The Central Bank of Nigeria has issued a series of new guidelines to govern how a holder of a fintech license in Nigeria may combine it with other types of fintech licenses in a holding company structure.

One notable feature of the new rules is that fintech companies in Nigeria, under a holding company structure, can now acquire controlling stakes in Nigerian financial companies, including fund managers, loan and credit companies, money brokerage companies, etc.

More specifically, CBN provides under Section 2.3 of the new rules that a Payment Service Holding Company (PSHC) is permitted to have only two hierarchies.

“Given the permissible level of hierarchies, the PSHC may have a subsidiary which is a parent to another subsidiary (intermediate company),” the new rules state.

“A PSHC may acquire controlling interest in any permissible financial and/or technological company, subject to prior approval of the CBN, where controlling interest represents a minimum of 51% of authorised share capital of the entity,” the rules add.

The Implications of The New Rules

The new rules imply that it is now possible for fintech companies in Nigeria to acquire controlling stakes in financial companies and expand the scope of their operations in the country. However, the key words from the latest guidelines are “any permissible financial…company… subject to prior approval of the CBN,” meaning that the CBN holds the decisive power to determine whether this is possible or not, and the extent of it.

Nevertheless, it remains unclear if instead of fintech companies in Nigeria relying most commonly on microfinance licenses to launch their operations in the absence of any of the payments licenses, they could now structure themselves under a holding company structure, permitting them to include traditional banks in their portfolios.

But then, again, the new rules are more particularly true for fintechs focused on mobile money operations, switching and processing or payment solution services.

The latest guidelines may be the much needed respite for mobile money operators in Nigeria. Under the CBN’s recently introduced rules for mobile money operations in Nigeria, holders of mobile money license are forbidden from undertaking activities, including granting any form of loans, advances and guarantees (directly or indirectly); accepting foreign currency deposits; dealing in the foreign exchange market except as prescribed in Section 4.1 (ii & iii) of the extant Guidelines for Licensing and Regulation of Payment Service Banks in Nigeria; insurance underwriting; accepting any closed scheme electronic value (e.g. airtime) as a form of deposit or payment.

The latest rules could now permit them, subject to CBN’s approval, to acquire companies doing any of the above activities under a holding company structure.

Although it is possible, before now, for companies in Nigeria to own stakes in Nigerian banks, the latest rules give new impetus to fintechs to make outright acquisitions of more financial companies in Nigeria, which could be a strategic way of increasing their product offerings above the limits permissible under the law in each case.

How Many Subsidiaries Must A Fintech Holdco Have To Be Approved By CBN?

According to the central bank, any fintech holding company must have at least two subsidiaries, which comprise a Mobile Money Operator (MMO) and a Switching firm, before it can be regarded as a Payments Service Holding Company.

Whatever activities conducted under this arrangement — whether the holdco desires to hold controlling interests, that is 51% or more of another fintech company or financial institution or simply to change back into a single license — requires the approval of the central bank.

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

For regulated fintech startups in Nigeria, there is a very quick way to kill oneself: fail to comply with the regulations of authorities. This is always seen in the barrage of revocation of licenses in recent times. Just before 2020 ended, Central Bank of Nigeria, the country’s apex bank, revoked the operating licenses of 7 fintech companies. This came immediately after it did a similar thing to 42 microfinance banks — a type of banking license usually, also, relied on by most fintech companies in Nigeria. Many reasons were given for that action by the CBN, but the most salient among them is that holders of the affected licenses failed to comply with the obligations imposed upon them by the apex bank according to the relevant laws.

In Nigeria, rules around bank-fintech partnerships are tough. Such fintech-bank partnerships require the approval of Central Bank of Nigeria. Image credit: True News

One such obligation which has more recently been pronounced by the CBN is the requirement of obtaining the bank’s approval before any fintech company in Nigeria can partner with a traditional bank. According to CBN’s circular, PSM/CIR/GEN/CIR/01/22, dated 9th December, 2020, “collaborations between licensed payment companies and other financial institutions in respect of product and services are subject to CBN’s prior approval.”

The direct implication of the above rule is that all classes of fintech companies in Nigeria with payment service licenses are required to seek and obtain CBN’s license first before partnering on any products or services offered by either.

There aren’t many fintech-bank partnerships in Nigeria yet, however one such partership is that between Kuda, Nigeria’s only digital bank and GT Bank and Zenith Bank. Under the partnership arrangement with the two banks, Kuda users can make over-the-counter deposits in these traditional institutions to fund their app-based accounts. There is also an existing partnership between Kuda and Access Bank, which allows its customers withdraw cash from Access Bank’s ATMs for free. Another example is Nigeria’s Piggyvest, a savings and wealth management platform, which partners with Wema Bank to create direct deposit account numbers for the fintech’s users. Now, under the CBN partnership regime, a prior CBN’s regulatory approval would be needed before the fintech companies above and the respective traditional banks could partner on any projects.

The partnership rule particularly looks harmful for fintech startups used to innovation and agility. Thus, it could be argued that if the rule had applied to wealth management startups such as PiggyVest, it would have been harder for them to migrate their existing customers from Providus Bank to Wema Bank within 24 hours (like they did) following the recent Central Bank of Nigeria’s directive to all banks in Nigeria to block all cryptocurrency trading accounts resident in Nigerian banks.

This rule could not apply to PiggyVest because it specifically applies to all “payment companies”, unless PiggyVest had previously procured approval from Wema Bank and had to simply switch over. If the rule had applied (as it would have if it were Paystack, Flutterwave or Interswitch), the startup’s agility with the migration to Wema Bank would have been hard to come by.

Although CBN’s rule on partnership may be of industry standards or may have been well intended, it substantially affects how fintech companies in Nigeria respond to new threats and opportunities. In Singapore, even though partnerships between banks and fintechs are subject to regulatory approval, if the arrangement relates to the provision of a banking business, or other business the conduct of which is regulated by the Monetary Authority of Singapore; or a business which is incidental to any of these; then there is no need for such approval.

Below is how bank-fintech partnerships are treated in other countries in Africa and in top global fintech destinations.

S/N

COUNTRIES

HOW FINTECH-BANK PARTNERSHIPS ARE TREATED UNDER COUNTRY LAWS

CURRENT PRACTICE

1

South Africa

South Africa’s Banks Act requires approval to be sought from the South African Reserve Bank (SARB) for contractual arrangements between a bank and a non-bank entity, where the parties undertake an economic activity that is subject to their joint control.

Although approval is required by most banks, fintechs do not encounter most challenges, partnering with local banks.

Article 96 of the Egyptian Banking Law, No. 194 of 2020 now requires outsourced service providers to be registered by licensed Egyptian banks. Generally, approval for partnership is required.

Fawry recently obtained approval to partner with an Egyptian bank. Partnerships moderately common.

Fintech-bank partnerships are established after fulfilling the requirements of local state laws. More specifically, under the Bank Service Company Act (BSCA), federal banking agencies have broadened their authority to control and investigate third-party service providers. In addition, the Federal Financial Institutions Examination Council’s (FFIEC) has released guidelines on financial regulators’ authority to investigate such technology service providers to banks. The Consumer Financial Protection Bureau (CFPB) has similar inspection and regulatory jurisdiction over financial institution service providers, including FinTech companies that offer services to those institutions.

Partnerships between FinTech entities and financial services providers have become common in the US

5

Singapore

Singapore’s apex bank, Monetary Authority of Singapore, generally requires approval for such partnerships, unless the arrangement is for the provision of a banking business, other business the conduct of which is regulated by the MAS, or a business which is incidental to any of these.

Partnerships or other arrangements with traditional financial services providers are common in Singapore

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

Nigerian central bank has issued a statement stating that it would gift N5 for every $1 remittance sent to Nigeria. The bank said the policy is part of efforts aimed at encouraging increase in inflows of diaspora remittances into the west African country. The policy tagged “CBN Naira 4 Dollar Scheme”, targets senders and recipients of international money transfers. The scheme which takes effect from Monday 8th March, 2021, will end on Saturday 8th of May, 2021.

“Accordingly, all recipients of diaspora remittances through CBN licensed IMTOs shall henceforth be paid N5 for every USD1 received as remittance inflow,” the bank said.

“In light of this, the CBN shall, through commercial banks, pay to remittance recipients the incentive of N5 for every USD1 remitted by sender and collected by designated beneficiary. This incentive is to be paid to recipients whether they choose to collect the USD as cash across the counter in a bank or transfer same into their domiciliary account. In effect, a typical recipient of diaspora remittances will, at the point of collection, receive not only the USD sent from abroad, but also the additional N5 per USD received,” the bank further stated.

CBN’s latest step comes on the heels of its recent order to Mobile Money Operators and Payment Switch providers to suspend the receiving of remittances or the integrating of their systems with International Money Transfer Operators (IMTOs).

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

By the stroke of a regulatory pen, Central Bank of Nigeria, the country’s apex bank, has swept away all investments made in cyptocurrency startups in the west African country. This is coming exactly a year after the country’s Lagos state government had declared a complete ban on ride-hailing services on its major highways. It is also coming barely four months after the country’s Securities and Exchange Commission, in charge of regulating investments and securities, had issued a statement, demanding that all traders in crypto assets must register with the commission. In CBN’s latest move, by a way of a letter signed by Bello Hassan Director of Banking Supervision and Musa I. Jimoh Director of Payment Systems Management Department, all commercial banks and financial institutions in the country have been ordered to close down all bank accounts associated with cryptocurrencies.

“Further to earlier regulatory directives on the subject, the Bank hereby wishes to remind entities that transacting or trading in crypto currencies or facilitating payments for cryptocurrency exchanges is prohibited,” CBN stated in the letter.

“Accordingly, all DMBs, NBFIs and OFIs are directed to identify persons and/or entities transacting in or operating crypto currency exchanges within their systems and ensure that such accounts are closed immediately.

Please note that breaches of this directive will attract severe regulatory sanctions.

This letter is with immediate effect,” the bank further added.

The End Of The Road For Cryptocurrency Startups In Nigeria?

The Nigerian cryptocurrency startup ecosystem is booming, but the worst hit by the new directive from CBN will be local cryptocurrency exchanges many of which have recently become emboldened by the recent statement from the Securities and Exchange Commission which latched some forms of order and legitimacy onto their operations. Apart from returning them to the old ways, the ban is a big dent on investments already made into the startups by investors (most of whom are foreigners). In 2020 alone, investments amounting to over $20m were poured into three Nigerian crypto-based startups— Yellow Card, Bitfxt, and Xend Finance — two of which are cryptocurrency exchanges.

Although Nigeria has been subtly regulating the country’s cryptocurrency market, this is one regulation that has hit home the hardest. The last directive from the central bank was in 2017 when it directed all Nigerian commercial banks and financial institutions never to act as cryptocurrency trading exchange. That directive, however, permitted them to host cryptocurrency trading exchanges run by companies or individuals in Nigeria as long as those exchanges or individuals complied with all rules relating to anti-money laundering and terrorism. (Worthy of note is that under both the 2017 and 2021 regulatory directives, Nigerian commercial banks were given far-reaching powers to decide who operated a cryptocurrency account or not.)

CBN’s latest move follows the most recent warning by South Africa’s Financial Sector Conduct Authority (FSCA) against the growing cryptocurrency scams in the country. The scams relate to one of the biggest Ponzi schemes pulled out by Mirror Trading International, a South African Bitcoin trading company. The company had promised investors a 10 percent monthly return on their investments in Bitcoin. However, on 22 December, 2020 in a letter posted on Telegram, the management of the company reported that they were deceived and that Chief Executive Officer Johann Steynberg of the company might have fled to Brazil. Around 28,000 local and global investors were consequently defrauded to the tune of $644 million.

Cameroon earlier this week also published its first national risk assessment (ENR) of money laundering and terrorist financing with support from the World Bank. The report indicated that over $290m cryptocurrency-linked transactions were made by ‘terrorists’ in 2018 alone.

“While certainty on the state of play of cryptocurrency activity — especially as it relates to the number of players and volume of transactions — in Cameroon is still very much limited in the absence of exhaustive report,” the report revealed, “intelligence reports on secessionist armed groups in English-speaking regions whose bank accounts had been blocked following the initiation of legal proceedings against them for financing terrorism, show that the armed bands are now using “ambacoin” cryptocurrency network to support themselves.”

“It is also not excluded that this funding tool is also used by other criminal organizations such as Boko Haram,” the report further added.

Given that Nigeria has yet to report any substantial scams involving cryptocurrencies, there are already insinuations in some quarters that the move by the central bank may not be unconnected with the recent #EndSars protests mainly waged by young people. At the peak of the protest, CEO and founder of the social media platform Twitter, Jack Dorsey, had called on his 4.7 million followers to donate Bitcoin in support, after the Nigerian government had blocked the accounts of crowdfunding platforms set up in support of the protests. By the time the protests ended, Bitcoin already constituted about 40% of the nearly US$400k raised.

The market for cryptocurrencies in Nigeria is big. According to a recent report by Paxful, a leading peer-to-peer bitcoin marketplace, Nigeria traded 60, 215 bitcoins in the last five years (2015–2016), valued at more than US$566m, making the country the second largest bitcoin market worldwide after the United States. Trade in bitcoin also surged the highest — volume (20,504.50) — in 2020, by Coin Dance’s report.

Crypto startups in Nigeria will be affected by the new rules to banks from the CBN.Paxful Nigerian naira (NGN) Volume USD Equivalent. Source: UsefulTulips.org

The days ahead would be tough for crypto startups in Nigeria who may be torn between staying back in Nigeria and going underground to the black market, or moving to other countries while targeting the Nigerian market. Paxful had stated that Ghana, Kenya, and South Africa remain its main markets in Africa apart from Nigeria. The report from Cameroon also showed that up to 31,000 units of cryptocurrency were purchased in that country by the end of September, 2018. The Financial Services Commission (FSC) of Mauritius has equally, recently, released a regulation making cryptocurrency trading exchanges now eligible for licenses. The FSC had released a 15 — page document outlining the new standards. This was the first time the government of Mauritius would be attaching legitimacy to the securities systems trading on tokens, although from the looks of the new licensing regime, the government appears not to be interested in fully regulating the market — although they still retain the power to revoke licenses and investigate fraudulent practices.

In the meantime, some facts are certain to happen: the act of trading cryptocurrencies in Nigeria will return to its black market days and a lot of staff working for the affected crypto startups may have to be retrenched. The lives of crypto trading exchanges are also hanging on the cliff: they may either opt to file for liquidation in Nigeria or explore other alternative markets. Bitfxt had already announced it is moving to Dubai, in the United Arab Emirates, which had recently passed progressive policies allowing foreigners to set up and own more than 51% of shares in companies without local sponsors —as well as shortened paths to citizenship for foreign skilled workers.

But first, the startups would have to spend some time moving their money resident in crypto-linked accounts in Nigerian banks to other destinations. That, too, would be an adventurous journey.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

crypto startups Nigeria central bank crypto startups Nigeria central bank crypto startups Nigeria central bank crypto startups Nigeria bank

It has emerged that the Central Bank of Nigeria (CBN) revoked the licenses of seven (7) payment service providers and one (1) switch service provider due to their inability to meet up with their statutory obligations and conditions, wherein they were formed. This was contained in an Official Gazette of the Federal Republic of Nigeria made available by the apex bank.

Although the statutory obligations that the affected firms failed to fulfil were not mentioned, however, the recent revocation might be connected to CBN’s renewed drive to strengthen and ensure a credible payment system in Nigeria amidst the new wave of Fintechs in the country offering varying but often nuanced services. It could be recalled that the CBN had approved new license categorizations for the Nigerian payment system.

In withdrawing the licenses, the apex bank said it did so in exercise of the powers conferred on it under Sections 60 and 62 of BOFIA, CAP B3, Laws of the Federation of Nigeria, 2004 to revoke the licenses of the payment service providers listed in Schedule I and the switch licence of payment services providers listed in Schedule II attached hereto. Central Bank sources say that the affected institutions will for a period of six months consecutively, cease to carry on in Nigeria, the type of business for which their licenses were granted.

The affected institutions are categorized into two schedules, with the first comprising of the 7 PSPs whose licenses were revoked, while the other comprised of a PSP whose Switch license was revoked. The seven affected payment service providers (PSPs) whose licenses were revoked as contained in Schedule I are; Easifuel Limited, Transaction Processing System (TPS), Grand Towers Limited, Paymaster Limited, E-Revenue Gateway Limited, Eartholeum Network Limited and Globasure Limited. While the sole payment service provider whose switch license was revoked is; 3Line Card Management Limited.

It is also pertinent to state that the affected firms are not barred from conducting businesses in Nigeria, however, their licenses to operate in their previous capacities as PSPs and Switch operator is what is revoked for the time being. According to an earlier modified guideline released by CBN two weeks ago, the minimum capital requirements to operate in Payment Service Providing and Switching/Processing capacities are N100 million and N2 billion respectively.

Some of the services provided by a Payment Service Provider and Switch operators include; POS terminal deployment and services, PTAD, Merchant/agent training and support, switching, card processing, transactions clearing and settlement agents etc.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Late August this year, one of Nigeria’s leading telecom companies, 9mobile, announced it has acquired the first ever payment service bank license from the country’s central bank, alongside Hope PSB and Moneymaster PSB. The payment service bank license will, among other things, enable it to launch a range of products, including mobile money services, among others. Barely four months after that event, the Central Bank of Nigeria (CBN) is back with yet another set of rules, this time relegating every fintech company still basking in the euphoria of possessing a “do-all” license to their respective playing fields.

“The Central Bank of Nigeria, in line with its commitment to promote a strong and credible payment system has approved new license categorisations for the payments systems,” a circular released by the CBN reads, in part.

What Do The New Rules State?

The new rules are nothing short of sending all fintech startups currently operating broadly using the Payment Service License into their respective territories, and then streamlining them according to what they can do and cannot do. Accordingly, four new groups have emerged, namely: switching and processing payment service providers; payment service providers involved in mobile money (MMOs); payment service providers involved in payment solutions (PSSs) ; and payment service providers under the regulatory sandbox.

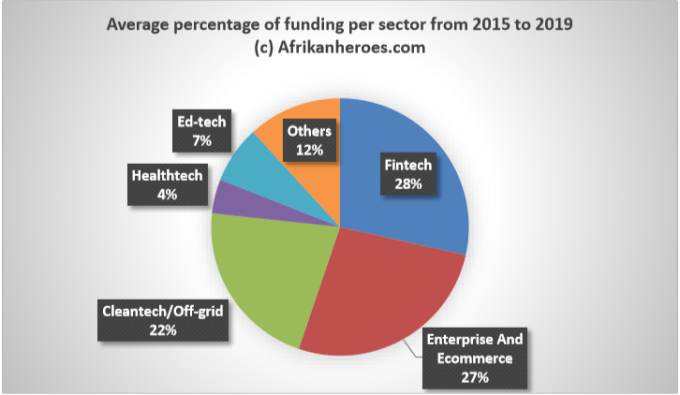

Sectorial VC funding, Africa. Data adapted from Partech

In Simple Terms, What May These New Groups Do And Not Do?

The implication of this new grouping is that one group may be forbidden from doing what other groups can do. To that effect, if you are a fintech startup under any of the groups, here is what you need to know:

Out of all the groups, only holders of a mobile money license can hold customer funds with them. Others cannot hold customer funds. In other words, mobile money services, at least to some extent, have the same status of a bank.

Where your startup wants to do both switching and mobile money operations at the same time, (like Interswitch doing mobile money together), your startup will need to set up a holding company, and make the companies engaged in switching and mobile money operations, separate subsidiaries (arms) of the holding company.

Companies which are payment solution service providers can hold a combination of payment service provider license, a payment terminal service provider or a super-agent at the same time.

The rules also state that before any startup within the group above can partner with any bank in Nigeria as regards the startup’s products and services, it must further get the approval of Nigeria’s central bank.

Type of License

Example Of A Fintech Company In Nigeria With This Type Of License

What Can Your Fintech Startup Do With This License?

What Is The Minimum Amount Required To Obtain The License?

Payment Solutions Services (PSSs)

Activities related to Super-agents, payments terminal service providers, payment solutions service providers

₦250 Million ($528K)

Super-agent

Innovectives; Flutterwave.

Recruit and manage agent networks, among other activities provided for in the Regulatory Framework for Licensing Super Agents in Nigeria

₦50 million ($132K)

Payment Terminal Service Provider (PTSP)

4ITEX Intergrated Systems

Deploys POS terminals; Own POS terminals; train merchants and agents

₦100 million ($264K)

Payment Solutions Service Provider (PSSP)

Paystack; Flutterwave

Offers gateway or portals for processing payments; Offers general payment solutions or develop payment applications software; or offers merchant services, aggregation or collection of payments

₦100 million ($264K)

Mobile Money Operation

MTN MoMo; 9PSB

Issues e-money; create and manage wallet, as well as manage pool accounts.

The Regulatory Sandbox Category is aimed at encouraging innovation and deepening financial inclusion. The CBN says it will review the products and solutions of applicants once the implementation of the Sandbox regime begins.

Not applicable

1 Dollar=₦380(official), December 11, 2020.Last Updated, Tuesday, May 25, 2021(9:00 AM)

The Implications Of The Above Tabulated Categories

According to CBN’s new rules:

A fintech startup in Nigeria can obtain a singular license called a Payment Solution Services License at ₦250 million, and this will allow the startup to do agency banking (Super Agent License); own POS terminals (Payment Terminal Service License) or own a payment processing portal ( Payment Solutions Service License). However, if the fintech startup does not have enough funds (₦250m) to go for the singular license that combines the three separate services, it can go for any of the three licenses (Super-Agent; PTSS; PSSs) separately.

Again, since a licensed mobile money fintech startup in Nigeria can hold customer funds , it is treated as a bank. Thus, where a startup wants to combine a mobile money banking license with any other type of licenses, it must set up a “non-operating” holding company. The holding company holds these other licenses, including a mobile money license under a subsidiary structure.

It is also possible for a startup under a holding company structure to acquire all types of licenses at the same time, provided that it maintains the minimum authorized capital thresholds for each of the licenses and obtains a no objection letter from the CBN’s Payments System Management Department created in 2018.

For startups without funds, the Regulatory Sandbox Category seems a sure bet, but CBN is yet to come clear on what criteria it will use to license fintech startups in this category.

It is worthy of note nevertheless that fintech startups in Nigeria have relied mostly on microfinance licenses than on any of these new groups. However, the new categorization rules are more particularly true for startups focused on mobile money services, switching, card processing and agency banking.

The deadline for complying with this new categorisation is 30th June, 2021.

To know more about the procedure for the new license categories, download CBN’s latest application guidance here (.pdf)

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

The Central Bank of Nigeria (CBN) recently released the guidelines that must be followed by individuals and businesses seeking to access the ₦50 billion ($139 million) targeted loan facility for households and Small and Medium Enterprises that are badly hit by COVID-19. Although there have been complaints from some quarters about the management of the fund, the central bank has further directed that there is no need to present any guarantor to be able to obtain the loan facility.

CBN governor Godwin Emefiele

“All successful Household and SME applicants who have submitted their account details for the CBN ₦50bn COVID-19 Targeted Credit Facility should expect their accounts to be credited within 48 hours of such submission, otherwise they should call 09010026900,” the bank stated in its most recent press release.

What Are The Requirements For The Loan?

To be able to apply to obtain the loan, every SME applicant must show, pursuant to the guidelines issued late March, 2020 ( and several other modifications), that:

That the business is an existing enterprise based in Nigeria (by presenting documents of registration of business or company as the case may be); OR that even though it has not commenced business, it has bankable plans to take advantage of opportunities arising from the COVID-19 pandemic but is short of adequate funding. However, it is highly improbable for businesses which have not commenced business already to obtain the credit facility because the CBN recently scrapped the requirement of business plan for purposes of procuring the loan. This is coupled also by the requirement of working capital discussed below. Nevertheless, such businesses can still try out their chances.

That the business operates in the following sectors: agriculture; hospitality (accommodation, hotel and food services); health (pharmaceuticals and medical supplies); and airline service providers; manufacturing/value addition; trading and any other income-generating activities as may be prescribed by the CBN.

That the business entity has been adversely affected as a result of the pandemic for businesses that are already in business before the Coronavirus pandemic. In determining whether your business entity’s account balance has been adversely affected by the pandemic as to qualify for the loan, CBN says your present year’s account balance (working capital) shall be, at most, 25% of the average of the previous 3 years’ annual turnover. In simpler terms, assuming your total annual turnover for the past three years is ₦900,000 and your current account balance is ₦150,000, you may not be considered for the loan because the average of the total turnover for the past three years (₦900,000) is ₦300,000 and CBN requires your business’ current working capital to be a maximum of 25% of the average of the working capital for the past three years. ₦75,000 is the 25% of ₦300,000 — the maximum working capital percentage required to process the loan. However, where the enterprise is not up to 3 years in operation, 25% of the previous year’s turnover will suffice.

The previous point implies that you must present your business’ financial statements for the past three years, as well as have, handy, tax clearance certificates for the said years.

The highest amount small and medium scale businesses can ever get under the scheme is ₦25m ($64,628); however the loan amount desired by the business entity would depend on the activity, cash-flow and industry size of the business.

No business plan is required to be able to procure the loan, apart from filling in the appropriate loan forms issued by NIRSAL. This is based on the CBN’s recent directive.

Nigeria ‘s COVID-19 loan facility is aimed at assisting small businesses to survive the pandemic. Image source: Nigerian Bureau of Statistics

How Much Is Charged As Interest On The Loan And Do I Need Any Guarantor And Collateral To Procure The Loan?

Interest rate

The interest rate on this loan is five percent (5) per annum, effective March 1, 2020. This is because of the CBN governor Godwin Emefiele’s earlier announcement of an immediate cut on interest rates of all applicable CBN intervention facilities from its former nine per cent (9%) following the outbreak of the COVID-19 pandemic in middle March, 2020. This also means that the interest on the facility shall revert to 9% per annum (all charges inclusive) as from 1st March 2021.

However, it should be noted that the Central Bank also gave further extension of the period of grace for the repayment of the loans by one year on all principal facilities, particularly intervention loans, effective March 1, 2020.

The combined implication of these is that the business entity will not start repaying the principal sum borrowed until after March 1, 2021, although it is still going to pay 5% per annum interest rate (all charges inclusive) on the facility. However, it should be further noted that the total duration of the loan shall not exceed 3 years, including the first year of the moratorium (that is, suspension of repayment of the principal sum) since the whole COVID-19 loan scheme will come to an end 31st December 2024. The NIRSAL Microfinance Bank is also given the power to work out a repayment schedule/work plan, convenient to it, at the application stage of the loan request.

Guarantor And Collateral

Guarantor

By the CBN’s latest modification to its earlier guidelines, SMEs applying for the ₦50 billion COVID-19 Targeted Credit Facility will not be required to provide guarantors before they can access the credit facility.

Collateral

It is entirely the decision of the NIRSAL Microfinance Bank which oversees the management of the facility to decide what the collateral for each facility would be. However, the range of collateral the bank may choose from include any one or more of the following:

By the terms of the guidelines, it is NIRSAL Microfinance Bank Plc that processes loan requests under the COVID-19 Targeted Credit Facility. So, all loan applications should be directed to the bank. The loan requests are submitted to NIRSAL Microfinance Bank with Bank Verification Number (BVN) with business registration documents stated above. NIRSAL Microfinance Bank appraises the applications and conducts due diligence on the application and, upon satisfaction, forwards it to the CBN which reviews and gives final approval for disbursement from the Micro, Small and Medium Enterprises DevelopmentFund to NIRSAL for on-lending to applicants.

Further enquiries may be made by contacting 09010026900–7 [Available: Monday to Friday (8am — 5pm)]; or by emailing covid19@nmfb.com.ng.

Are Applications Fees Paid Before Processing Loan Requests?

No! This is contained in one of CBN’s recent assurances. This was supposed to debunk an online article with caption “Central Bank of Nigeria Demands ₦10,000 from Small Business Owners Applying for COVID-19 Intervention Fund,” purportedly published by @SaharaReporters, on April 13, 2020. Consequently, there is no application fee for processing any such COVID-19 loan facility in Nigeria.

What You Should Do If Your Application For The Loan Has Been Declared Successful But You Are Yet To Be Credited

Successful applicants in Nigeria who are yet to receive the COVID-19 loan have been advised to visit here. Such applicants have also been notified to submit “their account details in any bank of their choice.”

However, the CBN has assured that all applicants to the ₦50 billion credit facility, who have successfully completed the application processes and submitted their account details, should expect credit alerts 48 hours afterwards. If an applicant does not receive credit alert after 48 hours of submitting their account details, such an applicant should contact the CBN by calling 09010026900.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer

As many people are now aware, the outbreak of the Novel Coronavirus Disease (COVID-19) in China has rapidly permeated and profoundly changed the world. While this crisis is first and foremost a public health issue, which has claimed the lives of over 123,600 people worldwide, and counting, the economic damages are unprecedented on several fronts: crude oil prices have declined dramatically to as low as US$17 per barrel by the end of March, even before applying the discounts many oil exporters are offering; stock valuations for the NSE-ASI, Nikkei, Dow Jones and FTSE-100 have declined by an average of 23.8 percent between January and March 2020; global airlines have lost about US$252 billion in revenues and across the broad range of industries from hospitality to services, the pain is growing. These outcomes have expectedly thrown the global economy into a recession, the depth and duration of which is currently difficult to fathom. In fact, the International Monetary Fund (IMF) predicts that the global economy would decline by 3 percent this year.

Godwin I. Emefiele, CON is Governor of the Central Bank of Nigeria

Around the world, countries have moved away from multilateralism and responded by fighting for themselves with several measures to protect their own people and economies, regardless of the spillover effects on the rest of the world. According to the World Customs Organization, a total of 32 countries and territories, adopted stringent and immediate export restrictions (https://bit.ly/34EmqxW) on critical medical supplies and drugs that were specifically meant to respond to COVID-19. As of 10 April 2020, an updated count of total export restrictions by the Global Trade Alert Team at the University of St. Gallen, Switzerland suggest a total of 102 restrictions by 75 countries.

On 4 March 2020, Germany announced an export ban that applied to all sorts of medical protection gear including breathing masks, medical gloves and protective suits. Around the same time, President Macron announced that France will requisition all face masks produced in the country, a de facto export ban. Between 8 February 2020 and 6 April 2020, India released eight (8) different export notifications banning several drugs and medical supplies including hydroxychloroquine, ventilators, personal protections masks, oxygen therapy apparatus, and breathing devices. On 3 April 2020, the Trump Administration invoked the war-era US Defense Production Act to stop major US mask manufacturer, 3M, from export of respirator masks, N95, to Canada and Latin America.

Fears of a long global recession have also led to worries about unprecedented global food insecurity, with concerns that agricultural production may be dislocated by containment measures that constrain workers from planting, managing and harvesting critical crops. Rather than seek cooperative and global solutions, several countries have resorted to export restrictions of critical agricultural produce.According to the International Food Policy Research Institute (IFPRI), about 37 countries have enacted various forms of food export restrictions in response to COVID-19, even in countries where average production exceeds domestic consumption.

For example, Viet Nam, the world’s third largest exporter of rice, suspended granting rice export certificates until the country “reviews domestic inventories”. Russia, the world’s largest wheat exporter, announced a ten-day ban on the export of buckwheat and rice due to concerns over panic buying in local supermarkets.

What if these restrictions become the new normal? What if the COVID-19 pandemic continues in a second wave or another pandemic occurs in which all borders are shut, and food imports are significantly restricted? What if we cannot seek medical care outside Nigeria and must rely on local hospitals and medical professionals? For how long shall we continue to rely on the world for anything and everything at every time?

Although these developments are troubling, they present a clear opportunity to re-echo a persistent message the CBN has been sending for a long time, and at this time even more urgently so: we must look inwards as a nation and guarantee food security, high quality and affordable healthcare, and cutting-edge education for our people.

For a country of over 200 million people, and projected to be about 450 million in a few decades, we can no longer ignore repeated warnings about the dangers that lie ahead if we do not begin to depend largely on what we produce locally, because the security and well-being of our nation is contingent on building a well-diversified and inclusive productive economy.

When I became Governor of the Central Bank in June 2014, imports of rice, fish, wheat and sugar alone consumed about N1.3 trillion worth of foreign exchange from the Bank. The immediate question that came to my mind was: can we not grow these ourselves? After all, only a few decades ago, Nigeria was one of the world’s largest producers and exporters of palm oil, cocoa and groundnuts.

Today, we import nearly 600,000 metric tonnes of palm oil, whilst Indonesia and Malaysia, two countries that were far behind us in this crop, now combine to export over 90 percent of global demand. In 2017, Indonesia earned US$12.6 billion from its oil and gas sector but US$18.4 billion in from palm oil. I believe that this pandemic and the immediate response of many of our trading partners suggest it is now more critical than ever that we take back control, not just control over our economy, but also of our destiny and our future.

In line with the vision of President Muhammadu Buhari, the CBN has indeed created several lending programmes and provided hundreds of billions to smallholder farmers and industrial processors in several key agricultural produce. These policies are aimed at positioning Nigeria to become a self-sufficient food producer, creating millions of jobs, supplying key markets across the country and dampening the effects of exchange rate movements on local prices.

This philosophy has been a consistent theme of the CBN’s policies over the last couple of years. At the 2016 Annual Bankers’ Dinner, I challenged the bankers that we needed to take decisive actions to fundamentally transform the structure of our economy. Throughout that speech, I talked about the damaging effects of Nigeria’s unsustainable propensity to import, and opined that it was high time we looked inwards and stopped using hard-earned foreign exchange (FX) to import items that we could produce locally.

This determination, therefore, formed the bedrock of the Bank’s policy, which restricts access to FX for importers of many items. These sentiments were re-echoed at the 2017 edition of the same Bankers’ Dinner, with specific examples of several companies that have benefited significantly from this policy of self-sufficiency. With President Buhari’s full support, we have continued to refine this policy to ensure that the best interest of Nigeria is served.Many times, the Bank has been accused of promoting protectionist policies. My answer has always been that leaders are first and foremost accountable to their own citizens. And if the vagaries of international trade threaten their wellbeing, leaders have to react by compelling some change in patterns of trade to the greater good of their citizens.

That is why in response to COVID-19, we are strengthening the Nigerian economy by providing a combined stimulus package of about N3.5 trillion in targeted measures to households, businesses, manufacturers and healthcare providers. These measures are deliberately designed to both support the Federal Government’s immediate fight against COVID-19, but also to build a more resilient, more self-reliant Nigerian economy. We do not know what the world will look like after this pandemic. Countries may continue to look inwards and globalization as we know it today may be dead for a generation.

Therefore, as a nation, we cannot afford to continue relying on the world for our food, education and healthcare. The time has come to fully transform Nigeria into a modern, sophisticated and inclusive economy that is self-sufficient, rewards the hardworking, but protects the poor and vulnerable, and can compete internationally across a range of strategic sectors.

In order to achieve this goal, we must begin immediately to support the Federal Government to:

1) Build a base of high quality infrastructure, including reliable power, that can engender industrial activity; 2) Support both smallholder and large scale agriculture production in select staple and cash crops;3) Create an ecosystem of factories, storages, and logistics companies that move raw materials to factories and finished goods to markets;4) Use our fiscal priorities to create a robust educational system that enables critical thinking and creativity, which would better prepare our children for the world of tomorrow;5) Develop a healthcare system that is trusted to keep all Nigerians healthy, irrespective of social class;6) Facilitate access to cheap and long-term credit for SMEs and large corporates;7) Develop and strengthen pro-poor policies that bring financial services and security to the poor and the vulnerable; and 8) Expedite the development of venture capitalists for nurturing new ideas and engendering Nigerian businesses to compete globally.

India is in a position to ban exports because it is producing critical drugs and medical supplies that the rest of the world needs. It also has companies that are global champions, and even making mergers and acquisitions in advanced nations. Why should this be out of our reach? We have the companies too; we have the manpower and some of the best brains in the world from the Americas to Europe and from Asia to Africa are Nigerians; driving global innovations in all fields. Nigerians are successful everywhere, and are already one of the most sought after immigrant groups in the United States.

But now is the time to seize this opportunity and create an environment that empowers our people to thrive within our own shores. To this end, the Central Bank has developed a Policy Response Timeline to guide our crises management and the orderly reboot of the Nigerian economy.

Immediate-Term Policies (0-3 Months)

In light of the fact that this crisis is an exogenous one thrust upon us without much warning, this phase reflects the government’s efforts at containment and mitigation. Although global cases are heading towards two million with over 123, 600 deaths as of 14 April 2020, we now have 343 cases, of which 10 deaths and 91 recoveries have been recorded. With President Buhari’s continuing strong leadership, Nigeria can now test 1500 persons per day in twelve (12) Molecular Test Laboratories. We believe that this strong leadership in travel restrictions, lockdown, social distancing, and other measures have been greatly effective to curbing the spread of the disease. More so, the Presidential Task Force and Nigeria Centre for Disease Control (NCDC) have helped the country stay ahead of the curve with increased testing capacity, provision of better-equipped isolation centres, and effective contact tracing. Within this milieu, the CBN has responded in several ways, first by supporting hospitals and pharmaceutical industry with low interest loans to immediately deal with the public health crises; then by working with the private sector Coalition Against COVID (CACOVID) to support the Presidential Task Force across its response, while mobilizing palliatives for the poor and vulnerable. Under this Immediate-Term Response, we have activated the following: 1) Ensuring financial system stability by granting regulatory forbearance to banks to restructure terms of facilities in affected sectors; 2) Triggering banks and other financial institutions to roll-out business continuity processes to ensure that banking services are delivered in a safe social-distance regime for all customers and bankers; 3) Granting additional moratorium of 1 year on CBN intervention facilities; 4) Reducing interest rates on intervention facilities from 9 percent to 5 percent; 5) Creation of N50 billion targeted credit facility for affected households & SMEs; 6) Strengthening the Loan-Deposit Ratio (LDR) policy, which is encouraging significant extra lending from banks; 7) Improving FX supply to the CBN by directing all oil companies (international and domestic) and all related companies (oil service) to sell FX to CBN and no longer to the NNPC; 8) Providing additional N100b intervention in healthcare loans to pharmaceutical companies, healthcare practitioners intending to expand/build capacity; 9) providing N1 trillion in loans to boost local manufacturing and production across critical sectors; and 10) Engendering financial inclusion by ensuring the poor and vulnerable are able, by all means necessary, through banks, microfinance, community and non-bank financial institutions, to access financial services to meet their basic needs.

Short-Term Policy Priorities (0 – 12 months)

As soon as President Muhammadu Buhari and the Health authorities determine our Coronavirus Transmission Curve is flattening and many of the ongoing restrictions are eased, this will be the phase for repositioning the Nigerian economic space. As part of the lessons from the current pandemic, we must ensure that that our value-added sector, the manufacturing industry is strengthened. Accordingly, the CBN will pursue the following policies in this phase: 1) Reinvigorate our financial support for the manufacturing sector by expanding the intervention all through its value-chain. In most cases, we will ensure that primary products sourced locally provide essential raw material for the manufacturing sector except where they are only available overseas; 2) With the support of the Federal Government, the CBN will embark on a project to get banks and private equity firms to finance homegrown and sustainable healthcare services that will help to reverse medical tourism out of Nigeria. By offering long-term financing for the entire healthcare value-chain (including medicine, pharmaceuticals, and critical care), banks will work with healthcare providers to consolidate on the current efforts to rebuild our medical facilities in order to ensure Nigeria has world class affordable hospitals for the people of Nigeria and those wishing to visit Nigeria for treatment; 3) The CBN will promote the establishment of InfraCo PLC, a world class infrastructure development vehicle, wholly focused on Nigeria, with combined debt and equity take-off capital of N15 trillion, and managed by an independent infrastructure fund manager. This fund will be utilized to support the Federal Government in building the transport infrastructure required to move agriculture products to processors, raw materials to factories, and finished goods to markets, as envisaged at the CBN Going for Growth Roundtable in March 2020; and 4) Continue to prioritize the provision of FX for the importation of machinery and critical raw materials needed to drive a self-sufficient Nigerian economy.

Medium-Term Policy Priorities (0 -3 Years)

Once the world returns to some new normal having tamed COVID-19 by a combination of vaccines and social distancing, and the Nigerian economy reopens fully for business, we will act quickly to enable faster recovery of the economy by targeted measures towards particular sectors that are able to support mass employment and wealth creation in the country. We will do so by focusing on four main areas, namely, light manufacturing, affordable housing, renewable energy, and cutting-edge research.

In manufacturing, for example, it is pertinent to note that Nigeria’s gross fixed capital formation is currently estimated at N24.55 trillion made up residential and non-residential properties, machinery and equipment, transport equipment, land improvement, research and development, and breeding stocks. Of this estimated value, machinery and equipment, which are the main inputs into economic production, are currently valued at only N2.61 trillion. In order to pursue a substantial economic renewal, including replacement of at least 25 percent of the existing machinery and equipment for enhanced local production, we estimate at least N662 billion worth of investments to acquire hi-tech machinery and equipment. Therefore, the CBN will consider an initial intervention of N500 billion over the medium term, specifically targeted at manufacturing firms to procure state-of-the-art machinery and equipment and automated manufacturing models that would fast-track local production and economic rejuvenation, as well as support increased patronage of locally processed products such as cement, steel, iron rods, and doors, amongst several other products. The recent private sector investments in cement production using enhanced technology and automated manufacturing models is a good example of the kind of economic renewal we will be pursuing in this phase. We will develop a thorough screening process and stringent criteria for equipment types that would qualify for funding under this phase.

In order to boost job creation, household incomes and economic growth, we will be focusing our attention to bridging the housing deficit in the country, by facilitating government intervention in three critical areas: housing development, mortgage finance, and institutional capacity.We will pursue the creation of a fund that will target housing construction for developers that provide evidence of profiled off-takers with financial capacity to repay. The current identification framework in the banking sector using the bank verification number (BVN) will be used to verify the information provided by the off-takers before the developer can access the funds. We will also be considering ways to assist the Mortgage Finance Sub-sector as well as build capacity at the State levels for their land administration agencies to process and issue land titles promptly, implement investment friendly foreclosure laws and reduce the cost of land documentation, as this has remained a major inhibiting factor in the provision of affordable housing in the country.

Over the next 3 years, we will also support the financing of environmentally friendly energy production, as this has a tangential long-term health benefits. We will look at efforts to drive innovation and research in every sector, through our universities, research institutions, creative industry initiatives, and all other media of novelty and inventions.

In conclusion, I believe we must now envision and work toward a Nigeria with the cutting edge medical facilities to provide world class care to the sick and vulnerable; enable our universities and research institutions to provide the requisite education and training that is required to keep these ecosystems functioning sustainably and efficiently; and millions of Nigerians employed in meaningful and well-paying jobs. This is the Nigeria that we must aspire to build. COVID-19 may have plunged us into a crisis of unprecedented proportions. But, as Winston Churchill once admonished, we must never let a crisis go to waste.

– Godwin I. Emefiele, CON is Governor of the Central Bank of Nigeria

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Preliminary disruptions of the international crude oil market and its ancillary effects as a result of the Covid-19 pandemic has forced the hands of the Nigerian government t take two tough decisions in a space of 48 hours. First was the reduction of the fuel pump price from N145 per litre to N125 per litre. The second was the devaluation of the country’s currency; naira from the official N307 to N360 to a dollar, with aim to achieve a uniform exchange rate, ditching a formula of dual to multiple exchange rates which has drawn the ire of many critics and economic analysts over the years.

The Central Bank of Nigeria, in a rather surprising move announced the migration of the exchange rates to a single exchange rate for the naira by collapsing the multiple exchange rate policy that determined the value for the local currency. Sources at the apex bank say that this decision was forced on the bank after the global coronavirus pandemic more than halved oil prices, raising pressure on the currencies of crude-dependent economies like Nigeria, Africa’s largest producer of the commodity. The action of the Bank thus weakened the official exchange rate by 15% to 360 naira per dollar from 307 naira. The rate for foreign portfolio investors was also altered, to 380 naira per dollar from 366 naira.

With the merging of the official rate, the rate for investors and exporters and rate for foreign-exchange bureaus are the first steps among others, according to the people, who asked not to be identified because they are not authorized to speak publicly about the matter.

Nigeria’s system of multiple exchange rates aimed to control demand for dollars following the collapse of oil prices in 2014. The official rate supplies cheap foreign exchange to government departments and select companies, including fuel importers. After its last devaluation in 2017, the central bank created an investors and exporters window, which allowed for some movement, but was closely managed by the regulator. The naira has come under tremendous pressure since oil prices slumped to around $30 a barrel, below the government’s $57 target. Earnings from sales of crude account for 90% of foreign-exchange earnings and more than half of government income.

A weaker official rate will give a big boost to the revenues of the federal government and states by allowing dollar earnings from oil to be converted to naira at a higher rate. It will also, however, increase the value of the government’s foreign liabilities in local currency. Changes to the exchange regime were welcomed by analysts and investors, but they may not be enough to ease pressure on the naira just yet.

Even at N360 to a dollar, some analysts feel that there will still be another shift closer to N400 to a dollar as market indices does not support a stronger naira at the moment. The blamed the inefficiencies and complexity of Nigeria’s exchange rate system made it prone to corruption, welcoming this move and hope the Central Bank will have the will power to do what is needful instead of falling to the whims of political interference.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Nigeria’s Central Bank of Nigeria (CBN) has dismissed insinuations over the devaluation of the naira, which has triggered panic in the FX Market, bringing the local currency down to N400 per dollar. Panic gripped the forex market on Thursday, throwing the Nigerian naira to N400/dollar on the streets.

CBN governor, Mr Godwin Emefiele

“The Central Bank of Nigeria wishes to note with displeasure the rumours and speculative activities of unscrupulous players in the foreign exchange market, borne out of the impression that the CBN is on the verge of devaluing the naira and triggering panic in the FX market. These rumours are false, unwarranted and calculated to serve their dubious and selfish ends,’’ the apex bank said in a statement.

Here Is All You Need To Know

The CBN alleged that the displeasure, the rumours, and speculative activities are from unscrupulous players in the foreign exchange market.

Admitting that the outbreak of the Coronavirus has led to the global economic slowdown, fall in the price of crude oil, and less inflow of dollars into Nigeria, it stated that the size of Nigeria’s foreign exchange reserves remains robust and comfortable, given the current realities of Nigeria’s genuine and legitimate FX demand.

Nigeria’s foreign reserves currently stands at $36.2 billion.

“We therefore wish to state that we have begun a robust and coordinated investigation in collaboration with the Nigerian Financial Intelligence Unit and related agencies to uncover the unscrupulous persons and FX dealers creating this panic, and the full weight of our rules and regulations will fall on them, including but not limited to being charged for economic sabotage. “The size of Nigeria’s foreign exchange reserves remains robust and comfortable, given the current realities of Nigeria’s genuine and legitimate FX demand.

“As such, the CBN remains able and willing to meet all genuine demands for foreign exchange for legitimate transactions. “In light of current circumstances and macroeconomic fundamentals, the CBN has not devalued the naira.

“Consequently, the CBN will invoke the full weight of applicable sanctions on any persons and authorised dealers found to be involved in such disruptive and speculative market behaviour,” the statement reads in parts.

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions.

He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance.

He is also an award-winning writer.

He could be contacted at udohrapulu@gmail.com