In a significant financial triumph, Ivory Coast-based fintech Julaya has emerged as a promising investment opportunity, yielding a remarkable 4x return for its early angel investors. The success story unfolds against the backdrop of Julaya’s recent $5 million pre-Series A funding round, bringing its total fundraising to $7 million. The round was led by Speedinvest, a European VC firm, with participation from notable investors such as EQ2 Ventures, Kibo Ventures, Orange Ventures, and Ivorian business angel Mohamed Diabi, among others.

The fresh capital injection is earmarked for Julaya’s ambitious expansion plans across Francophone West Africa, targeting countries like Benin, Togo, and Burkina Faso. The funds will also support talent acquisition and bolster product development, including the launch of a loan product catering to around 200,000 SMEs in the UEMOA area.

The decision to allow early investors to exit the business during this funding round was a strategic move, driven by an opportunity to bring in a new fund while managing dilution. This decision resulted in a substantial 4x return for the initial backers, marking a significant win for those who believed in Julaya’s vision early on.

CEO Mathias Léopoldie revealed that the company’s payment processing volume has skyrocketed, from over $1.5 million weekly in July 2017 to an impressive $7.5 million, with revenues experiencing an annual surge of nearly 500%. Notable clients such as Jumia and Sendy underscore Julaya’s growing influence in the B2B payments landscape in Francophone West Africa.

Julaya’s success isn’t confined to financial metrics alone. The startup’s innovative approach to corporate spending management distinguishes it in the market. Utilizing mobile money channels, Julaya facilitates bulk payments between businesses and their unbanked staff. Moreover, the company introduced a Mastercard-issued prepaid card designed for corporate cost management, further expanding its service offerings.

The inclusion of professional football star Édouard Mendy as an investor adds an intriguing element to Julaya’s investor base. Mendy, a limited partner in the company, exemplifies a growing trend where athletes recognize the potential of venture capital as both a lucrative investment and an opportunity to contribute to their home countries.

While Julaya’s financial returns are undoubtedly impressive, its success narrative extends beyond mere numbers. Founder Mathias Léopoldie emphasizes the importance of building a great company that creates genuine economic activity, underlining the nuanced definition of success that goes beyond financial metrics.

As Julaya continues to navigate the complex payment ecosystem in Francophone West Africa, its innovative solutions and strategic partnerships position it as a transformative force, not only in payments but potentially as a close banking partner for businesses in the region, according to Enrique Martinez-Hausmann, principal at lead investor Speedinvest. The company’s growth trajectory and investor returns underscore the pivotal role intuition, strategic decision-making, and a strong team play in shaping a fintech success story.

Charles Rapulu Udoh is a Lagos-based lawyer, who has several years of experience working in Africa’s burgeoning tech startup industry. He has closed multi-million dollar deals bordering on venture capital, private equity, intellectual property (trademark, patent or design, etc.), mergers and acquisitions, in countries such as in the Delaware, New York, UK, Singapore, British Virgin Islands, South Africa, Nigeria etc. He’s also a corporate governance and cross-border data privacy and tax expert. As an award-winning writer and researcher, he is passionate about telling the African startup story, and is one of the continent’s pioneers in this regard

The Economic Commission for Africa ECA Offices for North and West Africa convened an expert group meeting on Wednesday, November 1st, in Accra (Ghana) under the theme “Transition to Renewable Resources for Energy and Food Security in North and West Africa.”

The meeting took place within the context of the second joint Intergovernmental Committee of Senior Officials and Experts (ICSOE) for North and West Africa. Participants examined the impact of climate change in both sub-regions, discussed practical measures for countries to adapt and safeguard their energy and food security, while advancing their development and made some important recommendations.

Experts, researchers, development practitioners, and representatives from 22 North and West African countries attended the meeting, and discussed three critical issues:

Climate change, src: google.com

The impact of climate change and its implications for economic and social development strategies.

Energy security and climate change challenges, and especially the pivotal role of renewable energy in meeting the needs of the populations.

How intra-African trade can facilitate and accelerate the energy and agricultural transition, especially by contributing to food security and the emergence of sub-regional value chains in the agriculture sector.

“In North Africa, it is estimated that water scarcity could affect up to 71 percent of GDP and 61 percent of the population, compared to 22 percent and 36 percent for the rest of the world. However, alternatives remain: by relying on renewable resources, we can not only address these challenges but also accelerate sustainable economic development and social development in the region, along with poverty reduction, job creation, and social equity,” said Zuzana Brixiova Schwidrowski, Director of the ECA office for North Africa.

“Food insecurity is unfortunately a structural challenge in Africa, affecting 20% of the continent’s population compared to the global rate of 9.8%. In this context, three imperatives are evident: increasing agricultural and cereal productivity, mobilizing more domestic resources, and expediting the implementation of the AfCFTA, which serves as our cornerstone for poverty reduction and the acceleration of structural transformation,” said Ngone Diop, Director of the ECA office for West Africa.

Despite its limited contribution to global warming, Africa is significantly affected by this phenomenon: Currently, 17 out of the 20 countries most threatened by climate change are located in Africa and climate change already impacts 2 to 9 percent of national budgets across the continent[1]. According to the latest report from the Intergovernmental Panel on Climate Change (IPCC), North Africa and West Africa are particularly vulnerable with 1.5°C to 3°C expected temperature increases which poses significant threat to populations’ health, productivity and food security.

In response to this situation, African countries have to redirect a growing portion of their public finances towards mitigation efforts and the protection of their populations, thereby depriving themselves of resources needed to finance development, safeguard development gains and implement the Sustainable Development Goals (SDGs).

These constraints underscore Africa’s crucial need to develop innovative growth models capable of preserving and enhancing the well-being of their populations while adapting to climate change and contributing to its slow down.

These models should include appropriate land and water management within the framework of sustainable agriculture, the use of renewable energy to meet national energy needs in a variety of sectors including transportation, industries, heating, cooling, etc., and the establishment of financing models that can address such needs.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Amir Matar had been tilling at SWVL since the startup reached across to him to assist it with its legal compliance obligations. As a legal consultant, Matar was expected to help shape the company’s future by defining it in terms of the legal compliance strategies it needed to scale to the next stage. And so for years, Matar attended to this role in the hope that one day SWVL would grow to become a bigger establishment. But when the four-year-old ride-sharing startup recently announced it would be going public via SPAC at a valuation of $1.5 billion, Matar was nowhere to be found. In fact, he had since moved on. Not that that was his voluntary decision, but that he had been forced out by the company’s management.

“First of all, let me thank you for believing in Swvl. We believe that at the moment we can’t support part-timers anymore and we are working now on that across the whole company,” an email from Swvl’s CEO to Amir was quoted as saying. “We believe also that there is still some time until [redacted] becomes a core part of what we do so we decided collectively to end your employment at Swvl. Please consider Swvl your home and come back whenever you need. I am on a plane to [redacted] now, but let’s meet when I am back.”

According to Matar, he provided business development and legal advice to Swvl for no monetary pay, but was given stock in the company. When he approached Swvl’s CEO about the shares, he was told that they were promised on a one-year cliff, which he did not agree with, he said. Amir said that the offer and acceptance of shares made with him were made without any limitations.

While SWVL’s story is unique in that, aside from Matar, the firm has been the subject of several other employee-related complaints, several other African startup companies are presently experiencing or have had major internal conflicts that have jeopardized their very existence.

Understanding how and why these conflicts occur may serve as a major lesson for other startups that are considering or are just setting out on their journeys.

Amir Matar has since moved on to Mastercard as Senior Counsel, Regulatory Affairs for Middle East and Africa. Image credits: LinkedIn

Fights Among Co-founders

Unlike other causes, squabbles among co-founders have single-handedly destroyed the lives of startups in Africa; more so, if the dissenting co-founders carry enormous responsibilities with them.

Conflict among founders, most commonly, may result from the manner of equity distribution, access to key resources in the startup, compensation over time, among other reasons.

Interestingly though, fights among co-founders in Africa have mostly arisen immediately after major financial activities have occurred in the startups.

In Kenya, the disagreement between Kennedy Nganga, Lauren Dunford and Weston McBride of Safi Analytics, which led to the reportedly forcible ejection of Kennedy from the co-founding team (and invariably from the startup) happened soon after the startup landed its $1.8m investment from investors in 2018.

This is also true for Nigeria’s Cars45’s drama, where co-founders Etop Ikpe, Sujay Tyle alongside other executives moved out of the company in droves. The internal quarrels started in 2019, a year after OLX Groupinvested over $400m in the company. Insinuations are rife in the media that the co-founders were dissatisfied with the structure of equity holding in the company.

Also closely resembling this pattern of dispute is that among the co-founders of Gokada, a Nigerian ride-sharing startup. The exit of Gokada’s pioneer co-founder Deji Oduntan happened barely in March, 2019 just two months before the startup announced it raised $5.3m round from investors, suggesting uncertainties over issues related to finance and investments.

The fact that there is apparent difficulty resolving conflicts among co-founders shows that, in most cases, such conflicts can be fatal if they occur, and may affect a startup’s subsequent chances of accessing funding; and in worst case scenarios, cost it its life.

Employee-Management Fights

Virtually all internal conflicts plaguing startups in Africa have a touch of this colouration. Internal employee strife is rife. In fact, a major disagreement between ‘employees’ and Safeboda, partly ensured that the startup shut down its operations in Kenya recently.

Apart from shutting down operations, one major fall-out of the poor management of relationships between employees and management in African startups is that it has led to the resignations of the chief executive officers of the concerned startups.

This is evident in Wejapa, a Nigerian startup that helps tech talent gain access to job opportunities across the world. Following a series of complaints of exploitation and compromised payment standards from a host of the startup’s software engineers, CEO Favor Ori was forced to resign.

Where the rancorous relationships do not result in the shutting down of the operations or the resignations of the CEOs of the startups concerned, the startup may be subjected to intense public opprobrium and, and in worst cases, exposed to litigation liabilities (which are as a result of the employees deciding to slug it out with the startup company in courts.)

For instance, the rancorous relationships between SWVL and its employees over time have led to some of the employees leaving negative reviews for the startup in public domain — which may have significant effects on the startup’s quest to attract the best of talent. One example of how SWVL’s reputation has been impacted by this is this screenshot below of a LinkedIn interaction between a Swvl recruiter and an applicant (posted on Facebook).

Poor management of employee-startup relationships has also landed some startups in courts, which have, in some cases, turned out again them. This is particularly the case of iKOKOtv, which has been subject of such litigation cases in recent time. Just recently, a Nigerian court gave judgment against the company in a suit bordering on wrongful termination of employment, interpretation of a non-disclosure agreement, among others.

Rancorous Startup-Investor Relations

At most, a poor relationship with investors will succeed in giving both the investor and the startup big red flags before watchers-by.

This is certainly what HAVAIC, the prolific South African investor, understood when it recently called off a $4.45m court case against Custostech, a South African startup that protects content using blockchain technology.

Before calling off the case, HAVAIC was said to have signed a termsheet with Custos Media Technologies to close a convertible loan investment with Custos. All of the investment arrangements were agreed upon, and Custos confirmed that the terms had been authorized by their board, the venture capital firm said. According to HAVAIC, Custos then breached the agreement and opted not to proceed with HAVAIC’s investment. Custos’ CEO G-J van Rooyen, on the other hand, refuted this claim, claiming that the business did not sign any agreement with HAVAIC and that it was within its rights to reject its investment offer.

“We believe the founders and Custos have enormous potential to be internationally successful. Our preference is to restore the breakdown and work with the business to its full potential,” Ian Lessem, the CEO of HAVAIC said, before settling out of court with Custos.

Similar incident was reported at HealthPlus, a Nigerian healthtech company. According to founder Bukky George, she was lured to transfer 51.1% stake to a private equity investor, which she said, allowed the investor to oust her as the CEO of the company and replace her with another person.

Prior to the dispute, George owned 48.9% of HealthPlus, while the other investors owned 51.1 percent. However, this shareholding structure proved problematic. George stated that the investors committed to invest $18 million in the company, but only $10 million had been released since the deal was signed in 2018, meaning that the investors were not fully entitled to the 51.1% stake they claimed in the company.

Uganda’s Dunamiscoins’ recent scandal also represents the mounting cases of poor investor-startup relationships, misrepresentations and breaks in communication.

Notably, poor investor-startup relationship appears to be the most powerful internal startup conflict that tend to have crushing effects on startups, as it tends to shrink the chances of future access to funding for the startups affected.

Also notable is the fact that most investor-startup disputes are not largely reported for fear of the effects it would have on the startup’s funding journey as well as on the reputation of the investors.

Ethical Misconduct And Frauds Involving Startup Executives

This has the effect of not only destroying the reputation of the persons involved, but also has the effect of returning the operations of the startup to zero, especially if a major co-founder (the brain behind) of the project is involved.

This was disastrous for South Africa’s Springleap, a subscription-based platform for brands and agencies to source solutions for creative briefs. Springleap’s co-founder, Eran Eyal, was arrested in 2018 on the instructions of New York Attorney General on the grounds that he masterminded the stealing of $600,000 from investors — by fraudulently soliciting investors to purchase convertible notes through false representations about his company, Springleap.

Eran was found guilty in 2019 and was finally deported to Israel from the US in 2020. The huge effects the whole saga had on the startup could only be imagined.

Apart from fraud, sexual harassment has the effect of instantly killing the career of co-founders, if convicted. This would, in turn, push the startup into an entirely uncertain situation.

But for the exoneration of the CEO of Nigeria’s Tizeti, by an independent special investigation committee, from an allegation of sexual harassment, Kendall Ananyi’s career would have hit a brick wall, as was the fate of Kenya’s Alternative Circle, Anthony Kariuki and Ushahidi’s Daudi Were.

S/N

NAME OF STARTUPS

BASE COUNTRY OF OPERATIONS

YEAR FOUNDED

NATURE OF INTERNAL CONFLICT

YEAR CONFLICT WAS REPORTED

HOW RESOLVED

YEAR OF RESOLUTION OF CONFLICT

1

Safi Analytics

Kenya

2017

Kennedy Nganga, one of the ‘co-founders’ alleged that expat co- founders Lauren Dunford and Weston McBride dismissed him from the company immediately the company raised $1.8m, and after the failed to procure a negotiated exit from him.

2018

In April 2021, Nganga claimed that a crowdfunding campaign he initiated to institute a law suit against Safi was disapproved on M-Changa platform, one of Kenya’s crowdfunding platforms, citing his inability to meet the platform’s verification standards as one of the reasons for the rejection.

–

2

HealthPlus

Nigeria

1999

Founder Bukky George alleged that she was lured to transfer 51.1% stake to a private equity investor, which allegedly allowed the investor to oust her as the CEO of the company and replace her with another person. Mrs George owns 48.9% of HealthPlus, while the other investors own 51.1 percent. The reason for this is because the investors committed to invest $18 million in the company, but only $10 million has been released since the deal was signed in 2018.

2020

Under litigation

–

3

Cars45

Nigeria

2016

Co-founder, Etop Ikpe, Sujay Tyle alongside other executives (11 in total) left the company reportedly over squabbles related to equity structures and a potential buy-out. The squabbles started in 2019, a year after OLX Group invested over $400m in the company.

2020

Etop Ikpe has since proceeded to launch a rival company, Autochek.

–

4

Cellulant

Nigeria; Kenya

2014

Nigerian co-founder, Bolaji Akinboro resigned following reports of irregularities concerning post-audit results of the company’s platform, Agrikore. Also sacked were 35 employees for related offences.

2020

No reported case of how the conflict was resolved, but Bolaji finally left to found a new agritech platform, voriancorelli.com.

–

5

Risevest

Nigeria

2019

Former employee accused startup’s CEO of creating toxic work culture.

2021

CEO apologized, admitting that he mishandled the situation which culminated in the departure of the startup’s marketing lead from the company.

2021

6

Wejapa

Nigeria

2020

Developers accused startup CEO of extortion and underpayment for jobs and services they offered.

2020

CEO stepped down to allow for an independent investigation to be conducted. In the interim, co-founder and COO of WeJapa, took over the reins of the company.

2021

7

Gokada

Nigeria

2017

Co-founder, Deji Oduntan, resigned over unconfirmed reports of internal squabbles between members of the management team over funds management. In 2018, staff and software developers also exited the company enmasse, citing uncertainty about the company’s future. Ayodeji Adewunmi, Oduntan’s replacement (as Gokada President and Co-CEO.) also reportedly left the company in 2020.

2019

–

–

8

Ushahidi

Kenya

2018

Allegations of sexual misconduct against co-founder, Daudi Were.

2017

No official report, but co-founder proceeded to found a little known company Mikakati since 2018.

–

9

Tizeti (Wifi.com.ng)

Nigeria

2017

Allegations of sexual misconduct against CEO of the company, Kendall Ananyi, by a former Entrepreneur-in-Training at the Meltwater Entrepreneurial School of Technology (MEST).

2020

An independent legal counsel found, based on investigations, that no case of sexual harassment had been proved, a finding that was accepted by the Independent Special Investigation Committee. As a result, Tizeti’s CEO, Ananyi, has since been reinstated.

2020

10

Alternative Circle

Kenya

2016

Allegations of sexual misconduct against, against CEO Anthony Kariuki.

2017

–

–

11

Custos

South Africa

2014

Sued by investor HAVAIC. HAVAIC was said to have signed a termsheet with Custos Media Technologies to close a convertible loan investment by HAVAIC and its investors in Custos. All of the investment arrangements were agreed upon, and Custos confirmed that the terms had been authorized by their board, the VC said. According to HAVAIC, Custos then breached the agreement and opted not to proceed with HAVAC’s investment. Custos CEO G-J van Rooyen, on the other hand, refuted this claim, claiming that the business did not sign any agreement with HAVAC and that it was within its rights to reject its investment offer.

2020

Custos and HAVAIC reached an agreement on the 30th of November 2020. The dispute was said to have been settled in a friendly and discreet manner.

2020

12

Springleap

South Africa

2007

The New York Attorney General arrested founder Eran Eyal on August 23, 2018 and accused him the next day with stealing $600,000 from investors by fraudulently soliciting investors to purchase convertible notes through false representations about his company, Springleap.

2018

Eran was found guilty, in 2019, of cheating investors out of millions of dollars in three investment schemes, including a $42.5 million (R615 million) initial coin offering, by a New York court (ICO). He was finally deported to Israel from the US in 2020.

2019

13

WhereIsMyTransport

South Africa

2015

Internal employee squabbles suggested the company was in deep trouble, partly caused by mass retrenchment.

2018

Retrenchments occurred as a result of the company “going through a growth phase” and the necessity “to bring people of various experience into the business who are more focused on delivery and go to market,” according to WhereIsMyTransport.

–

14

iROKOtv.com

Nigeria

2011

By forming the firms known as africagent ltd. and freemedigital to operate the business of digital music distribution and offering other entertainment promotional services, iROKOtv.com sued former senior manager for breach of contract. According to iROKOtv, this is a violation of the non-compete and confidentiality duties outlined in the employee non-disclosure agreement signed by both parties on December 1, 2011.

2015

Court ruled against iROKOtv.com

2020

15

WiGroup

South Africa

2007

The company’s chief financial officer (CFO) resigned amid a “financial mismanagement” saga that struck the company. The incident unfolded just months after the company received funding from Virgin Group and retail solutions vendor Smollan to help it enter new and developed markets more quickly. The company had previously requested a forensic audit and as a result had been compelled to restructure its operations and downsize its workforce.

2018

–

–

16

SWVL

Egypt

2017

Several former Swvl employees, including the engineering team, gave Facebook testimonials regarding claimed cases of arbitrary dismissal, maltreatment, labor law violations, and a general atmosphere of discomfort and dread inside the company’s suburban Cairo headquarters.

2019

Founder has been making bold public relations moves to clear the allegations.

–

17

Dunamiscoins

Uganda

2019

Following 4,000 investor complaints, two of the company’s directors, Samson Lwanga and Mary Nabunya, were charged with 65 counts of collecting money under false pretenses and conspiracy to conduct a felony.

2020

Under litigation

–

18

Bitfxt

Nigeria

2016

Investor-startup squabbles that led to the startup $15m funding returned to the investors.

–

Funds invested repatriated to investors’ base.

–

19

Safeboda

Uganda

2015

Rancorous relationships with riders in Kenya

2020

Business operations shut down in Kenya.

–

Based on reported cases.

Some Time-tested Recommendations On Managing Internal Conflicts In Startups

Strong public relations strategies: A startup should have strong PR strategies that will assist in managing its public image. This includes establishing friendly relationships with the press, etc.

Placing all official communications under ‘CONFIDENTIAL’, ‘WITHOUT PREJUDICE’ or “SUB JUDICE” to prevent unfavourable communications from leaking to the public without consequences.

Timely and effective employee crisis management strategies. Strategies should be decisive, fair and not prevaricating.

Entering into standard contracts with co-founders with clear clauses on communications, vesting, cliff and exit periods.

Strict due diligence on investors before acceptance on offers and investments, especially if the investments will involve some significant dilution of founders’ equity.

Crisis management off public radar. Internal disputes should strictly be treated as internal affairs.

Unethical conducts should also be handled off public radar, if practicable.

Strong and professional leadership from the CEOs. CEOs should limit the frequency of unnecessary vituperations on workers.

Use cool-off period and rebranding if the situation created by an internal impasse becomes severely unfavourable to either the startups or the affected persons.

Africa startups conflicts Africa startups conflicts Africa startups conflicts Africa startups conflicts Africa startups conflicts Africa startups conflicts Africa startups conflicts Africa startups conflicts Africa startups conflicts

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Economic growth in Sub-Saharan Africa is estimated to have contracted by 2.0% in 2020, closer to the lower bound of the forecast in April 2020, and prospects for recovery are strengthening amid actions to contain new waves of the pandemic and speed up vaccine rollouts, according to the World Bank’s biannual economic analysis for the region.

The latest Africa’s Pulse, The Future of Work in Africa: Emerging Trends in Digital Technology Adoption, notes that a slower spread of the virus and lower COVID-19-related mortality, strong agricultural growth and a faster-than expected recovery in commodity prices has helped many African economies weather the economic storm induced by the COVID-19 pandemic. The report notes that economic recovery hinges on countries deepening reforms that create jobs, encourage investment, and enhance competitiveness. The resurgence of the pandemic in late 2020 and limited additional fiscal support will pose an uphill battle for policy makers as they continue to work toward stronger growth and improved livelihoods for their people.

Albert G. Zeufack, World Bank Chief Economist for Africa

“African countries have made tremendous investments over the last year to keep their economies afloat and protect the lives and livelihoods of their people,” said Albert G. Zeufack, World Bank Chief Economist for Africa. “Ambitious reforms that support job creation, strengthen equitable growth, protect the vulnerable and contribute to environmental sustainability will be key to bolstering those efforts going forward toward a stronger recovery across the African continent.”

Growth in the region is forecast to rise between 2.3 and 3.4% in 2021, depending on the policies adopted by countries and the international community. A second wave of COVID-19 infections is partly dragging down the 2021 growth projections, with daily infections about 40% higher than during the first wave. While some countries had a significant drop in COVID-19 infections due to containment measures adopted by the government, other countries are facing an upward trend in infections. Real GDP growth for 2022 is estimated at 3.1%. For most countries in the region, activity will remain well below the pre-COVID-19 projections at the end of 2021, increasing the risk of long-lasting damage from the pandemic on people’s living standards.

Sub-Saharan Africa’s recovery is expected to vary across countries. Non-resource-intensive countries, such as Côte d’Ivoire and Kenya, and mining-dependent economies, such as Botswana and Guinea, are expected to see robust growth in 2021, driven by a rebound in private consumption and investment as confidence strengthens and exports increase.

In the Eastern and Southern Africa subregion, the growth contraction for 2020 is estimated at -3.0%, mostly driven by South Africa and Angola, the subregion’s largest economies. Excluding Angola and South Africa, economic activity in the subregion is projected to expand by 2.6% in 2021, and 4.0% in 2022,

Growth in the Western and Central Africa subregion contracted by 1.1% in 2020, less than projected in October 2020 partly due to a less severe contraction in Nigeria, the subregion’s largest economy, in the second half of the year. Real gross domestic product in the Western and Central Africa subregion is projected to grow 2.1% in 2021 and 3.0% in 2022.

The Pulse also notes that African countries can speed up their recovery by ramping up their existing efforts to support the economy and people in the near term, especially women, youth and other vulnerable groups. Africa’s Pulse recommends those policies be complemented by reforms that fosters the country’s inclusive productivity growth and competitiveness. Reducing countries’ debt burdens will release resources for public investment, in areas such as education, health, and infrastructure. Investments in human capital will help lower the risk of long-lasting damage from the pandemic which may become apparent over the longer term, and can enhance competitiveness and productivity. The next twelve months will be a critical period for leveraging the African Continental Free Trade Area in order to deepen African countries’ integration into regional and global value chains. The report also notes that reforms that address digital infrastructure gaps and make the digital economy more inclusive–ensuring affordability but also building skills for all segments of society- are essential to improve connectivity, boost digital technology adoption, and generate more and better jobs for men and women.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

On January 20th, United States President-elect Joe Biden was sworn into office, ushering in a new administration, new foreign policy and a new approach to U.S. trade and investment in Africa. For its part, the Trump administration had not been short on growing U.S. private sector involvement in Africa, specifically under its trademark initiative, Prosper Africa. Designed to strengthen bilateral trade and investment, the initiative was launched in 2019 and supported by the Better Utilization of Investments Leading to Development (BUILD) Act. Signed by former President Trump in 2018, the BUILD Act consolidated the Overseas Private Investment Corporation (OPIC) and USAID’s Development Credit Authority into the U.S. International Development Finance Corporation (DFC), doubling the limit on investments from $29 billion under OPIC to $60 billion under the DFC.

United States President, Joe Biden

Serving as a critical instrument of American foreign policy, the DFC aims to mobilize private investment in emerging markets and generate returns for American taxpayers. Out of the $29.9 billion in active commitments globally, $8 billion has been directed to Africa alone, making it the second-largest recipient of investment following Latin America. With a rapidly growing, increasingly urbanized population – and associated needs for energy and infrastructure development – the African continent should be at the forefront of a U.S. investment agenda, in terms of developing a mutually beneficial, long-term relationship characterized by sustainable energy development and cooperation.

Advocating for Natural Gas Abroad

The African natural gas value chain represents a critical avenue for foreign investment and export opportunities, including the creation of onshore U.S. manufacturing jobs. The Total-operated Mozambique Liquified Natural Gas (LNG) project, for example, secured its largest share of senior debt financing from the U.S. Export-Import Bank, which aims to support U.S. exports for the development and construction of the LNG plant and create an estimated 16,700 American jobs over its five-year construction period. In terms of U.S. LNG exports, the relative proximity of certain sub-Saharan markets to North America renders the cost of transporting U.S. LNG to the continent as 20-40 percent less than transporting it to North Asia. As a result, the export market potential for U.S. companies looking to sell excess LNG supply to Africa – as a result of the country’s recent major investments in new liquefaction capacity – is substantial, coupled with Africa’s own large-scale energy needs.

As part of the Democratic Party platform, President Biden has targeted the elimination of billion-dollar oil and gas subsidies in the U.S. and called on other developed countries to do the same. While the proposition is unlikely to pass U.S. Congress, it suggests that the Biden Administration may follow the likes of Europe, in terms of restricting fossil fuel investment and signaling its commitment to climate change action. To date, U.S. oil majors (ExxonMobil, Chevron) have been less radical in their commitment to reducing carbon emissions and retooling investment strategies than their European counterparts (Total, Shell). If the U.S. can continue to lend support to gas development abroad – particularly in Africa, in which gas is positioned as a relatively clean burning fossil fuel able to deliver energy to scale – then it can cement its role as a leading provider of finance, infrastructure and technology to Africa’s energy transition.

Facilitating a Mutual Energy Transition

President Biden has been expectedly liberal in his stance toward a U.S. energy transition: in addition to once again committing the country to the Paris Agreement, he has pledged to transition the national economy to net-zero emissions by 2050, utilizing the revenues retained from subsidy cuts to fund a two-trillion-dollar climate action plan. That said, U.S. support of renewables should not be limited to the domestic market, and if the country plans to increase its fund allocation toward stimulating green business, then Africa represents a worthwhile recipient. The energy sector is already considered an investment priority by the DFC, attracting $10 billion in commitments to date.

In sub-Saharan Africa, total investment in power project development available to U.S. companies is estimated by Power Africa at $175 million. Meanwhile, universal electricity access by 2030 will require the construction of more than 210,000 mini-grids, mostly solar hybrids, connecting 490 million people at an investment cost of almost $220 billion, according to the World Bank’s Energy Sector Management Assistance Program. U.S. renewable-focused firms are well-equipped to meet African demand for renewable investment, offering an influx of technology, flexible capital and technical expertise, coupled with a free-market competition approach and reduced barriers to entry.

In addition to attracting external investment to reach continent-wide clean electrification goals, Africa is rich in minerals needed to fast-track the U.S. along its own energy transition. The Democratic Republic of the Congo, for example, is estimated to contain one million tons of lithium resources and is a global leader in the production of cobalt, copper, tantalum and tin. Such minerals are required to meet growing market demand for ‘green’ batteries that have the capacity to fuel U.S. clean energy by powering carbon-free grids, electric vehicles and green technologies.

Countering Chinese Influence

In terms of foreign policy, enhanced U.S. presence in Africa represents a strategic counter to Chinese influence, in the midst of an ongoing trade war between the two economic superpowers. The DFC offers a dynamic alternative to China’s Belt and Road Initiative, which has faced criticism due to its debt-heavy approach targeting government-to-government financing, along with its procurement to Chinese – and not African – firms and state-owned enterprises for the development of large-scale infrastructure projects. Criticism aside, China has been able to successfully extend its influence across the Global South because of the financial backing it receives from its government. Public sector support serves to alleviate perceived risk by providing a governmental vote of confidence – which the DFC has sought to do through reinsurance models that boost underwriting capacities and guarantees on behalf of American exports and contractors. Political risk insurance also seeks to protect U.S. investments against risk associated with currency exchange, expropriation, foreign government interference and breach of contract.

As it stands, bilateral trade between the U.S. and Africa is – for lack of a better word – underwhelming, decreasing from $31.3 billion in the first six months of 2019 to a paltry $12.7 billion over the same period in 2020. Last July, the U.S. began negotiations with Kenya over a free trade agreement targeting duty-free access for Kenyan goods to the U.S. market. If an agreement is reached – and it appears unlikely, given President Biden’s proclivity for multilateralism and his anticipated prioritization of the African Continental Free Trade Area – it could serve as a trading model for other sub-Saharan countries and to enhance commercial engagements. In short, the pieces of the puzzle for U.S. private sector-led growth in Africa are there; it is now up to the Biden Administration to put them together.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Vezeeta has come to Kenya, its first expansion into sub-Saharan Africa. The Middle East and North Africa e-health startup has expanded to the east African country by launching an app to help Kenyans access doctors from their smartphones.

Nana Frimpong, Vice President, Africa, Vezeeta

“Through our App and website, Kenyans will be able to access expert medical advice from the safety of their homes and receive professional guidance on identifying and dealing with COVID-19, without risking exposure,” said Nana Frimpong, Vice President, Africa, Vezeeta.

“As COVID-19 outbreak continues to present complex healthcare challenges to the public, we see our role and responsibility as a health-tech leader and trusted partner to ensure that the well-being and health of our patients remain uninterrupted,” noted Mr. Frimpong.

Here Is What You Need To Know

According to Nana Frimpong, Vice President, Africa, Vezeeta, the platform will provide Kenyans with an opportunity to access doctors across various disciplines on their terms.

Currently, the app has over 30 speciality areas that range from chest and respiratory, dentistry, dermatology, neurology, orthopedics and ENT among others with medical experts all registered under the Kenya Medical Practitioners and Dentists Council.

“We believe that through this initiative, we are supporting not only the Government of Kenya but also empowering Kenyans to make more informed decisions on their healthcare choices and improve access to doctors in general,” added Mr Frimpong.

With a global network of 30000 locally licensed doctors across 41 medical specialities, Vezeeta is present in 5 other countries — Nigeria, Jordan, Egypt, Saudi Arabia and Lebanon.

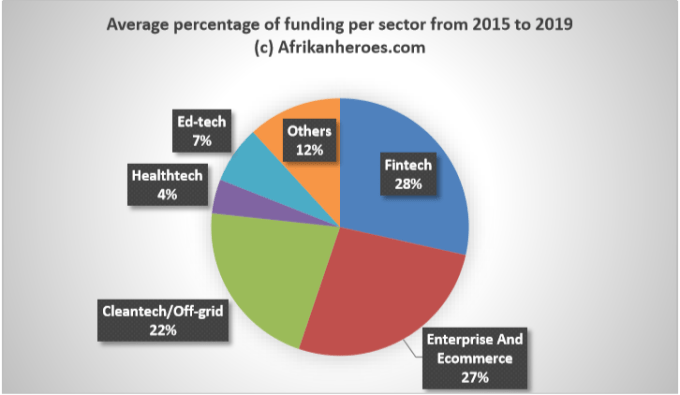

Chart 1: Prior to the coronavirus pandemic, percentage funding to African healthcare startups has been low. All data are as adapted from Partech Africa reports for the years considered.

Vezeeta has grown to become a mainstream digital leader of healthtech solutions, enabling patients to search, book and review the best doctors and medical services in just one minute. Currently operating in 50 cities across Egypt, Saudi Arabia, Jordan and Lebanon, the platform generates 4 million annual appointments, tripling year over year.

With the support of STV in 2018, Vezeeta was able to bolster its expansion plans primarily in Saudi Arabia.

“Leveraging our technology, we have helped patients tap into the power of choice, and the power of information, to access the kind of healthcare that our users deserve. We will continue to cater to local healthrelated pains while expanding our product portfolio to many more markets,” added Barsoum.

These growth plans underline the company’s commitment to creating value for patients and healthcare providers in emerging markets, by empowering them with data, ease of access and affordable solutions in healthcare.

“At Vezeeta, our vision is to make healthcare accessible, affordable and of better quality for all patients. This new development reaffirms the strength of our business, which continues to put patients at the heart of what we do,” said Mohammad ElMougi, Chief Product Officer, Platform, Vezeeta. “For this very purpose, we are aggressively growing our R&D team to reinvent the patient’s end-to-end journey,” he added.

“Doctors’ consultations and medication deliveries are key points of interests in healthcare. Medications alone account for 47 percent of the private healthcare opportunity, making ePharmacy a very exciting product,” explained Maha Melhem, VP of ePharmacy. “By providing a fully digitized pharmaceutical experience, we are able to eliminate the many middlemen that not only slow down the process but also hinder patients’ experience. Our multi-service ePharmacy channel is equipped to offer auto-refill services, medication reminders, seamless same-day deliveries and hassle-free secure online payments to all users, among other essential healthcare services,” she added.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

With a region as large and as vast as Africa, it is difficult to imagine a fully connected continent where every individual across all demographics and every business across all sectors can harness the power of cloud computing. Yet as technology continues to drastically change how we conduct our lives and connect with the world around us, this notion of a cloud-connected Africa becomes far more plausible and realistic.

In fact, many of us are already utilising cloud-enabled technologies on a daily basis. From cloud-based productivity apps to collaboration services like Microsoft Teams, the cloud is seamlessly integrating into our everyday lives. A future where a healthy cloud ecosystem is supported by integrated and innovative technologies is much closer than we think.

Enabling business continuity and growth

Given the current remote working environment, the value of cloud computing for local organisations can’t be emphasised enough. Apart from its geo-agnostic nature, the cloud is the best fit for today’s business landscape because of its scalability, flexibility and consumption-based charging model.

While being able to work from anywhere is key, this can be achieved through other, non-cloud-based technologies. However, the ability to rapidly implement and adapt in the cloud is what makes cloud-based solutions so valuable in our current business state. By driving efficiency and ensuring that employees are productive while working from home, cloud automation focuses workloads into the correct resource pools.

In turn, cloud services promote more streamlined operating systems and provide access to more markets and a wider range of service providers, helping companies reduce unnecessary costs and enable cost-effectiveness in the long run.

Connecting data centres to customers

As the demand for digital services continues to increase, the need for more processing power also grows, with more data centres setting up shop in our backyard. And, as more hyper-scalers position themselves throughout the continent, the technology industry is forced to find new solutions that will satisfy this hunger for the cloud. More sophisticated network architecture is required so that ISPs can find smarter ways to manage and orchestrate traffic between data centres and end-users.

Yet without reliable connectivity, no one can reach any cloud solutions, so there is also a responsibility on all ISPs to drive this penetration through Africa safely. Innovative products that are centred around cloud traffic are needed.

Thinking ahead

A fully connected Africa will, therefore, have intelligent networks, built on a foundation of stable and reliable facilities. In other words, the networking equivalent of a park-and-ride system with satellite navigation, ensuring traffic flow in peak hours and drivers finding the best routes to their destinations.

Reaching this desired connected state means a few critical things for our continent. Firstly, our connectivity will be on par with that of more developed countries. Secondly, it’ll enable any business to utilise the cloud and tap into the benefits of cloud computing unlocks, essentially allowing companies of all sizes in all sectors to do business easier. Thirdly, cloud capabilities will be able to be deployed closer to end-users, resulting in an increased uptake of cloud-based services for consumers.

Most importantly, however, a cloud-connected Africa could mean more job opportunities for parts of our population that previously couldn’t access work. And for a continent with high levels of poverty and unemployment, this is a massive win. If governments, businesses and entrepreneurs embrace the opportunities that the cloud provides, Africa could distinguish itself by using the cloud to drive growth and add value.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

As more African countries record cases of the rampaging Covid-19 disease caused by the Coronavirus, Facebook, in collaboration with the World Health Organisation, and the African Union, is making efforts to keep people informed of the developments. To tackle misinformation and the spread of fake news while keeping people genuinely informed is the reason behind Facebook’s expansion of the Coronavirus (COVID-19) Information Center across more African countries.

Facebook’s Director of Public Policy, Africa, Kojo Boakye

This expansion became necessary as part of the social media giant’s Coronavirus Information Center which will see 24 more countries in Africa covered in the ongoing commitment to empowering people around the world with timely and accurate news from trusted health authorities. The Coronavirus (COVID-19) Information Center is featured at the top of News Feed and provides a central place for people to keep informed about the Coronavirus. It includes real-time updates from national official sources, regional and global organizations such as the Africa Center for Disease Control and the World Health Organization as well as helpful resources – articles, videos and posts – and tips about social distancing and preventing the spread of COVID-19.

Facebook users can opt-in to the Center to get notifications and see updates in their News Feed from official government, regional or global health authorities. Facebook’s Director of Public Policy, Africa, Kojo Boakye, says: “Facebook is supporting the public health community’s work across the world to keep all communities informed during the coronavirus pandemic. We are happy to provide nearly every country in Sub-Saharan Africa with its own Information Center so people across the continent have a central place to find authoritative information around COVID-19.”

The new countries where Facebook is launching the Coronavirus Information Center are: Botswana, Burundi, Central African Republic, Comoros, Congo, Djibouti, Equatorial Guinea,Eritrea, Eswatini, Gambia,Guinea Bissau, Lesotho, Madagascar, Malawi, Mozambique, Namibia, Rwanda, Sao Tome and Principe, Sierra Leone, South Sudan, Tanzania, Uganda, Zambia and Zimbabwe

The Coronavirus Information Center is already in place in Benin, Burkina Faso, Cameroon, Cape Verde, Cote d’Ivoire, Chad Ethiopia,Gabon,Guinea,Kenya,Mali,Mauritania,Mauritius,Nigeria,Senegal,Seychelles,South Africa, The Democratic Republic of Congo (DRC) and Togo. Facebook said that this will help in no small way to ensure government and the people are on same age of information regarding the unfolding events.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Over the past months, I have been crunching company data, carrying out extensive reviews, and scheduling series of meetings with executives and officers of companies listed on stock exchanges as well as ordinary going concerns, all in a bid to help them reinforce their board effectiveness.

Paschal Doxie, former CEO, Diamond Bank

While profit making remains top on most companies’ priority areas, the final straw that often breaks the camel’s back is the companies’ failure to fulfill the demands of good corporate governance practices. That is, even with the right business strategies, the complex organisational structures of most companies sometimes reach a confusing peak that demands that the company have a rigid wall of governance and culture if it is to still maintain some appreciable level of sanity, survive or continue to make profit or contain losses.

For businesses or people resident in Nigeria, 2019 came with the revelation from Moody’s, the leading credit-rating and financial analysis agency, that the main reason why a foremost commercial bank in the country — Diamond — conceded to a merger with Nigeria’s leading commercial lender — Access Bank — was because of poor corporate governance practices adopted by the former. To quote a portion of Moody’s report, Diamond Bank’s weak governance structure meant:

A highly compromised board

A board with little ability to assess the bank’s risk exposure and;

And a board that failed to rigorously interrogate management over strategy.

Moody’s report is not entirely far from my experience reviewing companies’ board effectiveness. The points made below are meant to serve as a sneak-peek into the damage wreaked by weak corporate governance practices in most companies in Nigeria,and by implication Africa.

Total Absence of Good Succession Strategies and Plans

This is the most obvious emptiness you would find in most Africa n companies. There is often total absence of good succession plans or policies for top executives and senior management of companies. A succession planning policy is a tool that helps a company to be prepared for planned or unplanned absences of a director or other top management, which, among other things, clarifies authority and decision-making, thereby maintaining accountability and ensuring stability within a company.

Furthermore, a good succession planning policy of a company should also be able to predict where the next crop of directors or CEO of the company would come from, in order to avoid a situation where the company is suddenly ambushed by the emergence of little known persons who usually find it difficult gaining grounds within the first few years of takeover from present management.

From Moody’s report on Diamond Bank merger, we were able to glean that sometimes in 2018, there was a letter from Nigeria’s market research and analysis news site Proshare. The content of the letter simply was that a former chairman of Diamond Bank, Seyi Bickerstheth gave some hints on why Diamond Bank’s CEO, Mr. Pascal Dozie, should be replaced. The letter re-echoed the same demand from one of the biggest investors in the bank — Carlyle Group’s Carlyle Sub-Saharan Africa Fund (CSSAF) DBN Holdings — who also wanted Mr. Dozie shown the exit door.

“A key shareholder CSSAF DBN Holdings demanded an immediate removal of management, principally the CEO, but the Board favoured a less drastic approach to minimise disruption and also enable the Board secure new leadership,” Bickerstheth wrote in the letter. “After several discussions, the CEO of the Bank, who is also a representative of the second largest shareholder Kunoch Ltd agreed to resign effective January 3, 2019, but would not tender his letter to confirm his verbal notification.’’

This is a classic case of a poor succession planning policy in place. With a sound succession planning policy, it would have been easier to find a perfect replacement for the bank’s CEO who, from several reports, had already been compromised.

It is therefore necessary that every company in Africa, whether small or large should draft a detailed succession planning policy and appoint a committee (such as the governance, remuneration or nomination committee) to oversee affairs related to succession planning. Alternatively, the Committee should establish a succession plan that identifies critical executive and management positions, forecasts future vacancies in those positions and identifies potential managers who would fill vacancies. Vacancies will be filled from within or, in the event no viable candidate is available, on an “acting” basis while an external recruitment effort is conducted.

Weak Board Structures and Dynamics

This is unarguably, the strongest force that destroys a company even before it begins to make profit. From my experience, it seems most companies still revolve around powerful, god-like figures, without whom the company would struggle to exist. Truly so, if an individual is the strength of a company, in terms of finance or influence, it would be entirely difficult for the company to look stern when pointing fingers. But this is where the basic definition of a company resurfaces — a company is a person with a separate personality entirely independent of the promoters or the founders. A company with a very strong board structure or dynamics should be able to have these key essential features:

The Chairman of the Board should not double as the MD/CEO of the Board.

The Board shall consist of at least an executive, non-executive and an independent director in such a way that the number of non-executive directors shall be more than that of the executive directors. In fact, there is really no need appointing directors who are out of touch with practices in the relevant sectors the company are competing in. Apart from the fact that persons appointed to the board must be persons of proven integrity, they must also possess acute knowledge required of a person in that industry.

A good succession planning policy should be mindful of the fact that an ideal replacement period for each non-executive director is usually three years, although an executive director could stay on the board for a maximum period of three years of 4 years each, while the maximum period for an independent director should be 3 years of three years each. On their parts, MDs/CEOs’ tenure usually have an ideal maximum period of 10 years, which may be broken into periods, not exceeding five (50 years) after the expiration of his tenure as MD/CEO.

Quite obvious from my experience reviewing a number of companies is the practice of converting an existing non-executive director into an independent non-executive director. This practice is extremely unhealthy if the company is to survive. An independent director, in most cases, does not have any direct material relationship with the company; or in cases where they have some material relationship with the company, their equity interests in the company should not be more than 0.001% of the company.

Another instance of a weak board structure is the practice of filling a substantial portion of the board size with family and friends, who have little or no contribution or experience to bring to the board. A standard practice demands that not more than two members of a family shall be on the board of a company at the same time. The expression ‘family’ includes a director’s spouse, parents, children, siblings, cousins, uncles, aunts, nephews, nieces and in-laws. In the same vein, no two members of a family shall occupy the positions of Chairman and MD/CEO or Executive Director of the company and Chairman or MD/CEO of a company’s subsidiary at the same time.

Moody’s still offers us a classic example from Diamond Bank’s merger with Access Bank in this regard. According to the credit-rating agency, Diamond Bank failed because it did not have enough independent directors (the objective truth tellers) on its board and this resulted in a lack of effective board oversight.

By the end of 2017, only one of Diamond’s 13 board members met the Nigerian SEC’s definition of independent (another had retired in August),” Moody’s noted

“We believe Diamond’s board failed to provide an effective check against the bank’s management team. Board independence is important because it makes it more likely that management strategies are subject to rigorous questioning, reducing the risk of directors ‘rubber stamping’ management decisions.”

The implication of this is not far-fetched. Mr. Dozie, whose family was the second biggest shareholder in the bank, directly controlling 5% and another 9% indirectly through its investment firm, Kunoch Ltd (14% in total) was only 4% off the Bank’s biggest shareholder, Carlyle Fund, which controlled 18%. This meant, of course, a huge overbearing influence of one family over how the business of the bank was run. A striking example was the fact that a member of the founding family held the CEO role between November 2014 and March 2019 when it merged with Access Bank. During this period, profits fell by 78% in 2015 and bank deposits shrank by 22% between year-end 2014 and 2017.

Poor Board Processes And Oversight

From my experience, it appears that most companies do not seem to have a sound grasp of issues surrounding board processes and oversight. To begin with, there are certain committees a company must necessarily form. Chief among them are the risk, audit and corporate governance or remuneration committees. The absence of any of these committees must necessarily lead to a weak governance structure in the company. Consequently, for a company to have effective board processes and adequate oversight, it should be able to have these key essential features:

To make sure that there is some level of independence and checks and balances on the Committees, the Chairman of the Board/company shall not be a member of any of these committees stated above. All the committees must necessarily be headed by a non-executive director. In the same vein, the MD/CEO and other executive directors of the company shall not be members of the audit committee of the board as well as the committees on governance, remuneration or nomination.

Only those knowledgeable in risk management or audit shall be appointed to these committees. And as a matter of good practice, the board shall not replace members of the Board Audit Committees and External Auditors (not internal auditors) of the company at the same time.

The risk and audit committees must necessarily play some oversight functions on the company’s risk officer and internal auditor, and as a matter of good practice, both officers must report directly to the committees on risk management and audit respectively.

Boards of Companies shall ensure that the company’s risk management framework provides for regular and independent reviews of the risk management policies and procedures as well as periodic assessment of the adequacy and effectiveness of the risk management functions.

Moody’s particularly drew out a line here. It said Diamond bank did not attract enough corporate borrowers who are a major moneymaker for banks and that, well, it loaned out more money to the oil and gas sector than the Central Bank of Nigeria thought was prudent (52% versus 20%). So when oil prices fell in 2015 and 2016, the bank came crashing with it. This is purely a case of inadequate oversight over the bank’s risk management department by the bank’s risk committee. This is so because Moody’s noted that Diamond Bank’s weak governance structure necessitated: a highly compromised board; a board with little ability to assess the bank’s risk exposure and; and a board that failed to rigorously interrogate management over strategy.

Little Or No Adherence To Policies on Transparency and Disclosures

Although most companies tout themselves to be pro-transparency and disclosures, this is not often the case in reality. From my experience, a lot of information is still being buried or swept under the carpet by companies’ top management, in connivance, sometimes with the board. This is worsened by occasions of conflict of interests necessitated by the directors’ participation in the equity of the company. A transparent board should be able to disclose information about the each director’s interest or shareholding in the company, as well as his directorship in an another company, if any. It should also be able to disclose the exact cumulative years of service of each director, and that of the external auditor at the end of every financial year.

Again, the most common challenge being faced by most companies on transparency in Nigeria revolves around issues of financial reporting. This is the stage where usually all the books are cooked, especially when the appropriate structures for checks and balances are weak. As a matter of best practices, companies should adopt the following around their financial reporting efforts:

The board committee on audit must necessarily hold a meeting once in every three months of the financial year of the company and deliberations at such meetings must include, at least consideration of the quarterly reports of the internal auditor. The board committee on audit must as a matter of good practice, investigate all audit reports and resolve all issues arising from the reports.

At least once in a financial year, the Board Audit Committee should endeavour to hold a discussion with the head of the internal audit function and the external auditors without the presence of management, to facilitate an exchange of views and concerns that may not be appropriate for open discussion.

As a matter of standard practice, the tenure of an external auditor in a given company shall be for a maximum period of 10 years after which the audit firm shall not be reappointed in the company until after a period of another seven (7) consecutive years.

Recall that it is standard practice that the MD/CEO and all the executive directors of the company should not be members of the Audit Committee. The audit committee of the board should consist only of the Non-executive or independent non-executive director of the company.

A classic example of the effect of a poor governance structure found in a company

One notable abuse of these principles is found in Cadbury Nigeria Plc’s case. In 2006, Cadbury Nigeria filed with Nigeria’s Securities and Exchange Commission its annual report and accounts for years 2002 to 2005 which contained untrue and misleading statements. Investigations revealed that Cadbury Nigeria’s former chief executive officer (CEO), and its former finance executive director, had deliberately made overstatement of the company’s financial position over the course of a few years to the tune of between N13 to N15 billion in connivance with the Company’s heads of accounts, internal audit and sales operation and supported by the company’s board chairman.

Further studies revealed that the Audit Committee of Cadbury Nigeria consisted of 3 executive directors, against the standard practice described above. The head of internal audit and members of Audit Committee also failed in making proper recommendations to the board at meetings. They also failed to examine the auditor’s report to review and make appropriate recommendations on management matters with the external auditors. Luckily enough, the discovery of this fraud has to be the most timely intervention that saved the company from filing for bankruptcy, especially as it had actually made a loss totaling N5 billion during the period.

A classic example of the effect of a poor governance structure found in a company

Failure On Strategy and Planning

Finally, one recurring problem in most companies from my experience is the absence of any formal strategic framework for the companies. In the current era of disruption and innovation, not having any comprehensive policy on strategy is foolhardy. Any company that wishes to survive and adapt must strive to remain relevant through strategies. To this effect, the following best practices must be adopted and reviewed on yearly basis by boards of companies:

The board should adopt a plan detailing the strategic priorities for the company and how it expects this to be actualized.

It must also dedicate enough time to strategy planning and must as a matter of urgency define annually the most significant issues facing the company in order to build extensive regular discussion of these issues into the Board meeting agenda.

When this is done, the company’s performance, relative to the general state of the economy, is bound to improve.

The Bottom Line

Issues around a company’s failure or success is neither here nor there, since there are different economic, social or even political factors that may influence a company’s existence over a period of time, but the principles of building a sustainable company are almost always the same. Some of these principles as discussed above are so important that a company wishing to build a long-lasting legacy cannot do without them.

On the other hand, small companies seem, however, to be having a hard time understanding that a company is a separate legal entity from the owners, an issue which they must quickly address, if the future would be any near brighter for them.

Reviewing the effectiveness of every company’s board is a good way to start towards building a sustainable company in Africa.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based Lawyer with special focus on Business Law, Intellectual Property Rights, Entertainment and Technology Law. He is also an award-winning writer. Working for notable organizations so far has exposed him to some of industry best practices in business, finance strategies, law, dispute resolution, and data analytics both in Nigeria and across the world

Charles Udoh has worked with companies in insurance, finance, banking, leasing, investment funds as well as real estate to strengthen their board effectiveness. He could be reached at udohrapulu@gmail.com or charles@teamnominees.com

Africa lost one of its most vocal business voices over the weekend as Mr. Ali A. Mufuruki, 60 is one of Africa’s richest business moguls. A Tanzanian entrepreneur, philanthropist, public speaker and leadership coach succumbed to death in a South African hospital. Mufurki, who is a Henry Crown Fellow of the Aspen Institute Class of 2001 co-founded the Africa Leadership Initiative in 2002 with mission is to engage the energy and talent of emerging leaders in Africa in order to release their potential to build a good society for their nations. Mr. Mufurki is the owner, Chairman and CEO of Infotech Investment Group LTD, a family business that has interests in ICT, media, telecoms, private equity, retail and real estate across a number of countries in Africa and beyond.

Mr. Mufurki is the owner, Chairman and CEO of Infotech Investment Group LTD,

He is also the co-founder and chairman of the CEO Roundtable of Tanzania, a policy dialogue forum that brings together more than 100 CEOs of leading companies in Tanzania. This group engages regularly with the senior government leadership of Tanzania to find solutions for the country’s economy.

Ali Mufuruki is currently Chairman of the Boards of Msingi LTD (Kenya), Legacy Capital Partners Ltd (Tanzania); Trademark East Africa (Kenya), Chai Bora Ltd (Tanzania) and Vodacom Tanzania Ltd. He serves as Director on the boards of BlueTown Holdings Ltd (Denmark) and AMSCO (Netherlands).

Chairman of Vodacom Tanzania PLC,Chairman of Board of Trustees – National Environment Trust Fund, Tanzania, Chairman of Chai Bora Limited, Tanzania, and Co-Founder – Legacy Capital Partners LTD,Trustee – ATMS Foundation, Netherlands, Member of the Tanzania National Business Council (TNBC), Director of BlueTown ApS, Copenhagen, Denmark.

He has previously served as Chairman of The CEOs’ Roundtable of Tanzania, Member of the Board of Directors and Chairman of the Audit Committee of the Tanzania Central Bank Board, Member of the Board of Directors Technoserve, Inc. of Washington, DC, Chairman of Wananchi Group Holdings Kenya,Chairman of Mwananchi Communications LTD,Chairman of Air Tanzanian Co LTD,Co-Chairman, UK Parliamentary Commission of Inquiry into impact of UK Aid for Africa Free Trade Initiative (AFTI). He is also a Policy Fellow Resident at the Rockefeller Foundation Bellagio Centre 201. He previously sat on the Board of the Tanzania Central Bank where he was elected the first ever independent chairman of the Audit Committee. He also served on the Board of Directors of Technoserve, Inc. of Washington, DC and Nation Media Group of Kenya.

Mr. Mufurki has been at the forefront of promoting entrepreneurship in Africa, and he is a firm believer that Africa has all it takes to grow the continent into an economic powerpouse. At the Great Africans Getaway” hosted by Strathmore Business School this year, with the theme Transforming Leadership: What Africa needs. The event the first of its kind held by the Business School at the Great Rift Valley Lodge as part of an effort to bring together great Africans comprised of fellow Alumni, Business Executives, Governors and Senators to a fun filled golf tournament weekend held to partake in knowledge sharing and building strong networks.At the event, was able to share in his vast experience on what he thinks are Africa’s top 5 needs which can be executed if Africa has the right discipline.

He pointed out that Africa needs to believe/imagine something incredible almost impossible that can be done with confidence and with a plan which requires discipline, knowledge and collaboration. Mr. Mufuruki primarily attributed his talk to the ‘Venus and Serena’ film , which takes an unfiltered look into the remarkable lives of the greatest sister-act professional tennis has ever seen. In a sport (Tennis) where they were not welcomed, the indomitable Williams sisters faced the opposition with grace and courage not only breaking new ground for female and African American athletes everywhere, but dominating the women’s game for over a decade. The film tells the inspiring story of how these two women, against all odds, but the help of visionary parents, made it to the top.

Firstly Imagination: Africa needs to have a boundless vision of a future that is fantastic to the point of being crazy leading us to strive to be like the rest of the world if not better. Africa has what it takes to be a great continent all that is needed is to imagine ourselves as being great. We need to not limit ourselves but to let ourselves dream big.

Self-confidence: Africans should have the confidence to do things by itself other than delegate. Africa has a billion people and more reasons to be confident; it has more land and water than any other continent more minerals more bio diversity and more young people what then keeps us from being confident? For what we hold as a continent the world needs. Confidence is precious but then again very fragile and can be broken quickly.

Thirdly a bold Plan: It is great to invest in visions such as vision 2030 or even a greater vision 2050 that together as continents we can build our GDP. For no single country can make it by itself. Therefore Africa needs to make an impact, to plan together with all 54 countries to craft a plan for Africa and come up with ways to grow ourselves

Execution discipline: Africa needs to work hard, sacrifice have discipline. As a continent we need to avoid excuses and looking for ways to say that we can’t make it. In the end Africa needs to stop looking for ways to attain instant gratification all our effort must be put in for the goof of the continent.

Lastly “we need stay motivated and focused to understand the world around us to find direction to stay the course in the face of challenges, to seek perfection in everything we do to win”. Africa he said needs individuals to master the use and application of these tools. Not ordinary people but enlightened value driven extraordinary effective leaders. The continent still has enormous potential, and business leaders have a big role to play in unlocking it a lot of lessons could be learned from successful business leaders in Africa. “We therefore as a continent need to choose the best among us to lead developing more business leaders is crucial to Africa to address its big challenges” he said. He noted that the continent needs more specialized business schools such as Strathmore Business School; develop these kinds of leaders. African enterprises and business leaders should therefore be the part of the catalysts in developing business schools that not only expose executives to international best practices, but also adapt these to African business realities”.

Mr. Mufurki’s death has been variously described as a huge loss not only to Tanzania, Africa, but to the world. He graduated with a B.Sc. in Mechanical Design Engineering from Reutlingen University, Germany in 1986 and lives in Dar-es-Salaam, Tanzania with and his wife and four children.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry