The absence of digital rights laws that meets the needs and expectations of the times especially with the flurry of developments within the information communications technology (ICT) in the last few years has been a hindrance in developing robust online protection for its citizenry which makes the people potentially vulnerable to shady online characters from around the world. And unless African governments put more work into digital rights legislation which falls into the wider area of fundamental human rights and freedom of speech laws enshrined in almost all constitutions, the continent will still be lagging behind other parts of the world. This was the submission of Adeboro Odunlami, a Legal Officer with social enterprise outfit, Paradigm Initiative, PIN urging governments to treat works on such legislations as urgent.

Adeboro Odunlami, Legal Officer at Paradigm Initiative

According to Odulanmi, “the use, development and deployment of technology in African countries are greatly increasing and governments have to urgently update laws to accommodate the changes whilst promoting development and protecting rights,” noting that the role of internet rights groups revolves around providing technical support to the government on internet rights-related matters, demanding for accountability from the government and enlightening citizens on their rights.

She added that net rights groups like PIN and other collaborators have repeatedly called on governments to engender broad-based consultations throughout the process of enacting digital rights legislations.

A CIPES Digital Rights report published in March 2019 stressed the point stating: “African countries need legislative and policy environments that enable the digital society to thrive – be it in the areas of innovation, affordable access or enjoyment of digital rights.” It noted the “limited citizens’ participation” in making these laws and regulations which it attributed to “weak consultative mechanisms by policy makers who often give limited time for feedback on the draft laws and, where feedback is offered, it is often disregarded.

“Policy makers should also be more transparent in the policy-making process by offering more time for consultations and meaningfully considering the inputs they receive from citizens and other interested parties,” the report added. For Abeboro, digital rights groups – as key civil society players – are important for being the voice that prioritizes citizens and their well-being. “The role of internet rights groups revolves around providing technical support to the government on internet rights-related matters, demanding for accountability from the government and enlightening citizens on their rights.”

She also stressed the role of public interest litigation in remedying unfair digital rights laws. “At the heart of public interest litigation is the drive to either enforce positive laws or enforce negative laws strictly.” She added: “Strategic litigation plays a fundamental role in demanding an answer from state actors for their action and this, in turn, promotes accountability.

“Furthermore, there is the potential of the aggrieved getting some remedy for the wrong done against them. Setting precedents with strategic litigation is also one of its core benefits.” PIN has pursued strategic litigation cases in the line of enforcing digital rights in Nigeria. The group also denounced a recent law in Tanzania that banned the measure.

Journalists and opposition voices across Africa increasingly face arrest and jail time for their views online, a situation that watchers say has passed the stage of a trend in Africa, to an expected occurrence, across the continent from Algeria through to Ivory Coast, Ethiopia, Chad and Zambia. Adeboro, who is also a Mandela Washington Fellow, highlighted how legislation, litigation and the judiciary in digital rights should be inclusive of the ecosystem.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

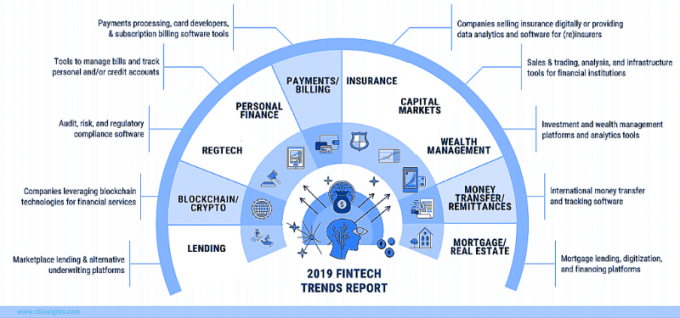

The Central Bank of Nigeria (CBN) has asked commercial banks to share their customer data with FinTech companies to improve access to financial services and provide better services to customers.

CBN Director, Payment System Management, Musa Jimoh at a recent FirstBank FinTech 4.0 Virtual Summit held in Lagos on the topic: “How Blockchain and Artificial Intelligence Will Disrupt FinTech in Nigeria”.

He said the directive was in line with the umbrella bank’s five-year vision and the open banking regime policy that would require banks to open their account base to fintechs to attract more people into the financial system. Jimoh described Fintechs as a technological innovation in financial services that could lead to new business models, applications, processes or products with an associated material effect on the delivery of financial services.

Fintech companies like Quick-teller, MoniDey, Baxi, PocketMoni, Unified Payments, Paga, Cellulant, to name a few, but a few are now part of the financial system, offering banking services to both banked and unbanked people Population. Businesses help consumers pay bills, pay retail, purchase airtime, and use unstructured supplemental service data (USSD) transactions.

They also collect payments from all specters of the population — whether they are banked or not. Jimoh said the CBN is also boosting the use of artificial intelligence in the banking industry and promoting access to digital payment across all sectors of the economy.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

After more than 30 years, companies in Nigeria now have a brand new law that will regulate how they operate. The law which repealed the Companies and Allied Matters Act, Cap C20, Laws of the Federation of Nigeria, 2004 and enacted the Companies and Allied Matters Act, 2020 provides, among many other things, for the incorporation of companies, limited liability partnerships, limited partnerships, registration of business names together with incorporation of trustees of certain communities, bodies, associations; and for related matters, 2020.

Special Adviser to the Nigeria’s President on Media and Publicity, Chief Femi Adesina

“The President’s action on this important piece of legislation, therefore, repealed and replaced the extant Companies and Allied Matters Act, 1990, introducing after 30 years, several corporate legal innovations geared toward enhancing ease of doing business in the country,’’ Special Adviser to the Nigeria’s President on Media and Publicity, Chief Femi Adesina said in a statement.

Here Is What You Need To Know About The New Law

One Person Can Now Form A Company In Nigeria

Under the new law, although public companies are still required to have at least two members, a person can now form a private company. However, even though this is encouraged, the long-term prospects of the startup company should be considered, given that most startups are built for exit through IPOs or acquisitions etc., which makes a one-shareholder structure highly unsuitable for them in practice.

A Private Company May Now Transfer Its Shares

Unlike the old law where share transfer in a private company was restricted, this is not the case with with new law which gives all private companies in Nigeria the option to choose whether or not to transfer its shares in their articles of association. The implication of this is that in private companies, a structure in which most startups exist, shares can now be bought or sold at will. However, the company must obtain the consent of all its members before it sells more than 50% of the assets of the company. A shareholder in a private company is not also permitted to sell more than 50% of his shares to a non-shareholder unless he first offers to existing shareholders the shares meant for sale. He may then proceed to sell to a non-shareholder if the existing shareholders refuse. In the same way, that non-member willing to purchase the shares offered to him must also be ready to buy other shareholders’ interests in the shares offered.

Under the new law, every public or private company still needs to have a secretary. The requirement of a company secretary is only exempted for private companies which are small companies.

Annual General Meetings No Longer Compulsory For Small Companies Or Single Shareholder Companies

By virtue of the provisions of the law, small companies will no longer be mandatorily required to hold Annual General Meetings.

Under the law, a company qualifies as a small company in a year if for that year the following conditions are satisfied —

It is a private company;

The amount of its turnover for that year is not more than ₦120 million or such amount as may be fixed by the Commission;

Its net assets value is not more than ₦60 million or such amount as may be fixed by the Commission;

None of its members is an alien (a foreigner)

None of its members is a Government or a Government corporation or agency or its nominee; and

The directors hold between themselves at least 51 per cent of its equity share capital.

Small Companies Exempted from Audit Requirement

Under the new law, a company (excluding banks and insurance companies) is exempt from the requirements relating to the audit of accounts in respect of a financial year if-

(a) it has not carried on any business since its incorporation ; or

(b) its turnover in that year is not more than ₦120 million and the balance sheet total is not more than ₦60 million. In other words, the company is a smalll company.

One Person Can Now Be A Director In A Small Company

The new law also made provisions concerning directors of a company. According to it, the minimum number of directors for every company (whether public or private) shall be two directors. However, in the case of a private company which is a small company, the minimum number of a director shall be one, unless otherwise provided by the company’s articles or any applicable industry specific legislation.

Other notable provisions include that a director of a public company shall not hold position of both the CEO and the Chairman at the same time. Again, a person cannot be a director in more than 5 public companies at a time.

For the first ever, the new company law is properly defining who an independent director is. Consequently, there must be 3 independent directors in every public company, who must not be employees in the company and who have not made or received any payment in excess of N20m from the company. They must also not own more than 30% direct or indirect equity in another company transacting with (transaction sum should not be more than N20m) the company. They should also not own more than 30% direct or indirect equity in the company.

Nigeria ‘s new law for companies is a game changer for the country and its ease of doing business. Click here to expand image. Source: Visual Capitalist

The new law is also revolutionary in that it gives wider options to places where the meetings of a company may be held. Accordingly, it states that although all statutory and general meetings of companies may be held in Nigeria, small companies or companies with a single shareholder may hold its meetings anywhere in the world. Again, a private company (and not public companies) may hold all its meetings on the internet provided that it has created room for that in its articles of association.

Electronic Communications And Ease of Doing Business

The new law now make it possible for business to be run more easily. For instance, every member can now have a right to attend any general meeting of of a private company (either physically or electronically) and to speak and vote on any resolution (physically or through electronic means) before the meeting. The certified true copies of all such electronically filed documents are now admissible in evidence.

Struggling Companies In Distress Can Now Be Rescued From Total Collapse

Under the new law, the directors of the company may voluntarily arrange with those the company is owing for a way of satisfying all outstanding debts owed by the company.

No More Common Seal For Companies

The law has also put an end to the requirement for each company to have a common seal. In its place, it states that should any document be required by any law or otherwise to be under the common seal of the company, it is enough if the documents were signed by a director and a secretary; or by at least two directors of the company; or by a director in the presence of a witness who shall attest the signature.

Bottom Line:

Remarkable, especially with the introduction of new provisions that have taken care of the difficulties necessitated by the coronavirus pandemic. However, apart from these, in practice, the law remains substantially the same with the old version. While certain provisions may look attractive given their cost-saving implications, there are several provisions which are unsuitable for companies with long-term vision.

For more on the new law and how it may affect your startup company, click here. (PDF)

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

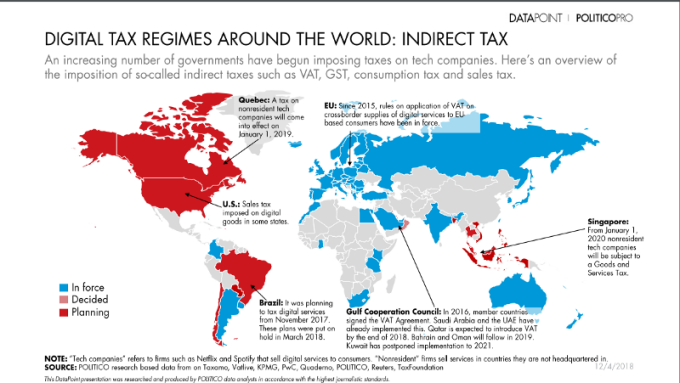

The new 1.5% ‘Digital Service Tax’ imposed on the gross transaction value of services is due at the time of payment.

Here Is What You Need To Know

Additionally, under Kenya ’s new 2020 Value Added Tax (Digital Market Supply) Regulations, digital marketplaces (ecommerce websites) that fail to pay Value Added Tax (at 14%) pursuant Section 5(8) of the country’s Value Added Tax Act, 2013 shall, in addition to the penalties prescribed under the law, be liable to restriction of access to their websites in Kenya until such tax is paid.

“A digital marketplace supplier from an export country who is required to register under the simplified VAT registration framework shall apply to the Commissioner for registration within thirty days from the publication of these regulations,” the regulation reads in part.

Under the regulation, any person offering taxable services through a digital marketplace (ecommerce) shall be required to register for tax in Kenya.

The new tax now means that if, for instance, you are are taking an Uber and the cost of the trip is KES 100, the digital service tax is KES 1.5. If the fee is KES 200, the tax is KES 3.

The Kenya Revenue Authority (KRA), in charge of implementing and enforcing taxes in Kenya, has said it has created a special unit to track transactions and tax multi-nationsl using data-driven detection.

Which Digital Marketplaces (Ecommerce) Are To Pay Tax?

The taxable services made through a digital marketplace shall include electronic services under Section 8(3) of the Value Added Act and: –

Downloadable digital content including downloading of mobile applications, e-books and movies;

Subscription-based media including news, magazines, journals, streaming of TV shows and music, podcasts and online gaming;

Software programs including downloading of software, drivers, website filters and firewalls;

Electronic data management including website hosting, online data warehousing, file-sharing and cloud storage services;

Supply of music, films and games;

Supply of search-engine and automated helpdesk services including supply of customized search-engine services;

Tickets bought for live events, theaters, restaurants etc. purchased through the internet;

Supply of distance teaching via pre-recorded medium or e-learning including supply of online courses and training;

Supply of digital content for listening, viewing or playing on any audio, visual or digital media;

Supply of services on online marketplaces that links the supplier to the recipient, including transport hailing platforms;

Any other digital marketplace supply as may be determined by the Commissioner.

What Criteria Are To Be Used In Determining Whether The Digital MarketPlace Is Required To Pay VAT?

Under the new regulations, a digital services company (Ecommerce) rendering taxable services through a digital marketplace shall be required to register for VAT in Kenya if:

(a) the online services are offered by a business located outside Kenya to an end user in Kenya in business-to-consumer transactions.

(b) the business entity is doing business in Kenya and any of the following situations occur:

(i) the user of the services is in Kenya; or

(ii) the payment made to the business entity staying outside Kenya by the user, for the rendering of the internet-based services, starts from a Kenyan bank registered or authorized in the country; or

(iii) the user of the internet-based services, even though he/she resides outside Kenya, has business, residential or postal address in Kenya.

In any case, where the business entity staying outside Kenya to offer the business-to-customer services is not able to register for tax under the simplified Kenyan VAT registration framework, it shall appoint a tax representative to account for the VAT on their digital services.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Are you a fintech startup in Kenya, not just a digital money lender? Are you worried by the recent proposal by the Central Bank of Kenya to regulate you like well capitalized commercial banks? You have got a chance, till August 11, 2020, to make your submission known to the National Assembly in Nairobi.

“The Departmental Committee on Finance and National Planning should investigate the operations of all mobile money lending platforms in the country with a view to stopping unregulated money lending and subjecting all non-compliant mobile lenders to applicable money lending regulations,” read the petition by MP when the proposal was first introduced in parliament in October last year.

Here Is What You Need To Know

The public has until August 11 to give their views on a proposed regulations that will empower the Central Bank of Kenya (CBK) to oversee the operations of digital financial service providers.

In a public notice, the National Assembly has asked interested individuals to email views to the clerk.

The Central Bank of Kenya (Amendment) Bill, 2020, although purports to curb the steep digital lending rates that have plunged many borrowers into a debt trap as well as predatory lending, also extends its tentacles, by its operation, to all financial technology services in Kenya.

The Implications Of The Proposed Law On Digital Financial Services Startups In Kenya

Implied Lifting Of The Ban On Credit Lending Startups

Once the new law is passed into law, its first implication would be to terminate the ban on credit lending startups in Kenya as regards submitting credit information on their borrowers to Credit Reference Bureaus (CRBs). Thus, with a renewed power to report customers for blacklisting to the country’s central credit information sharing center, it is only safe to say that the risks associated with their business model have become, once again, more manageable.

Licensing of Digital Financial Services Companies/Startups

Another direct implication of the proposed new law on digital financial services startups in Kenya is that the Central Bank of Kenya will now possess recognized power under the law to issue operational licenses to startups desiring to provide services related to a digital financial product, financial product advice, market, administrative or management services or credit under a regulated credit contract in Kenya.

What this means is that startups that offer digital banking services will now also have to maintain a minimum authorized capital of five billion shillings ($46.4 million), which may be increased by such amount as shall be determined by CBK, unless the contrary is stated by the CBK.

In other words, all the rules regulating commercial banks and other financial institutions will now have to apply to startups offering digital financial services if the bill becomes law.

The Bill is coming amid complaints that digital lenders do not provide full information to borrowers on pricing, punishment for defaults and recovery of unpaid loans.

Digital lenders have also been accused of abusing personal information collected from defaulters’ mobile phone contacts list to bombard relatives and friends with messages regarding the default and asking third parties to enforce repayment.

FinTech covers all areas of human interaction with commodity-money circulation and uses a large class of IT technologies. Source: — Aspilos.com

Regulation of Interest Rates Charged Users Of Digital Lending Services

Even though digital lenders in Kenya may still be allowed to lend, the law would however, if passed into law, see that they do not charge interests on their loans excessively. This is because the CBK could now determine the maximum rate of interest they charge their customers.

The latest move to control the activities of digital lenders follows the removal of legal cap on commercial lending rates by the Central Bank of Kenya in March 2020. The cap, established far back in 2016, which set interest rates chargeable by banks at 4%, was intended to address the issue of the affordability of credit for small enterprises and working people, as they had complained for years that high interest rates had locked them out of accessing credit.

Its removal in March this year has, however, resulted in the proliferation of digital lenders, who seek to take advantage of the business opportunities it offered. For instance, Tala, Branch, which are among top players in the mobile digital lending market in the country, offer interest rates of 152.4 percent and 132 percent per year respectively.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

The future of bike-hailing in Africa looks certainly unclear. From Uganda to Rwanda to Nigeria. The latest is Ghana. The country’s National Insurance Commission (NIC) has directed insurance companies to stop issuing insurance policies to motorcycles and tricycles used for commercial purposes.

“We wish to bring your attention that regulation 128 of the Road Traffic Regulations, 2012 (Legislative Instrument 2180) prohibits the usage of motorcycles and tricycles to carry fare-paying passengers and also prohibits the DVLA from licensing motorcycles and tricycles to be used to carry fare-paying passengers,” the Commission noted in a statement.

“The Commission hereby directs all insurance companies to desist from issuing insurance policies to cover motorcycles and tricycles used for all commercial purposes, except courier and delivery services,” the statement further reads.

Here Is What You Need To Know

According to Ghana ‘s Insurance Commission, usage of motorcycles, whether digitalised bike-hailing or not; and tricycles to carry fare-paying passengers is illegal.

The Commission further added that “henceforth, accident victims who were fare-paying passengers on motorcycles or tricycles will not qualify for compensation from the Motor Compensation Fund.

Below is the full statement from the NIC

This further confirms that commercial bike-hailing in the whole of Ghana is a no-no under the law

What Does The Future Look Like For Bike-Hailing Startups In Africa?

Perhaps, would this be the best time African startup founders looked away from launching out bike-hailing startups given the continuing policy instability against bike-hailing across the continent?

In May 2019, Rise Capital with Adventure Capital, First MidWest Group, IC Global Partners and other investors led a $5.3 million investment in Gokada, an on-demand motorcycle taxi startup in Nigeria. A month after, this was exceeded by another motorcycle startup, MAX.ng which raised a $7 million funding round led by Novastar Ventures, with the participation of Japanese manufacturer Yamaha, an investment which brought the startup’s total funding to $9 million. Inspired by the funding MAX.ng planned introduction of electric motorcycles. And yet five months later, in November 2019,Opera’s Africa-focused fintech startup added a new $120 million to its $50 million series A round which it raised in June of 2019, backed by Chinese investors.

In Uganda, leading bike-hailing startup Safeboda has up to $1.3 million in funding with most of the investments coming from Allianz X, the digital investment unit of international financial services provider Allianz Group. Go-Ventures, a venture fund whose cornerstone investor is the Indonesia-based “Super App” company GO-JEK also participated in that investment. Investment in Safeboda was Allianz X’s first ever investment in an African-headquartered company

Opay had earlier this month, after several insinuations in the media about its troubled Super App, come clear, declaring that “some of our business units including the ride-hailing services: ORide, OCar as well as our logistics service OExpress will be put on pause.”

Opay’s move was the first sign that all was not well with existing bike-hailing startups in Nigeria whose operations had been severely affected by government ban, even though they had all pivoted to other Nigerian cities, apart from Lagos, including branching out to other business verticals such as logistics.

Notwithstanding all these, Tunisia’s bike-hailing startup InstiGo has recently gone ahead to secure renewed confidence of investors in the continent’s bike-hailing ecosystem. The startup raised a new $1 million from Capsa Capital Partners and other investors, early July, although it plans to use the investment to explore deeper into other market opportunities, including car sharing.

Neither Lagos, Ghana nor Kampala is the first African city to lead the ban on bike-hailing. The Rwandan government did so a few years ago, only to famously back-track on the decision after the streets of Kigali ground to a near halt. Today, Rwanda is encouraging startups to take up the challenge of helping the government regulate an industry in which most riders are self-employed.

From all indications, it looks like bike-hailing startups in Africa still have a pretty long future, if not an entirely foggy one.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Good news for promoters who have launched their projects under the ANSEJ (National Agency for Youth Employment Support) in Algeria. The country’s Minister of Finance, Aymane Benabderrahmane, has announced a series of facilitation measures in their favor.

Minister of Finance, Aymane Benabderrahmane

“After a series of marathon meetings with all the officials concerned, we managed …to come up with solutions to the financial and tax problems that were blocking the microenterprises of Ansej,” said the minister.

Here Is What You Need To Know

Under the new regime, there would be rescheduling of debts in favor of companies in activity and which have difficulty in repaying their bank loans. This will also include “simplified procedures, such as erasure of late penalties and reducing interest rates by 100%” the Minister said.

With regard to companies that have been shut down but which remain indebted to banks, it was agreed, according to the minister, that the banks be compensated by ANSEJ’s guarantee fund.

“This is the best way to allow banks to recover their due,” said Aymane Benaderrahmane.

In addition, the Minister announced that government has also decided to increase to five, instead of three years, the duration of payment of tax credits by these companies. This provision will be included in the 2021 finance law, said the minister.

The minister also assured that decision had already been taken to accelerate the process of financial disputes involving promoters of companies under ANSEJ, and consequently to release the promoters from liabilities.

To that effect, all criminal proceedings against promoters in litigation with the banks or with the Public Treasury have, consequently, been lifted and withdrawn.

For the minister, all these measures are intended to breathe new life into the ANSEJ system, which has created hundreds of jobs.

Algeria’s National Agency for Youth Employment Support ( Ansej ) is the country’s organization responsible for managing a credit fund for the creation of businesses. She participates in the public employment service .

Ansej is in charge of implementing a support system for business creation for people under 40 years of age. It manages a credit fund, granting loans at zero interest rate (0 rate loans), complementary to bank loans. Committees composed of representatives of banks and institutions grant the loans after examining the files of the promoters.

A bank guarantee fund supplements the financing instruments. Algeria ‘s Ansej advisors provide follow-up to promoters who have obtained a loan.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Uganda doesn’t look like it is ready to continue to have many vehicles around Kampala’s city center again. Latest move by Kampala Capital City Authority (KCCA), the country’s agency in charge of maintaining the country’s capital city, Kampala, is to make it mandatory for all private cars entering the city centre to pay a certain fee, on top of parking fees and other levies. Uganda’s minister of Kampala, Ms Betty Amongi, said a draft policy would soon be shared in Cabinet for discussion and once approved, it will then be tabled to Parliament for endorsement.

minister of Kampala, Ms Betty Amongi

“You will be charged an amount to enter the city. If you have a private car, you will have to pay before you enter the central business district,” the minister said. “The policy is under discussion and once Cabinet and Parliament approve it, we will commence with its implementations.”

Here Is What You Need To Know

The minister said the KCCA would soon determine how much money each vehicle is expected to pay before accessing the city centre.

On why private cars should be made to pay, the minister said the phenomenon is not new since some cities both in Africa and world over charge private cars entering main cities.

The proposal to introduce a fee for private vehicles coming into the city came up last year but was rejected by the motorists.

Private car owners are made to pay for parking fees of between Shs5,000 ($1.3) and Shs10,000 ($2.7) per day for designated places and Shs1,000 (27 cents) per hour.

They also pay for third party insurance, which ranges from Shs45,000 to Shs70,000, and tax on fuel.

The latest move is coming after boda bodas were granted a grace period of 90 days to temporarily operate in the city centre until November 1.

Ms Amongi said the grace period will enable boda boda riders to register with Kampala Capital City Authority (KCCA) so that they are allocated gazetted stages.

The minister of Transport, Gen Katumba Wamala, at the same press conference directed all digital transporting companies such as Safe Boda, Bolt and Uber to register with the government.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Renewable energy companies in Senegal, including startups, have a new set of VAT exemptions to benefit from. The country’s Minister of Finance and Budget and the Minister of Petroleum and Energy have by a joint decree, set the list of materials intended for the production of renewable energies exempt from value added tax.

The list of equipment benefiting from VAT exemption, under the new laws, concerns energy from solar and wind sources as well as biogas.

Here Is What You Need To Know

Regarding solar energy equipment, the photovoltaic solar panel, the solar thermal collector or panel, the charge regulator, the solar pumping kit etc. have all been exempted from VAT.

This exemption also extends to wind energy equipment such as the tower, blade, rotor, nacelle and core.

Finally, with regard to the biogas equipment, the exemption applies to the biogas stove, the biodigester, the water trap, the substrate mixing device, etc.

However to benefit from the new set of tax exemptions, the exempt equipment must be certified by international certification bodies.

Upon application for exemption, renewable energy companies, including startups, will be issued with exemption certificates by the General Directorate of Customs or the General Directorate of Taxes and Domains.

Electricity Production in Sub-Saharan Africa: 2014. Source: Euromonitor

According to the Business Council of Renewable Energies of Senegal (COPERES), this initiative constitutes a significant step forward for the development and promotion of renewable energies in Senegal.

The implication of this for renewable energy startups in Senegal is that, at the point of entry into the country of the exempted materials, there shall be no VAT payable on them. However, this is subject upon applications for exemption from tax made by them.

Value added tax (VAT) is levied at a rate of 18% on transactions (supply of goods and services) in Senegal by persons who, either regularly or on a casual basis, purchase goods for resale or carry on activities other than those relating to agriculture.

This is in addition to the corporate income tax (CIT) rate of 30% levied on companies in the West African country.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

It looks like the state of regulation of bike-hailing startups in Africa is now taking a certain shape. Five months after Nigeria’s largest city, Lagos, banned bike-hailing on its major highways, Uganda is indirectly showing signs that the days of bike-hailing startups are numbered; at least, as long as the country’s capital city, Kampala, is concerned. After much agitation against a previous directive banning commercial cyclists from accessing the city centre and surrounding places, government has now suspended the enforcement of the guideline, all moves coming immediately after more than 3 months of COVID-19 lockdown in the East African country.

Mr Fred Enanga, the police spokesperson

“This morning,” Mr Fred Enanga, the police spokesperson, announced, “we had started operating the free zones. But upon guidance from the Ministry of Works and Transport, the operation on the implementation of the boda boda free zones has been suspended to allow creation of outer stages out of the gazetted zones and signage.”

“Some boda boda riders, including passengers were not being guided. So a roadmap clearly outlining the process will be released for our implementation. We call upon those in the boda boda industry to continue with their operations pending new developments. They should observe the SoPs (standard operating procedures) and should also work within the timing of the curfew and avoid carrying more than one passenger,” Mr Enanga added.

Those new developments are now expected to occur on August 31, 2020. On and after that day, all boda bodas, including their digital adaptations — Safeboda, and others — are expected to disappear from the Kampala city center and its adjoining territories.

“We said the enforcement will start on August 31. So there was no need to start enforcement today. Maybe the security forces were enforcing the national directive, not the one issued by KCCA,” Mr Daniel Nuweabine, the acting KCCA manager of communications and corporate affairs said in a press briefing.

Uganda’s digital evolution in phases. Digital bike-hailing services are relatively new in Uganda. Source: GSMA Intelligence

A Tactical Way Of Gradually Shutting Out Digital Bike-Hailing Companies?

Perhaps or perhaps not. Earlier in May this year, Uganda’s State Minister for Kampala, Kampala Lord Mayor Erias Lukwago, Kampala Capital City Authority (KCCA) and the Ministry of Works and Transport issued guidelines expressing their intentions to force all traditional commercial motorcyclists (locally more known as “boda boda”) to go digital or cease to exist.

The latest announcement by government reopening roads for boda boda operators appears, however, to indicate that government is now back-tracking on the plans, but with some caveat: going forward, from the terms of the new guidelines, the Kampala Capital City Authority (KCCA) wants all bike-hailing operators to form a union or a company.

“All Boda Boda operators must be registered at any of the gazetted stages and this shall be their address,” the guideline reads in parts.

“All Boda Boda App companies and associations shall share the register of all their members (after registering every member to a gazetted stage),” it further reads.

One indirect implication of this is that the unions or companies may be a way of gradually (and easily) making way for the on-boarding of boda boda operators onto digital platforms. Already, KCCA has launched an invitation to tender inviting all digital companies operating in Uganda to be part of the government’s new era of disruption in the country’s public transport system.

“In light of the presentations, KCCA in consultation with other key government agencies has come up with a roadmap that will facilitate operation of the digital companies as well as streamlining public transport. The roadmap entails a validation exercise for digital companies and make recommendations to each for the city to achieve a harmonized transport system,” the invitation reads in part.

While this may be a possibility, the future of bike-hailing startups operating around the country’s capital city, Kampala, looks chequered.

“Cabinet approved Boda Boda Free Zone where All Boda Bodas are prohibited from entering/accessing,” the earlier guidelines further read.

By the terms of the new guidelines, the Boda Boda Free Zone exists along the following key roads: Wampewo Roundabout- Jinja Road to Kitgum House junction — Access Road — Mukwano Road to Clock Tower -Kafumbe Mukasa Road -Kisenyi Road -Mackay Road- Kyaggwe Road- Watoto Church-Bombo Road — Wandegeya — Hajji Musa Kasule Road- Mulago roundabout- Kamwokya junction — Sturrock Road — Prince Charles Drive- Lugogo Bypass-Jinja Road- Wampewo Roundabout.

Uganda ‘s Cabinet approved bodaboda Free Zone where all bike-hailing services or bodabodas are prohibited from accessing. Safeboda is Uganda ‘s leading digital bike-hailing service.

In any case, while it may look like there is still hope for bike-hailing startups operating in Uganda given that not all roads, and cities were blocked from access by bodabodas, they should however be doubtful of the sustainability of their business models. KCCA says it is soon procuring Boda Boda Stage Signs to mark the gazetted stages permanently as well as Traffic signs to demarcate the Boda Boda Free Zone as approved by Cabinet.

One thing is, however, clear from all these: come August 31, 2020 there is nothing free about the Boda Boda Free Zone, and all digital bike-hailing companies must procure operational licenses in order to be able to even operate outside the Free Zone where their movement had not been blocked.

What Does The Future Look Like For Bike-Hailing Startups In Africa?

Kampala is Uganda’s largest city, population-wise, by far ahead of cities like Gulu, Entebbe, Lira, Mbarara or Nansana which have a combination of not up to 1,000,000 people. Only about 18 million Ugandans, representing about 40.1% of the population have access to the internet.

Perhaps, would this be the best time African startup founders looked away from launching out bike-hailing startups given the continuing policy instability against bike-hailing across the continent?

In May 2019, Rise Capital with Adventure Capital, First MidWest Group, IC Global Partners and other investors led a $5.3 million investment in Gokada, an on-demand motorcycle taxi startup in Nigeria. A month after, this was exceeded by another motorcycle startup, MAX.ng which raised a $7 million funding round led by Novastar Ventures, with the participation of Japanese manufacturer Yamaha, an investment which brought the startup’s total funding to $9 million. Inspired by the funding MAX.ng planned introduction of electric motorcycles. And yet five months later, in November 2019,Opera’s Africa-focused fintech startup added a new $120 million to its $50 million series A round which it raised in June of 2019, backed by Chinese investors.

In Uganda, leading bike-hailing startup Safeboda has up to $1.3 million in funding with most of the investments coming from Allianz X, the digital investment unit of international financial services provider Allianz Group. Go-Ventures, a venture fund whose cornerstone investor is the Indonesia-based “Super App” company GO-JEK also participated in that investment. Investment in Safeboda was Allianz X’s first ever investment in an African-headquartered company

Opay had earlier this month, after several insinuations in the media about its troubled Super App, come clear, declaring that “some of our business units including the ride-hailing services: ORide, OCar as well as our logistics service OExpress will be put on pause.”

Opay’s move was the first sign that all was not well with existing bike-hailing startups in Nigeria whose operations had been severely affected by government ban, even though they had all pivoted to other Nigerian cities, apart from Lagos, including branching out to other business verticals such as logistics.

Notwithstanding all these, Tunisia’s bike-hailing startup InstiGo has recently gone ahead to secure renewed confidence of investors in the continent’s bike-hailing ecosystem. The startup raised a new $1 million from Capsa Capital Partners and other investors, early July, although it plans to use the investment to explore deeper into other market opportunities, including car sharing.

Neither Lagos nor Kampala is the first African city to lead the ban. The Rwandan government did so a few years ago, only to famously back-track on the decision after the streets of Kigali ground to a near halt. Today, Rwanda is encouraging startups to take up the challenge of helping the government regulate an industry in which most riders are self-employed.

From all indications, it looks like bike-hailing startups in Africa still have a pretty long future, if not an entirely foggy one.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer