Africa’s leading cable entertainment giant MultiChoice says it is in discussions with Nigerian authorities over the instruction it issued to local banks to freeze its accounts over unpaid taxes. It could be recalled that the Federal Inland Revenue Service (FIRS) froze bank accounts of the company in a bid to recover 1.8 trillion naira (around R63 billion) from the pay-tv company in unpaid VAT. MultiChoice said it was “currently in discussion with FIRS regarding their concerns” and believes that the matter will be resolved amicably.

FIRS executive chairman Muhammad Nami

FIRS had last week raised alarm over the level of non-compliance by MultiChoice Africa, the parent company of MultiChoice Nigeria. According to FIRS, the company has never paid VAT since its inception and appointed Nigerian Deposit Money Banks as agents to freeze and recover the sum of 1.8 trillion naira from the accounts of MultiChoice Nigeria and MultiChoice Africa, Vanguard reported.

FIRS executive chairman Muhammad Nami said the decision to freeze the accounts was as a result of the group’s under-remittance of taxes and continued refusal to grant FIRS access to its servers for audit. MultiChoice is not the first South African company operating in Nigeria which has found itself in hot water with authorities.

African’s largest telecommunications company, MTN, has faced various challenges by Nigerian authorities, including a fine of more than $5 billion (later reduced to $1.7 billion) in 2015 for failing to disconnect five million SIM cards that belonged to unregistered users.

Three years ago, the Nigerian central bank ordered MTN to return $8.1 billion in dividends which it paid to its parent company in SA. According to the bank, this was an illegal payment. Following lengthy negotiations, MTN made a “resolution payment” of $53 million.

Shortly after that, Nigeria’s attorney general slapped MTN with a $2 billion tax bill for payments to foreign suppliers. This was later scrapped.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

The Federal Inland Revenue Service (“FIRS”) recently issued a Revised Information Circular on the Tax Treatment of Non-Governmental Ogranisations (NGOs), hereafter referred to the as “Revised Information Circular” or “the Circular”. The Circular, published on 31 March 2021, amends, updates or replaces the FIRS’ initial information circular (issued in 2010) on the tax exemption status of NGOs – but only to the extent that the initial circular contains information that is inconsistent with the Revised Information Circular.

Ibrahim Moshood, Associate, The Centurion Law Group

The Revised Information Circular reiterates the tax-exemptions, filing and other compliances obligations of NGOs. It also provides clarification on the application of the term “public character” to NGOs when evaluating their eligibility to enjoy the tax exemptions granted under the Companies Income Tax Act (CITA). It is noteworthy that the FIRS’ clarification on the application of the term public character is issued following an inclusion of a definition for “public character” in the CITA by Finance Act, 2020.

The CITA exempts from tax the profits of “any company engaged in ecclesiastical, charitable or educational activities of a public character in so far as such profits are not derived from a trade or business carried on by such company” (emphasis ours). Prior to Finance Act 2020, CITA did not provide definitions for “public character” or “activities of a public character”. Taxpayers, the FIRS and even the Courts therefore interpreted these terms and its application, for tax purposes, in varied ways:

All ecclesiastical, charitable and educational activities are generally accepted as activities of a public character. Therefore, a company engaged in such activities immediately qualifies for tax exemption on profits from (and proven to be from) those activities.

Ecclesiastical, charitable and educational activities are only of public character if those services are freely available for all Nigerians to use, share in or enjoy. If such services/activities are provided at a fee, they no longer pass the public character test because not all Nigerians will find those services affordable.

It is only a body or institution whose activities are meant to benefit Nigerians in general, and particularly the public, and its profits are not available for distribution to its promoters that can qualify as a “public character” company eligible to enjoy tax exemption on its profits.

The long-standing debate has been whether the pre-condition for enjoying the tax exemption is that the company seeking the exemption is an “institution of public character” or the activities provided by that company are of “public character”. To clarify, the Finance Act 2020 defines public character as “with respect to any organisation or institution means an organisation or institution that is (a) registered in accordance with the relevant law in Nigeria; and (b) does not distribute or share its profit in any manner to its members or promoters.” The FIRS’, in its Revised Information Circular, expatiates on this point by stating that distribution of assets (even by way of gift) in cash or kind by such company to its promoters or members will qualify as a distribution of profits.

Defining public character by reference to company/institution and not activity, shifts the focus of the tax exemption from the nature of activities provided to the nature of the company providing those services. This will appear contrary to the law which provides that “any company engaged in…. activities of a public character” may qualify for a tax exemption. It is therefore arguable that while introducing a definition of “public character” in the law may be helpful in some respects, it doesn’t do much to resolve the age-old dispute between Taxpayers and FIRS on how the tax exemption should be applied. The question of what constitutes activities of a public character, which to our minds is the more relevant question given the clear provision of the law, remains unanswered.

Further, more questions may arise based on the definition of “public character”. The requirement that the institution “does not distribute or share its profits in any manner to its members or promoters” is interesting. According to the Companies and Allied Matters Act, it is only a company limited by guarantee that is precluded from distributing profits to its promoters and members. A company limited by shares has no such restriction. Is the intention, therefore, to exclude a company limited by shares from enjoying the tax exemption? Or is such a company eligible for the tax exemption provided if it doesn’t (and can presumably prove) that it does not make distributions to its shareholders or promoters?

Conclusion

Any clarification of a hitherto ambiguous term in a Tax Statute will typically be considered a welcome development. However, the definition of the term “public character” in Finance Act 2020 and the Revised Information Circular may prove insufficient to rest the long-standing issue on the interpretation and application of the tax exemption granted in CITA to ecclesiastical, charitable and educational institutions.

It will be interesting to see how the definition of public character will be applied vis-a-vis the clear provision of the law going forward and how Taxpayers will react to it. Will a company limited by shares that engages in activities of a public character accept that it may no longer qualify for a tax exemption? Or will it continue to contest its eligibility for the exemption in court?

Ibrahim Moshood, Associate & Tozaye Balogun, Director of Tax Services in Africa, The Centurion Law Group

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Nigeria ‘s Federal Inland Revenue Service is set to begin clampdown on tax defaulters today, December 18, 2019, if the most recent notification sent to tax payers warning them to clear their taxes or face sanction is anything to go by.

Muhammad M Nami, newly appointed FIRS chairman

“The FIRS hereby informs all taxpayers (individuals, partnerships, enterprises, corporate organisations, ministries, departments and agencies) who are in default of payment of taxes arising from self-assessment, tax audit, tax investigation, transfer pricing audit, demand notices and any other liabilities, that the service will commence a nationwide tax enforcement exercise from December 18, 2019 with a view to prosecuting defaulters and recovering all outstanding tax liabilities.

“The taxes referred to are as follows: 1. Petroleum Profits Tax; 2. Companies Income Tax; 3. Value Added Tax; 4. Withholding Tax; 5. Tertiary Education Tax; 6. NITDA Levy; 7. Stamp Duty; 8. Capital Gains Tax,” the notice reads.

”We Are Going After Everybody”

The Nigerian tax agency has recently explained that it is hustling hard to meet its N8 trillion revenue target for 2019.

The FIRS also seriously wants to increase Nigeria’s current tax population to 45 million. To do that, it would be relying on multiple information sources, outgone DG of FIRS, Mr Babatunde Fowler said. And that would include invading the country’s Bank Verification Number database and other related agencies with relevant information.

“We are going after everybody. I am sure you have heard that we have placed lien on some accounts of defaulters that have a billion naira turnover annually. So certainly, we are not leaving anyone out of the tax net,’’ he said.

Voluntary Asset and Income Declaration Scheme (Nigeria ’s Tax Amnesty Programme was launched in 2017) Is Going After Companies.

The programme gave tax defaulters in Nigeria a one-year period of grace to declare and settle their unpaid taxes. This appears to be a hard time ahead for most companies in Nigeria.

Most taxpayers are insisting that the scheme was just designed to eliminate them from business. Mr. Fowler said “administrative error” should take the blame arising from the huge number of accounts involved.

“Well, there is certainly one or two instances where we made administrative error, but when you are looking at over 50,000 accounts. There is a tendency that sometimes an error might be made. For those that we made errors on, I wrote them personally apologising and of course we lifted the lien on their accounts,” he said.

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world

The rush after sources of taxation is not yet over for the Nigerian government. Next on the line of taxation is online transactions. And Nigerian Federal Inland Revenue Service (FIRS), an agency of government responsible for the collection of taxes in Nigeria is not going to do so by deploring tax police after physical businesses. It is going to come by way of demanding Nigerian banks to put a Value-Added Tax (VAT) on every online transaction they are processing on behalf of their customers.

FIRS Boss, Babatunde Fowler

“Not that it is something new; it actually should be in existence. “We will certainly follow up to make sure that every VAT that is due to be collected is collected. Soon, we will ask banks to impose VAT on online transactions for purchases of goods and services,”the Chairman of the agency, Mr Babatunde Fowler said.

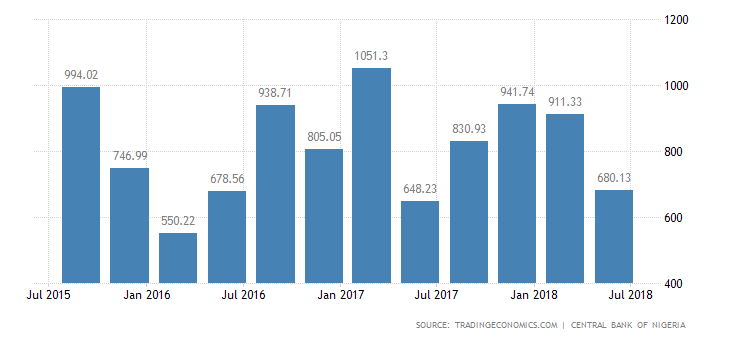

Nigeria’s Revenue History Over The Years

‘’We Are Going After Everybody’’

Hard day for online purchasers in Nigeria. Expect an extra deduction each time you purchase goods or services online, local or international.

The Nigerian agency has further explained that it is hustling hard to meet its N8 trillion revenue target for 2019. And it doesn’t stop with online purchasers.

The FIRS also seriously wants to increase Nigeria’s current tax population to 45 million. To do that, it would be relying on multiple information sources, Mr Fowler said. And that would include invading the country’s Bank Verification Number database and other related agencies with relevant information.

“We are going after everybody. I am sure you have heard that we have placed lien on some accounts of defaulters that have a billion naira turnover annually. So certainly, we are not leaving anyone out of the tax net,’’ he said.

Voluntary Asset and Income Declaration Scheme (Nigeria’s Tax Amnesty Programme was launched in 2017) Is Going After Companies.

The programme gave tax defaulters in Nigeria a one-year period of grace to declare and settle their unpaid taxes. This appears to be a hard time ahead for most companies in Nigeria.

Most taxpayers are insisting that the scheme was just designed to eliminate them from business. Mr. Fowler said “administrative error” should take the blame arising from the huge number of accounts involved.

“Well, there is certainly one or two instances where we made administrative error, but when you are looking at over 50,000 accounts. There is a tendency that sometimes an error might be made. For those that we made errors on, I wrote them personally apologising and of course we lifted the lien on their accounts,” he said.

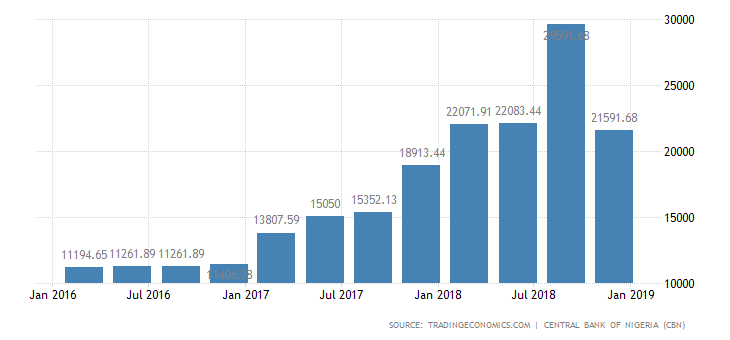

External Debt in Nigeria averaged 9263.57 USD Million from 2008 until 2018, reaching an all time high of 29591.68 USD Million in the third quarter of 2018 and a record low of 3627.50 USD Million in the first quarter of 2009.

Compare the debt profile against Nigeria’s revenue

Charles Rapulu Udoh

Charles Rapulu Udoh, a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organisations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution and data analytics both in Nigeria and across the world.