Startups in Nigeria do not seem to be leaving any stones unturned. Nigerian based solar energy distribution startup, Anergy has raised 9 million (NGN3.2 billion) in Series A to fund its commercial growth with new business models, improve on partnership avenues, and expand its activities.

The Funding At A Glance

The funding round was led by Breakthrough Energy Ventures, while Shell-funded All On Energy, the European Union-backed ElectriFI and the Norwegian Investment Fund for Developing Countries (Norfund) participated in the capital injection.

Founded in 2014 by Femi Adeyemo and Kunle Odebunmi, Anergy provides solar power systems to homes and businesses, with a special focus on companies spanning the hospitality, education, financial, agriculture, and healthcare industries.

In the last half-a-decade, the startup claims to have installed over 2 MW of clean energy solutions for more than 2,000 clients.

Funding Was To Scale Operations

“We believe that energy needs in Nigeria have surpassed rudimentary requirements of low power utilization and our product offerings are solving for reliability and not just access,” says CEO Femi Adeyemo, Anergy

“ElectriFI, an EU-funded access to energy impact facility, is thrilled to join such a strong group of investors backing visionary entrepreneurs who will positively impact thousands of local businesses in Nigeria,” said Dominiek Deconinck, ElectriFI Fund Manager.

What Anergy Does

Anergy’s distributed energy systems leverage the amalgamation of solar power, superior storage solutions, and proprietary remote management technologies. The startup uses this to deliver scalable, reliable, and affordable solutions designed to address the problems associated with intermittency and grid unreliability.

“Arnergy inherently understands the West African market and its need for power reliability. Creating accessibility to reliable renewable energy sources is paramount to economic growth in this region.With Arnergy’s technology, we can significantly decrease carbon emissions, and it’s a model that can be replicated all over the developing world,” said Carmichael Roberts of Breakthrough Energy Ventures.

What Attracted Investors To The Startup

The startup got the investment because, according to Mark Davis, EVP Clean Energy from Norfund,

“Access to clean and stable energy is a prerequisite for job creation and development.’’

Davis said Norfund is proud to support the expansion of Arnergy which will provide Nigerian households and businesses on a weak-grid connection with a cheaper, cleaner and more reliable power solution to meet their daily needs.

‘‘ElectriFI, an EU-funded access to energy impact facility, is thrilled to join such a strong group of investors backing visionary entrepreneurs who will positively impact thousands of local businesses in Nigeria,” said Dominiek Deconinck, ElectriFI Fund Manager.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Nigerian ed-tech startup ScholarX has joined the league of African startups that raise funds to kick-start their businesses. The startup has raised US$100,000 towards an intended US$200,000 pre-seed funding round to launch new products and grow its team.

At A Glance

The startup was launched in Nigeria in 2016. The ScholarX app allows users to select parameters and scroll through lists of available scholarships that match their requirements.

Co-founder and chief executive officer (CEO) of ScholarX, Bola Lawal said this round of funding for ScholarX (US$100,000 of a pre-seed round so far) came mostly from angel investors.

“We are primarily raising for our new model, called SkillsFund, which we are ready to run a full pilot of in July,” he said.

“SkillsFund democratises labour-force reconditioning by providing financing to help new entrants — recent graduates — get up-skilled via verified training partners in in-demand skills and then help place them with local employers seeking fresh talent.”

The World Bank ‘s map of tech hubs in Africa. Click herefor a more expanded view

The startup said funds raised would also go towards building the startup’s capacity in terms of staff and technology to handle funding, recruitment, and placement of successful students in the program.

“This means that ScholarX will be positioned to actualise its goal of building an ecosystem around education financing for current students and recent graduates. It means that we won’t just stop at providing scholarships but provide additional training opportunities that will directly lead to jobs for the growing youth population,” he said.

ScholarX last rolled out a new product back in 2017 when it launched Village, an education crowdfunding platform that allows African secondary school and university students to create fundraising campaigns for backing by sponsors.

The Nigerian startup took part in the global WISE Accelerator and the Cape Town-based Injini ed-tech incubator last year and was named part of the third Google Launchpad Africa accelerator cohort in March.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

“References to the currency of Zimbabwe shall, with effect from the 24th of June 2019 be construed as references to the form of legal tender and the electronic currency with which the term Zimbabwe dollar is.’’

The above statement is from the Zimbabwean government as the country begins a new journey to reshape its bad currency.

Henceforth, international and regional currencies such as the rand, US Dollar, Botswana Pula, and British Pound will no longer be acceptable in Zimbabwe as legal tender. Zimbabwean Finance Minister has gazetted mandatory and sole usage of the Zimbabwe Dollar for all local transactions.

‘It is hereby notified that the Minister of Finance … has made the following regulations; Zimbabwe dollar to be the sole currency for legal tender purposes,” reads a part of the Statutory Instrument issued today.

“With effect from the 24th June 2019, the British pound, United States Dollar, South Africa rand, Botswana Pula and any other foreign currency whatsoever shall no longer be legal tender alongside the Zimbabwe dollar in any transactions in Zimbabwe.”

The Statutory Instrument states that “references to the Zimbabwe dollar are coterminous with references to the following and to no other forms of legal tender or currency — (1) the bond notes and coins, 2.) the electronic currency that is to say the RTGS$”.

Zimbabwe has been using multiple currencies since 2009 when hyper-inflation ravaged the country’s local unit.

In 2016, the central bank of Zimbabwe introduced bond notes which traded at par with the US Dollar but have quickly been losing value.

Zimbabwe Is Poised To Have Its New Currency Now Or Never

Earlier this year, Zimbabwe introduced a new currency, the RTGS$ with President Emerson Mnangagwa and the Finance Minister, Mthuli Ncube, saying in the past few months that Zimbabwe was set to have a substantive currency of its own.

It also says the current bond notes and RTGS$ are at par with the Zimbabwe dollar. This has been viewed as an effective introduction of a new currency for Zimbabwe, which is currently battling a severe financial crisis.

Free For All

Companies such as Old Mutual have been accused by allies of President Mnangagwa for fueling informal market currency rates which have spiked out of control. Early Monday morning, the bond notes were trading around 1:10 against the US Dollar while the official interbank market rate is around 1:6.2.

Other listed companies in Zimbabwe have been facing accounting challenges and several have sought permission from the Zimbabwe Stock Exchange to delay financials following the introduction of the RTGS$ in February this year.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Mauritius is preparing for some radical reforms to its current tax regime. Its 2019–2020 budget proposal is saying so. Changes range from international tax reforms; value-added tax changes; new corporate tax relief measures, including a new patent box regime; a regime for peer-to-peer lending; individual tax breaks; and a tax amnesty scheme.

Below are some of the changes.

Companies or Startups Involved In Innovation Activities Would Get An Eight-Year Tax Holiday

Mauritian 2019–2020 budget is proposing a big incentive for highly innovative companies and startups. For newly established startups and companies, in innovation-driven activities, they stand a greater chance of benefiting from an eight-year tax holiday on income derived from their intellectual property assets which were developed in Mauritius. For existing startups or companies, the eight-year tax holiday would be on income derived from intellectual property assets developed in Mauritius after June 10, 2019.

The Budget also makes changes concerning loss carryforwards for companies. Presently, in Mauritius, the accumulated losses of a company lapse if there is a change in the ownership of the company. However, in the case of a manufacturing company, the Minister may allow the carry forward of the losses if he is satisfied that it is in the public interest to do so and provided conditions relating to the safeguarding of employment are complied with. This derogation will be extended, under the new rule, to any company facing the financial difficulty that is taken over by another shareholder provided conditions imposed by the minister are met. This amendment will be deemed to be effective as from July 1, 2018.

A Five-Year Tax Holiday For E-commerce Startups, Peer-To-Peer Lending

The Budget also proposes a five-year tax holiday for a startup or company setting up an e-commerce platform provided the company is incorporated in Mauritius before June 30, 2025.

Also within the five-year bracket are peer-to-peer lending operators, provided the company starts its operation prior to December 31, 2020.

All interest income received by an individual from peer-to-peer lending will be subject to income tax at the rate of three percent (3%). Any bad debt and fees payable to the peer-to-peer operator will be deductible from taxable interest income. No tax deduction at source will be applied to peer-to-peer interest income.

Also, Mauritian businesses spending on capital goods, which are goods that are used in producing other goods, rather than being bought by consumers, would now breathe some relief. This is because the Budget also improves tax relief for expending on capital goods. Presently, capital expenditure incurred on plant or machinery may be fully expensed in the year incurred if the amount does not exceed MUR30,000 (USD835). The threshold will be raised to MUR60,000 under the new regime.

Four Year Tax Holiday For Oil Bunkering

The new budget also places a four-year tax holiday on all income derived from bunkering of low Sulphur Heavy Fuel Oil.

Under Its Tax Amnesty Rule, Small and Medium Enterprises Will Be Given An Opportunity To Regularize Their Tax Default

To this effect, Small and medium enterprises (with a turnover not exceeding MUR50m) will be given the opportunity to regularize any undeclared or underdeclared income with the Mauritian Revenue Authority free from penalty and interest, provided payment is made on or before March 31, 2020.

The proposed tax amnesty scheme also allows a person making a voluntary disclosure on or before March 31, 2020, to be subject to tax on the disclosed chargeable income at a rate of 15 percent, free from any penalty and interest. However, criminal proceeds are excluded from this grace.

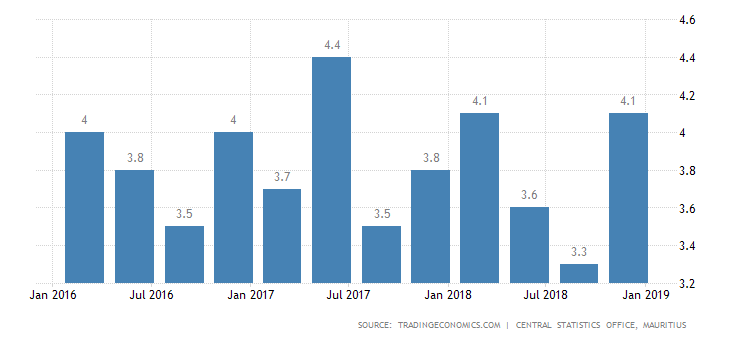

The GDP in Mauritius expanded 4.1 percent year-on-year in the last quarter of 2018, following a 3.3 percent growth in the previous period. Manufacturing rebounded (2.3 percent compared to -1.2 percent) and faster increases were seen in financial and insurance activities (5.2 percent compared to 5.1 percent); real estate (3.1 percent compared to 2.6 percent); and construction (10.1 percent compared to 6.8 percent). Wholesale rose 3.7 percent, the same as in Q3 and agriculture went up 1.7 percent, also the same as in Q3. Considering full 2018, the economy expanded 3.8 percent, the same as in 2017. GDP Annual Growth Rate in Mauritius averaged 3.89 percent from 2001 until 2018, reaching an all-time high of 9.80 percent in the first quarter of 2003 and a record low of -0.80 percent in the first quarter of 2005.

Value-Added Tax (VAT) Also Saw The Greatest Reforms

Under the new VAT regime, cooking gas for domestic use by households in cylinders of up to 12 kg is being made zero-rated for VAT, and certain foodstuffs, including bread, will be newly exempt.

The Budget also says that a wholesale dealer in liquor and alcoholic products will have to be registered with the Mauritian Revenue Authority as a VAT-registered person. The Budget also provides that where there is a splitting of a business entity into different entities to avoid registration for VAT purposes, each entity will be required to be compulsorily registered for VAT.

Consequently, with a view to expediting the processing of VAT refunds, all VAT-registered persons will have to file their VAT return and pay VAT electronically as from March 1, 2020.

As it stands now, a VAT-registered person in Mauritius may claim repayment of input tax in respect of capital goods such as building, plant, machinery, or equipment. The Budget also proposes for provisions to be made to allow repayment of VAT paid on goodwill on acquisition of a business; and the acquisition of intangible assets such as software, patents, or franchise agreements.

Mauritian Banks Who Grant Loans And Other Credit Facilities To Startups, Agric and Renewable Energy Businesses Would Receive 5% Less Tax On Their Taxable Income

Under the new arrangement, a reduced tax rate of five percent (5%) is applicable on the chargeable income of a bank in excess of its chargeable income in the base year (year of assessment 2017/2018) if the bank grants at least five percent of its new banking facilities to any of the following categories of businesses: SMEs in Mauritius; enterprises engaged in agriculture, manufacturing, or production of renewable energy in Mauritius; or operators in African or Asian countries.

Generally, a new taxation system for banks will be re-modeled as follows:

income derived by banks from Global Business Companies will be exempted from the levy under the Value Added Tax Act;

The rate of the levy will be increased from four percent to 4.5 percent of operating income for banks having operating income exceeding MUR1.2bn in a year;

a cap will apply on the increase in levy payable by a bank in order to ensure that no bank is burdened by an excessive levy amount;

it will be clarified that the levy is not a deductible expense under corporate tax; and

no foreign tax credit will be allowed.

Mauritians Will Become Increasingly Tax-Free Under The New Proposal

The new tax regime also sees major changes to personal income tax, including increases to tax-exempt allowances and relief for carers for persons with disabilities.

The Budget that as it concerns inheritance tax, the lump-sum income received by a person by way of payment of pension before the legal due age, death gratuity, or as compensation for death or injury will be excluded from the computation of the solidarity levy. This change will be backdated to take effect as from July 1, 2017, the date the solidarity levy was introduced.

The law will, however, be amended to clarify that an individual’s share of income in a society or succession will be taken into account in the computation of the solidarity levy.

There Would Be Major Changes In The Way International Taxes And Transfer Pricing Are Done In Mauritius

The budget also seeks to amend the Income Tax Act of Mauritius. The amendment of the Income Tax Act would be to implement the recommendation of industry stakeholders regarding the determination of tax residency for companies so that a company will not be considered as tax resident in Mauritius if it is centrally managed and controlled outside Mauritius.

The budget will also address the deficiencies identified by the EU in the territory’s partial exemption regimes.

To this effect, the Income Tax Regulations 1996 will be amended to:

define the detailed substance requirements that must be met in order for a taxpayer to enjoy the partial exemption benefit; and

lay down the conditions that must be satisfied where a company outsources its core income generating activities — namely:

the company must be able to demonstrate adequate monitoring of the outsourced activities;

the outsourced activities must be conducted in Mauritius; and

the economic substance of service providers must not be counted multiple times by multiple companies when evidencing their own substance in Mauritius.

Mauritius also intends to introduce controlled foreign company rules, and the legal provisions relating to the arm’s length test for transfer pricing purposes will be fine-tuned, the Budget says, “to remove any doubt or uncertainty about its application.”

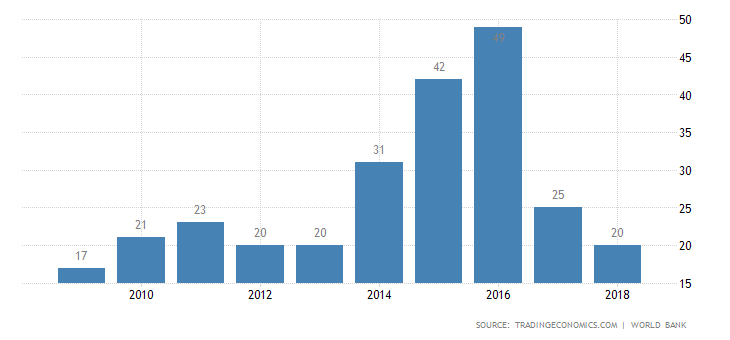

Mauritius is ranked 20 among 190 economies in the ease of doing business, according to the latest World Bank annual ratings. The rank of Mauritius improved to 20 in 2018 from 25 in 2017

Mauritius Would Soon Be A Regional Hub For Fintech

The budgets are not taking the disruptive and profitable nature of Fintech for granted. It sets out measures the territory will take to establish Mauritius as a hub for Fintech in the region. Accordingly, the Financial Services Commission will:

establish a regime for Robotics and AI enabled financial advisory services;

introduce a new license for Fintech Service providers;

encourage self-regulation for Fintech activities in consultation with the United Nations Office on Drugs and Crime;

introduce the use of e-signatures and e-licenses on a pilot basis; and

create crowdfunding as a new licensable activity.

Development of Real Estate Investment Trusts

The Budget announces proposals for new rules and an attractive tax regime to promote the development of Real Estate Investment Trusts (REITs); an “umbrella license” for wealth management activities; and a scheme for headquartering of “e-commerce” activities.

Tax Break For Electric vehicles

The Budget proposes improvements to tax breaks for electric vehicles, including a double deduction for businesses investing in a fleet of eco-friendly cars.

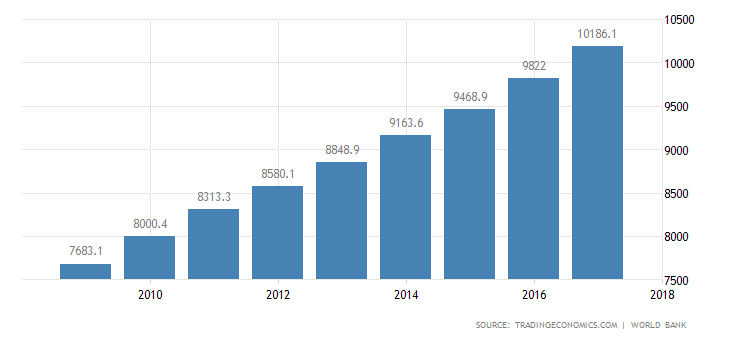

The Gross Domestic Product per capita in Mauritius was last recorded at 10186.10 US dollars in 2017. The GDP per Capita in Mauritius is equivalent to 81 percent of the world’s average.

Gaming Tax Enforcement

The Budget says appropriate amendments will be made to the Income Tax Act to reduce the possibility for a casino or a gaming house to split payment to winners in order to avoid the 10 percent tax on winnings exceeding MUR100,000.

Tax Perks For Marinas

The Government has announced incentives for the development of marina, including new regulations for marinas and a yacht code; an eight-year income tax holiday for a newly set-up company developing a marina; and a VAT exemption will be provided on the construction of marinas.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

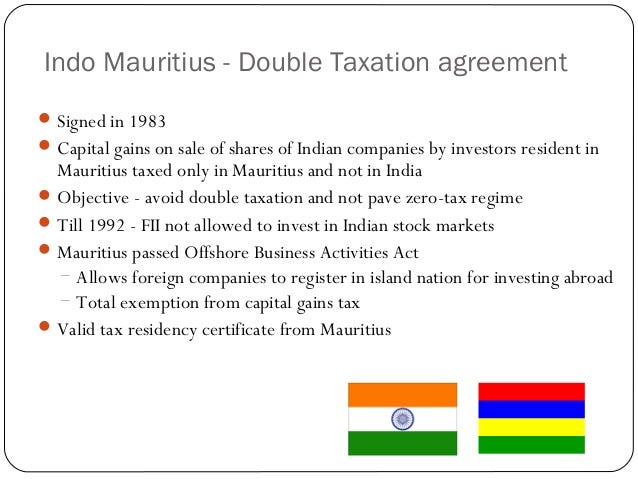

Until recently, Mauritius used to be the tax haven where all businesses flock to. But that is about to change. The Mauritius government’s proposal to amend tax residency rules for companies is giving jitters to foreign funds operating from the tax haven. The current order is that companies set up their corporate offices in Mauritius while having their business operations overseas, in other countries.

The new proposal by the Mauritius government is that any moment from now, a company will not be considered tax resident in the country if it is centrally managed and controlled outside Mauritius. In other words, the era of tax haven in Mauritius is crawling to an end. Consequently, funds may lose tax benefit after the rule amendment.

To Understand The Implication of This, Here Is A Quick Recap of Ways of Taxing Foreign Companies In Mauritius

Under the Mauritian Global Business sector, a foreign company can fall in either one of two categories: GBC1 or GBC2.

A Global Business Company (GBC 2)

A Global Business Company (GBC 2) is a company that has its office in Mauritius but does business outside Mauritius. At all times, the company has the Management Company acting as Registered Agent in Mauritius. The GBC 2 is non-resident for tax purposes and therefore is a tax-exempt entity and cannot avail itself of the relief under the Double Taxation Treaty in force in Mauritius. Thus, a GBC2 company pays no corporate tax; no withholding tax on dividends; no interest and royalties; no Capital Gains tax; and has no access to the Double Taxation Avoidance Treaty.

The proposed amendment announced in the latest budget said that the Partial Exemption Regime under the Income Tax Regulations 1996 will be amended to define the detailed substance requirements that must be met in order for a taxpayer to enjoy the partial exemption benefit.

A Global Business Company 1(GBC 1)

A Global Business Company 1(GBC 1) can be in the form of a Trust, Sociéty and Partnership. This includes small and medium scale businesses. A GBC 1 is considered to be tax resident in Mauritius and is subject to corporate tax at 15%. Tax advantages for GBC 1 in Mauritius are that there is no capital gains tax and also no withholding tax on dividends, interest, and royalties paid or estate duties.

The expanding network of Double Taxation Treaties has further reinforced Mauritius as a tax efficient jurisdiction and is also one of the prime reasons explaining the growing investment in GBC 1. Activities commonly undertaken by a GBC 1 requiring no specialized license are Investment Holding, Trading and International Consultancy and it normally takes an average of 3–4 weeks to incorporate a GBC 1 with such standard activities.

Interpretation of The Intended New Rule

From the above, only the GBC 1 has access to Double Taxation Treaties between their countries and Mauritius. That is, where the business is run in South Africa and Mauritius at the same time. South Africa is a party to a Double Taxation Treaty with Mauritius. And as such, the business in Mauritius would be considered tax resident in Mauritius and is subject to corporate tax at 15%. Tax advantages for GBC 1 in Mauritius are that there is no capital gains tax and also no withholding tax on dividends, interest, and royalties paid or estate duties.

Example of the benefits derivable from a double taxation treaty arrangement

Should this new rule come into effect, hundreds of similar offshore funds operating out of the island nation would be heavily hit.

The question now, therefore, will be what operations are centrally managed and controlled?

The general rule is that a company will have to demonstrate that its entire management resides in Mauritius and if it is centrally managed and controlled outside, then it may not be entitled to it.

“If the authorities find that it is not in Mauritius, then the entity is not a tax resident at all, and if it’s not a tax resident, then the treaty benefits it gets with other countries will not be available to it,” experts said.

This change would hit hundreds of offshore funds operating out of the island nation and invest in their countries to take advantage of the double taxation treaties between their countries and Mauritius.

As An Example

In determining what operations of a company are centrally managed and controlled, let’s study this scenario.

A South African company may have its board of directors in Mauritius while it is managed from South Africa. In this case, the authorities could say the company is not eligible for tax residency. They will now look at the substance on the ground in Mauritius.

In many cases, the board meetings happen in Mauritius, directors are in Mauritius but the control and management are actually not in Mauritius. This would no longer be the case under the new arrangement.

The fallout of this move will be that many of the structures currently set up in Mauritius and claiming treaty benefits on the basis that they have tax residency certificates may now have to take a look at the structures again.

So, many of the Mauritius structures may get challenged in Mauritius itself and several existing structures will be forced to increase the substance requirements within Mauritius for them to continue getting the tax benefits, experts said.

In simple terms, the consequence of not being considered tax resident in Mauritius is that the company would not benefit from the numerous tax advantages that obtainable from running its business in Mauritius. So, it is not a case of claim benefit from Mauritius, but do business in your home country. You have to manage your business in Mauritius before you claim the benefits.

Mauritius is a tax treaty jurisdiction and has so far concluded more than 42 tax treaties which are in force with the countries listed above.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Airtel Africa Plc is preparing to list (IPO) on the Nigerian Stock Exchange and on the London Stock Exchange at the same time. This is another chance for investors in stocks or shares of companies to cash out big time.

Here Is The Timeline For The Nigerian Offer

Announcement of the offer price, offer size, the publication of the pricing statement and allocation of ordinary shares — 28 July 2019.

Allotment of new ordinary shares to the shareholders — 29-Jun-19

Crediting of ordinary shares to accounts — 3-Jul-19

Nigerian listing and start of unconditional dealings on the NSE — 4-Jul-19

The Amount Of Offer And Share Price

In a prospectus released by Airtel Africa Plc (“the Company”), the global Initial Public Offer ( IPO ) would put ordinary shares worth $750mn (or N270.0bn) out for public subscription.

Airtel Africa says the price for each of the shares is at a range of 80 pence and 100 pence/share or (£0.8-£1.0/share) for the London issue.

The Nigerian offer of the issue is opened at an offer price expected to be between N363 and N454/share (technically a naira conversion of the pounds sterling expected price per share) which will be followed with a secondary market listing on The Nigerian Stock Exchange (NSE).

The price range stated above (between N363 — N454/share) is indicative only and may change in the course of The Offer or be set within, above or below the price range.

The Company is expected to be admitted to the premium listing segment of the main board of the London Stock Exchange (LSE) at the end of the transaction.

Application has been made to the Nigerian SEC for the registration of all of the ordinary shares to be issued in connection with The Offer and to the council of the NSE, to be listed and admitted to the official trading list of the NSE.

Analysis of Airtel’s Intended IPO

The amount Airtel Africa intends to raise is $750mn. This is adding the London and the Nigerian IPO together. This offer is 14.0% and 18.9% of Airtel’s issued ordinary share capital, depending on the offer price.

Airtel, from their prospectus, would be allowing 10% of the issue to be ordinary. This is in accordance with the over-allotment option described in the company’s prospectus.

Airtel is looking at using the proceeds from the issue to reduce the level of their indebtedness on their balance sheet, particularly to achieve a targeted leverage ratio of 2.5x.

Airtel is being strategic about the Nigerian offering. It is planning that the Nigerian IPO (or ‘The Offer’) will be offered through a ‘book-building’ exercise pursuant to Rules 320 to 323 of the Nigerian SEC Rules, to determine the issue price and the level of demand. That is, the price may be readjusted according to the demand and response from the public about the offerings.

All ordinary shares subject to The Offer will be issued or sold at the offer price, which will be determined by the Company, following a book building process and in consultation with the Joint Global Co-ordinators.

From the prospectus, interested individual in the Nigerian offer will be deemed to have represented and agreed that it is either a ‘High Net Worth Investor (HNI)’ or a ‘Qualified Institutional Investor (QII)’ as such terms are defined in Rule 321 of the Nigerian SEC Rules.

Airtel may have to consider a number of factors in determining the Offer price, share size and the basis of allocation. This will include the level and nature of the demand for The Offer during the book-building process and prevailing market conditions. In simple terms, it is most likely the share prices will fluctuate.

From the prospectus, there are no restrictions on the free transferability of the Nigerian Offer Shares, meaning that prospective investors may buy and resell their shares at will. This is expected to lead to fluctuation in share prices. Most times, first to buy always win in this kind of situation.

Caveat

The Nigerian Offer is not underwritten, meaning that the consequences of the customer’s actions on the IPO day are not insured.

From the prospectus, it does appear that if UK Admission does not occur or unsuccessful, all conditional dealings will be of no effect and any such dealings will be at the sole risk of the parties concerned. Temporary documents of title will not be issued. UK Admission shall not be conditional on Nigerian Admission, but the Nigerian Admission shall be conditional upon the UK Admission. There can be no assurance that Nigerian Admission will occur on the date indicated above or at all.

Issuing Houses

In relation to the Nigerian Offer and the listing on the NSE, Barclays Securities Nigeria Limited and Quantum Zenith Capital & Investments Limited have been appointed as Nigerian joint issuing houses. Greenwich Securities Limited and Chapel Hill Denham Advisory Limited have been appointed as Nigerian receiving agents.

Points To Have In Mind When Investing In Stocks of Companies

Own at least 10–30 different stocks, preferably in different industries:Don’t put all your money in one company/mutual fund/industry and invest in a wide variety of them.

Invest in established leaders in the industry, preferably companies in the top 25% or 30%: Choose great and stable companies. Remember: We’re investing in businesses, not gambling on racehorses.

The Company you’re buying should have a Long, Unbroken Record of Dividend Payments: If a company gives good dividends to their stockholders, it means it has actual earnings to pay it.

Choose companies with a 7-year Price-to-Earnings (P/E) Ratio of Less than 25 (and less than 20 in the past 12 months): Choose good companies with a moderately low P/E Ratio (less than 25).

Raghunath Mandava, MD and CEO, Africa, said: “Airtel Africa’s Gross Revenue grew by 11.2 percent on a YoY basis. Data traffic grew by 61 percent, voice minutes increased by 25 percent and Airtel Money throughput grew by 29 percent on a YoY basis.

NB: These points were postulated by Benjamin Graham, author of the classic “The Intelligent Investor

Additionally,

Set a minimum limit of the amount you can invest in companies.

Invest in companies that are making profit or has all the metrics to make profit.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Navigating through the complex terrains of finance for startups could one of the toughest stages in developing a business idea. While commercial institutions, family and friends donations as well as personal savings may one of the toughest nuts you have to crack, raising capital to start a business is generally a tall order. How much then is enough to start up your business?

To properly determine what type of funding you should commit into your startups, it is important you first ask the following questions, according to Bob Adams:

How much cash will I have at risk?

How much time will it consume?

How much energy will it take?

Do I currently have other obligations that will prevent me from giving the business 100 percent?

Would there be a much better time for me to start a business other than now?

What are my alternatives if I don’t start a business now?

What are the chances of success?

Am I looking at starting a business from a position of relative strength — feeling good about myself and feel I am relatively well off — or am I looking at starting a business from a position of relative weakness — recently laid off from a job and being behind on my bills?

Can I test-run the business part-time before quitting my job?

Should I choose between a higher-risk or lower-risk business?

Suppose my business provides less income than I expected. How long should I stick with it?

If the business doesn’t work out, how easily will I be able to pick myself up and move along to the next endeavor?

These questions are important because nobody would want to stop halfway into the journey when funding has been made and time spent. That said, deciding on how much is enough to get your new business started would be considered under the following questions.

What Type of Business Do You Plan Going Into?

The U.S.’s Small Business Administration, says microbusinesses cost around $3,000, while most home-based franchises cost $2,000 to $5,000 to start. This may vary according to countries, depending on the value of their currencies and the per capita income of the citizens.

The 10 most profitable small business industries by net profit margin (NPM) are:

Accounting, Tax Preparation, Bookkeeping, and Payroll Services: 18.4 percent NPM

Lessors of Real Estate: 17.9 percent NPM

Legal Services: 17.4 percent NPM

Management of Companies and Enterprises: 16 percent NPM

Activities Related to Real Estate: 14.9 percent NPM

Offices of Dentists: 14.8 percent NPM

Offices of Real Estate Agents and Brokers: 14.3 percent NPM

Nonmetallic Mineral Mining and Quarrying: 13.2% NPM

Offices of Other Health Practitioners: 13 percent NPM

Medical and Diagnostic Laboratories: 12.1 percent NPM

The 10 least profitable industries in the US by net profit margin (NPM) are:

Oil and Gas Extraction: -6.9 percent NPM

Software Publishers: -5.1 percent NPM

Beverage Manufacturing: -3.7 percent NPM

Semiconductor and Other Electronic Component Manufacturing: -0.3 percent NPM

Forging and Stamping: 0.4 percent NPM

Farm Product Raw Material Merchant Wholesalers: 0.9 percent NPM

‘‘If it is a manufacturing unit you can choose a location that can let you save money on electricity, water, taxes, and transportation. Look for a place where manpower is easily available and raw materials can be sourced easily. You can even look for a location that can get you rebates and subsidies from the government.

If yours is a niche product or a service, you may have to look for a single location where all your competitors are. For instance, if it is a software company you want to start, you may have to look for a software belt where all other software companies have set their shops. Similarly, the ideal location for a gold vendor / jeweler would be a gold mart that has housed many such shops.

Offices can be set up in any place that is accessible and offers good facilities such as parking spaces, refreshments, transportation, and so on.

Make sure the location fits well within your budget and offers scope for expansion. An ideal location would be one that complements your business in the best possible way.

Considering the above is so important that entrepreneur Drew Gerber, who started a technology company, a publicity firm and a financial planning company noted that:

“One of the main reasons most small businesses fail is that they simply run out of cash. Writing a business plan without basing your forecasts on reality often leads to an unfortunate, and often unnecessary, business failure. Without the benefit of experience or actual historical financials, it’s easy to overestimate a new company’s revenue and underestimate costs.”’

He estimated that an entrepreneur will need six months’ worth of fixed costs on hand at startup.

“Have a plan to cover your expenses in the first month,” he said. “Identify your customers before you open the door so you can have a way to start covering those expenses.”

‘‘When planning your costs, don’t underestimate the expenses, and remember that they can rise as the business grows,’’ Gerber said. ‘‘It’s easy to overlook costs when you’re thinking about the big picture, but you should be more precise when planning for your fixed expenses.’’

What Costs Are Necessary To Get The Business Running?

After considering what type of business you plan going into, it is best to consider what costs are necessary to get the business running.

The American Small Business Administration says that there are various types of expenses to consider when starting your business.

‘‘It’s important to differentiate these types of costs to properly manage your business’s cash flow for the short and long term,” said Eyal Shinar, CEO of Fundbox, a cash flow management company.

Business owners usually face these types of costs when they plan to start their businesses:

One-time vs. ongoing costs: One-time expenses will be necessary in most cases in the startup process, such as the expenses for incorporating a company.

If there’s a month when you must make a one-time equipment purchase, your money going out will likely be greater than the money coming in, Shinar said. This means your cash flow will be disrupted that month, and you will need to make up for it the following month.

Ongoing costs, on its own, are incurred on a regular basis. Examples include expenses such as utilities. These generally do not fluctuate as much from month to month.

2. Essential vs. optional costs: Essential costs are expenses that are absolutely necessary for the company’s growth and development. Optional purchases should be made only if the budget allows.

“If you have an optional and nonurgent cost, it may be best to wait until you have enough cash reserves for that purchase,” Shinar said.

3. Fixed vs. variable costs: Fixed expenses, such as rent, are consistent from month to month, whereas variable expenses depend on the direct sale of products or services.

‘‘Fixed costs may eat up a high percentage of revenue in the early days, but as you scale up, their relative burden becomes negligible,’’ Shinar said

Below are some of the estimates of both fixed and variable costs, although these depend on the nature of the business you are running

Office space: (On-going; essential) $100-$1,000 per employee per month

Inventory: (On-going; essential)17–25% of the total budget

Marketing: (On-going; essential) 0–10% of the total budget

Website: (On-going; depends) About $25 per month

Office furniture and supplies: (On-going; essential) 10% of the total budget

Utilities: (On-going; essential) About $2 per square foot of office space

Payroll: (On-going; depends) 25–50% of the total budget

Professional consultants: (On-going;optional) $1,000 to $5,000 per year

Insurance: (On-going; essential) An average of $1,200 per year

Taxes: (On-going; depends) Variable

Travel: (On-going; depends)Variable

Shipping: (On-going; depends) Variable

Are There Ways You Can Track Your Spending To Ensure That You Stick To Your Budget?

Important here is the need to keep track of your expenses by calculating these costs from time to time. This will give you a clearer picture of the amount needed to keep your business viable.

Bill Brigham, director of the New York State Small Business Development Center in Albany, New York, advised new business owners to project their cash flows for at least the first three months of the business’s life. He advised startup owners to add up not only fixed costs but also the estimated costs of goods and best- and worst-case revenues.

‘‘If you borrow money, make sure you know not only how much you borrowed but also the interest you owe. Calculating these costs puts a floor on the revenues needed to keep the business viable and provides a good picture of the cash necessary to start it up,’’ Brigham said.

Shinar advised that once you get your business going, you can use QuickBooks or FreshBooks. These tools can connect directly to your bank account. They will also help you to track expenses throughout each month and during tax season.

For Brigham, while starting, it is wise not to resort to borrowing as an option.

‘‘Borrowing puts a lot of pressure on any business and its owners, as it leaves less room for error,’’ he said.

Click here to download a cash flow template to be able to track your monthly cash flow.

Follow this link to find out how you can attract investors to your startup.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Mutual money managers in Nigeria are having the best of fun. Figures from Nigeria’s Securities and Exchange Commission show that it is one sector of the country’s Stock Exchange that is still making profit. The value of mutual funds investment hit N746.5bn at the end of May 2019 according to SEC.

How Mutual Funds Work

Mutual funds are professionally-managed investment programs that pool money from many investors to purchase securities. They are made up of ethical funds, equity-based funds, money market funds, bonds funds, fixed income funds, real estate investment funds, and mixed funds.

A Break Down of The Figures

The figures show that:

Money market fund, which invests only in highly liquid instruments such as cash, cash equivalent securities and high credit rating debt-based securities with a short-term maturity — less than 13 months-recorded the highest investment of N563.9bn, made up of funds pooled from 19 investment schemes.

Money market funds offer high liquidity with a very low level of risk.

The Schemes Under The Fund Are:

Top Money Managers

S/N

NAME OF COMPANY

VALUE OF MONEY MARKET FUND (NAIRA)

1

Stanbic IBTC Money Market Fund ()

262.66 billion

2

FBN Money Market Fund ()

163.27 billion

3

ARM Money Market Fund

57.88 billion

4

AXA Mansard Money Market Fund

25.73 billion

5

Abacus Money Market Fund

9.88 billion

6

Zenith Money Market Fund

7.52 billion

7

EDC Money Market Fund Class A)

6.16 billion

8

Cordros Money Market Fund

5.83 billion

9

Coronation Money Market Fund

5.82 billion

10

Legacy Money Market Fund

5.42 billion

11

United Capital Money Market Fund

4.58 billion

12

Greenwich Plus Money Market Fund

3.24 billion

13

Chapel Hill Denham Money Market Fund

1.62 billion

14

AIICO Money Market Fund

979 million

15

GDL Money Market Fund

953 million

16

Meristem Money Market Fund

782 million

17

PACAM Money Market Fund

601 million

18

Afrinvest Plutus Fund

596 million

19

EDC Money Market Fund Class B

368 million

The top three fund managers under the money market fund were:

Stanbic IBTC Asset Management Limited

FBN Capital Asset Management Limited

Asset & Resources Management Company Limited.

Fixed income funds increased by 11.56 percent month-on-month to N78.27bn from N70.16bn in April.

Real estate funds, pooled from three sources:

Skye Shelter Fund

Union Homes REITs

UPDC Real Estate Investment Fund –

Real estate funds stood at N45.55bn, an increase of 0.73 percent from the N45.22bn recorded in April.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Hard as it may seem, the era of internet disruption is already here and South African small businesses who are not prepared to take these trends seriously may soon be in for a surprise. From the recent survey conducted by GoDaddy, only half of the South African small businesses reported either having their own website (28%) or are planning to build one soon (22%), while around 42% said they rely solely on social media platforms.

The GoDaddy Global Small Business Research Survey was conducted in April and May 2019 in Australia, Canada, Germany, Hong Kong, India, Mexico, South Africa, Turkey, United States, and the United Kingdom.

The GoDaddy Global Small Business Research Survey Is Interesting In Many Ways

GoDaddy also looked at the attitudes of small business owners. Here are some of the key findings:

Small business owners in South Africa value the flexibility of running their own business, with nearly half (48%) saying it’s the best aspect of being an entrepreneur. For 13% of respondents, the money they can make is the biggest plus of running their own small business, while 12% cited helping the world to solve a problem;

On the flip-side, 32% said that the risk of failure and uncertainty about the future is the worst thing about being a small business owner;

Encouragingly, 91% of South African respondents said they would start their own business if they had to make the choice again knowing what they know now, and 84% reported they are happier since becoming an entrepreneur;

The skills shortage is a major challenge for small South African businesses, with 76% saying it is somewhat hard, hard, or very hard to find talented workers;

57% of small South African businesses serve mostly local customers (within 80 kilometers of their location) and only 10% serve mostly international customers;

41% of small business owners worked for a corporate employer before setting up their own venture; 26% were working for a small business; 16% were unemployed and 16% were students.

Right Now, Small Businesses In South Africa Say The Major Problems of Running A Small Business In South Africa Include:

Insufficient Investment

Around one third (34%) identified insufficient investment as a significant obstacle to growth, followed by failure to keep up with technology (20%) and cyber-security risks (13%).

Instability

Almost half (46%) of South African small businesses cited political instability and social turbulence as may be caused by change, including economic, technological or cultural factors as a major challenge to their growth prospects.

Cyber Attack

While few small businesses (7%) in the South African sample reported being victims of a cyber-attack, for those who did, the consequences were severe.

Those who were attacked reported that it shut down their business for some time; customers couldn’t reach them. They had to spend money to repair systems, and they lost access to accounts needed to service their customers, the survey found.

Technology and Disruptions

One of the biggest issues facing workers globally is the rise of automation, artificial intelligence and robot disruption that raises concerns about the future of jobs.

However, the vast majority of small business owners in South Africa believe they are insulated from those risks — 70% felt protected against job loss from these technology developments.

While technology disruption is likely to pose challenges, it also can reduce the barrier to entry to create a small business.

Local small businesses were least likely to have a website among the countries in the survey, and the most likely to rely on social channels, the survey noted

Research firm Savanta conducted the field research of the 4,505 small businesses in the countries. The South African respondents comprised companies with less than 25 employees.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.

Egypt’s Swvl, a mass-transit system that enables riders heading in the same direction to share a ride in a van or bus, has raised US$42 million as it looks to expand into other parts of Africa, including Nigeria.

Its latest round of investment is the largest ever secured by an Egyptian tech startup, beating its own record, and is co-led by Vostok Ventures and BECO Capital. Also participating are Arzan VC, Autotech, Blustone, Endeavor Catalyst, MSA, OTF Jasoor Ventures, Sawari Ventures, and Property Finder chief executive officer (CEO) Michael Lahyani.

The funding will see Swvl continue to solidify its position as a leader in building tech-enabled public transportation. It already facilitates hundreds of thousands of rides each month, serving tens of thousands of customers on its network of more than 200 routes in Cairo and Alexandria in Egypt, and Nairobi in Kenya. Other African launches are planned, while Swvl is also launching an R&D facility in Berlin, Germany.

“The plan is to be in at least two or three more African cities by the end of the year,’’ Mostafa Kandil, the founder and chief executive officer, said. “Lagos, Nigeria, is most likely the next market.’’

Not Afraid Of Competition

Although Swvl is the first riding app to offer bus services in Egypt, giant transportation startups Careem and Uber have recently offered their own bus services.

Mostafa Kandil, Egyptian CEO and founder of Swvl, has however noted that the joining of Uber and Careem to the industry has not influenced Swvl’s growth asserting that they have witnessed remarkable development since the two competitive players have launched. In 2018, the startup was valued at nearly US$100 million, becoming the second Egyptian company after Fawryto reaches these figures.

The startup has recently signed an agreement with Ford motor company to deploy more cars on the road. Ford Transit, which the startup intends to use is already the third best selling van of all times. SWVL is already in possession of about 100 Ford Transits. Hazem Taher, SWVL’s Head Marketing Manager, said the vans were ready to go and they’re excited to push them on SWVL’s route.

The startup launched its bus sharing services in Nairobi early this year after raising more than US$30 million in 2018 at a valuation of approximately US$100 million.

Founded in 2018 by Mostafa Kandil, Ahmed Sabbah and Mahmoud Nouh, Swvl is presently available in 200 routes between Cairo, Alexandria, and Nairobi.

To date, the app which is available for both Android and iOS users has registered over a million customers who frequently use their services.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world.