Over-the-top (OTT) services providers in Nigeria such as YouTube, Facebook, Twitter, WhatsApp, Blackberry Messenger and many others, will soon be required to declare the revenue they generate from Nigerian consumers and pay tax.

Nigeria’s Vice President Yemi Osinbajo

This is one of the major fallouts of the new finance Act which now subject all multinational digital companies operating abroad with significant economic presence in Nigeria to taxation.

“So, most digital and multinational technology companies do not have a physical presence in Nigeria, yet make significant income in Nigeria from online activities. They pay no tax to Nigeria because they do not have a physical presence in Nigeria, now we are no longer relying on physical presence,” Nigeria’s Vice President Yemi Osinbajo said, confirming the new position.

Here Is All You Need To Know

By the move Nigeria is following the steps of many countries, which have policies that guide these services.

Only companies that have a physical presence in the country were being taxed previously

“Under the new Act, once you have a significant economic presence in Nigeria, you are liable to tax whether you are resident here or not,” Osinbajo noted.

Taxation will definitely serve as a means to curb these excesses of the OTTs while also boosting Nigeria’s tax base.

For Association of Telecommunications Operators of Nigeria (ALTON), the umbrella body of telecom operators in the country, it is not right that a company providing traditional telecommunications services has to meet certain regulatory requirements, like those concerning data protection and taxes while a company providing comparable services over the web does not.a

An over-the-top (OTT) media service is a streaming media service offered directly to viewers via the Internet. OTT bypasses cable, broadcast, and satellite television platforms that traditionally act as a controller or distributor of such content

Gbenga Adebayo, chairman, ALTON, recently said that:

“We are beginning to see the need for regulators to look at regulating technology instead of services.

“These over-the-top services have social, economic and security implications. If they are not licensed, it means they are not regulated, and in that case, there is no limit to the scope of what they can do. There is also no control over services and content they may provide,” he said.

Nigerian Communications Commission (NCC) which until now has insisted on technology neutrality of the OTTs may be forced to facilitate the revenue generating process with the right technological devices to ensure transparency.

The Nigerian government appears to be abandoning the previously proposed 7.5% VAT increase on all VATable goods and services. Parliament seems to be dancing to a different tune now. The highest legislature in the country, the Senate is proposing to tax Nigerians on all calls, sms or the cable stations they make, send or watch. The tax would be fixed at 9%.

“A 9% communication service tax shall be levied on such Electronic Communication Services like Voice Calls; SMS; MMS; Data usage both from Telecommunication Services Providers and Internet Service as well as Pay per View TV Stations.” Nigerian Senator Ali Ndume, Chairman of the Senate Committee on Army said.

Here Is All You Need To Know

The Bill entitled ‘Communication Tax Bill, 2019 (SB.12)’ sponsored by Chairman of the Senate Committee on Army, Senator Ali Ndume, passed the first reading at plenary on Wednesday.

The bill will now go for second reading before being referred to the appropriate committee for further legislative action including public hearing.

The proposed introduction of the tax is meant to replace the 2.2% increase in the Value Added Tax being planned by the Federal government as announced by Finance and National Planning Minister, Zainab Ahmad, recently.

The Communication Service Tax Bill provides that the rate of the tax is 9% of the charge for the use of the communication service.

A Look At Some Provisions of The Bill

The Bill provides among other things that:

“There shall be imposed, charged payable and collected a monthly Communication Service Tax to be levied on charges payable by a user of an Electronic Communication Service other than private Electronic Communication Services.”

It further provides that

“The tax shall be levied on Electronic Communication Services supplied by Service Providers.”

“For the purpose of this clause, the supply of any form of recharges shall be considered as a charge for usage of Electronic Communication Service.”

The target of the Bill

The targets Tax on the such Electronic Communication Services like Voice Calls; SMS; MMS; Data usage both from Telecommunication Services Providers and Internet Service as well as Pay per View TV Stations,

Once the bill is passed,

“The tax shall be paid together with the Electronic Communication Service charge payable to the service provider by the consumer of the service.”

“The tax is due and payable on any supply of Electronic Communication Service within the time period specified under sub-clause (5) of whether or not the person making the supply is permitted or authorized provide Electronic Communication Services.”

Authority In Charge Of Tax Collection

The Bill provides that:

“The Federal Inland Revenue Service (FIRS) established under section 1 of the Federal Inland Revenue Service (Establishment) Act, 2007 shall be responsible for collection and remittance of tax, any interest and penalty paid under this Bill.”

Consequently, “the FIRS shall pay the tax collected together with any interest and penalty into the Federation Account.”

Who Pays The Tax

Under the Bill, while the tax payers may be the end users of those services proposed to be tax, it is the duty of all service providers to file a tax return to account for the tax.

“The tax return shall be in a form prescribed by the FIRS and shall state the amount of tax payable for the period and any related matters that may be required.

The return and the tax due to the accounting period to which the tax return relates shall be submitted and paid to the FIRS not later than the last working day of the month immediately after the month to which the tax return and payment relates,” the Bill reads in part.

However, under the Bill:

“The FIRS may extend the period within which the tax return may be submitted and payment made on application in writing by a service provider, where good cause is shown by the applicant. “The extension shall (accordingly) be communicated to the applicant in writing and shall state the circumstances under which the tax return shall be submitted for the particular period.”

Penalty For Non-Payment of The Tax

Under the Bill, any “service provider who without justification fails to submit to the FIRS the tax return by the date is liable to a pecuniary penalty of N50, 000.00 and a further penalty of N10, 000.00 for each day the return is not submitted.”

Sponsor of the bill, Senator Ndume while justifying the proposed tax said the imposition of tax on communication service is a better way of distributing wealth in such a way that would not affect the ordinary people. According to him, increasing VAT would have very deadly effect on the economy as it could affect prices of goods and services and take them beyond the reach of the ordinary people.

The Implication of This Bill In Relation To The New Digital Tax Proposed By The FIRS And The Proposed 7.5% VAT

The draftsman of the Bill, by coming up with this Bill, obviously has Nigerian internet users in mind. Recall that Nigeria’s tax authority, the FIRS has hinted at the introduction of VAT for all online purchases in 2020. However, until Nigeria’s Value-Added Tax Act is further amended, there is nothing much the agency can do in terms of enforcing its proposed digital tax. The draftsman of the new Bill appears also to be a step smarter here. By renaming it communication sevice tax, instead of digital tax or VAT(amendment), the bill appears to have cast its tax nets wider. Payers of the tax would now not only include internet-savvy users who can buy or sell online but indeed all Nigerian phone users whether connected to the internet or not. The Global State of Digital in 2019 report discovered that there are 98.39 million internet users in Nigeria.

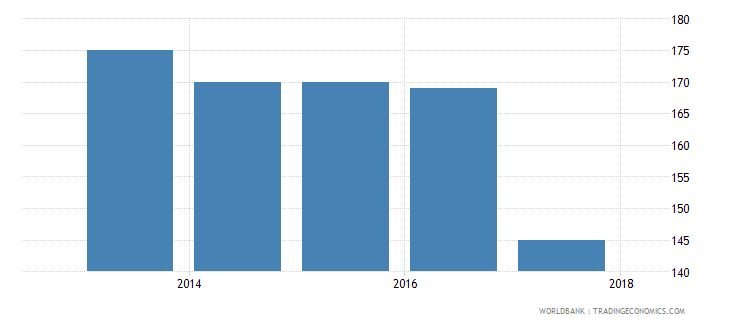

Source: Jumia Nigeria mobile report

According to a recent report released by Nigeria’s leading ecommerce company, Jumia there were over 172 million mobile subscribers Nigeria in 2018, accounting for a penetration rate of 87% of the population. Compared to the figures on internet users, the latter is way too high and more realistic.

In practical terms, 9% of every ₦100 ($0.28) mobile phone recharge voucher in Nigeria is ₦9, meaning that mobile phone users would only be exposed to ₦91 airtime credit. The effect of multiplying ₦9 by over 172 million phone users could only be imagined.

For now, Nigerian government can afford to shelve the proposed highly controversial 7.5% VAT or the internet tax, originally pegged at 5%. The road to the new communication service tax appears to be the quickest compared to the highly vague and often technical alternative of VAT.

The Nigerian government may have finally caught all Nigerians in its tax net.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world

Apart from the fact that companies in Nigeria pay a 30 percent flat-rate corporate tax and other range of taxes and levies, now added to this list are the new 0.005% police fund levy (N5 per N100,000) to be paid out of the net profits of companies, and a possible increase in VAT by 2.2 percent (now 7.5%), barring any last-minute rejection by Nigeria’s parliament.

Here Is All You Need To Know

The New Police Fund Levy

Companies in Nigeria will now have to pay 0.005% police fund levy (N5 per N100,000) out of their net profits. The Nigerian Police Trust Fund Act (the “Act”) was passed by the National Assembly in April 2019, and signed into law by the President on 2 July 2019. The Act establishes a Fund, proceeds from which will be used to train police personnel and procure security machinery and equipment.

Imposition of a levy: The Act imposes a levy of 0.005% of the “net profit” of companies ‘operating business’ in Nigeria.

Funding from Federation Account and other sources: The Fund will also consist of 0.5% total revenue accruing to the Federation Account, in addition to proceeds from grants, intervention funds, aids, donations, investment income and so on.

Establishment of a Board: The Act establishes a board responsible for administering the Fund, making investment decisions, and fulfilling other objectives of the Act.

Duration of the Fund: The Fund will be wound up 6 years after its establishment. The assets and liabilities will be transferred to the Nigeria Police Force.

The New VAT At 7.2%

Nigeria ’s Federal Executive Council also approved 7.2 per cent as new Value Added Tax rate for the country, up from the current five per cent.

Although a definite decision has yet to be taken as to the effective date of the new rate, Nigeria’s Minister of Finance, Budget and National Planning, Zainab Ahmed, who spoke with State House Correspondents after the FEC meeting in Abuja, said consultations were in process over when the new rate would apply.

However, the first hurdle the new tax regime will face would be in Nigeria’s parliament which is either expected to approve or reject the proposal. Nigeria’s VAT Act would also have to be amended by the National Assembly before the commencement of the new rate. Already, the Ministry of Finance has hinted effective date to be sometime in 2020.

“We are proposing and council has agreed to increase in the VAT rate from five per cent to 7.2 per cent,’’ she said.

“This is important because the Federal Government only retains 15 per cent of the VAT; 85 per cent is actually for the states and local governments.

“The states need additional revenue to be able to meet the obligations of the minimum wage.”

“This process involves extensive consultations that need to be made across the country at various levels and also it will involve the review of the VAT Act. So, it is not going to be implemented immediately until the Act is reviewed, ” she added.

The Implication of This

Of course, once the old VAT Act is amended, and the new rate becomes effective, the new rate will automatically be applicable to online transactions carried out in Nigeria. Nigeria ’s Federal Inland Revenue Service, the national tax agency has recently announced that digital tax will become effective January, 2020. This is expected to discourage online transactions and shrink the purchasing powers of Nigerians in a country where the gdp per capita is still less than $2000 ( one of the lowest in the world) and over 86.9, representing 50% of the population are still living below the global poverty line (the worst in the world).

African countries generally have an average VAT rate of about 15 percent, the Americas and Oceania have an average rate of 13 percent, and Asia has an average VAT rate of 12.3 percent. VATs are as low as 5 percent in countries such as Canada (federal only), Taiwan, and Zambia, to as high as 27 percent in Hungary. The average VAT rate in Europe is 20 percent, about 5 percentage points higher than the global average. However, the average European corporate income tax rate is 18.7 percent, which is lower than the worldwide average of 22.8 percent. From the above facts, Nigeria alone would have the highest corporate rate in Europe were it a European country. In a bit, Europe’s average VAT rate is justifiable because of its low corporate tax regimes. To worsen situation, African countries have one of the lowest industrial outputs across the world.

Source: worldatlas.com

Again, although the 0.005% (N5 per N100,000) police fund levy on the net profits of companies may not be very significant, it however places additional tax burden on corporate taxpayers.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

As a way of saving cost for startups and businesses in Nigeria, it is wrong for landlords, lessors, hirers in Nigeria to demand VAT on rent paid by tenants or lessees, hirees of residential premises according to the Federal Inland Revenue Service (FIRS). The VAT is only chargeable on premises used for commercial purposes.

Here Is Why

Residential premises are exempted from VAT under paragraph L(C) 6 of the FIRS Information Circular №9701 of 1st January 1997.

Who Pays VAT, Landlord or Tenant?

From the clarification from the FIRS, the tenant, lessee, the hiree pays VAT for use of commercial properties since he/she pays the rent, whereas the landlord pays the Withholding Tax (WHT) in respect of the property. Withholding tax is usually 10% of the rent and the agent or legal fees.

Yes. Both may form part of computation for rent in respect of all properties whether residential or commercial.

However, here is the trick: where agency or legal fees are charged by the landlord, hirer or lessor where the property is purely for commercial purposes, the lawyer and the agent has to pay 5% VAT each (that is total of 10%) on the fees. The VAT is deducted by FIRS from the total value of the transaction.

Where no agency or legal fees are charged where the property is purely for commercial purposes, VAT is restricted only to rent for use of the commercial property. In this case, only 5%.

Residential properties generally do not attract VAT. However, where the lawyer or the agent charges his/her 10% fee, VAT of 5% will be charged on those fees collected by them.

The Implication of This:

This simply means that your landlord, lessor or hirer cannot add VAT payment to your rent where you are using residential premises unless you are also paying agency or legal fee. In practice, this may apply to first-time tenants who have to pay agent or lawyer’s fees together with the rent.

For tenant, hiree or lessee of commercial premises, he/she must continue to pay VAT on rent for use of such premises, virtually on yearly basis, depending on the payment period. Where agency or legal fees are paid, VAT will also be paid on them, in addition to the VAT already paid on the rent.

In essence, new tenants will receive double VAT deductions for their first rent payment for use of a commercial property. Subsequent tenants of commercial properties in Nigeria will have VAT restricted to only to rent paid.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.