South African government has killed Section 12J of the country’s Income Tax Act of 2009, which allows investors who make investments in approved Venture Capital Companies (VCC) — that then invest in qualifying small companies, including startups — a tax deduction. This is the most prominent shock delivered in the country’s 2021 national budget statement. Although the scheme was set to expire on 30 June 2021, after being in existence for about 12 years, it was the hope of industry players that government would consider an extension.

Tax

By the terms of the Budget 2021 statement issued by the country’s treasury, the scheme was cancelled because it did not “sufficiently” achieve its objectives of developing small business, generating economic activity, and creating jobs.

“Instead, it provided a significant tax deduction to wealthy taxpayers,” the Treasury said, in the statement.

“Far from investing in small businesses and riskier ventures, Treasury found that the majority of the S12J investments were “low risk”, and offered guaranteed returns “that would have attracted funding without the venture”.

According to the treasury department, more than R11 billion ($756m) was invested in some 360 S12J venture companies, but only 37% of these companies added new jobs after receiving funding. Many of the companies offered property investments.

Simplifying Section 12J, In Full

In simple terms, Section 12J of South Africa’s Income Tax Act of 2009, allows investors who make investments in approved Venture Capital Companies (VCC) — that then invest in qualifying small companies — a tax deduction.

Thus, by investing in a Section 12J venture capital company, the investor not only qualifies for a full deduction of the total investment amount from their taxable income in the relevant tax year, but they are also indirectly supporting the South African economy and the growth of local SMEs. Section 12J is similar to Venture Capital Trusts (VCT) in the United Kingdom, which allow individuals with high net worth to save tax and instead invest in a VCT, which will then invest in startups.

A South African tax-paying entity approaches a VCC with its investment.

The VCC accepts the investment for investments in its portfolio companies and issues the investor with a certificate for the amount invested.

With this certificate, the investor approaches the South African Revenue Service (SARS) and presents the certificate. The certificate empowers the investor to deduct the full value of the investment from their taxable income in that tax year.

Section 12J is so attractive to investors that using it investors can offset any tax on capital gains incurred from the proceeds from the sale of an asset. What this implies is that if in the current tax year a South African taxpayer has a capital gains tax case, the taxpayer will use a portion of his/her income to make an investment in a Section 12J business and write off a portion or all of the tax on capital gains owed.

This explains why there are, today, many VC firms in South Africa and why South Africa collected more than 21% of all VC funding deals in Africa between 2014 and 2019, whereas Nigeria only received 14% of the deals, even though Nigeria is the continent’s largest economy and has more than 3 times South Africa’s population.

What Will Replace Section 12J And What Happens To Newly Launched Funds Under Section 12J After June 30, 2021?

Nothing more specifically stated, but the country’s Treasury said it is currently reviewing tax incentives for research and development. Although the proposed tax incentives are welcome, it is time South Africa pushed for a law, such as a Startup Act, which will more specifically target startups, as against the wider net cast by Section 12J.

For newly launched funds under Section 12J, the implication of the Sunset Clause relating to the section is that no deduction shall be allowed in terms of the VCC incentive in respect of shares acquired after June 30, 2021.

However, there is still uncertainty as to the provision of Section of 12J which states that South Africans investing through section would also have to wait for at least 5 years to get back (if at all) their earnings, alongside the accumulated profit, if any.

In worst case scenarios, the June 30th, 2021 deadline will only have an impact on VC’s ability to raise capital after the date, and not materially affect the functioning of Section 12J on the investments made under the section before that date.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

The Kenyan government has reiterated plans aimed at raising revenue through digital taxation. In this vein, the government has started to implement the Digital Services tax it proposed last year for internet businesses. They are hoping to raise 45 million dollars in revenue before the second half of the year.

Kenya tax

The Kenya Revenue Authority (KRA) had in 2020 released a draft of its proposed taxing online goods sold in the country. Some of these online goods include cloud storage, transport hailing platforms, music, movies, podcasts, mobile apps, and other e-commerce product offerings. According to the proposal, businesses and individuals are obligated to pay a 1.5% fee on the value of products and services offered or sold online and levy VAT at 14% on several goods.

With the advancement in technology, many business transactions are increasingly going digital. The government said it is difficult to effectively tax the income derived through such platforms due to these transactions’ nature. The Digital service tax will facilitate a framework for taxing online businesses.

It could be recalled that other African countries had similar projects. South Africa had in 2014 became the first country on the continent to introduce taxes on e-services. The country’s tactic was to make registration within the country an obligation once companies crossed a threshold of over ZAR50,000 ($3500 at the time). When Uganda introduced the Digital Service tax in 2018, internet users, including social media users in the country, were required to pay the daily duty tax of Ush200 ($0.05).The Ugandan government said the service tax was to reduce gossip on social media and expand the country’s tax base.

In 2018, Tanzania introduced an online content regulation policy. The government said, “a telecommunication service operator providing data used for accessing over the top services is liable to account and pay excise duty on the access to over the top services.”

The Tanzanian government put this policy in place to curb hate speech and fake news from bloggers and online radio and television services. According to the regulation, Over the top (OTT) services, which usually include WhatsApp, Facebook, or Twitter, will be subject to a tax duty of UGX 200 (USD 0.05) per user per day of access. It also required bloggers to pay an annual fee of $900. Online content publishers were mandated to apply for a license at a fee of Tsh100,000 ($43), pay an initial license fee of Tsh1 million ($429), and an annual license fee of Tsh1 million ($429).

The pandemic helped scale many online businesses, with many of them plugging into the system to generate revenue; however, this new development will affect online businesses that utilize the internet to sell. According to reports, more than 60 digital platforms, including Facebook, WhatsApp, and Twitter, were affected by the tax. Uganda lost nearly 30% of internet users between March and September 2018 when the government introduced the tax.

In 2018/2019, users across the country stopped paying and the tax collected decreased by Ush234 billion ($63 million) in 2018/2019. This was because most internet users started using Wi-Fi in their workplaces to avoid over-the-top tax payment.

On the flip side, the proactive measures to solve the modern era’s challenges might be in line with the government’s plans to rehabilitate near-death revenue collections and rescue the growing public debt. In the past, Kenya got into a huge debt problem. It had to hire a team of debt management experts to handle the country’s escalating loan load that caused unsettling liquidity pressures on the Kenyan economy. Chinese debt accounts for 21% of Kenya’s foreign debt and 72% of Kenya’s bilateral debt.

The Kenyan revenue authorities say it expects the number of registrations to hit 1000 by June 2021, generating a possible revenue of 5 billion Kenyan shillings ($45 million).

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Tax evasion has robbed African countries of billions of dollars that could have been deployed to tackle infrastructural decay and poverty across the continent. This was made known by a new report from a nongovernmental organization, Global Alliance for Tax Justice. According to the Report, the African country with the highest losses from corporate tax evasion is Nigeria, losing $10.57 billion per year. Following are South Africa ($2.71 billion), Egypt ($2.12 billion), and Angola ($2.05 billion). Sudan loses $644 million, Kenya $502.4 million, Mozambique $452 million, Morocco $451 million, Algeria $434.75 million, and Ethiopia $362.66 million.

Algeria Suspends Tax

Of all the countries in Africa that has been experiencing heavy losses through tax evasions, Morocco is on number eight with a cumulative loss value of $521,534,833 annually. The group in their 2020 report on global tax evasion notes that of this sum, Morocco loses $69,923,248 to offshore tax evasion.

With offshore wealth amounting to only $3.7 billion, Morocco accounts for 0.0% of global offshore wealth. Its offshore wealth represents 3.1% of GDP. Revenue loss from untaxed offshore wealth, however, amounts to $69.9 million. Morocco also loses $451,611,585 per year to corporate tax evasion, giving the country the eighth-highest corporate tax loss in Africa.

While Morocco loses more to corporate tax evasion than Algeria, it does not inflict any loss on other countries by enabling corporate tax abuse, according to the report. In contrast, Algeria inflicts $550,339,691 in tax loss on other countries by enabling corporate tax abuse, even greater than Nigeria, which is responsible for $112,521,003 in lost corporate taxes.

Given the global COVID-19 pandemic, the NGO emphasized where these lost corporate tax resources could have been spent. The report calculates Morocco’s corporate tax loss as adding up to 20.24% of its public health budget. The loss could alternatively cover the average salaries of 130,186 nurses.

The report ranks Morocco as the 72nd biggest enabler of tax evasion and financial secrecy in the world. In the top spots are the Cayman Islands, the United States, Switzerland, and Hong Kong. Morocco’s most vulnerable trading channel — the channel through which the country is most vulnerable to illicit financial flows — is outward foreign direct investments. The report considers vulnerability as the “average financial secrecy level of all partners with which the country trades with or invests in for that channel, weighted by the volume of trade or investment each partner is responsible for.”

Morocco’s trading partners with the most responsibility for this vulnerability are France (44%), Mauritius (8.9%), and Luxembourg (8.7%).

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

South Africa’s National Treasury has said it was introducing a new tax subsidy of 500 rand ($28) per month for each worker to employers for the next four months to cushion financial losses suffered by firms due to the coronavirus.

“The tax adjustments are made in light of the National State of Disaster and due to the significant and potentially lasting negative impacts on the economy from the spreading of the COVID-19 virus,” the treasury said in a statement.

Here Is All You Need To Know

In a statement, the treasury said it would also permit businesses with revenue of 50 million rand or less to delay paying 20 per cent of their employees’ tax liabilities over the next four months.

South Africa entered a 21-day lockdown on Friday with people restricted to their homes and most businesses shuttered. The country has reported over 1,180 cases of coronavirus and now faces a near certain deep recession.

The announcement also follows Friday’s decision by Moody’s to cut the country’s debt to subinvestment, meaning all three of the top ratings firms now rank the country at junk.

Earlier, Finance Minister Tito Mboweni told the Sunday Times newspaper South Africa would consider approaching the International Monetary Fund and World Bank for funding to fight the coronavirus.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

He could be contacted at udohrapulu@gmail.com

Nigeria ’s Minister of Finance, Zainab Ahmed, has said that the new finance bill, which recommends a 50 per cent increase on Value Added Tax (VAT) passed by the Senate will take effect from January 2, 2020.

Nigeria ’s Minister of Finance, Zainab Ahmed

According to Ahmed the intent of the new tax regime was not to hurt businesses but to grow the country’s non-oil sector contribution.

“The Nigerian economy is characterised by structural challenges that limit the country’s ability to sustain economic growth, create more jobs and achieve significant poverty reduction.

“One of the biggest challenges of all is our high dependence on oil for our economic activities, fiscal revenues and foreign exchange earnings.

“In 2016, Nigeria fell into recession due to its vulnerability to oil.

“Although the oil and gas sector accounted for just about 10 per cent of the GDP, it represented 94 per cent of export earnings and 62 per cent of government revenues (federal and state) in 2011–2015.

“This narrative is changing but we still have much more to do to get to our desired revenue to GDP ratio of 15 per cent by 2023, which we anticipate to come from non-oil revenues.

“We must grow our tax to GDP ratio from the current six per cent as of 2018.”

The minister observed that the country is still short of the Sub-Saharan African average of 19 per cent.

Experts have argued that the country should have focused on increasing the tax net as the burden of paying more taxes will fall on a formal economy, which is segmented in few states like Lagos, Abuja and Rivers.

The government has however, placed some reliefs such as a zero increase on food items in the finance bill to mitigate against the shocks many Nigerians will feel on their disposable income.

The House of Representatives has so far held its assent to the bill.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world

Those who pay tax online in Namibia using the newly introduced Integrated Tax Adiministration System (ITAS) will have their previous penalties incurred for not paying tax forgiven. Namibia’s Finance Minister Calle Schlettwein said Namibian taxpayers can now get relief from the taxman’s noose if they register for the new Integrated Tax Administration System (ITAS), which was introduced in January this year.

“Taxpayers are therefore hereby informed that the ministry is offering an incentive in the form of waiving penalties charged on tax accounts. The incentive program covers the period since the launch of ITAS and ending on 30 June 2020,” he said.

Here Is All You Need To Know

According to the minister, the tax incentive program will be introduced in order to encourage taxpayers not only to register as e-filers but also to continually use the online service.

Schlettwein said that the ministry’s aim is to reach a target of 90 percent of the taxpayer population register as e-filers by June 2020.

He further said taxpayers who have already registered as e-filers since the launch of ITAS also benefit from this incentive and penalties for those without outstanding returns will be waived automatically.

The new online tax initiative in Namibia is meant to see a shift from manual interaction between the Inland Revenue Department and taxpayers to continuous use of the online platform.

“Reaching this target is necessary because the ministry may in future require taxpayers to file all tax returns electronically without an option of manual filing,” Calle Schlettwein said.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world

The competition for international investors is on. Three years off IMF-backed reform. A 5.6% growth in GDP in the 2nd Quarter of 2019. A fast-declining pace of on-boarding new investors. Egypt is set to introduce a new legislation on tax that will bring the country back on track.

Here Is The Deal

The new legislation will focus on automating and simplifying customs and tax processes, Egypt’s Finance Minister Mohamed Maait said on Monday,

“Just yesterday, I contracted a company to automate all these unified tax procedures.” He said IBM (IBM.N) and SAP (SAPG.DE) secured the contract but did not disclose its value.

Now the government is working on a bill to unify tax procedures, Maait said.

“By the end of October, we will have the chance to issue the first draft to the business community, to civil society,” he added.

Maait however acknowledged that a lot still need to be done.

“I have to be very honest. There is a lot of work we have to do in order to make us more attractive to foreign direct investment,” Maait told Reuters in an interview on the sidelines of the Euromoney Egypt conference.

Egypt Has Launched A Series of Reforms So Far

Apart from devaluing its currency by half, Egypt has also been introduced a value-added tax and slashed fuel subsidies. One such significant innovation is Egyptians’ ability to now file their taxes electronically.

Changes to income tax would be procedural, and no changes would be made to overall tax policy or tax rates, Maait added.

Automated customs procedures are already in place at Cairo airport, Maait said, and are being developed at Port Said.

Apart from these tax procedural reforms, Egypt is also planning to sell off its long-delayed stakes in state-owned enterprises, with Maati saying plans to do so would definitely resume in the coming months.

“We strongly believe the private sector will be the main driver for this economy and for creating jobs,” Maait said. “We have to do a lot to give them the confidence, and to make the environment for them easy to do business.”

Euroclear Deal Will Now Allow Holders of Egypt’s Sovereign Debt to Clear Transactions Outside The Country.

Egypt recently signed, in April 2019, an agreement with Euroclear, Europe’s biggest settlement house for securities, to allow holders of its sovereign debt to clear transactions outside the country.

A clearing house manages the post-trade process of getting to a point where settlement can take place

“It is on track, but might not be next month,” Maait said on Monday, adding that a legal change was needed to govern the process and he hoped it would be ready at the beginning of 2020.

A clearing house is a financial institution that acts as an intermediary between buyers and sellers of financial instrument. They take the opposite position of each side of a trade, acting as the buyer to the seller and the seller to the buyer.

Egypt is now Euroclear’s 47th market by this agreement, said Sudip Chatterjee, head of global capital markets at Euroclear.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Effective from January 2020, businesses in Zambia would no longer pay tax on goods and services supplied or imported into the country under the old Value Added Tax Act, but will now do so under the new Sales Tax. And this will come at an extra cost.

Here Is What You Need To Know About The New Sales Act

The Sales Tax will replace the current Value Added Tax (VAT) Act.

The Sales Tax Act will apply to the taxable supplies of good and services. Sales Tax will also apply to the taxable importation of goods and services into Zambia.

The rate of tax is 9% for locally supplied goods and services and 16% for imported goods and services. The Minister is empowered to reduce the rate applicable to a taxable supply by Statutory Instrument.

The Act retains most of the principles that applied under the VAT Act with respect to definitions of supplies, goods, and services. It also largely retains the definitions of time of supply and place of supply. As with the current VAT Act, the return filing deadline remains the 18th of each month.

Exemption

Under the Act, the following goods and services are exempted from sales tax:

Capital goods

Inputs

Designated basic and essential goods or services

Designated suppliers to privileged persons

Exports

The Act also empowers the Minister to provide exemptions to Sales Tax by means of Statutory Instrument.

The Significance of The New Sales Tax To Zambian Businesses

This new Act is so significant for Zambian businesses because, under the old VAT system, consumers used to pay 16% regardless of the value chain. Under the Sales tax regime, the longer the value chain, the higher the tax paid.

Here Is An Example

Under the new sales tax regime, if a Zambian manufacturer imports raw materials from South Africa, for instance, he will pay 16% because from the new law, 16% is payable as sales tax on all goods imported into Zambia. However, when he/she sells to a wholesaler, 9% local sales tax will be levied on that sale. Again, when the wholesaler sells to a retailer, 9% will also be levied. Should the retailer also sell to the final consumer, 9% will also be charged as sales tax?

The implication of this is that Zambia’s final consumers — the farmer, villagers, informal sector worker — will be paying 41% tax instead of 16 % VAT previously the case. In the case of certain Zambian workers who are paying under Pay and As You Earn (PAYE) at the top rate of 35%, the total effective tax on their income would now be 76% without taking into account other levies.

The new sales tax has been criticized as being against the social, economic and political good of Zambians.

“VAT works better when you have an economy that has a strong manufacturing base. But we don’t have it! We are in constant refund and it cannot work now. We have to grow the manufacturing base because that is the sector that needs that support of a VAT refund. Right now, VAT is a subsidy and we are in austerity — we can’t afford subsidies. It is as simple as that.

The VAT system was introduced 23 years ago in 1995 to replace Sales Tax.

For Foreign Investors and Businesses

When the new Zambian Sales Tax Act comes into force in 2020, Zambia will be the only country in Southern African Development Community and possibly in the Common Market for Eastern and Southern Africa region to have a sales tax system and this may influence foreign investors in their decision to locate their companies. The country may likely be less competitive a destination for foreign investors compared to its neighbours.

Why 2020 Is The New Date And The Implication of This For Businesses

The new date for the Sales Tax Act, according to Zambia’s Finance Minister Bwalya Ng’andu is to allow for further refinement of the law.

Addressing parliament, Ng’andu said he was withdrawing the draft law and would re-introduce it in the next session in September, the ministry of finance said in a statement.

“This will allow for sufficient time to address the concerns in the Sales Tax Bill that stakeholders raised,” Ng’andu said.

Since being appointed last month, Ng’andu has sought to mend fences with the miners, with relations deteriorating following tax changes and an ownership dispute over Konkola Copper Mines.

Zambia’s mining industry fiercely opposes the tax.

Zambia is Africa’s second-largest copper producer.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Mauritius is preparing for some radical reforms to its current tax regime. Its 2019–2020 budget proposal is saying so. Changes range from international tax reforms; value-added tax changes; new corporate tax relief measures, including a new patent box regime; a regime for peer-to-peer lending; individual tax breaks; and a tax amnesty scheme.

Below are some of the changes.

Companies or Startups Involved In Innovation Activities Would Get An Eight-Year Tax Holiday

Mauritian 2019–2020 budget is proposing a big incentive for highly innovative companies and startups. For newly established startups and companies, in innovation-driven activities, they stand a greater chance of benefiting from an eight-year tax holiday on income derived from their intellectual property assets which were developed in Mauritius. For existing startups or companies, the eight-year tax holiday would be on income derived from intellectual property assets developed in Mauritius after June 10, 2019.

The Budget also makes changes concerning loss carryforwards for companies. Presently, in Mauritius, the accumulated losses of a company lapse if there is a change in the ownership of the company. However, in the case of a manufacturing company, the Minister may allow the carry forward of the losses if he is satisfied that it is in the public interest to do so and provided conditions relating to the safeguarding of employment are complied with. This derogation will be extended, under the new rule, to any company facing the financial difficulty that is taken over by another shareholder provided conditions imposed by the minister are met. This amendment will be deemed to be effective as from July 1, 2018.

A Five-Year Tax Holiday For E-commerce Startups, Peer-To-Peer Lending

The Budget also proposes a five-year tax holiday for a startup or company setting up an e-commerce platform provided the company is incorporated in Mauritius before June 30, 2025.

Also within the five-year bracket are peer-to-peer lending operators, provided the company starts its operation prior to December 31, 2020.

All interest income received by an individual from peer-to-peer lending will be subject to income tax at the rate of three percent (3%). Any bad debt and fees payable to the peer-to-peer operator will be deductible from taxable interest income. No tax deduction at source will be applied to peer-to-peer interest income.

Also, Mauritian businesses spending on capital goods, which are goods that are used in producing other goods, rather than being bought by consumers, would now breathe some relief. This is because the Budget also improves tax relief for expending on capital goods. Presently, capital expenditure incurred on plant or machinery may be fully expensed in the year incurred if the amount does not exceed MUR30,000 (USD835). The threshold will be raised to MUR60,000 under the new regime.

Four Year Tax Holiday For Oil Bunkering

The new budget also places a four-year tax holiday on all income derived from bunkering of low Sulphur Heavy Fuel Oil.

Under Its Tax Amnesty Rule, Small and Medium Enterprises Will Be Given An Opportunity To Regularize Their Tax Default

To this effect, Small and medium enterprises (with a turnover not exceeding MUR50m) will be given the opportunity to regularize any undeclared or underdeclared income with the Mauritian Revenue Authority free from penalty and interest, provided payment is made on or before March 31, 2020.

The proposed tax amnesty scheme also allows a person making a voluntary disclosure on or before March 31, 2020, to be subject to tax on the disclosed chargeable income at a rate of 15 percent, free from any penalty and interest. However, criminal proceeds are excluded from this grace.

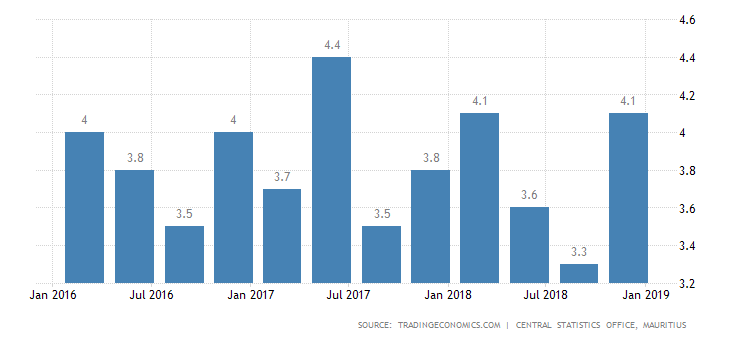

The GDP in Mauritius expanded 4.1 percent year-on-year in the last quarter of 2018, following a 3.3 percent growth in the previous period. Manufacturing rebounded (2.3 percent compared to -1.2 percent) and faster increases were seen in financial and insurance activities (5.2 percent compared to 5.1 percent); real estate (3.1 percent compared to 2.6 percent); and construction (10.1 percent compared to 6.8 percent). Wholesale rose 3.7 percent, the same as in Q3 and agriculture went up 1.7 percent, also the same as in Q3. Considering full 2018, the economy expanded 3.8 percent, the same as in 2017. GDP Annual Growth Rate in Mauritius averaged 3.89 percent from 2001 until 2018, reaching an all-time high of 9.80 percent in the first quarter of 2003 and a record low of -0.80 percent in the first quarter of 2005.

Value-Added Tax (VAT) Also Saw The Greatest Reforms

Under the new VAT regime, cooking gas for domestic use by households in cylinders of up to 12 kg is being made zero-rated for VAT, and certain foodstuffs, including bread, will be newly exempt.

The Budget also says that a wholesale dealer in liquor and alcoholic products will have to be registered with the Mauritian Revenue Authority as a VAT-registered person. The Budget also provides that where there is a splitting of a business entity into different entities to avoid registration for VAT purposes, each entity will be required to be compulsorily registered for VAT.

Consequently, with a view to expediting the processing of VAT refunds, all VAT-registered persons will have to file their VAT return and pay VAT electronically as from March 1, 2020.

As it stands now, a VAT-registered person in Mauritius may claim repayment of input tax in respect of capital goods such as building, plant, machinery, or equipment. The Budget also proposes for provisions to be made to allow repayment of VAT paid on goodwill on acquisition of a business; and the acquisition of intangible assets such as software, patents, or franchise agreements.

Mauritian Banks Who Grant Loans And Other Credit Facilities To Startups, Agric and Renewable Energy Businesses Would Receive 5% Less Tax On Their Taxable Income

Under the new arrangement, a reduced tax rate of five percent (5%) is applicable on the chargeable income of a bank in excess of its chargeable income in the base year (year of assessment 2017/2018) if the bank grants at least five percent of its new banking facilities to any of the following categories of businesses: SMEs in Mauritius; enterprises engaged in agriculture, manufacturing, or production of renewable energy in Mauritius; or operators in African or Asian countries.

Generally, a new taxation system for banks will be re-modeled as follows:

income derived by banks from Global Business Companies will be exempted from the levy under the Value Added Tax Act;

The rate of the levy will be increased from four percent to 4.5 percent of operating income for banks having operating income exceeding MUR1.2bn in a year;

a cap will apply on the increase in levy payable by a bank in order to ensure that no bank is burdened by an excessive levy amount;

it will be clarified that the levy is not a deductible expense under corporate tax; and

no foreign tax credit will be allowed.

Mauritians Will Become Increasingly Tax-Free Under The New Proposal

The new tax regime also sees major changes to personal income tax, including increases to tax-exempt allowances and relief for carers for persons with disabilities.

The Budget that as it concerns inheritance tax, the lump-sum income received by a person by way of payment of pension before the legal due age, death gratuity, or as compensation for death or injury will be excluded from the computation of the solidarity levy. This change will be backdated to take effect as from July 1, 2017, the date the solidarity levy was introduced.

The law will, however, be amended to clarify that an individual’s share of income in a society or succession will be taken into account in the computation of the solidarity levy.

There Would Be Major Changes In The Way International Taxes And Transfer Pricing Are Done In Mauritius

The budget also seeks to amend the Income Tax Act of Mauritius. The amendment of the Income Tax Act would be to implement the recommendation of industry stakeholders regarding the determination of tax residency for companies so that a company will not be considered as tax resident in Mauritius if it is centrally managed and controlled outside Mauritius.

The budget will also address the deficiencies identified by the EU in the territory’s partial exemption regimes.

To this effect, the Income Tax Regulations 1996 will be amended to:

define the detailed substance requirements that must be met in order for a taxpayer to enjoy the partial exemption benefit; and

lay down the conditions that must be satisfied where a company outsources its core income generating activities — namely:

the company must be able to demonstrate adequate monitoring of the outsourced activities;

the outsourced activities must be conducted in Mauritius; and

the economic substance of service providers must not be counted multiple times by multiple companies when evidencing their own substance in Mauritius.

Mauritius also intends to introduce controlled foreign company rules, and the legal provisions relating to the arm’s length test for transfer pricing purposes will be fine-tuned, the Budget says, “to remove any doubt or uncertainty about its application.”

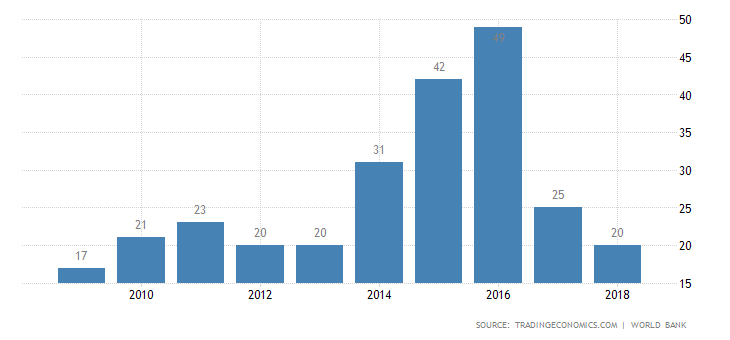

Mauritius is ranked 20 among 190 economies in the ease of doing business, according to the latest World Bank annual ratings. The rank of Mauritius improved to 20 in 2018 from 25 in 2017

Mauritius Would Soon Be A Regional Hub For Fintech

The budgets are not taking the disruptive and profitable nature of Fintech for granted. It sets out measures the territory will take to establish Mauritius as a hub for Fintech in the region. Accordingly, the Financial Services Commission will:

establish a regime for Robotics and AI enabled financial advisory services;

introduce a new license for Fintech Service providers;

encourage self-regulation for Fintech activities in consultation with the United Nations Office on Drugs and Crime;

introduce the use of e-signatures and e-licenses on a pilot basis; and

create crowdfunding as a new licensable activity.

Development of Real Estate Investment Trusts

The Budget announces proposals for new rules and an attractive tax regime to promote the development of Real Estate Investment Trusts (REITs); an “umbrella license” for wealth management activities; and a scheme for headquartering of “e-commerce” activities.

Tax Break For Electric vehicles

The Budget proposes improvements to tax breaks for electric vehicles, including a double deduction for businesses investing in a fleet of eco-friendly cars.

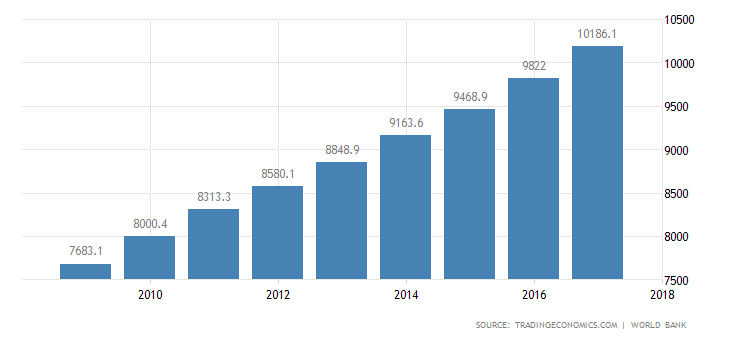

The Gross Domestic Product per capita in Mauritius was last recorded at 10186.10 US dollars in 2017. The GDP per Capita in Mauritius is equivalent to 81 percent of the world’s average.

Gaming Tax Enforcement

The Budget says appropriate amendments will be made to the Income Tax Act to reduce the possibility for a casino or a gaming house to split payment to winners in order to avoid the 10 percent tax on winnings exceeding MUR100,000.

Tax Perks For Marinas

The Government has announced incentives for the development of marina, including new regulations for marinas and a yacht code; an eight-year income tax holiday for a newly set-up company developing a marina; and a VAT exemption will be provided on the construction of marinas.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Businesses in South Africa would now have to pay new taxes, thanks to the Carbon Tax and the Customs and Excise Amendment laws which will both come into effect from 1 June 2019.

Key Points About The New Laws

Both laws will work together in dealing with administrative issues surrounding the implementation of the new carbon tax.

‘Carbon tax’’ according to the new law is a tax on the carbon dioxide (CO2) equivalent of greenhouse gas emissions.

A person is a taxpayer under the Act and is therefore liable to pay an amount of carbon tax calculated in respect of a tax period if that person conducts an activity in South Africa resulting in greenhouse gas emissions above the limit allowed under the Act.

Cyril Ramaphosa, South African President

Under the new law, taxpayers are expected to pay R120 ($8.3) per ton of carbon dioxide according to the amount of greenhouse gas emitted by the taxpayer. This rate would be increased from R120 to any amount depending on the prevailing market inflation in South Africa, plus an additional 2% for the tax period between now and December 31 2022. After 31st December 2022, the carbon tax rate would depend on the prevailing market inflation alone.

Those given some allowance from taxation under the new law include industrial taxpayers; taxpayers engaged in activities that cannot reasonably prevent the emission of carbon dioxide; taxpayers who are exposed to carbon dioxide emission by reason of their exports or imports activities; taxpayers that have implemented measures to reduce their greenhouse gas emissions in respect of a tax period (5% tax allowance); taxpayers that operated within a city limit for carbon dioxide emission even though they emitted the gas (5% allowance).

All taxes are to pay in accordance with South Africa’s yearly environmental levy prescribed under the Customs and Excise Act, 1964 (now 2019 as amended), for every tax period. Hence, the essence of the Customs and Excise Amendment Act is that a new levy known as the environmental levy (which is the carbon tax) is now to be charged by the South African customs on goods, whether imported into or manufactured in South Africa.

Who Is Going To Feel The Impact of the New Carbon Tax?

The new tax will also affect any substantial drop in petrol price, with South Africa’s Central Energy Fund’s data for mid-May, 2019 showing a 5 to 7 cents per litre increase (including the tax) in the price for the month of June for these both petroleum and diesel products.

The contributions of economic sectors to global greenhouse gas emissions. Credit- From the FAO report‘Greenhouse Gas Emissions from Agriculture, Forestry and other Land Use’ 2016.

Longer Impact

South Africans should also expect ‘trickle-down taxing’ on emissions that escape by accident in the petrol and diesel value chains from oil production, transport and venting systems which will likely be passed down to consumers. The heavily hit would be industries that rely heavily on carbon dioxide.

Global carbon dioxide emissions by sector from data from FAO 2017. Credit: Our World in Data

Enforcement?

Expect the South African Tax Commissioner to go all out to implement the new Carbon Tax law. This is because, under the new law, he must annually submit to South Africa’s Energy Minister a report showing the total amount of greenhouse gas emissions reported in respect of which taxpayers are liable for the carbon tax and the amount collected as a carbon tax.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organisations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution and data analytics both in Nigeria and across the world.