Stripe, the fast growing mega payment company has said that it will take its mission to “to increase the GDP of the internet” and build the “economic infrastructure” of the online world to the next level as it plans to be a $100 billion fund for small businesses. Established by two brothers, Patrick and John Collison and today a company with millions of global users, more than 40 of whom do $1 billion-plus a year in transactions using the Stripe platform.

Stripe founders, Patrick and John Collison

The brothers became two of the world’s most successful entrepreneurs by starting a payments company aimed at pleasing developers—the coding carpenters of the internet’s landscape. Stripe was a hit with startups, soothing as it did the headaches that come with getting paid over the internet. Since then, the company’s pitch has evolved to include multiple services that make it more of a one-stop-shop for running a business. Customers can use Stripe’s credit card fraud detection service, or its Atlas product to form a company in Delaware. This month, Stripe launched its Treasury product in partnership with the likes of Goldman Sachs; platform companies like Shopify, an e-commerce firm, can use it to offer bank accounts to their merchants.

Meanwhile, the Collison brothers are climbing the Forbes list of global billionaires, which currently ranks them around No. 900, worth $3.2 billion each. That accounting may soon be out of date. In a new funding round under discussion, Bloomberg reported Stripe could be valued as high as $100 billion, about triple its valuation in April. Covid-19 body-slammed most of the global economy, but not Stripe. Lockdowns and social distancing accelerated the shift from cash to digital payments, according to just about everyone, and that benefits companies like Stripe. During the first half of the year, US online retail spending hit $347 billion, according to McKinsey (pdf), a 30% jump from the same period in 2019.

Investors, meanwhile, are rabid for firms that can grow in the online economy, and the US market for tech IPOs has taken off accordingly. Hedge funds and sovereign-wealth funds are scrambling to get in on the action by buying shares in private companies, like Stripe, before they go public: Bids for pre-IPO shares of Stripe in the secondary market have skyrocketed, according to Liquid Stock data.

Bids for pre-IPO shares of Stripe in the secondary market have skyrocketed, according to Liquid Stock data. Stripe execs don’t appear to be in any rush to file IPO paperwork. But the hiring this summer of CFO Dhivya Suryadevara, formerly of General Motors, was fodder for speculation that a listing could come sooner than the Collison brothers are letting on. Stripe doesn’t comment on why Stripe doesn’t accept PayPal, one of the world’s most-downloaded payment apps and a key pioneer of internet commerce. But it seems obvious: The companies are rivals, and, as Patrick’s conversation with Thiel shows, the brothers have targeted the 22-year-old PayPal since their operation’s early days.

One of Stripe’s main competitors is Braintree, which PayPal bought for $800 million in 2013 when PayPal was still part of eBay. The deal included Venmo, an acquisition that gave PayPal a fast-growing mobile-payments service that’s popular with the millennial set. But Braintree’s payment platform was also a gem—it provided transaction plumbing for the latest generation of internet companies like TaskRabbit and OpenTable. Fast forward to 2020 and those companies are counted as customers on Stripe’s website.

Adyen is another big rival. The Dutch payment company was founded in 2006, and its market capitalization of nearly $70 billion—up from $8 billion during after its IPO in 2018—puts it among Europe’s most valuable tech companies. Valuations for Stripe and Adyen have tended to hover in the same territory, and they are increasingly going head-to-head for customers with major global operations. When it comes to merchant payments, Stripe and Adyen “lead the pack,” according to a report in September by Forrester. The research firm gave Stripe a slight edge when it comes to current offerings and strategy.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

Nigerianfintech startup Paystack which was recently acquired by American giant Stripe has entered into a partnership with Google to empower at least 500,000 Small and Medium-Sized Enterprises in Nigeria, Kenya and South Africa, via the Google Economy Recovery Program for SMEs. Paystack in a statement posted on its official Twitter handle said that the partnership is to help the SMEs “restart, recover and digitize their businesses with new tools, financial support and training.”

Shola Akinlade, Co-Founder of Paystack

According to Shola Akinlade, Founder of Paystack, the partnership with Google would enable reliability, “which would guarantee that all businesses paid via Paystack are thoroughly checked for legitimacy and credibility. In a low-trust environment like Nigeria, where many people are paying online for the first time, it’s important to deliver a safe, fraud-free experience. This is a responsibility that Paystack takes extremely seriously.”

Paystack’s partnership with Google will help SMEs to grow and digitize their businesses with new tools, financial support, training and help businesses in the selected African countries – Nigeria, Kenya and South Africa to grow and expand their country’s economy. It will further help businesses bring their ideas to market and grow their online sales, using Paystack’s collection of simple, powerful commerce tools. In 2018, Paystack partnered with other tech-based platforms like Truecaller, a smartphone application that has features of caller-identification, call-blocking, flash-messaging call-recording and more to facilitate online payments across the African continent.

The partnership with Truecaller involves using Truecaller’s database of verified phone numbers to verify payments for transactions performed on their platform. Paystack and Google share a lot in common, especially their dedication to helping businesses in Africa find growth by leveraging technology to provide them with the essential tools needed to find more customers and grow online sales.

Kelechi Deca

Kelechi Deca has over two decades of media experience, he has traveled to over 77 countries reporting on multilateral development institutions, international business, trade, travels, culture, and diplomacy. He is also a petrol head with in-depth knowledge of automobiles and the auto industry

When Ezra Olubi set out to build a little known payments startup in 2015, alongside his university school mate, Shola Akinlade, he never knew that it would five years later be bought for $200 million. But that has happened!

In a remarkable African startup exit, exciting for American investors who constituted more than 40 percent of all venture capital investments on the continent between 2014–2019, Silicon Valley-based payments and software-as-a-service company, Stripe, has acquired Olubi’s startup, Paystack, in a deal reported to be worth more than $200 million.

While this is a huge entrepreneurial respite — and of course real cash — for him, the journey to building one of Africa’s strongest fintech companies has just begun.

“I quit my job in 2015 so I could work on Paystack,” Olubi said. “My friends and family definitely weren’t surprised. They were like: ‘Oh, he’s doing another new thing again!’ I’d been working with startups for pretty much my whole career until that point anyway. I’d always chosen startups instead of jobs with high salaries at big-name companies.”

L-R: Paystack co-founders, Ezra Olubi and Shola Akinlade. Photo Credit: Brent Franson for Paystack

With the excitement of a major Nigerian startup acquisition still raging on, a few insights into Paystack’s success may be helpful.

Building A Local Solution With A Global Mindset

By industry stereotypes, Paystack’s founders Shola Akinlade and Ezra Olubi could easily have been dismissed as high-risk investments. Both founders studied in Nigeria, with some of the lowest ranked educational institutions, and have equally lived much of their lives in the West African country. And so there is every reason to doubt their capacity to deliver good returns on investments. Which is why both founders instantly sought to first plug the startup into the global ecosystem before deeply treading the startup path.

“After starting the company, the first thing Shola and I did was apply for Y Combinator,” said Olubi. “It seemed like a really farfetched idea. I remember thinking: ‘There’s no way we can get into this program. We’re just a couple of young guys in Nigeria.’ We got rejected the first time, but we applied again and were accepted. We were the first ever startup from Nigeria to enter the program. It was a surreal time in my life. Firstly, because I had never traveled outside of Nigeria before. Secondly, because being accepted into the program was strong validation. I knew we needed to do everything possible to make the most of this opportunity. That meant a lot of learning — fast.”

Without meaning to deter intending startup founders in Africa, it is noteworthy to point out that there is always some “herd mentality” surrounding globally validated startups. Paystack’s validation by Y Combinator was a deal breaker. It gave room for immediate funding to the startup from global giants like Tencent, Stripe, Visa, among others.

But that was 5 years ago and things have changed. In as much as Y Combinator is still glamorised, there has been a consistent rise in the number of venture capital firms and accelerator programs across Africa.

The success of Paystack’s founders, nevertheless, marks a watershed in the Nigerian startup ecosystem, for it is the first time a startup founded by purely local talents will be witnessing the biggest startup acquisition in Nigeria.

Therefore building a local solution with a global mindset is crucial.

When It Comes To The Biggest Startup Acquisitions In Africa, Investors Are Biased Towards Fintech

Paystack’s high-figure acquisition is a confirmation of investors’ bias towards fintech in Africa. Record number of fintech startups have been acquired in Africa within the shortest period of time after they were founded. From Sendwave to Beyonic, the table below captures it clearly.

“It is really pattern recognition; they see the kind of deals that have happened in the past and they try to mimic that,” said Jean-Claude Homawoo, Co-founder & Managing Partner, Lori. “They (investors) look for the same makeup over and over again. So for founders that don’t look like those…in the past there is a hurdle.’’

It is therefore relevant that startup founders acquaint themselves with the sectors that have attracted the most acquisitions in Africa in the past. Although this may be one of the earliest guiding principles in choosing which startup idea to pursue, market size, market fit and strikingly innovative solutions (check out South Africa’s SweepSouth, for instance) and overwhelming passion from founders have always dragged investors’ interests into new areas.

However, since startups are themselves largely untested territories (considering that a majority of them have not existed for an appreciable length of time nor have they been affected by policy changes or market trends), investors tend to stick more to sectors that have proven to return most highly on their investments.

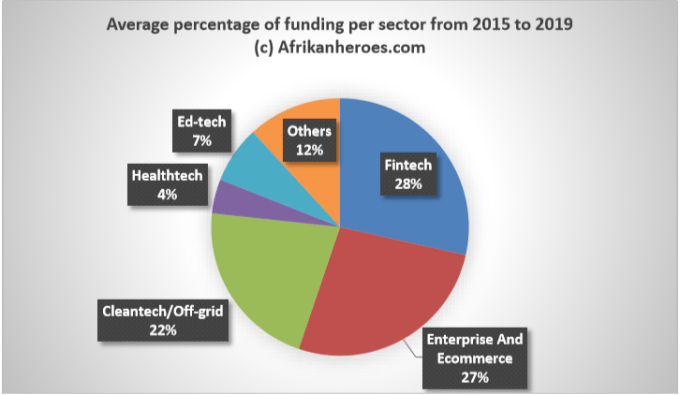

Apart from recording the highest number of high-figure acquisitions in Africa, fintechs have also topped the chart for venture capital funding in Africa. In 2019 alone, out of a total of 250 deals amounting to a record-breaking $2.02 billion reported by data firm Partech, financial technology companies (fintech), at 41%, received the lion’s share of the whole investment sum.

Percentage funding to African startups between 2015–2019. All data are as adapted from Partech Africa reports for the years considered.

S/N

Name of Company

Sector

Year Founded

Year Acquired

Value of Acquisition

Acquirer

Country

1

Sendwave

Fintech

2014

2020

$500m

WorldRemit

US; Kenya

2

Beyonic

Fintech

2006

2020

Undisclosed

MFS Africa

Uganda

3

Apposit

Software Development

2017

2020

Undisclosed

Paga

Ethiopia

4

Harmonica

Online dating

2017

2019

Undisclosed

MatchGroup

Egypt

5

StarterHub

Community

2015

2019

Undisclosed

RiseUp

Egypt

6

Menabytes

Media

2017

2019

Undisclosed

RiseUp

Egypt

7

Mobisol

Off-grid energy

2011

2019

Undisclosed

Engie

Kenya

8

PayFast

Fintech

2007

2019

Undisclosed

DPO Group

South Africa

9

Paystack

Fintech

2015

2020

Over $200m

Stripe

Nigeria

10

iHub

Innovation Hub

2010

2019

Undisclosed

CcHub

Kenya

11

Surf Kenya

Wi-Fi

2015

2019

Undisclosed

BRCK

Kenya

12

Haltons

Healthcare

2013

2019

$5 million

mPharma

Kenya

13

Amplify

Fintechs

2016

2019

Undisclosed

OneFi

Nigeria

14

OLX Africa

Online Classifieds

2012

2019

Undisclosed

Jiji

Nigeria

15

Konga

Ecommerce

2012

2018

$10m (Reportedly)

Zinox

Nigeria

16

Kngine

AI

2008

2018

Undisclosed

Samsung Electronics

Egypt

17

QuickHelp

AI (chatbot)

2015

2018

Undisclosed

1001 Squared

Nigeria

18

Cape Networks

SaaS

2013

2018

Undisclosed

HP

South Africa

19

orderTalk

Foodtech

1998

2018

Undisclosed

Uber Eats

South Africa

20

TopCheck

Ecommerce

2015

2018

Undislosed

Silvertree

Nigeria

21

Careem

E-hailing

2012

2020

$3.1 Billion

Uber

Egypt

*Select African startups acquired between 2017 and 2020. Statistics are not exhaustive of all acquisitions.

Long Term Friendship With Investors Almost Always Defeats Short Term Desperation For VC Funding

Paystack’s acquisition is remarkable in that it is one of the few African startups where the investor became the buyer. In looking to build a startup therefore, getting the right investors has, again, been confirmed as the single most important thing that will determine the success of the startup in the long run.

“When we invest in startups, we’re not trying to tie them up with complicated strategic investments,” Patrick Collison, Stripe’s co-founder and CEO said. “We try to understand the broader ecosystem, and keep our eyes pointed outwards and see where we can help.”

Therefore, while there may be pressing need to raise funds now, it is equally important to look at what the startup’s relationship with its investors will look like, say, 20 years from now.

Co-Founding With Less Squabbles

In as much as it is good to be in a hurry founding startups and bridging skills gap on the team, it is important to be mindful of who makes up the starting team.

“I first met my co-founder, Shola Akinlade, back in 2002,” said Olubi, “we hit it off at a software exhibition in my first year of university and we’ve been friends ever since. We’ve been working together, on and off, for more than a decade now. While Shola was consulting for a bank, he stumbled onto an easy way of doing recurring billing. Knowing my background and interests, he came to me and said: ‘Let’s start a company together. I want you to be a part of this with me.”

In essence, business acumen with a deeper touch of friendship may help take the startup project far.

lessons from Paystack acquisition lessons from Paystack acquisition lessons from Paystack acquisition lessons from Paystack acquisitionlessons from Paystack acquisition lessons from Paystack acquisition lessons from Paystack acquisition

A Look At What Paystack Does

Founded in 2015, Paystack, based out of Lagos, Nigeria provides a quick way to integrate payments services into an online or offline transaction by way of an application-programming interface (API).

The company currently has around 60,000 customers, including small businesses, larger corporates, fintechs, educational institutions and online betting companies, and the plan will be for it to continue operating independently, the companies said.

“Back in 2007,” Olubi said, “when I was working for another company, the internet was still quite inaccessible in Nigeria, outside of workplaces and cyber cafes. People relied on their mobile phones, but it wasn’t easy to top up airtime. We were working on a solution, and created a wallet system where customers could prepay and then send a text message when they wanted more airtime.”

“I thought: ‘If people have all this money stored with us, why don’t we let them spend it all over the internet?’ I built an API around that idea and found myself in the world of online payments. Eventually, I left that company and went on to do other things, but the seed was already sown in my mind for what would later become Paystack,” he adds.

Paystack’s acquisition is the biggest acquisition to date to come out of Nigeria, as well as Stripe’s biggest acquisition to date anywhere in the world.

“There is enormous opportunity,” said Collison. “In absolute numbers, Africa may be smaller right now than other regions, but online commerce will grow about 30% every year. And even with wider global declines, online shoppers are growing twice as fast. Stripe thinks on a longer time horizon than others because we are an infrastructure company. We are thinking of what the world will look like in 2040–2050.”

Charles Rapulu Udoh

Charles Rapulu Udoh is a Lagos-based lawyer who has advised startups across Africa on issues such as startup funding (Venture Capital, Debt financing, private equity, angel investing etc), taxation, strategies, etc. He also has special focus on the protection of business or brands’ intellectual property rights ( such as trademark, patent or design) across Africa and other foreign jurisdictions. He is well versed on issues of ESG (sustainability), media and entertainment law, corporate finance and governance. He is also an award-winning writer