to spending wealth, according to the report. While spending time with family featured highly, along with quality leisure time — including pursuits like travel, reading and fine dining — most HNWIs in Africa were primarily focused on preserving their wealth for broader investment or for future generations, rather than spending it. Few of Africa’s HNWIs were considering acquiring airplanes or prestige purchases that did not grow or preserve their wealth.

Workaholics

According to the report, relatively few respondents opted to give up working after accumulating their wealth, with almost two thirds still working at least 40 hours a week. A significant portion of respondents from all countries still maintain long office hours — between 40 and 60 hours a week — with many still working more than 60 hours a week. Ghana, Kenya and Nigeria were the only countries where any respondents spent more than 10 hours a week on leisure time. In Mauritius and South Africa, no respondents spent more than 10 hours a week on these activities and a significant proportion (39% and 27% respectively) didn’t spend any time on them at all.

“For you to be successful in your business you must work hard, you must be a workaholic like the likes of [Nigerian billionaire] Aliko Dangote, Bill Gates and others. They work all round and that has [convinced me to] wake up very early, go to bed late, thinking of how to add some innovations to my business,” a Nigerian respondent was quoted as saying.

A Ghanaian respondent, however, said: “For every transaction, for every deal that you do, take 10 percent of that money and just have fun with it. There’s no sense in working very hard if you aren’t going to enjoy the money that you’ve made and play with it… And when you’ve made money there’s a lot of satisfaction in enjoying it. But there must be a balance, you have to know when to say, ‘playtime is over’.”

The Most Common Vehicle For Consolidating And Preserving Wealth Is Property

The study found that in Africa, the primary vehicle chosen for consolidating and preserving wealth was property — from urban residential and commercial, through to industrial property, farmland and agribusiness. In fact, across all five countries surveyed, only in South Africa was property not the primary vehicle for wealth preservation. Investments in stock and – equities took the top spot in this country.

Strength in Diversification

The insights show that there is a strong appreciation of the power of diversification across Africa, which was consistently cited by respondents across all markets as being critical to long-term wealth preservation.

“All business is risky. I have diversified my portfolio and invested in different things. I have property, I am in farming, I have a car hire business. So, I might lose in one area but not in all,” one respondent said.

While it may also reflect the strong entrepreneurial streak prevalent in these three countries, respondents also appeared to believe that continued investment in what had helped them accumulate wealth in the first place was a prudent strategy. One Nigerian interviewee said:

“One of the major problems business people have is that … they withdraw the capital and use it for pleasure, but I don’t think that is the right thing. As [my] business is growing, I should keep investing in my business more so that it can grow bigger and better.”

Where Africa’s wealthy made their money from. Source: The African Wealth Report, Standard Bank

When it comes to concerns about preserving wealth, political instability and personal security are the key issues for most high-net-worth Africans. The report noted that without long-term visibility of the policy environment, it is very difficult to make informed investment decisions as a volatile political climate can dramatically affect the value of assets. The political environment is seen as a significant risk to wealth preservation in the majority of markets surveyed — with 82% of South Africans highlighting it as a concern, followed by Ghanaians (67%), Nigerians (64%) and Kenyans (55%). By contrast, only 31% of Mauritian respondents saw the political environment as a threat.

The Bottom Line:

Good report! Africa’s wealthy as analysed in the report is completely captured in what one respondent was quoted (in the report) as saying “what enables you to build wealth in Africa is exactly the same thing that enabled you to build wealth in America and European countries in the 19th and 20th centuries.” However, it should be noted that the 265 sample opinions may not holistically represent what obtains across Africa. The report also appears to have completely excluded North Africa’s wealthy. But the report entirely presented the enormous investment potential across Africa. With 38% of high-net-worth individuals in the survey being between the ages of 36 to 50 years, it means that over 62% of Africa’s wealthy are still 50 and above. With rapidly expanding technological disruptions across the continent and the average age of Africa’s population being 19.7 years, Africa’s wealthy’s psychology and interests in the near future remain open-ended.

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Newly launched women-entrepreneurs-focused fund ShEquity has made its first investment in Nairobi-based data analytics and AI platform, Superfluid Labs, making the latest investment part of series of investments into the startup in recent time.

auline Koelbl, ShEquity Founder and Managing Director

The investment ethos of ShEquity is novel given the several structural and societal inequalities that usually curtail the fulfillment of aspirations of several visionary women. The company is providing a unique platform to equalize gender gaps and will allow many female entrepreneurs to achieve their set business vision much more easily than before. We join others to celebrate ShEquity on this noble cause,” SuperFluid co-founder Winifred Kotin said.

Here Is What You Need To Know

Although the exact amount of this investment remains undisclosed, Superfluid Labs had previously received funding from Green Capital, in 2019.

The investment will help the Superfluid team to continue scaling their operations in Africa, facilitate further IT developments as well as close business development contracts.

Superfluid had also attracted investment from a consortium of angel investors in late 2019 and had recently won the ENGIE credit scoring challenge at the Africa Tech Venture Summit in January 2020.

The startup has also been growing at a exemplified rate even during the COVID-19 pandemic, according to previous investor, Greentec Capital in a statement.

“At Superfluid Labs, we empower businesses creating sustainable lives for impact with the needed intelligence to better serve their customers and create value. The investment will propel our growth and increase our ability to expand economic opportunities through the power of data and AI. Specifically, we shall scale both business and product development as needed to achieve our ambitious growth plans,” Winifred said.

Why The Investor Invested

ShEquity invested in Superfluid for its innovative SaaS business intelligence and algorithmic service offerings.

“We are excited to be backing Superfluid Labs and joining hands with GreenTec to support the team’s journey towards growing and scaling Superfluid Labs. Superfluid Labs is tackling serious challenges which affect many African businesses, especially startups, and the Co-founders, Winfried and Timothy, understand very well African markets where this solution is most needed. Since ShEquity’s offers more than money, we look forward to working closely with the team so that we can get this solution to many businesses across Africa” Pauline Koelbl, ShEquity Founder and Managing Director said.

This is ShEquity’s first investment from its newly launched fund which focuses on providing smart and sustainable investments for African female entrepreneurs and innovators. The investment vehicle which is spearheaded by Pauline Koelbl, provides early-stage capital and structure operational support as well as the facilitation of access to high-value networks.

Led and co-founded by siblings Winfried Kotin and Timothy Kotin, Superfluid Labs is a B2B Data Analytics and AI Platform for businesses and organization to understand and serve customers, predict business events and create sustainable livelihoods. The startup currently serves the following industries: financial services, clean energy, agriculture, retail and startups.

The startup is addressing the following challenges:

Access to finance due to high credit risk.

Limited consumer insights and market intelligence.

Poor customer retention and life-time value growth

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

The COVID-19 crisis has revealed banks to be not part of the problem for a change, but part of the solution. They have so far proven to be resilient, mostly as a result of the stricter capital and liquidity requirements imposed on them following the 2007-09 global financial crises. Today, many governments are using banks to channel funds to households and firms hit by the pandemic’s economic fallout.

Xavier Vives, Professor of Economics and Finance at IESE Business School

The worse economic fundamentals and forecasts become, the more mysterious stock-market outcomes in the US appear. At a time when genuine news suggests that equity prices should be tanking, not hitting record highs, explanations based on crowd psychology, the virality of ideas, and the dynamics of narrative epidemics can shed some light.

Furthermore, governments have granted banks a temporary moratorium on implementing tougher regulatory and supervisory standards, in order to reduce the potential pro-cyclicality of measures introduced in the last two decades and avert a credit crunch. As a result, banks now have an opportunity to reverse the reputational damage they suffered in the financial crisis.

But they are not out of trouble, in part because the crisis will sharply increase the volume of non-performing loans. Moreover, as a recent report that I co-authored points out, the pandemic will accentuate pre-existing pressures – in particular, low interest rates and digital disruption – on bank profitability.

Digitalization will now advance rapidly, because both banks and customers have realized that they can work and operate remotely in a safe and efficient way. The resulting increase in information-technology investments will render many banks’ overextended branch networks obsolete sooner than they expected, particularly in Europe. That will necessitate a deep restructuring of the sector.

Medium-size banks will suffer because they will find it difficult to generate the cost efficiencies and IT investment needed in the new environment. Although consolidation could offer stressed banks a way out, political obstacles to cross-border mergers will likely arise in several jurisdictions as governments become more protective of national banking systems. In Europe, for example, where banking nationalism has been running high (with the exception of the United Kingdom), domestic consolidation seems more likely.

In addition, banks may face renewed competition from shadow banks and new digital entrants that were already challenging the traditional bank business model before the pandemic. In the United States, financial-technology firms, or fintechs, have made important inroads in mortgages and personal loans. And in emerging markets, “BigTechs” – large digital platforms, such as Alipay in China – have come to dominate some market segments such as payment systems.

The rapid digital shift resulting from lockdown measures to combat COVID-19 suggests that the pace of change in the banking sector may take everyone by surprise. That acceleration may in turn also hasten the adoption of different forms of digital currencies, including by central banks.

By further reducing entry and exit barriers in the financial-services market, digitalization will increase competitive pressures and constrain incumbent banks’ profitability in the short run. But its long-term impact is more uncertain, and will depend on the market structure that eventually prevails.

One possible outcome is that a few dominant platforms – perhaps some of the current digital giants, plus some transformed incumbents – control access to a fragmented customer base that inhabits different financial ecosystems. In this case, customers would register their demands on a platform, and financial-services providers would compete to supply them. The degree of platform rivalry and level of customer service would depend on the costs of switching from one ecosystem to another: the higher they are, the less competitive the market will be.

Bank regulators have already adapted to the post-pandemic world by relaxing the implementation timetable for capital requirements. In addition, digital disruption will require them to balance fostering competition and innovation with the need to safeguard financial stability.

In order to do so, regulators must ensure a level playing field, and coordinate prudential regulation and competition policy with data policies. This will require navigating complex tradeoffs among the system’s stability and integrity, efficiency and competitiveness, and privacy.

The pandemic and its fallout will test the resilience of the financial system and of the regulatory reforms introduced after the 2007-09 crisis. The first report by IESE Business School’s Banking Initiative last year concluded that these measures had made banking sounder, but that some work remained to be done, particularly concerning shadow banking.

The response to the current crisis will stretch the limits of central-bank intervention – especially in Europe, where sovereign-debt sustainability may become a more salient issue over the medium term. Furthermore, the crisis will test the eurozone’s banking union, which remains incomplete without common deposit

Banks have a chance to improve their battered public image by playing a constructive role in mitigating the current economic crisis. But with COVID-19 set to accelerate the sector’s digitalization and restructuring, their future could soon become more uncertain.

Xavier Vives, Professor of Economics and Finance at IESE Business School, is co-author (with Elena Carletti, Stijn Claessens, and Antonio Fatás) of the report The Bank Business Model in the Post-Covid-19 World.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

While funding accruing to the African startup ecosystem from venture capital firms is increasing year-on-year, the number of startups involved in the funding are relatively small compared to available data about the number of startups in Africa. In 2019, for example, while a platform like VC4A listed a total of 13,500 startups in Africa, only about 427 startups raised over $2 billion in funding. This means that if you are a startup in Africa, you are only about 3% more likely to raise funds from venture capital firms. Again, this possibility increasingly varies depending on which African country your startup has its headquarters or is operating in. According to a recent report, between 2014 to 2019, venture capital investors preferred to invest more in startups in Southern Africa (mostly South Africa, etc.), with the region getting about 25% of all VC deals; followed by East Africa — Kenya, Tanzania, Uganda , etc. — (23%); and West Africa (21%) — Nigeria, Ghana,etc. While other African countries shared the remaining 31%, Egypt, and other North African countries are also proving to be good destinations for startups in terms of funding.

Why then are many startups still left out in the whole funding bubble? An attempt will be made to provide answers to this.

Poor Understanding of How Venture Capital Funding Works

This is a foundational challenge that confronts most startup founders across Africa. There is an overwhelming disconnect among many founders about what venture capital, and not investors generally speaking, really means. The ability to know the difference between venture capital and angel investors, bank loans, funds from family and friends, or grants is what makes the whole difference between founders who have raised funds for their startups through VCs and those who have not.

Prior knowledge of venture capital, even before setting up a startup company, is very vital for startups desiring to raise funds from VC investors in the future. At the earliest stage, such knowledge would not only assist them in choosing their business ideas, but would also help them in properly structuring their business entities so as to suit the structures usually prefered by VC investors.

Fundamentally speaking, unlike banks that give you only loan and expect interest payment and repayment of the capital sum after a period of time without desiring a stake in your company through the loans, a traditional venture capital company usually takes up ownership stake (shares) in your company, while providing you with the desired capital to run your business, in anticipation of future returns on its investments (usually, also, at an agreed percentage). Venture capital is also different from grants because grants are free money to businesses while venture capital is not.

Knowing these differences will therefore assist startups in choosing what type of business idea to pursue (since VCs are mostly interested in high-growth startups with long-term growth potential); and what structure of business to adopt (since VCs are also interested in taking up shares in the business, or even sitting on its board).

Thus with this explanation, it may be more difficult for a small business which was not structured as a company and which sells fabrics on a small scale to secure venture capital than for another business structured as a company, and which runs a piggery, and has a plan of leveraging technology to expand its market, or which, even though does not leverage technology, has such potential as to so quickly grow and expand across locations and to different markets.

“VC is relevant for high-growth companies. Taking money from VCs and then not growing very fast is the source of many headaches and grey hairs,” says Jean-Claude Homawoo, co-founder and chief product officer at Lori Systems, one of Africa’s bigger fundraising success stories.

“When you take on that money, that money needs returns, and it is a big responsibility. You have to scale the company,” Etop Ikpe, CEO of Nigerian company Cars45, another startup that has successfully raised funds, adds.

The Products/Services And Their Sectors Matter

This is another fundamental problem hindering many startups in Africa from accessing funds from VCs. Indeed, VCs are also business people who, like startups, are out to make money. There may be VCs whose guiding investment values support promotion of social or environmental projects or causes, but a majority of VCs get their funds from other investors, such as pension funds and high net-worth individuals, and therefore, are expected to be accountable and make profit on their investments.

Indeed, acquainting oneself with knowledge of which sectors have attracted VC funding most in Africa in the past should form one of the earliest guiding principles in choosing which startup idea to pursue, although market size, market fit and strikingly innovative solutions (check out South Africa’s SweepSouth, for instance) and overwhelming passion from founders have always dragged investors’ interests into new areas.

Again, since startups are themselves largely untested territories (considering that a majority of them have not existed for an appreciable length of time nor have they been affected by policy changes or market trends), investors tend to stick more to sectors that have proven to return most highly on their investments.

“It is really pattern recognition; they see the kind of deals that have happened in the past and they try to mimic that,” says Homawoo. “They (investors) look for the same makeup over and over again. So for founders that don’t look like those that have raised in the past there is a hurdle. That’s something that we have to break.’’

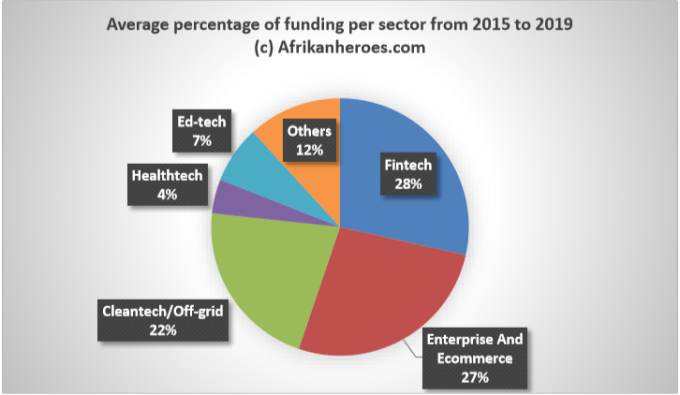

As an instance, until now, much of the investment on the African startup space has gone more to other sectors than healthcare. In 2019 alone, out of a total of 250 deals amounting to a record-breaking $2.02 billion reported by data firm Partech, financial technology companies (fintechs), at 41%, received the lion’s share of the whole investment sum. The set of data below further paints this picture better. From the data, healthcare startups in Africa have managed to secure only about 4% of the total funding raised by African startups in the past four years, compared to the increasing interests shown by investors in other sectors, such as fin-tech (which, at 28% has netted the highest percentage of funding coming to African startups) or enterprise and eCommerce( 27% of the total funding accruing to African startups).

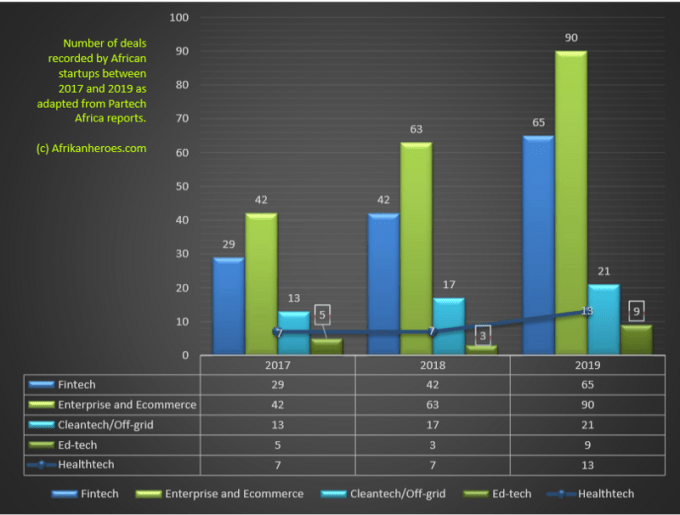

Also worrisome is the fact that investors, until the descent of the coronavirus, had not shown much interests in the African healthcare startup ecosystem compared to others . This perhaps explains the fact that in the past three years (2017–2019), healthcare startups in Africa only closed 27 deals (a majority of them being follow-on or new rounds of investments, as against investment in entirely new healthcare ventures). 27 deals is so meager compared to what fin-tech or enterprise and eCommerce (at 136 and 195 deals respectively) got within the same period.

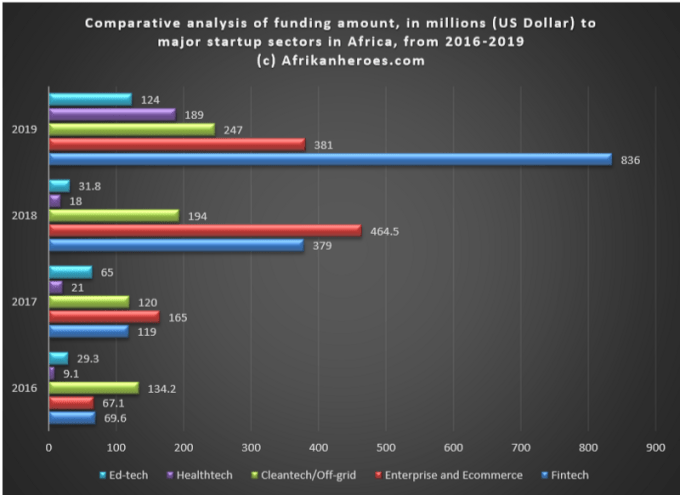

The worst fact about investment in the African healthcare startup space is however yet to come: out of a jaw-breaking $4.1 billion received by African startups in total in four years (2016–2019), healthcare startups only boast of a meagre $237.1 million.

This is far behind what sectors such as fintech or enterprise and ecommerce ( at $1.4bn and $1.07bn respectively) secured during the said period. (For fuller version of all the sectors and how VCs have invested in them click here.)

Therefore, it is recommended that African startup founders, desirous of securing funds from venture capital firms, first study the investment patterns, over the years, of Africa-focused VCs in order to get an insights into how their startups may be affected.

Team Is Everything

Startup founders should not underestimate investors’ bias about who the team members are. In most instances, the choice by VCs, of which team to work with has always, from practical experience and from facts, been influenced by such things as age, gender, race, class, educational background, previous experience founding a startup, nationality or even social networks.

However, while we may not change our individual identities to attract investors, it pays to be strategic. For instance, even though a startup’s founding team may entirely be constituted by persons who are newbies to the startup environment or who have not had any previous experience founding successful startup companies, it pays to have a strong team of advisors/board members, or persons of influence projected prominently behind the team. Investors are more tended to finance who they can trust; who has strong credibility and integrity and who knows their mettle about the sectors they are playing in. The more dense the team, in terms of character, value or influence, the chances of the startups securing funding any time soon. Below is a table of some African startup founders and their pedigree.

B.B.A (Howard) MBA (Harvard); One year experience before co-founding Jumia.

2

Iyinoluwa Aboyeji

Andela

20-30

B.A., Legal Studies (Waterloo); Two years experience before co-founding Andela.

3.

Xavier Helgesen

Zola Electric

30-40

MBA Oxford; Previous CEO and 8 years previous experience.

4

Fara Ashiru Jituboh

Okra

20-30

B.A (North Carolina); Previous 9 years IT experience.

5

Yinka Adewale

Kudi

30-40

B.SC (Ife, Nigeria); 4 years previous IT experience.

6

Obi Ozor

Kobo360

30-40

B.A (Pennyslavia); 6 years previous experience, including at Uber and J.P Morgan.

7

Franklin Peter

Bitfxt

20-30

B.Sc (Nsukka, Nigera); at least one year previous experience.

8

Elia Timotheo

East Africa Fruits

30-40

B.A (Mzumbe, Tanzania); 8 years previous working experience.

9

Aretha Gonyora

Payitup

30-40

B.A (Zimbabwe); 3 years previous experience.

10

Aisha Pandour

SweepSouth

40-50

P.HD (Cape Town, South Africa); 8 years previous experience.

11

Adegoke Olubusi

Helium Health

20-35

B.Sc. (Maryland, USA); 3 years previous experience, including at eBay, Paypal, Goldman Sachs)

12

Adetayo Bamiduro

Max.ng

30-40

MBA (MIT, USA); Over 10 years previous experience.

13

Gregory Rockson

mPharma

30-40

B.A (Westminster, UK); Over 10 years previous experience, including WEF Global Shaper.

14

Trevor Gosling

Lulalend

35-45

B.A (Pretoria, South Africa); 10 years previous experience, including at Goldman Sachs, Rand Merchant bank.

15

Rapa Ricky Thomson

Safeboda

30-50

No education history; Natural entrepreneur with previous experience in transport.

16

Onyeka Akuma

Farmcrowdy

30-40

B.Sc (Sikkim Manipal, India); Over ten years previous experience.

17

Ahmed Wadi

MoneyFellows

40-50

B.Sc (Stuttgart); 5 years previous experience, including at National Bank of Kuwait.

18

Abraham Cambridge

Sun Exchange

40-50

B.Sc (Sussex); Over 10 years previous experience.

19

Deji Oduntan

Gokada

30-40

MBA (Cornell, USA); Over six years previous experience, including at GTB Bank, Jumia.

20

Karl Westvig

Retail Capital

50-60

B.Sc (Cape Town, South Africa); Over 20 years experience.

21

Femi Adeyemo

Arnergy

40-50

M.Sc (Stockholm, Sweden); Over 10 years experience in the IT space, including at Huawei.

22

Meshack Alloys

Sendy

30-40

M.Sc (Nairobi, Kenya); Over 7 years experience in the IT sector.

23

Tosin Eniolorunda

TeamApt

30-40

B.Sc (Ife, Nigeria); Over 8 years previous experience, including at Interswitch,

24

Gilbert Blankson-Afful

Sumundi

30-40

B.Sc (Ghana); Founded Sumundi immediately after education.

25

Adan Mohammed

Ecodudu

30-40

B.Sc (Kenyatta, Kenya); Founded Ecodudu immediately after education.

26

Prince Kwame Agabata

Coliba

30-40

B.Tech (Ghana); Founded Ecodudu immediately after education.

27

Belal El Borno

Yumamia

35-45

B.Sc (AASTMT, Egypt); Over 10 years previous experience, including at Kuwait Food Company.

28

Mohammed Youssef ElBaz

Zedny

50-Above

MBA (Arizona, USA); Over 10 years of previous experience.

29

Neto Ikpeme

WellaHealth

35-45

MBBS (Dublin, Ireland); Over 5 years previous experience.

30

Benji Meltzer

Aerobotics

30-40

B.Sc (Cape Town, South Africa); At least 5 years previous experience, including at Uber.

31

Timothy Mwangi

Amitruck

35-45

B.Sc (MIT, USA); Over 9 years previous experience, including at Oracle, USA.

32

Mostafa Kandil

Swvl

30-40

B.Sc (Cairo, Egypt); At least 2 years previous experience, including at Careem.

33

Temidayo Isaiah Oniosun

Space In Africa

20-30

B.Tech (Akure, Nigeria); At least 3 years previous experience.

34

Waleed Abdl El Rahman

Mumm

35-45

B.A (Cairo, Egypt); Over 10 years previous experience, including at Procter & Gamble, Lebanon.

35

Geoffrey Mulei

Tanda

20-30

B.A (Malaysia); 2 years previous experience at former startup.

36

Stone Atwine

Eversend

40-50

B.Sc (Mbarara, Uganda); Over 10 years previous experience, including at Alliance Francaise.

37

Fatoumata BA

Janngo

30-40

M.A (Toulouse, France); Over 8 years previous experience, including at Jumia.

*Data are based on the public profiles of the founders. In most cases, the number of years of experience and respective age brackets of founders are based on estimates.

It should be noted, however, that a majority of the founders listed above, whose startups have secured VC funding, represent a tiny portion of the entire ecosystem of startup founders in Africa. It should also be noted that all extra information as provided, even though may be of some considerable importance to some VCs, may not be to others.

True entrepreneurship is not bestowed solely on the basis of educational qualifications or age, as can be found above. Of course, there are thousands of entrepreneurs and startup founders scattered across Africa (most of whom are running successful businesses) who may not fit into the qualifications above. What is only stated here is that, given that there are not many VC firms operating on the continent, like it is obtainable elsewhere in the world, it only pays to be strategic enough, through a strong team, to be able to access the limited ones available.

From experience, most startup founders, in a bid to protect their intellectual property, often hide relevant information from investors. In as much as it pays to protect one’s intellectual property, it also pays to determine what information is material enough to be excluded from investor’s early scrutiny. “You can’t keep trade secrets from your investors,’’ says Barry Schuler, managing director at DFJ Growth, one of the first venture firms to focus on growth as a specific practice and an investor in Twitter and Tesla. “The number-one sign of complete transparency is an entrepreneur who says, “I don’t know the answer to that question, but I will get it to you.”Barry adds.

Generally, at a glance, a good startup pitch deck should, among other things, have a strong value proposition, and must give a sufficient clue about how the startup intends to utilise the proceeds of the investment it seeks to secure from the investor.

“People come to me and say they are playing in whatever market,”says Andrea Böhmert, co-managing partner of South African VC firm Knife Capital, “but when we really drill down, their value proposition puts them in a different market. You need to be able to define your value proposition. And then based on that your market. And then understand your numbers and how big that market is.”

Apart from constructing a precise value proposition, a pitch deck must also provide an in-depth guide on how the startup can make returns on the investor’s funds. No investor would be willing to commit hard-earned currencies into a project that has no clear plan on how to spend the money.

“Sweat the financial details,” says Victoria Fram co-founder and managing director of VilCap Investments. “ You need to show an awareness that one of your jobs is to not run out of cash. You need to speak intelligently on dilution and valuation. Say why you’re raising a given amount, what milestones that money will allow you to achieve, and what milestones come next.”

However it goes, always remember to keep your deck concise enough. Whether it is Venture Capitalists or Angel Investors that you are pitching to, keep your deck focused. As VC Iskender Dirik notes, “The attention span of a VC is even shorter than you might think. Be as striking, simple and short as possible.” (source). Similarly, Angel Investor Jordan Rothstein says that one of the key factors in creating a great pitch deck is keeping it “clear and concise” (source, Angel investor).

And finally be transparent with your disclosures when you have established a fair confidence in the investors. To learn how to bounce back from a failed pitch effort click here.

Pitching The Wrong Investors

Nothing could be so frustrating as pitching the wrong investor. Consider the waste of time and resources!

African startup founders usually make the mistake of assuming that most VCs are sector-agnostic. The fact is that while some VCs would prefer to invest in exceptionally ground-breaking solutions that are outside their sectors of focus, the opportunity to do so don’t always present themselves. It therefore behoves on startup founders to first research on active investors in their sectors of focus. This will assist them not only in reducing the time and resources spent scouting for investors, but will increase their chances of landing funding anytime soon.

“Lots of first time entrepreneurs don’t take the time to put together their thoughts,” says Ian Lessem, managing partner of South African investment and advisory firm HAVAÍC.

“If you want to attract VC funding from the US you must understand that companies involved are servicing much bigger businesses serving much bigger markets. If you have no plans to scale outside of South Africa, you would be naive to think a US VC would be interested.”

For African startups playing in the healthcare industry, this link will lead you to a list of active investors in that industry.

Gain Traction

In as much as a recent report says that nearly one third (32%) of the total number of early-stage investments reported in Africa between 2014 and 2019 were seed stage deals, these deals, however, accounted for only 5% of the total deal value, showing that while more investors were investing at the seed stage than at any other stages, they weren’t pouring in more in monetary sums into the startups compared to the amount invested at other stages.

One more way to stand out as an African startup is, therefore, to gain traction. The African market is often referred to as an emerging market because it has not entirely shed its traditional economic focus that relied more on agriculture and the export of raw materials. Hence, investors often regard such markets as highly risky, and therefore deplore greater caution in their investment strategies when investing in them.

“Traction: It’s what investors everywhere are looking for in order to determine whether to anoint your startup,’’ writes Mike Belsito in his book Startup Seed Funding for the Rest of Us: How to Raise $1 Million for Your Startup — Even Outside of Silicon Valley.“the next big thing” and inject the cold, hard cash needed to accelerate your business. If you can’t find traction, forget raising capital — your business will struggle just to stay alive. Find traction, and raising capital will never be an issue for you. It’s important, however, to understand what traction really is — and what it isn’t.”

This writer wishes you great success and luck in your fund-raising journey. The journey may be hard, but always remember that patience, almost always, pays; plus you are always one pitch away from getting a signed term sheet.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer.

A new report released by Startup Genome, tagged the Global Startup Ecosystem Report (GSER) 2020 has ranked both Cairo, Egypt’s capital city and Cape Town, South Africa as Africa’s number one startup ecosystems, closely followed by Lagos, Nigeria. While Cairo city and South Africa’s Cape Town were ranked 51 in the world, Lagos, Nigeria and Kenya’s Capital, Nairobi were both ranked 61 in the world, signaling a major loss for Africa’s most populous country, Nigeria, which has suffered continued losses in similar reports released recently. The three African cities, however, are the only African startup ecosystems to feature on the Top 100 Emerging Ecosystems Ranking.

“Our ranking this year goes beyond the top ecosystems to include “Emerging Ecosystems” — the next 100 ecosystems after the top ones. As startup culture and entrepreneurship spreads across the world, different ecosystems are gaining relevance and impacting economies in a meaningful way. The factor weights used to rank these ecosystems are slightly different from those used with top ecosystems (detailed in our methodology section) to reflect their emerging status and emphasize the factors that influence more in ecosystems that are just beginning to grow,’’ the GSER report noted.

Here Is What You Need To Know

According to the report, the top 10 Emerging Ecosystems globally are, in order: #1 Mumbai, #2 Jakarta, #3 Zurich, #4 Helsinki, #5 Guangzhou, #6 (tie) Barcelona, #6 (tie) Madrid, #8 Philadelphia, #9 Manchester-Liverpool, and #10 Research Triangle.

Combined, the Emerging Ecosystems represent 49 countries and $348 billion in Ecosystem Value.

Europe is the leading continent for Emerging Ecosystems, with 38 cities in the list followed by North America with 32 startup ecosystems and Asia-Pacific is third with 22 ecosystems.

Elsewhere, the report noted that the top five global startup ecosystems remain the same, although with some movement within them. Silicon Valley maintains its #1 position. New York remains at #2, although now London is up and tied with it. Beijing is at #4 and Boston is at #5. Among the top five global startup ecosystems, only London was not in the top five in the 2015 ranking. Tel Aviv and Los Angeles follow, both tied at #6.

The Rise of Asia is more visible this year in the report, with 30% of the top ecosystems coming from the region, compared to 20% in 2012. Of the 11 new ecosystems that made it to the top ecosystems list, six are out of Asia-Pacific.

Top 100 Emerging Ecosystem Ranking . Source: Startup Genome

The report noted that the ranking is primarily driven by one question: In which ecosystems will an early-stage startup have the best chance of building global success?

To determine this, the report based its findings on key broad areas:

Ecosystem Value:

A measure of the economic impact of the ecosystem, calculated as the total exit valuation and startup valuations over a two-and-a-half-year time period.

Exits

The number of exits over $50 million and $1 billion, as well as the growth of exits.

Startup Success:

How much startups succeed in the ecosystem. Measured in early-stage success (ratio of Series B to Series A companies), late-stages success (ratio of Series C to A companies and number of billion-dollar club startups), and speed to exit (both to IPO and other exits)

Using these, it found that:

Silicon Valley remains the top performer in value creation and exits, with ecosystems like Boston, London, New York City, and Beijing also performing strongly.

Chinese ecosystems do exceptionally well in the measurement of Startup Success, showing how Chinese startups are able to move onto the next stage of funding with relative ease — for instance, going from Series A to B.

São Paulo, Salt Lake-Provo, and Delhi punch above their weight in translating successful startups into subsequent high valuation funding rounds.

The report adopted Steve Blank’s definition of a startup as a “temporary organization in search for a repeatable and scalable business model,” thus discounting the notion that a startup must necessarily be technology-driven.

Why Egypt’s Cairo Was Ranked First In Africa

The report noted that Cairo was ranked Africa’s top emerging startup ecosystem because Egypt has 95 million mobile users, the highest penetration in Europe, the Middle East and Africa, including 14 million e-wallets, a young population and several government initiatives aimed at financial inclusion. In 2019, Fawri, a local e-payment provider, filed for an IPO after processing 1 billion transactions worth $3bn. Cairo has several fintech accelerators and funds, including the Central Bank of Egypt’s $58 million fund and Disruptech’s $24 million fund.

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

The exact amount raised by African startups from venture capital funding in 2019 continues to be an object of controversy. While this report by WeeTracker shows startups in Africa raised $1.3 billion in VC funding in 2019, another report from Partech Africa says 243 African tech startups raised a total of US$2.02 billion in 2019. Added to the growing list of reports (which, by the way, have unanimously established that startups in Africa did cross the $1bn mark in VC funding in 2019) is this newest report from the association that unites all private equity and venture capital organisations in Africa, African Private Equity and Venture Capital Association. The association’s latest report says about $1.4bn was invested in VC deals in Africa in 2019 across 139 deals — double the value of 2018.

“Despite the relative infancy of the entrepreneurial space in Africa, a culture of entrepreneurship is growing across the continent.

In recognition of the importance of entrepreneurship for economic development, job creation and poverty reduction, various national governments have also begun to implement supportive public policy to streamline business regulation for start-ups and small businesses.

Tunisia and Senegal have both passed Startup Acts to create a better local environment for innovation and entrepreneurship, and startup legislation is also being pursued in Mali, Ghana, and Rwanda. As Africa’s VC ecosystem expands, the actors operating within the industry are also diversifying,” the Association noted in the report.

The report noted that fintech and IT deals dominated the African startup scene accounting for 19% of the total volume of VC deals done between 2014 and 2019.

Both sectors were followed by consumer discretionary (18%) and industrials (12%), while communications services, healthcare and consumer staples collectively account for just 19% of the volume of VC deals over the same period.

Which Countries Are Receiving The Most Investments?

According to AVCA’s report, venture capital companies are investing more in Southern Africa, with the region attracting the highest volume of VC deals at 25%, followed by East Africa (23%) and West Africa (21%), while multi-region deals attracted the largest share by value.

South Africa’s well-developed VC ecosystem accounted for 21% of deals between 2014 and 2019, closely followed by Kenya (18%) and Nigeria (14%).

Here is a major indictment on the African startup ecosystem according to the report:

Even though all the startups that raised between 2014–2019 have their operational base in Africa, about one fifth (21%) of the total number of VC deals between 2014 and 2019 were in companies headquartered outside of Africa.

The report however noted that these early-stage companies with their headquarters outside Africa raised money to expand in Africa or further strengthen their African presence. Of these companies with headquarters outside Africa, the majority (53%) are based in the United States.

At Which Stage Of The Startups’ Development Are The Investors Investing More?

According to the report, investors are investing more at the seed stage of a startup than at other stages.

According to the report, nearly one third (32%) of the total number of early-stage investments reported in Africa between 2014 and 2019 were seed stage deals. These deals, however, accounted for only 5% of the total deal value, showing that while more investors were investing at the seed stage than at any other stages, they weren’t pouring in more in monetary sums into the startups compared to the amount invested at other stages.

Series A and Series B transactions together accounted for 29% of the total volume, and 38% of the total value of early stage deals.

The report also stated that there is a large number of deals in which the funding series are unknown, representing 34% and 29% of the total volume and value of total deals reported.

Another interesting fact from the report is that almost two-thirds (65%) of the total number of all VC deals in Africa between 2014 and 2019 were below US$5mn in size, while a quarter (25%) were between US$5mn and US$20mn in size.

Just 3% of the total volume of VC deals reported from 2014 to 2019 were above US$50mn in size.

For the first time, the report mapped comprehensively where VC investors to the African startup scene came from.

Quite alarming is the fact, according to the report, that North American investors represented 42% of the total number of investors that participated in VC investments on the continent between 2014 and 2019, followed by European based investors at 23%.

African based investors accounted for 20%, followed by Asia-Pacific (8%) and investors based in the Middle East (6%). This, perhaps, shows why the continent lags behind other continents in terms of funding available to its startups ecosystem.

The report also noted that a majority of the investors that took part in VC deals on the continent between 2014 and 2019 were US-based, representing 40%. South Africa (9%), Nigeria (4%) and Egypt (2%), which also constitute three of the most prominent VC hubs in Africa, were within the top 10 countries where investors that participated in VC deals on the continent from 2014 to 2019 are based, the reported noted.

The report also noted the growing interest from Middle East based investors on the African VC landscape. The United Arab Emirates, it noted, was amongst the top 10 countries where investors that participated in VC deals in Africa from 2014 to 2019 are based, representing 3% of the total number of investors.

Finally, the report noted that PE/VC Fund Managers (i.e. firms that have raised, or are currently raising, third-party PE/ VC funds from institutional investors), represented 39% of the total number of investors that participated in VC deals reported in Africa between 2014 and 2019, more than incubators, accelerators, non-profit organisation, family office, government agency, financial institutions or others.

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer.

Barring any last minute changes, all venture capital investors in Kenya, who get their funds from public funds, will have all their investment into Kenyan startups scrutinized under a proposed new amendment to the country’s Capital Market Authority law. This would affect venture capital firms’ operations especially those based in Kenya whose only access to funds is from public sources such as pension funds, etc. Also to be affected are private equity (PE) funds.

“In 2015, the investment guidelines under the retirement benefits regulations were amended to allow pension schemes to invest up to 10 per cent of their assets in private equity funds and venture capital funds which are licensed by the Capital Markets Authority (CMA). However, the Capital Markets Act was not amended to provide for regulations of these private equity and the venture capital. In this regard, I have proposed amendments to the Capital Market Act to provide for the regulation of private equity and venture capital companies by the Authority,’’ Kenya’s National Treasury Cabinet Secretary Ukur Yatani said in in his 2020/2021 Budget Statement before parliament.

Here Is What You Need To Know

Under the proposed amendment to the the Capital Markets Act (Cap 485A), Capital Markets Authority in Kenya will, once the bill is passed into law, now be authorised to license, approve and regulate private equity and venture capital companies that have access to public funds.

If the amendment is passed by Parliament, CMA will have the powers to scrutinise the books of firms that have attracted resources from public funds considering that pension schemes investments in PE firms has been on a growth trajectory in recent years. Kenya has allowed PE firms to fund raise from pension schemes after amending the Retirements Benefits Authority (RBA) Act allowing schemes to invest up to 10 per cent of their assets in the firms.

The firms through their lobby group, the East Africa Private Equity and Venture Capital Association (EAVCA), have since gone ahead to oppose the proposal to be regulated by the CMA on the basis that it will amount to “overregulation” given that pension schemes are regulated by Kenya’s Retirement Benefits Authority (RBA).

“If the proposal is passed PE firms will not have the incentive to raise funds locally from pension schemes,” said Eva Warigia, EAVCA executive director.

The new law will definitely be life-changing for startups in Kenya, given that Kenya has always attracted a majority of all startup investment in the whole of Africa. In fact in 2017, Kenya was only second to South Africa in terms of total startup funding in Africa by country (a staggering $147 million). The regulation proposed for the Capital Markets Authority of Kenya, over venture capital and private equity funds having access to public funds, by the country’s government would mostly likely result in over-regulation as well as increase in fees and cost of doing business for the investment firms. This is especially as they are already playing in a risk-ridden sector. The bottom line of this could be migration to lower-risk countries like Mauritius or reduction in the number of investment deals concluded on Kenyan businesses by the firms.

From a public policy point of view, the proposal attempts to place a check on access to public funds as well as demand greater accountability on the use of public funds, especially where there could be instances of conflicts of interest in the management of resources by the investment firms. In December 2016, Kenya’s Retirement Benefits Authority then CEO Edward Odundo said Kenya’s pension industry would be KES1trn ($9.8bn) by the end of that month.

The new investment law in Kenya may make or mar investors’ willingness to increase the volume of their investment in Kenyan startups, since access to funds for investors is already being threatened.Image Source: Quartz Africa

One could nevertheless ask what the functions of Retirement Benefits Authority in Kenya are under the law establishing it. For one thing, Section 5(a) of Kenya’s Retirement Benefits Act already empowers the country’s Retirement Benefits Authority to regulate and supervise the establishment and management of retirement benefits schemes. It also vests in the Authority the powers to investigate a manager, custodian, trustee or an administrator who may have engaged in embezzlement, fraud, misfeasance or other misconduct in connection with activities related to pension fund administration in Kenya.

Perhaps the proposed new amendment to the CMA law aims to cast a wider net over all public funds in Kenya made available to private equity funds or venture capital firms in Kenya, and not pension funds alone.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer.