Startups have enjoyed a bull run in the last decade with record highs across the board. After all, some of the biggest tech companies in the world have breached the trillion-dollar market capitalization in the last few years (Apple, Microsoft, and Alphabet).

However, with COVID-19 and oil wars escalating, the markets took a turn for the worst with the DOW dropping a sharp 2000 points, one of the worst days of trading since 2008.

Many believe that this could mean an upcoming recession or downturn that has been forecasted years ago.

But with all this news, what will happen to startups?

When you put startups and recessions together, the first thing you usually assume is a whole bunch of negative things due to risk and volatility.

But this isn’t entirely true.

Let’s go through some scenarios related to startups and funding.

Amount of Angel & Seed Deals Remain Constant

In a downturn, one of the first things expected is startups getting less funding opportunities in the market, especially for early-stage ones.

Looking at historicals, however, the most surprising thing is the number of deals angels and seed investors made during the global financial crisis (GFC) remained constant and actually rose.

As seen above, following the dark navy line, you can see an increase in deals over the GFC period since 2007.

But why would this occur?

One of the biggest reasons that this could be the case are angels, and seed investors generally have much riskier profiles. This means they are willing to take a bet for a higher return so if they don’t think a recession would put the startup out of business, there is no reason not to make an investment.

Additionally, angel investors usually invest in a specific startup as they believe in the product itself due to a personal reason or if they have directly seen the pain point themselves.

The factor that did change, however, was the investment amounts.

During the GFC, the amount an angel or seed investor put in did decrease, which probably indicates some risk management measures, as seen in the graph above.

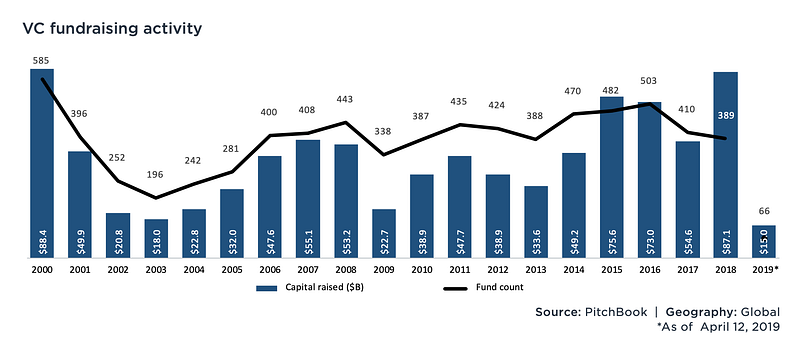

If you think about how VC funds like Andreessen Horowitz, Benchmark, Index Ventures, and Sequoia Capital raise significant amounts, it’s done so by pooling large amounts of money from investors.

Typically, these funds raise approximately every few years and, in recent years, have been successful in raising record amounts.

In a downturn, however, as investors become more risk-averse, their willingness to invest decreases.

As seen in the graph above, the significant years to look at are 2000–2001 (2000 stock market crash off the .com bubble) and 2008–2009 (GFC). Both periods of time had major crashes, and both showed huge drops in capital raised from a VC fund point of view.

Subsequently, this scenario will most likely play out again.

This will result in VC funds having less money, which means bad news for startups overall.

This means Venture Capital will be harder to access, and the following might occur for startups:

Startups are forced to give out more equity during rounds

Rounds might become smaller than historical averages

Valuations for a company might be smaller

Startups need to prove themselves, even more, to get funding (be profitable from early on)

Early Stage Startups — Are You Default-Dead?

Typically, anything at a Series A or prior may struggle to keep afloat during a recession.

As businesses cut costs, startups may find it hard to get deals inside the door, especially as companies cut budgets.

This includes the ability to raise subsequent rounds at a large enough scale to support the startup.

The concerned startups, however, are ones that need to raise more money to survive. These are startups that are not profitable yet, and if they cannot get access to cash, this could mean potential bankruptcy and closing shop.

These startups are what Paul Graham coins “default-dead” startups.

“Assuming their expenses remain constant and their revenue growth is what it has been over the last several months, do they make it to profitability on the money they have left?” — Paul Graham

This doesn’t necessarily mean these startups stay ‘dead’ forever as many need to reach a specific scale before switching the dial to turn profitable.

Many of these startups need to generate enough growth and worldwide coverage (think of your Ubers, Airbnbs, etc.) and are more likely within a non-software play.

However, since there is now a possibility of a recession, time is more limited for these startups to reach that point of profitability.

Some of these were massive giants that took in billions (WeWork!) and remained default-dead to this very day.

This means it’s never been so important to become lean and turn the profitability switch to remain in business, especially as an early-stage startup.

It’s not all bad news though

Just as some investors are waiting to buy-in during a dip, there are similar opportunities within the startup world.

For later-stage or well-funded startups, recessioncan be a golden opportunity to buy out competitorswho may be struggling.

Other things also become cheaper such as office space (especially during this coronavirus period) as well as travel expenses.

Businesses within specific spaces such as collaboration also have opportunities to expand within the current market.

The most redeeming note, however, is, there were still many startups that became huge unicorns from the last recession in 2008.

Here is a list from 2008 and 2009:

2008:

Airbnb (private; $38B, 2019)

Pinterest (public; $14B, Oct 2019)

Cloudera (public; $2.5B, Oct 2019)

Beats (acquired by Apple for $3B in May 2014)

Yammer (acquired by Microsoft for $1.2B in July 2012)

2009:

Uber (public; $54.6B, Oct 2019)

Square (public; $26.9B, Oct 2019)

Slack (public; $12.5B, Oct 2019)

Nutanix (public; $4.9B, Oct 2019)

From this list alone, we can see that even if a recession does occur, it doesn’t stop startups on the road to being a unicorn.

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

He could be contacted at udohrapulu@gmail.com

Here is a note that we sent to Sequoia founders and CEOs today to provide guidance on how to ensure the health of their business while dealing with potential business consequences of the spreading effects of the coronavirus.

Dear Founders & CEOs,

Coronavirus is the black swan of 2020. Some of you (and some of us) have already been personally impacted by the virus. We know the stress you are under and are here to help. With lives at risk, we hope that conditions improve as quickly as possible. In the interim, we should brace ourselves for turbulence and have a prepared mindset for the scenarios that may play out.

All of you have been inundated by suggestions for precautions to take around COVID-19 to protect the health and welfare of you, your employees, and your families. Like many, we have studied the available information and would be happy to share our point of view — please let us know if that is of interest. This note is about something else: ensuring the health of your business while dealing with potential business consequences of the spreading effects of the virus.

Unfortunately, because of Sequoia’s presence in many regions around the world, we are gaining first-hand knowledge of coronavirus’ effects on global business. As with all crises, there are some businesses that stand to benefit. However, many companies in frontline countries are facing challenges as a result of the virus outbreak, including:

Drop in business activity. Some companies have seen their growth rates drop sharply between December and February. Several companies that were on track are now at risk of missing their Q1–2020 plans as the effects of the virus ripple wider.

Supply chain disruptions. The unprecedented lockdown in China is directly impacting global supply chains. Hardware, direct-to-consumer, and retailing companies may need to find alternative suppliers. Pure software companies are less exposed to supply chain disruptions, but remain at risk due to cascading economic effects.

Curtailment of travel and canceled meetings. Many companies have banned all “non-essential” travel and some have banned all international travel. While travel companies are directly impacted, all companies that depend on in-person meetings to conduct sales, business development, or partnership discussions are being affected.

It will take considerable time — perhaps several quarters — before we can be confident that the virus has been contained. It will take even longer for the global economy to recover its footing. Some of you may experience softening demand; some of you may face supply challenges. While The Fed and other central banks can cut interest rates, monetary policy may prove a blunt tool in alleviating the economic ramifications of a global health crisis.

We suggest you question every assumption about your business, including:

Cash runway. Do you really have as much runway as you think? Could you withstand a few poor quarters if the economy sputters? Have you made contingency plans? Where could you trim expenses without fundamentally hurting the business? Ask these questions now to avoid potentially painful future consequences.

Fundraising. Private financings could soften significantly, as happened in 2001 and 2009. What would you do if fundraising on attractive terms proves difficult in 2020 and 2021? Could you turn a challenging situation into an opportunity to set yourself up for enduring success? Many of the most iconic companies were forged and shaped during difficult times. We partnered with Cisco shortly after Black Monday in 1987. Google and PayPal soldiered through the aftermath of the dot-com bust. More recently, Airbnb, Square, and Stripe were founded in the midst of the Global Financial Crisis. Constraints focus the mind and provide fertile ground for creativity.

Sales forecasts. Even if you don’t see any direct or immediate exposure for your company, anticipate that your customers may revise their spending habits. Deals that seemed certain may not close. The key is to not be caught flat-footed.

Marketing. With softening sales, you might find that your customer lifetime values have declined, in turn suggesting the need to rein in customer acquisition spending to maintain consistent returns on marketing spending. With greater economic and fundraising uncertainty, you might even want to consider raising the bar on ROI for marketing spend.

Headcount. Given all of the above stress points on your finances, this might be a time to evaluate critically whether you can do more with less and raise productivity.

Capital spending. Until you have charted a course to financial independence, examine whether your capital spending plans are sensible in a more uncertain environment. Perhaps there is no reason to change plans and, for all you know, changing circumstances may even present opportunities to accelerate. But these are decisions that should be deliberate.

Having weathered every business downturn for nearly fifty years, we’ve learned an important lesson — nobody ever regrets making fast and decisive adjustments to changing circumstances. In downturns, revenue and cash levels always fall faster than expenses. In some ways, business mirrors biology. As Darwin surmised, those who survive “are not the strongest or the most intelligent, but the most adaptable to change.”

A distinctive feature of enduring companies is the way their leaders react to moments like these. Your employees are all aware of COVID-19 and are wondering how you will react and what it means for them. False optimism can easily lead you astray and prevent you from making contingency plans or taking bold action. Avoid this trap by being clinically realistic and acting decisively as circumstances change. Demonstrate the leadership your team needs during this stressful time.

Here is some perspective from our partner Alfred Lin, who lived through another black swan moment as an operating executive:

“I was serving as the COO/CFO of Zappos when I was summoned to Sequoia’s office for the infamous R.I.P. Good Times presentation in 2008, prior to the financial crisis. We didn’t know then, just like we don’t know now, how long or how sharp or shallow of a downturn we will face. What I can confirm is that the presentation made our team and our business stronger. Zappos emerged from the financial crisis ready to seize on opportunities after our competitors had been battered and bruised.”

Stay healthy, keep your company healthy, and put a dent in the world.

Best,

Team Sequoia

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

He could be contacted at udohrapulu@gmail.com

It’s wonderful you’re considering an investment in a startup! As a VC who might invest after you, I’d like to share thoughts that may help — especially if you’re in a newer startup market where there are fewer experienced angel investors to offer guidance.

Roy Bahat, the Head of Bloomberg Beta

You’ve succeeded in other walks of life, so you might read this and think, “Who is he to tell me what to do?” I’ll make my best case — feel free to ignore me!

Fact: You will probably lose your money in this company. In almost every case, no amount of “structuring” or “risk mitigation” can protect you. The mythical profitable business that still needs your money and can also grow to enormous size is… rare. This startup you’re considering investing in probably isn’t it.

Naive angels worry about salvaging money from their losing investments — that is, “fixing the dogs.” It’s a fool’s errand (though supporting a founder emotionally during tough times is important). Experienced angels worry about keeping the upside by investing at a reasonable valuation so the winners actually make up for the losers.

2. Diversify

We only know one way to reduce your risk: take many bets. You probably need to invest in ~10 companies before you feel like you are getting a handle on things, and ~20 before you have good odds of earning a return.

3. Resist the urge to get cute with the deal terms

Yes, a shopping mall might thrive because an investor inserted a thoughtful covenant with the lender. Investments with known business models and predictable markets are just different than startups, which are defined by their search for a lasting business model.

Specifically avoid guaranteed returns (other than protecting your capital with the standard 1x liquidation preference), milestone-based valuations (complicated and perverse incentives!), extra control provisions (like a veto right on a sale when you are investing $10,000), options on the next round (other than the standard pro-rata), pre-negotiated sales before everyone gets liquid.

Quirky terms rarely survive, anyway. Later investors force their removal as a condition of investment. Sometimes, these terms even kill a startup because the cap table is too hairy for a good investor to wrestle with it. In startups, even more so than in life generally, simplicity wins, complexity kills, and the road to dissolution is paved with good intentions.

If you want a “deal” (that is, especially good terms), just be transparent and argue that you deserve it. Offer a lower valuation or valuation cap. If another investor will invest at a $3 million valuation and you will only invest at $2 million, tell the founder why you are worth more dilution.

4. Pay a market price (and avoid overpaying)

Know the market price for startups at different stages. Experienced angels know that by overpricing the initial valuation they actually may hurt the company — by hindering future fundraising. Down rounds can ruin businesses.

5. Control your urge to be in control

Startups with less investor control seem to outperform those with more. Startup investments run on trust. If you trust the founder, there are few areas where you’ll need special terms in the documents. If you don’t trust the founders, no special terms can save you.

6. Use standard startup documents

There are many standard forms you can use — like Series Seed if you want equity, or SAFEs if you want something else. These are tried and tested, and the only successful modifications we see come from experienced startup investors. Our fund even published the documents we use — including an explanation of the major terms.

If you are using convertible notes, find an experienced startup investor that has a standard note document without any unusual terms and copy their note.

7. Get the startup an experienced startup lawyer

Yes, you have your trusted firm with which you’ve done dozens of deals, and they have “startup” experience because they’ve incorporated new companies and negotiated private investments. And you trust your sister-in-law with your will and real estate. But startups are different. If you were arrested on a DUI, would you call your brother the tax lawyer to represent you? Use an expert — it matters.

The company’s lawyer must also be independent. We’ve seen cases where an angel thinks they’re doing a company a favor by setting them up with the investor’s lawyer. “We’re all friendly.” Good startups develop the habit of taking their own counsel.

8. Be fast and light

Know if you are willing to be the first investor, or if you want safety in numbers, and be clear about which you are willing to do. You can create damaging ambiguity hanging around the hoop.

Match your diligence to the size of your check and the stage of the business. Asking a day-zero company for five-year financials is a waste of their time and will provide no real information for you. Most experienced angels decide on investments of up to $100,000 in a meeting or two at most (though they often do substantial work calling references or validating assumptions with customers, etc.).

If you do too much diligence, you’ll end up with lemons. Good companies eventually have options. If you spend six months kicking the tires for a $10,000 investment, the startups who wait around for your company-proctology are more likely to be duds.

After you invest, asking the founder to report to you too frequently will only tax your own chances of success — “you can’t grow the pig by weighing it every day.” Imagine if every investor who had less than 5% of a business wanted a weekly update in person. (And, founders, if you want investors to be ready to help you and to stay off your back, then it’s on you to provide them regular updates — monthly is the default though quarterly is fine as long as you include real data about the important metrics.)

9. If you want the founder to respect your experience, you need to respect the limits to how widely your experience applies

Copy editing the founder’s website as a condition of making an investment is… probably a bad idea.

Maybe some of your experience bootstrapping a small manufacturing company in the early 1980s is relevant to an A.I. company in 2018 — most is probably stale. Business experience gets old like milk, not aged like wine. Explaining to employees that you’re going to miss payroll: relevant. Pontificating on which apps you think twentysomethings want: less so.

10. Your time is valuable, too

Think like a medic on the battlefield: triage. Spending half your week on the company that’s not going anywhere is a bad use of your time. Ironically, helping portfolio companies is time-efficient if you control your instincts — founders are the busiest professionals alive! The five minutes you spend crafting one email for your best company to get an intro to one big customer — that’s the stuff that matters.

I’ve seen the movie of startup investing more than 100 times and I believe these principles are in your best interest. The best-performing startups tend to have angels who are experienced and easy. In fact, those angels (especially those who founded startups themselves) are often the most valuable investors on the cap table (even more than, capitalism forbid, us “professional” VCs).

If you want to see and get into the best startups, recognize that this deal probably isn’t it — and your reputation with founders will shape how many deals you see and win in the future.

So treat the founders right, and we’ll all do better together.

Best, A seed VC

Roy Bahat is the Head of Bloomberg Beta, investing in the best startups creating the future of work.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

He could be contacted at udohrapulu@gmail.com

It’s the feedback that has shattered the dreams of many founders. That moment when an investor says: “You’ve got a great business, an innovative idea, you’re a passionate visionary with huge potential … but I need to see traction before I write a cheque.”

Benjamin Chong, partner at venture capital firm, Right Click Capital.

Traction is the difference between the success and failure of a business, and the ability for a founder to secure the funding they need to take the business to the next stage. It is a deal maker, and a deal breaker, for investors.

So what is traction?

Traction is momentum. It is a measurable set of customers or users that allows a founder to demonstrate their big idea is more than just an idea; it is a viable business and the founder is on the journey to product-market fit.

It demonstrates they have established evidence there is a sizeable market for the product, and there are green shoots of sustainable growth.

A startup doesn’t even need to be profitable to demonstrate traction. Instagram had a large customer base before it was able to experiment with ways of monetising this rapidly expanding user base. It had enough traction to persuade investors to part with their money even without clarity on how it would eventually make money.

Measures of traction will differ based on a startup’s business model and they are dynamic, changing throughout the life stage of the business. Early stage startups are still very much trying to show people will use an app that finds dog walkers in their neighbourhood. Later stage businesses need to show dog owners are willing to pay for this convenience regularly and love the idea so much they will recruit other pet lovers.

Early stage startups should start by defining relevant metrics

Founders first need to know the traction metrics for their startup. This isn’t always straightforward.

The easiest way to get a handle on these numbers is for founders to spend time engaging with potential customers, often referred to as customer development. Founders should be looking to talk to everyone who signs up, hold their hand, bring them on board as advocates and, of course, talk to them about the benefits of becoming a paying customer. This closeness allows the founder to see how customers might use the product, the application the new product is replacing and how the customer themselves measure the use of the product.

A founder recently pitched to me an exciting new business in healthcare technology that allows GPs to reduce the time spent on certain types of consultations. As an investor I was looking to understand how doctors value the efficiency this product brings and the impact on their profitability. I wanted to know if the doctor uses the technology ten times a day and it allows them to claw back time to treat an additional 20 patients every week. Or is this is a relatively infrequent request where time savings due to technology have little impact on the doctor’s ability to see and bill more patients?

Most importantly, I wanted to know the feedback from doctors and if this easily translates into actual sales for the founder. This is the product-market fit that is vital in early stage traction and shows the founder can convert the first wave of users to paying customers because they value the product.

Metrics for more mature startups

A mature startup will have a good understanding of the lifecycle of the customer, whether their pricing is right and whether there is elasticity in this pricing. They will know how much they can they charge for the product and how long they can keep the customer for, as well as having rich insights into customer behaviour.

The metrics used for measuring traction of later stage startups become more standardised. For a mature software app for instance, investors will want to understand the behaviour of existing users. Specifically, they will be looking at the daily, weekly and monthly usage patterns of users. Of the 100 users who open the app in a month, what is the percentage who open the app every week and what percentage open it every day?

Founders of these later stage startups should benchmark their vital user stats against a relevant peer. For example, WhatsApp has a daily average user (DAU) to monthly average user (MAU) ratio of 70%. This means that of 100 users who open WhatsApp in a month, an average of 70 users will open it on a daily basis. This is a high-water mark! For the same measure, Facebook sits at 66%. For a restaurant booking app, founders may consider how often, on average, people visit restaurants and use this to adjust their benchmark.

There are also metrics such as new monthly customers, customer churn rates, and viral or user coefficient measures (for every one person that signs up, how many will they get to join?) that will demonstrate traction. Session length and the number of installs are additional measures, and, naturally, revenue trajectory is also of great interest.

Generating traction is challenging at any stage of the startup journey but eventually traction turns to growth, which is a universal language.

For those founders who are seeking initial funding, having passion in the product, knowing the market, plotting a pipeline, and building an early fan base that demonstrates paid conversions, are what makes traction evident and attractive for potential investment.

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

He could be contacted at udohrapulu@gmail.com

A new report from DocSend, a cloud-based document sharing startup that specializes in things like pitch decks, found that institutional venture capital is trickling down into pre-seed funding rounds that often come in the earliest days of a company.

DocSend CEO Russ Heddleston

“Pre-seed isn’t the new seed,” DocSend CEO Russ Heddleston said in an interview. “We are seeing that, for a particular range of companies, there is a logical range of money you need if you aren’t wealthy enough to prove out the metrics to prove out the company. It’s a formalization of the angel round.”

The report looked at pitch decks of 174 startups that self-identified as pre-seed stage and sent pitch decks to investors via DocSend. The startup’s software tracks how many times an investor opened the files, how long they spend reading the deck, and which parts of the deck they spent the most time reviewing.

These are the 9 key milestones DocSend found could make or break a startup in the earliest days.

Before Heddleston started DocSend, he created and sold a young company to Facebook. Now, entrepreneurs of all stripes ask his advice for grabbing the attention of major tech companies and Sand Hill Road investors — and his answer is to always have an MVP, or minimally viable product.

“Pre-seed isn’t pre-idea,” Heddleston said. “A lot of people who ask for advice tell me, I have this minimal viable PowerPoint, but the data says if you are going to raise $500,000, you need to have a product.”

According to the report, investors spend roughly 3 minutes reviewing a deck but spent a majority of that time looking over product slides. This is the opposite of what happens in later stages of fundraising, Heddleston said, because investors assume founders have figured out product-market fit if they have achieved specific revenue goals.

On the flip side, it’s a bad sign if investors gloss over the product and get hung up on the business model, Heddleston said. That should be less of a concern at earlier stages because the team has yet to figure out what exactly the business will look like.

The pitch deck looks and feels like something from a more mature company.

Investors are creatures of habit, Heddleston said, and will often expect every startup they meet with to present roughly similar decks. So even though a pre-seed company will have fewer data available, the general format of the presentation should roughly mirror that of a later-stage company.

“The companies that are on the West Coast organize their decks in a more standard way,” Heddleston said. “Maybe they have a friend that raised money or an investor or an advisor that could help.”

None of the 174 startups in the study had the exact same presentation format. But all West Coast companies did include dedicated slides to the problem they wanted to solve, what the solution was, and who was part of their team. Startups in other geographies might not have the same network to know what is expected of their pitch decks, Heddleston said.

The deck is edited down to roughly 12 slides from 20 slides.

The report found that investors spend a little over 3 minutes, on average, reviewing pitch decks that were sent to them by founders. The average pitch deck, however, is about 20 slides, meaning that investors are spending about 9 seconds on each slide. Heddleston said the discrepancy highlights how important it is for entrepreneurs to be concise in their decks.

“People don’t spend a ton of time reading these things,” Heddleston said. “Don’t write an entire novel. Manage the content and manage the time you spend on it.”

Successful pitch decks included 12 distinct slides, the study found. Those include things like problem and solution, but also more nuanced points like why investors should back a company now and what future traction might look like.

Your pitch deck includes a “Team” slide.

Of all the slides to include, Heddleston thinks including a “Team” slide is often the most overlooked but can be the most important. This is especially true of teams that are not located in Silicon Valley, and are less likely to have met potential investors in person.

“I can’t invest in a company that doesn’t have any people,” Heddleston said.

In all, just 89% of startups in the survey opted to include the slide, although all West Coast companies had it. The larger disparity among startups outside Silicon Valley means there might be a lack of clarity about what investors are looking for.

“Uncertainty is a killer for people going through this process because they don’t know if they are doing okay or not,” Heddleston said.

The team can be flexible enough to incorporate feedback from investor meetings to address questions proactively in later meetings.

One of the biggest differences between pre-seed funding rounds and angel rounds is how many meetings founders typically have, Heddleston said. With angel networks, there are only a handful of meetings before angels tend to invest because they likely already know or have met the founder before.

With an institutional round, founders might have to cast a significantly wider net. The report found that founders will take roughly 26 investor meetings, on average, before closing the round. But more isn’t always better, Heddleston said.

“Some people think it’s better to pitch more, but there are diminishing returns,” he said. “If you give 30 pitches and you get 30 ‘nos,’ it’s time to change something. Don’t do 30 more pitches.”

Even two meetings that provide similar feedback is enough to make founders stop and think about changing things up, Heddleston said.

There’s enough initial capital to outlast roughly 20 weeks of fundraising meetings.

Compared to later funding rounds, a pre-seed check might seem like chump change with a typical max amount hovering around $500,000. But that doesn’t mean investors will skip doing diligence on the investment, and usually means the round takes longer to close than those down the road.

“It’s the most painful round of funding for a company,” Heddleston said. “Every round of funding is easier than your pre-seed.”

He advises that founders have enough capital on hand to outlast the average 20-week fundraising process to avoid any kind of financial crunch. Even then, the report found it takes about 3-and-a-half weeks for the funds to land in the company’s bank account after the round is officially closed.

“People assume it’s really easy, but it takes forever,” Heddleston said. “People don’t budget time correctly for the pre-seed round.”

Be ready to give up at least 10% of the company to outside investors, or be prepared to take a valuation cut.

Many founders want to optimize for the highest valuation possible, Heddleston said, but it’s not always the right decision out of the gate. Typically, investors seek 10% ownership of the company with pre-seed funding rounds and value the startup accordingly. Founders will also set aside another 10% for an employee option pool to start hiring in earnest.

“People try to optimize that, but really they should just focus on getting the amount raised and get back to work,” Heddleston said.

He said that entrepreneurs that are building a highly valued company can easily see higher valuations in later rounds once they have revenue and other hard metrics to show. If they are overly concerned with ownership, he advises holding out until the seed round if possible.

“Otherwise, just don’t stress about it,” Heddleston said.

You’ve brought on cofounders, or asked larger founding team members to step down.

Although single founders are not at all uncommon, the report found bringing on a cofounder can help increase the pre-seed round size itself and help cut the number of investor meetings. But Heddleston advises against bringing on more than two additional cofounders.

“You get diminishing returns after 3 founders,” Heddleston said.

Investors hesitate to work with larger teams because they’ve seen hundreds of startups fail because of conflicts among founders. So the rational thinking goes, the more founders, the higher chance of conflict.

“You can’t have 5 founders because you can’t all be equal,” Heddleston said. “It comes down to, which of you will be booted off the island and how quickly.”

The startup has a consistent narrative

But at the end of the day, nothing else matters as much as the story founders want to tell to investors, Heddleston said. It is one of the easiest parts to overlook because founders are knee-deep in the trenches of building a company, but they often struggle to effectively communicate what it is they are trying to build.

“You need to convince someone you can build and run a billion-dollar company,” Heddleston said.

One of the most effective ways to do that is to include a “why now” slide, according to the report. It can help provide context, highlight current technical shortcomings, and explain market conditions that are ripe for growth in ways that a competitive landscape graph can’t.

“How to craft a great narrative is not something you can automate,” Heddleston said. “It’s hard to create that from scratch. It’s like a great song. I can tell you if it’s a catchy song, but it’s not like I can go make a catchy song myself.”

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

He could be contacted at udohrapulu@gmail.com

Founders, companies, and investors are rebelling against the investment banks — and taking matters into their own hands

Mike Hofman, writer and editor, New York

By all accounts, 2019 was a terrific year for the stock market, with the Dow Jones Industrial Average rising by more than 22% and the S&P 500 up nearly 29%. But even as a broad range of businesses fared well in 2019, one specific category proved to be a decidedly mixed bag, and it was a surprising one at that: companies that were on the verge of going public.

Though the Renaissance IPO Index ended the year up 35%, beating the broader market, investors, underwriters, and entrepreneurs are left feeling walloped. That’s because a number of headline-grabbing misfires dampened enthusiasm for initial public offerings of stock. WeWork’s yanked IPO was the most high-profile example of trouble, but there are others. Endeavor, the sports, fashion, and talent conglomerate once valued at $7.8 billion, pulled its planned IPO due to a lack of support, as did Postmates, the delivery service, which is now said to be seeking a buyer.

Meanwhile, the companies that did make it out found the public-market terrain to be fairly brutal. Once-celebrated unicorns such as Uber, Lyft, Peloton, and Pinterest went public only to struggle to generate investor enthusiasm. And B2B player Zoom, the videoconferencing software company, which had a juicy pop of 72% on its first day of trading, has seen its fortunes seesaw, falling from a high of $102 to roughly $88 at press time, even as the broader market, especially the tech sector, has been on a tear. Even Saudi Aramco, the oil-and-gas colossus that went public in Riyadh on December 11 and instantly became the world’s most valuable company, is said to have fallen short of the Saudis’ expectations that it should be valued at $2 trillion.

It is unusual to have a year when the stock market did so well overall, while the market for private companies going public proved to be punishing, particularly for the best-known startups.

All told, the 159 companies that went public in the U.S. in 2019 raised $33 billion, according to PitchBook, down nearly 30% from 2018.

And more recently, unicorn mattress-maker Casper, which had its IPO in February, ended up slashing its offering price before going public with a market cap of less than $500 million, well below its $1.1 billion pre-IPO valuation.

How is it that the hottest growth companies have stumbled out of the gate? The IPO market is notoriously mercurial, of course, and often performs differently from the market as a whole. Still, it is unusual to have a year when the stock market did so well overall, while the market for private companies going public proved to be punishing, particularly for the best-known startups.

One could argue that this particular crop of companies is simply uniquely lacking for some reason, like a fumbly year in the AFC East or a dull season on Broadway. To be sure, more than a few IPO candidates in 2019 boasted — and were burdened by — extremely high, late-stage valuations despite lacking profitability. Uber, for example, was valued at $84 billion at its peak, while WeWork hit $47 billion at its imagined high point; neither firm has turned a profit, though Uber says that its core rides business would be profitable on its own.

Some observers argue that the market worked as intended, correcting for unrealistic optimism on the part of venture capitalists and private equity investors who poured millions into these businesses without fully interrogating whether the business models worked. But it’s difficult to prove that hypothesis, and, anyway, it might not matter. That’s because a growing chorus of entrepreneurs and venture capitalists are deciding that if the IPO market isn’t hospitable to their companies, there must be something wrong with the IPO market. More so than ever before there’s a move afoot to knock the chess board on the floor, scatter the pieces, and start fresh. “Sometimes we need a big shakeup in the system,” says Aswath Damodaran, a professor of finance at New York University’s Stern School of Business.

Led by Benchmark Capital’s Bill Gurley, these IPO skeptics are now looking to popularize the direct listing, an alternative avenue for a company to go public, selling existing shares rather than issuing new shares. They argue the process is streamlined and less regulated, and more democratic and entrepreneurial. They cut out Wall Street, provide greater flexibility to key stakeholders including equity-holding employees, and prevent the unnecessary dilution of private shareholders. After Spotify went public using a direct listing in April 2018, Slack used a direct listing to go public on the New York Stock Exchange in June, and Airbnb is said to be considering one as well.

Critics argue that direct listings are less rigorous than IPOs (in terms of due diligence and public disclosures) and therefore are ripe for abuse, creating more risk for Main Street investors and thereby possibly diminishing the integrity of the public markets. Now, a lawsuit in California involving Slack is placing the debate center stage — with Slack’s lawyers arguing that companies that go public through a direct listing should face fewer regulatory obligations. The outcome of the case could have huge implications for technology companies, Silicon Valley, Wall Street, investing in the stock market — and the very future of the IPO.

Last October, Benchmark’s Gurley invited a group of iconoclastic Silicon Valley personalities to meet at the Palace Hotel in San Francisco — best known as the site of ardent capitalist Warren G. Harding’s death in 1923 — to discuss the state of the IPO market. A hundred entrepreneurs reportedly attended the invitation-only event, as well as representatives from 25 venture capital firms, and more than 200 CFOs and other financial executives from technology companies. After spending a morning cataloging their gripes — from high fees to unnecessary dilution — the participants’ attitudes about the IPO process, and about Wall Street underwriters in particular, were as stone-cold as the 29th president.

“We’re not out to start a fistfight, we’re not out to vilify a particular bank,” Gurley told CNBC after the event. “There’s that old saying, ‘Don’t hate the player, hate the game.’ It may be that the game has changed in a way that all of these players are self-optimizing.”

Or, put another way, self-dealing. IPO critics have long resented the high fees charged by the investment banks such as Goldman Sachs and Morgan Stanley to underwrite an IPO. And given the recent travails of post-IPO companies, entrepreneurs and VCs are wondering what exactly those steep fees are getting them.

Gurley, for example, argues that the traditional IPO roadshow, during which Wall Street underwriters act as a high-class chaperone, bringing CEOs and CFOs from city to city to make their PowerPoint pitch to conference-rooms-full of large, institutional investors, emphasizes “anxiety and pageantry.” The actual market-building activity implied by underwriting adds precious little value, as banks rely on the same handful of clients to participate in each IPO they do. “Even in 2019 with a traditional IPO someone basically just got a list of accounts and how much they’re willing to give,” Gurley told author and well-known asset manager Patrick O’Shaughnessy on his podcast.

Many insiders have seen other investors reap big gains only to have their stock languish closer to the end of the lockup period.

And in exchange for this service, banks charge a fortune in fees. The typical underwriting fee in the U.S. is about 7%. “That’s a lot to take off the top,” says Robert Pozen, a senior lecturer at the MIT Sloan School of Management and the former executive chairman of MFS Investment Management. “Plus, there are lots of other expenses and if you don’t really need the money why should you do it?”

The capital markets have changed dramatically even as the IPO process has not. Historically, an IPO was the only way to raise a truly significant war chest for your company. But access to capital for private businesses has become much more abundant over the past 20 years. The cost of capital for a large Series D, E, F, or G round is often much lower than on a comparable amount drawn through an IPO.

One problem, of course, is liquidity. Absent access to public markets, it can be difficult for investors, founders, and early-stage employees to cash in their shares; there are some fledgling secondary markets for pre-IPO shares, such as SharesPost, EquityZen, Forge, and Cooley Go — but the volume on these exchanges is dwarfed by the public markets.

Once a company goes public, it can seem as if founders, employees, and early investors are needlessly constrained by arcane rules. That’s because company insiders are obliged to hold their shares for 180 days after an IPO is completed, a period known as the “lockup.” But given gyrations among recent IPO stocks, many insiders have seen other investors reap big gains only to have their stock languish closer to the end of the lockup period, in effect limiting their ability to profit from their contribution even as fair-weather latecomers make out handsomely. And then when the lockup does finally expire, insiders scramble to sell shares, making a weak stock even weaker. At Uber, for example, the day the employee lockup expired, the share price tumbled by 7%.

“The lockup is there to protect the retail investor,” says David A. Frankl, the managing partner at Founder Collective, an early-stage venture capital firm, with offices in Cambridge, Mass., and San Francisco. But critics argue that banks use the looming deadline of a lockup expiring to upsell companies on additional transactions.

“I think a lot of [Gurley’s] rallying is that as much as the lockup serves as a stabilizer, it’s another way of enabling more fees,” Frankl says. “You can do secondary sales to institutions in that period, for example, but there are lots more fees along the way.”

And then there are long-standing complaints about pricing in general. While the business media and many market watchers often celebrate a big, first-day-of-trading spike in share prices (see Zoom as a prime example), venture capitalists, entrepreneurs, and late-stage investors take a dimmer view. This phenomenon is known as underpricing, and it occurs when a Wall Street underwriter prices shares too cheaply, essentially failing to determine the latent demand for the stock and thereby undervaluing the company.

“The pop is the bone of contention,” Frankl says. “For an entrepreneur or late-stage investor, imagine if a company was priced at $20 and on Day One it closes at $40. The press has made it like the bigger the pop the better it is, but the entrepreneur is left thinking ‘I should have doubled the price per share.’ If everybody is feeling so good about themselves, they haven’t done the math.”

Besides not capturing cash that would have gone right to the IPO company’s balance sheet, VCs and other private shareholders in this scenario see their ownership stakes diluted much more than they had to be.

Underpricing is so common that Jay Ritter, a professor of finance at the University of Florida, has found that over the past 10 years, $171 billion in value eluded newly public companies and accrued to hedge funds and other Wall Street insiders in the first 24 hours following an IPO.

The phenomenon may be due to a misapprehension of the share price on the underwriter’s behalf, or it may be something less honorable — an instinct to manufacture a windfall for their own institutional clients. Distrusting Wall Street bankers is, of course, something of a national pastime. “The investment banks have been tarred, rightly or wrongly, by the financial crisis,” says Damodaran. “In the past, people thought the banks might not be the best, but at least they are good at pricing. That was the perception. But lately, the pricing has been so bad that it wiped away the last vestige of what people thought the banks were good for.”

“They are viewed as people who didn’t know what they were doing, which is bad,” Damodaran continues, “or they knew what they were doing and did it anyway, and that’s worse.”

With an IPO, large investors buy shares at an offering price, akin to a friends-and-family price for Wall Street clients that can sometimes be much less than the opening price — that is, the price at which shares begin trading on the public market. A direct listing collapses the gap between offer and opening price, which is in theory better for the issuing company but represents a lost opportunity for the banks.

And what if a stock falls on its first day? Yet another point of contention occurs with the so-called “greenshoe” option, which allows an underwriter to create an incremental number of shares (equal to 15%) on top of those a company plans to issue, which the underwriter can repurchase in the event the stock struggles at open. In theory, the banks can move in and stabilize a faltering stock by buying up shares, but in practice, Gurley asserts, they often treat this as an opportunity to maximize gains. In the case of Uber, Gurley says, the underwriter made an incremental $100 million on the greenshoe option. And in the Aramco deal, the greenshoe option likely netted well into the billions.

Enter the direct listing, in which a company sells existing shares — drawn from investors, founders, and employees — made available to the public for the first time. There’s no need for a traditional underwriter or a roadshow. There’s no lockup hamstringing employees, founders, or investors. The fees paid by the company are simplified and greatly reduced, with much less regulatory red tape.

In theory, the drawback is an inability to raise new funds. But with the rise of large, late-stage deals, a company can choose to raise money privately and then use a direct listing primarily to achieve public liquidity. “It is good to have an alternative way to go public for companies that have that kind of investor interest don’t have a need to raise a lot of cash,” MIT’s Pozen says.

For every hyped unicorn, there are plenty of unsexy companies that are as interested in raising money as they are in gaining liquidity.

Best of all, Gurley argues, the pricing dynamics of a direct listing are much more straightforward — essentially algorithmic, like the bond market or, for that matter, StubHub — in terms of matching sellers with buyers. “You could hire a programmer in Python, probably a first year out of a top 100 comp-sci program, and they could do it in a weekend,” Gurley said on Patrick O’Shaughnessy’s podcast. “It’s not hard technically and it’s not hard intellectually.”

Gurley asserts that long-term institutional investors are also able to build up a meaningful position in a company much more smoothly and efficiently once the underwriters are out of the picture, which would typically result in less volatility and more stability for the stock.

This is the rosy picture, of course. Skeptics say that the direct listing model, while attractive in its overall simplicity, isn’t a feasible replacement for an IPO. They argue that it only really works for high-profile companies that have raised a lot of money privately, and are already well known to institutional investors. For every hyped unicorn, there are plenty of unsexy companies that are as interested in raising money as they are in gaining liquidity. And for businesses that are not already staples of CNBC and the business press, the chance to tell their story through an organized roadshow does provide a meaningful opportunity to raise their profile in the investor community. “One reason you need banks is people don’t know who you are,” Damodaran says.

And though direct-listing proponents assert that the model derives a list price more accurately and fairly, others aren’t so sure. “With both Spotify and, more recently, Slack… the aftermarket has not been kind to the stocks,” Joe Nocera wrote in Bloomberg. “Which is to say, the direct listing mispriced the stocks — it was just a different kind of mispricing from a traditional IPO.”

Regulators at the Securities and Exchange Commission have so far signaled a wariness about moving too fast. A bid by NYSE to allow companies to sell not only existing shares to the public through a direct listing, but also to issue new shares, was rejected in December, though it will likely be reconsidered in 2020. More ominously, the Journal reported that the SEC is taking a closer look at activity on Slack’s first day of trading.

And now there’s the Slack lawsuit, which could complicate the drive to popularize direct listings even further. Filed by a group of individual investors in federal court in California, the suit alleges that Slack failed to disclose certain material risk factors as part of the direct listing process. This type of suit is garden variety, but what is unusual is Slack’s defense. In effect, the company is saying that because there was no IPO registration statement, there was no disclosure to hold it accountable for; Slack also says that because there was no original listing price, it would be impossible to establish damages.

It’s a high-risk, high-reward legal strategy. If Slack prevails, it will likely pave the way for more direct listings as companies see it as reducing their legal exposure. But by making the argument that it shouldn’t be held to the same standards as other public companies, Slack is all but inviting greater regulatory scrutiny.

When it comes to direct listings, the chatter so far has outstripped actual concrete action. But that may soon change. Between three and five companies, including Airbnb, could go public through a direct listing in 2020, according to the Wall Street Journal — spurred in part by VCs who are still haunted by the lackluster performance of 2019’s IPO class. If that comes to pass, look for tensions between Silicon Valley and Wall Street to rise, as the Valley looks to sweep away one of the most powerful leverage points bankers have in the entrepreneurial world.

“There is a very high-class rift between mainly the later-stage investors and Wall Street,” Founder Collective’s Frankl says. Adds MIT’s Pozen: “I’m sure that Wall Street is always made nervous by ways people can be successful without them.”

After years of being celebrated as the creative visionaries of the American economy, entrepreneurs in the Valley are generally feeling attacked.

But while VCs like Gurley are among the most vocal proponents of changing the system, keep an eye on the entrepreneurs. Ultimately, their willingness to stick with the traditional IPO process or try another approach will be decisive here.

And right now, they’re restless.

After years of being celebrated as the creative visionaries of the American economy, entrepreneurs in the Valley are generally feeling attacked — by policymakers and presidential candidates, privacy experts, regulators, Wall Street analysts, local officials, the press, and even their own employees.

“The mood — it’s beyond defensiveness,” says Margaret O’Mara, a professor of history at the University of Washington, and the author of The Code: Silicon Valley and The Remaking of America. “People in Silicon Valley are getting pushback, and they’re not used to that. In some cases, they’re in denial. They think, ‘Hey, we’re doing the right thing, and we’re just misunderstood.’”

In a unicorn entrepreneur’s world view, then, building a company to the point where it’s a viable IPO candidate should be rewarded. But as they watch the public drubbing suffered by the likes of Adam Neumann, Travis Kalanick, Away’s Steph Korey, and even Elon Musk, founders are more apt to see themselves as mistreated and even harassed by various gatekeepers. And they seem to be particularly vulnerable, like Neumann, in the run-up to an IPO.

Snapchat CEO Evan Siegel articulated what many entrepreneurs are no doubt thinking when he half-joked in an interview this fall that the one piece of advice he would give any ambitious founder is “Don’t go public.”

The word go is doing a lot of work there, providing a dissenting view to the axiom that the journey is the reward. In the world of IPOs, the journey — from being a late-stage, well-funded private company to becoming a public company — represents the annoying and potentially hazardous part of the great American entrepreneurial success story.

Companies generally want to be public — they want liquidity for early-stage investors, employees, and founders; they want to be able to acquire other companies; and they want access to growth capital. They want to see their ticker symbol crawl across the bottom of the screen on CNBC. They just don’t want to run a gauntlet to get there.

Mike Hofman is a writer and editor living in New York.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

He could be contacted at udohrapulu@gmail.com

Startups and established companies all face a dilemma when building new technology products. If they hit upon something innovative that has high potential, they invite the scrutiny of large technology companies such as Amazon, Google, Facebook, and Microsoft. Big Tech has the money, technology, data, and talent to replicate and enhance any technological innovation that is not fully protected by patents — which encompasses most digital products.

Thales S. Teixeira, co-founder of Decoupling.co, a digital disruption and transformation consulting firm

Recent episodes have shown this copycat behavior to be quite common and life-threatening to startups. The copying comes in various flavors. Sometimes tech giants simply copy innovative features. When Snapchat was doing well with stories that disappeared after 24 hours, for example, Facebook retaliated by introducing the same feature to its products, including Instagram and WhatsApp. Subsequently, Snapchat’s usership stalled. It has had trouble regaining momentum, and its stock price went down dramatically.

In more egregious cases, whole “form factors” (in Silicon Valley jargon) have been copied. After years of growing its user base at nearly 5% per month (!) Slack’s adoption rate has slackened and started to show signs of decline. The pivotal event? The introduction of Microsoft’s knockoff product, Teams. Microsoft did what it does best: waited to see signs of success (four years, in this case) then copied the offering and later integrated it into its other products.

A third approach is to copy a niche product. Allbirds acquired a cult following by developing a line of wool shoes sourced in an environmentally responsible manner. In response, Amazon copied the top-selling product almost point-for-point and sold it online for nearly half the price.

Despite this predatory behavior — and the resulting reluctance of some venture capitalists to invest — a few startups have managed to survive beyond their early stages and become sizable players in the same space as the tech giants. On the surface, it looks as if they succeeded due to luck or lack of interest on Big Tech’s part. In reality, though, these challengers succeeded by using the companies’ strengths against them. This strategic move, although counterintuitive at first, can lead to copy-proof innovation.

Consider Wayfair. Today it’s the largest online seller of home goods and furniture. Back in 2014, a Harvard case I co-authored described how the company had just merged more than 200 niche product websites into the Wayfair brand. When I spoke with its co-founder and CEO, Niraj Shah, it was clear that Amazon was the constant threat. Over the years, Wayfair had implemented many features that it had seen work for Amazon, and Amazon developers also copied features from Wayfair.

One thing that Amazon did not replicate — and that worked remarkably well for Wayfair — was taking its own pictures of and measurements for the furniture and home furnishings that it sold. This additional detail helped consumers visualize the home decor they were planning, and it helped Wayfair to differentiate itself and get traction. (Its five-year revenue growth has been an astounding 49% [CAGR], compared to Amazon’s 26%.) Yet, Amazon continued to show only the pictures provided by the manufacturer.

Why? I suspect it’s because Amazon has 3 billion items for sale, whereas Wayfair offers 14 million. The infrastructure and added cost that Amazon would require to take unique pictures of products is daunting, particularly given that more than half its sales comes from the marketplace listings that are managed independently by third-party sellers. And it’s not just about costs. To succeed with Wayfair’s approach, Amazon would need longer lead times for adding new products, reducing the speed of growth at the “everything store.” Plus, it would cause the website to load slower and be more visually cluttered. Amazon could have copied Wayfair, but it chose not to, as that was not in its own interest.

Zulily, which sells women’s and children’s clothing online, found another approach to competing with Amazon in a way that the giant retailer chose not to emulate. Amazon is relentlessly customer-centric: Shoppers tend to get lower prices, quicker delivery times, and great customer service. However, in retailing, catering to the shopper above all else comes at the expense of the supplier — and Amazon’s suppliers put up with a lot. Amazon routinely withholds or delays payment, often arbitrarily. Worse, it copies suppliers’ products and undercuts them, often putting the supplier out of business.

So it made perfect sense for Zulily to offer suppliers high-quality service, commit to volume purchases, and offer fair purchase prices. As a result of Zulily’s approach, many suppliers accepted exclusive supply deals with the startup instead of selling on Amazon’s much larger marketplace. This, in turn, allowed Zulily to offer novel and unique items not available elsewhere. The company grew revenues tremendously — from 2009 to 2014 at a CAGR of 161% — until it was acquired by Qurate, owners of QVC and HSN, in 2015 for $2.4 billion as one Harvard case study shows.

Outside of e-commerce, in its early days Dropbox took advantage of Microsoft’s massive enterprise software sales prowess. For years, Dropbox was a tiny startup with only a few dozen employees and no salesforce to sell cloud storage to enterprise CIOs and CTOs. Instead, Dropbox offers its service for free to individual consumers. As people adopted the service and it grew, Dropbox got this network of people to start using its product at work. Over time, those users lobbied their bosses, CIOs and CTOs, to purchase and offer Dropbox for Business, the subject of a Harvard case study. In other words, they used personal consumption as a Trojan horse.

This judo-like approach, in which a smaller challenger leverages the opponent’s larger size and strength, is promising, but it’s certainly not guaranteed to work or to be sustainable over the long haul. If they don’t copy you, the giant you’re challenging might opt to build a standalone competitor and still copy point-for-point what you built. That said, it’s generally easier to compete with a stand-alone spinoff than the “mother ship.” When TikTok offered a video-sharing app that allowed users to share music snippets, it appealed to younger users who thought Facebook was for their parents and grandparents, and it quickly grained traction. In response, Facebook launched a nearly identical stand-alone app called Lasso, which thus far has not gained traction.

Alternatively, Big Tech might simply attempt to acquire the threat. But that’s not guaranteed to succeed, either. Acquisition is sometimes very costly and increasingly it’s just not an option. Facebook did try to buy Snapchat and was denied. Microsoft did try to buy Slack without success. In these cases, it was the startup founders and investors that rejected the offers. Amazon, reputationally the least acquisition-prone of the Big Tech bunch, has historically preferred to develop in-house rather than acquire from outside.

I have been using this approach with the startups that I advise to various degrees of success. In order to leverage Big Tech’s strengths against them and avoid being besieged by copycat behavior, you will need to address these questions:

Does the opponent have a major strength that is predominantly responsible for its success?

Can you identify a product offering (niche, feature, or format) that a segment of customers value and the delivery of which is made harder by possessing the above-mentioned strength?

Would mimicking the novel offering somehow hurt the larger opponent’s main business?

If the product offering eventually has traction in the market, would the Big Tech opponent necessarily need to give up its strength to copy or compete?

If you can answer “yes” to these questions, then you too may have found a way to deter blatant copying and to succeed unencumbered. Of course, no single strategy can deliver an advantage forever. In order to thrive, constantly creating copy-proof innovation is essential.

Acknowledgement: Leandro Guissoni, Mark Hill, Greg Piechota and Hem Suri provided valuable suggestions for this article.

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

He could be contacted at udohrapulu@gmail.com

The story of a founder and co-founder who met remotely and ended up launching a startup

Dave Schools, a Cofounder at Hopin

Starting a business with someone is always an arduous process. There are contracts. There are differences in personal values and backgrounds. There are questions of trust, personality clashes, and sacrifices that have to be made.

But starting a business with someone you’ve never actually shaken hands with changes the game completely.

Given our virtually unlimited ability to meet people around the world in today’s global and tech-powered economy, it’s becoming less and less uncommon that two people in two different countries can come together and launch a business together.

Launching a business is different from remote hiring and contracting, which we know is a growing trend. See, employment is de-risked. The employer is stable and established (we hope). The employee or contractor receives a paycheck and/or benefits. Remote workers do a regular job, remotely.

Entrepreneurship has all the risk, with more unknowns, more pressure, and more work, and less pay, if any, at the start. And benefits? What are those?

Add in the dynamic of being fully remote and entrepreneurship can be uniquely challenging. If you think entrepreneurship is hard enough with a partner you’ve known for years, try it with a partner you’ve only just met on the internet who lives in another timezone.

Being a remote co-founder isn’t half bad

I’ve just gone through this process with my business partner Johnny and our company Hopin. It turns out it’s not that bad at all. In fact, it could be argued that remote entrepreneurship is easier than centralized entrepreneurship and as I mentioned before, we’re probably going to see more of it. Regardless, as with anything, there are pros and cons.

Today, Hopin is a team of 14 remote employees building version 2.0 of our live online events platform. But just like any new company, Hopin started at ground zero. It was just Johnny in London and later me in Richmond. Two years ago we were total strangers.

Have calls in the early mornings and late evenings — you’ll see different sides of each other.

How two strangers built a company together

Johnny is the founder, coder, and visionary behind our startup. He started working on Hopin in 2018 and built the MVP. I’m the writing, marketing, and sales Swiss Army knife who joined Hopin as cofounder in 2019.

The first time we met was via a typical introduction over email. I was interviewing the super-connector founder of a very large Slack community for an article and he fired off a number of quick one-line email introductions at the end of our phone call. One of them was to Johnny.

Johnny and I jumped on an initial video call. It was a typical what-are-you-working-on conversation that ended on a let’s-see-where-this-goes and stay-in-touch note.

A month later we hopped onto another video call. It was a typical check-in. We chatted about new updates from both sides. Good stuff. A couple weeks later, another check-in. A few weeks after that, another.

Each time we spoke, Johnny had made updates to Hopin and he asked me to test these new features with him. I was curious about the platform and I thought it would work well with my Medium publication’s audience. So I obliged.

Despite my blossoming freelance career, when Johnny asked me what I saw myself doing as a career in the long run, it dawned on me that I did not want to keep freelancing. Hopin was a product and a market I could plunge into with two feet. So after over a month of back-and-forth negotiating, we put our agreement into a contract in September 2019 and signed. I quit my client work completely and joined Johnny as his full-time co-founder.

I still had not met Johnny in person. As a commemoration of our agreement, I booked a flight to London the next month on my own dime.

It was mildly surreal to meet in person. When you have long and intense conversations with someone you’ve never physically been in the same room with — about family, worldviews, morality, health, and money — the relationship deepens. But then, when you meet that person for the first time in real life, there’s a palpable sense of starting over. We were physically strangers but familiar companions at the same time.

I spent five days in London. We worked, we went out to eat, we worked more. By the time I left, we were already talking about when I would return. Over the next few months up to today, it has continued to be a great match. Of course, we’ve not been without our disagreements, mistakes, and misaligned expectations, but at a core level, there’s something unassailable about our partnership, something that transcends the doubts and absence caused by distance. This has remained so as we’ve hired more people and the company has scaled.

How to be a successful remote co-founder

If I were to put my experience into some takeaways for others who are looking to do the same thing, I’d say this about starting a business with someone you’ve never met:

Put in the time to get to know each other. Don’t jump in too early. You don’t want to apply undue pressure on your partner or yourself before the proper trust is there to bear it. But don’t hold back until it’s too late. Really get to know each other. Be open. Let the conversations leave the world of projects and let it get personal.

Once, Johnny and I discussed a personal topic for over three hours on one call. It was heated at moments but it proved to both of us we can communicate soundly amid disagreement, a key trait for partners. It’s important to know how someone views the world, not just how they view work, as they are inseparable. Be flexible enough to get on calls that are both scheduled and spur-of-the-moment. Have calls in the early mornings and late evenings — you’ll see different sides of each other. Ask questions that have an edge of randomness or friendly confrontation to them. The best questions start with why — they can illuminate how someone reasons. Communication like this is necessary when the only way you meet someone is through the same webcam.

In the end, there’s always risk. But entrepreneurship is inherently risky; this version of it only adds an extra layer of unknowns. If that’s the con, the pro is that there is a healthy separation that centralized entrepreneurs don’t get to have. Instead of living close together, such as sharing a flat in San Francisco and absorbing each others’ lives to the point of social suffocation and peer overload, there’s space and balance. For us, this provides a boost in productivity and an efficient collectedness when we do touch base.

In the end, the rules of starting a business are changing. You no longer need to shake hands, meet for coffee, or share an office to form a company with someone. With today’s video conferencing and remote work tools, you can meet anyone across the world and grow enough trust to even quit your job and jump into a startup venture together. If someone asked me if I would do another non-remote co-founder arrangement again after this, I would say yes — in a heartbeat.

Why limit your opportunities and possibilities to the city you live in?

Dave Schools is a Cofounder at Hopin an online events platform where you can create engaging online events that connect people around the globe.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

He could be contacted at udohrapulu@gmail.com

California ‘s new law on employment is a game changer for visionary African startup

Gavin Newsom, California state governor

In a perfect world of the gig economy, James should be able to hire a car from a rental service store, present his driving license and other certifications to Uber (a car hailing service, for instance), get registered if he is considered qualified based on a series of paper checks and tests, and take to town helping online car hailers to reach their destinations, at an automated pay rate, and of course, as long as he fully complies with the terms and conditions of his engagement with Uber. In this arrangement, although James uses the Uber hailing service as a vehicle to carry out his business, he is still considered by Uber as an independent contractor who works off the controls and the supervision of Uber, except on occasions where he is skidding off his original rules of engagement. Thus, in a gig economy, James should not be on Uber’s payroll and is not even qualified to be classified as an employee of Uber. But all that has been shaken up, disrupted by the US State of California in a landmark new law that had been assented to [and which took effect from January 1, 2020] by the Californian state governor. If other jurisdictions draw inspiration from California ’s new standards, then all logistics, transport and other similar startups that have built their business models around independent contracting would be back to square one.

(Image for: California employment law African startups)

Bradley Tusk, president of Tusk Ventures and Uber’s first political strategist, told The Verge, “A domino effect [is] not just possible, it’s all but guaranteed.”

First Here Is What The New Law States

California ‘s new employment law has changed the criteria for being an independent contractor.

Now, for a company to classify a worker as an independent contractor, it must prove three things (you may hear this being called the “ABC Test”). If they can’t, then the worker is treated as an employee.